Video: Cambridge Forum discussion on the U.S. and globalization

The Cambridge Forum hosted a videotaped mini-conference on the impact of global engagement on the U.S. and world economies on April 16. Speakers and topics included University of Massachusetts Amherst economic professor Robert Pollin on the “Globalization of Labor: Is a Race To the Bottom Inevitable?”; Economic Policy Institute Director of Trade and Manufacturing Policy Research, Robert Scott, on the “Globalization of Capital: The Rise of the Multinationals”; editor-at-large of The American Prospect and Washington Post columnist Harold Meyerson on the “Globalization of Markets: Do Corporations Need American Consumers?”; and Harvard Kennedy School of Government Professor of International Political Economy Dani Rodrik, who delivered the keynote address on his book, The Globalization Paradox (New York: W.W. Norton & Company, Inc.).

Each participant delivered brief remarks and engaged in wide-ranging question-and-answer sessions with the audience that were moderated by Robert Kuttner, co-founder of The American Prospect (Note: Kuttner is an EPI co-founder and board member). You can watch videos of all four speakers below:

Paging the congressional ophthalmologist

Sometimes it all seems to come together in a perfect storm of bewildering congressional myopia. This seems like one of those times.

This weekend, as many as 236,300 Americans without work will lose their unemployment insurance as a consequence of the “compromise” that Congress passed in February to save the payroll tax cut and UI extension. This is on top of the estimated 173,000 of the jobless who already lost their benefits this year. Some will inevitably argue that this is a good thing because extending benefits keeps people from taking available jobs. This is a wildly deceptive claim. The research shows that in some cases, the availability of unemployment insurance allows people greater flexibility to find jobs that better match their skills, but it’s not causing anyone to give up work entirely. In fact, unemployment insurance keeps discouraged job seekers from giving up their search for work, and adds a meager source of income to those individuals who are the most likely to spend their income and bolster overall aggregate demand.

The real problem is that there simply are not enough available jobs. Yet, instead of strengthening programs that help these and other people still struggling in the wake of the Great Recession, the Republican-controlled House voted yesterday to slash $310 billion in funding for such programs to avoid the previously agreed-upon cuts to the defense budget. What’s perhaps most shocking about this vote is that it comes despite the fact that an overwhelming majority of Americans—both Democrats and Republicans—favors reductions in defense spending over cuts to other domestic programs.

Cutting important social protections and reducing assistance to people in need is only going to push more Americans into poverty. But in the cruelest of ironies, some members of Congress were not content with shooting America in the foot; they voted to blind her as well. On Wednesday night, House Republicans voted to defund the Census Bureau’s American Community Survey, an incredibly powerful source of data for examining state and local economic trends, and one of the primary tools that the government uses to track poverty!

Some might argue that all of this constitutes the House’s attempt to commit the crime and then hide the evidence. I’ll give them the benefit of the doubt that it is just plain short-sightedness.

Larry Summers shrewdly reframes tax simplification

Last week, economists Martin Feldstein and Larry Summers sparred over tax reform on a panel discussion hosted by the Brookings Institution’s Hamilton Project. It is widely agreed that Washington is overdue for and likely headed toward comprehensive tax reform in the next few years. Any compromise on a long-term deficit reduction package will necessitate more revenue and a quarter-century has passed since the last major scrubbing of the tax code (though the Tax Reform Act of 1986’s revenue- and distributional-neutrality makes it an inappropriate benchmark for reform). Most of the reform proposals have focused on broadening the tax base—i.e., eliminating or curbing tax expenditures—rather than raising marginal tax rates to increase revenue. Tax reform is also typically couched in the objectives of simplifying the tax code, reducing economic distortions, and creating a “pro-growth” tax code.

Summers raised an excellent point about the tax reform discourse, particularly the way tax simplification is spun by many advocates. Simplifying the tax code is often falsely equated with reducing the number and scale of marginal tax rates. The House Republican budget, for instance, proposed consolidating the income tax to two brackets—of just 10 and 25 percent—as the cornerstone of “simplifying the tax code and promoting job creation and economic growth.” But in the age of tax return software, Summers argued that tax rates don’t add to complexity; the complicating factor is calculating taxable income. Even before TurboTax, citizens managed to navigate a much longer schedule of marginal tax rates; the tax code had at any time between 24 and 26 marginal tax rates between World War II and 1978. The tax code was also much more progressive, particularly at the top of the income distribution, and income growth was evenly shared over this period. At present, compressing the number of marginal tax rates (currently at six) would only further decouple the contours of the tax code from the increasingly uneven distribution of income gains.

Reform is often framed in terms of broadening the tax base and simplifying the code in tandem, but Summers noted the two are often contradictory objectives. Base broadening inherently increases the amount of taxable economic activity, which in some circumstances can actually make the tax code more complex. Summers gave the example of repealing the exclusion on owner-occupied home sales from capital gains taxation, which would broaden the tax base and raise revenue but unquestionably increase complexity for many filers. Summers downplayed the need for simplification—at least as it’s often thought of—in this tradeoff, and instead endorsed base broadening in ways that increase revenue and the perception of tax fairness.

The complex nature of the tax code favors—both in effect and appearance—those with numerous financial planners and accountants, including dozens of Fortune 500 companies paying nothing in taxes. The tax code needs to be cleaned in ways that inhibit tax gaming and avoidance—best accomplished by reducing tax loopholes that allow for income shifting, such as the preferential rates on capital gains and dividends or the tax deferral for U.S.-multinationals’ foreign source income. That largely amounts to base broadening. Flattening the schedule of marginal income tax rates, on the other hand, would not improve tax compliance or simplify the tax code but would markedly reduce both tax fairness and revenue. When push comes to shove, much of what is peddled as “tax simplification” is nothing but an attempt to further undermine tax progressivity and reduce effective tax rates for upper-income households; doing so would amount to a tax cut, not tax reform.

Senate health committee hearing stresses importance of paid sick time

As my colleague, Ross Eisenbrey, pointed out earlier, the Senate Committee on Health, Education, Labor and Pensions held a very important hearing today (in honor of the upcoming Mother’s Day holiday this weekend) looking at the balance between work and family. This work/family balance has become one of the most ubiquitous sources of economic stress for millions of American families.

One of the important policy proposals covered at the hearing was providing a minimum number of paid sick days to all workers. As Judith Lichtman of the National Partnership for Women and Families noted during the hearing, 40 million workers have no paid sick time to care for themselves or family members when they get sick. Most of the evidence presented at the hearing in favor of providing this important policy was compelling, and it should be clear by now that paid sick time is essential for working families’ economic security. The personal testimony of Kimberley Ortiz about her lack of job security and the penalties she faced at work when she needed to take care of her sick son was particularly compelling and powerful.

In the Senate hearing, Juanita Phillips, Director of Human Resources of Intuitive Research and Technology, spoke about the flexibility her company provides to her workers. She attributes these characteristics—e.g. flexible work hours, paid time off, parental benefits (including short term disability)—to why her company is rated the country’s No. 2 best small business to work for by the Great Place to Work Institute.

Given this, it’s surprising that she argues against the Health Families Act. She claims her company will be punished for already doing the right thing. As an economist, that argument simply makes no sense. To her company, the law is what we economists call a “nonbinding constraint.” They currently provide 15 days of paid time off to new employees for use immediately, and 20 days of paid time off at three years of service. The bill proposes only 7 days.

It doesn’t add up. The one thing Phillips said that could explain her company’s position, is their concern about losing their competitive edge to recruit and retain the best talent. So, she admits the policy is a good one, but doesn’t want to encourage others to engage in it as well. Let’s just say that keeping millions of American families stressed so that a couple of high-road companies get a better pool of resumes when they offer job openings seems like a bad trade-off to me.

This issue is too important to our working families—particularly those at the middle and low end of the wage scale. Furthermore, in the context of similar legislation that was passed in Connecticut, the bill would be of very little cost to businesses, even including those businesses that are not already in compliance with the law.

Organized business’s knee-jerk opposition to paid sick days legislation

The Senate Committee on Health, Education, Labor, and Pensions is holding its Mother’s Day hearing today, and the main subject is paid sick leave, something every working mother needs. Sen. Tom Harkin (D-Iowa) and Rep. Rosa DeLauro (D-Conn.) have introduced a bill, the Healthy Families Act (S. 984/H.R. 1876), to mandate that every employee receive at least seven days of paid time off for illness each year. Everywhere in the civilized world, employees have the right to at least some minimum amount of paid leave when they or their children are sick or when they have to see a doctor—everywhere except in the United States.

The organized U.S. business community—represented by the Washington lobbyists and dozens of giant trade associations—fiercely opposes giving American workers this right.

Why? Because business owners don’t want to be told what to do by anybody, least of all by the government. They consider themselves entitled to force employees to choose between working while sick, taking leave without pay (if the employees are lucky enough to have the right to take unpaid leave), or being fired.

At this morning’s hearing, the business community was represented by the Society for Human Resources Management, which reflexively takes the position that workers should not have legal rights; they should not, for example, have the legal right not to be fired without just cause, they should not have the right to a minimum wage, they should not have the right to unpaid leave to care for family members, they should not have the legal right to advance notice that their office, store or factory will be shut down, etc. The SHRM position is that wages, benefits, and protections should be left to the whim of the employer, or in fancier terms, to market forces.

As usual, the SHRM witness is testifying this morning that her business treats its employees well, giving its employees with three years or more of service 20 days of paid leave. The implication is that left alone, businesses will treat employees as well as they can afford to, and everything will be for the best.

But this benign view is not true. Absent legislation, businesses will treat employees only as well as they want to, even if they can afford to do much more. Even businesses whose CEOs are paid millions of dollars a year can deny all or most of their workers any paid sick leave at all. This problem is so widespread that about 40 percent of the private-sector workforce has no right to even a single day of paid sick leave. That’s 40 million people—mostly low-wage workers who are barely scraping by—who go unpaid if they get sick or if they have to take time off to care for a sick family member.

The SHRM witness argues that a mandate is “inflexible,” and that’s true. It should be inflexible; the whole point is to guarantee a basic, minimum right to workers—most of whom are women—that they need very badly. Nothing would prevent a business from doing more, as the SHRM witness’ business already does.

SHRM’s alternative arguments against the paid sick leave legislation are altogether astonishing. SHRM’s witness argues that providing generous benefits is a competitive advantage to her company that would be lost if every business were compelled by law to provide them, ignoring that the bill’s mandate is for only seven days of paid leave, rather than the 20 days her business provides, leaving plenty of competitive advantage.

“We provide generous paid leave so that we can continue to be an employer of choice for employees and applicants in our area. What we do not want is a government-imposed paid leave mandate to take away our competitive edge over other employers.”

And finally, she argues that it is somehow degrading to be told what to do by the government:

“Organizations such as ours that are already extremely successful with flexible workplace outcomes should not be brought down to the mediocre level that regulatory approaches would be trying to get not-so-well-run companies up to achieving.”

The silliness of these arguments is pretty good evidence that the business community has no good reason (no economic reason) to oppose the Healthy Families Act. Their opposition is ideological: They own the businesses, and no one has the right to tell them (the 1 percent) how to treat their workers—not even a government of the people, by the people, and for the people.

Grasping at Chinese straws

The Commerce Department released another depressing report on the U.S. trade deficit this morning, our monthly reminder of the huge gap between globalization’s economic reality and American economic policymaking.

In March, we bought about $52 billion (28 percent) more from the rest of the world than we sold. From first quarter 2011 to first quarter 2012, the deficit on goods and services rose almost 8 percent, with China representing almost two-thirds of our non-oil deficit with the rest of the world.

Yet, over the past year or so, a drumbeat of analysis in the establishment business press has been telling us to stop worrying; our chronic trade imbalance with China will soon disappear. New York Times columnist Eduardo Porter last week summed up the happy scenario: Chinese wages and transpacific transportation costs are rising and the Chinese are allowing their currency to appreciate. The implication is that rather than exerting unpleasant political pressure on China, we should trust in the natural workings of the market and the good common sense of the Chinese leaders who “appear to understand the need for change.”

Don’t hold your breath.

Porter is correct that wages are rising in China faster than they are in the United States. But to get a perspective, check out the Bureau of Labor Statistics’ numbers on international labor costs in manufacturing, where the latest data—for 2008—is that Chinese manufacturing costs are a little over 4 percent of U.S. levels. Yes, they probably have risen since then, but the gap is still immense and will clearly not be closed anytime soon.

Moreover, the narrowing of the gap may have as much to do with U.S. workers getting less as Chinese workers getting more. The corporate poster boy for looking at the bright side is General Electric, which has moved some production of a few heavy appliances back to the U.S. from China. What the poster leaves out is that GE workers who used to make $22 an hour are now making $13.

It is also true that rising fuel costs are making it more expensive to import large, heavy products from across the Pacific. But that hardly means that production will move back to the U.S. Thanks to the North American Free Trade Agreement, multinational producers of big appliances and autos and parts who find importing from China too expensive, are moving to Mexico where labor costs are 18 percent of what they’d pay in the U.S.

Finally, Porter writes that the Chinese strategy of manipulating their currency to keep their exports cheap and imports expensive “may be turning the corner.” He notes that the Chinese, while they don’t want to appear caving to American pressure, have quietly allowed the renminbi to appreciate 40 percent against the dollar since 2005.

Just so. And over that time our trade deficit with China has grown by over 45 percent, suggesting how large China’s comparative advantage in trade has become. Moreover, despite the endless parade of American officials to Beijing pleading for more currency appreciation, the Chinese apparently think they’ve already done enough. Porter himself quotes China’s premier Wen Jiabao to the effect that the dollar-renminbi now may “have reached equilibrium level.”

Thus, there is little evidence that either the market or the Chinese leadership intend to rescue the U.S. from its trade quagmire.

Unfortunately, neither is there evidence that American leaders—from either party—intend to take responsibility for doing it themselves. Not only do they have no strategy to deal with the trade deficit, but President Obama and congressional Republicans are busily preparing for yet another of the so-called free trade agreements—this one to a group of countries around the Pacific rim—that have allowed our multinationals to off-shore production for the American consumer for over three-and-a-half decades.

But the market will not be denied; eventually we will balance our trading account. So, in the absence of a proactive policy, GE will be the model—the relentless lowering of American wages and living standards until the gap with workers in China and Mexico is closed.

Andrew Biggs is at it again

Comic Demetri Martin has this advice: “Only people in glass houses should throw stones, provided they are trapped in the house with a stone.”

Feeling trapped might explain the American Enterprise Institute’s Andrew Biggs’ penchant for stone throwing, such as accusing public pensions of projecting rosy rates of return (in Biggs’ view, anything higher than Treasury bond yields) despite the fact that he once hyped Social Security private accounts with promises of riches galore.

His latest: charging the National Institute of Retirement Security with advocating stone throwing—or at least window breaking—in order to stimulate the economy (apologies for the colliding metaphors).

Specifically, Biggs says NIRS ignores the cost to taxpayers in its research on the economic impact of public pensions, likening this to advocating window breaking as a way to create jobs for glaziers. Aside from the fact that the report in question repeatedly cites taxpayer costs, author Ilana Boivie is straightforward about the fact that her study measures the gross (not net) economic impact, as even Biggs eventually acknowledges. Thus, the economic stimulus from pensions can be compared to other forms of saving or spending without being limited to a specific counter-factual.

Biggs seems to think the relevant comparison should be with cutting public pension benefits and refunding the cost to taxpayers, as if they could be cut without damaging employee recruitment or retention—and, by extension, public services. He also cites another potential counter-factual: What would happen to the economy if state and local governments switched from traditional defined benefit pensions to 401(k)-style defined contribution plans? In theory, contributions to retirement plans should increase to make up for these plans’ inefficiency due to high fees and a lack of risk pooling. In practice, 401(k) contributions tend to be grossly inadequate, since anxiety, it appears, is not a good motivator. So such a switch would more likely lead to a decline in saving, an increase in consumption spending, and a short-run boost to our economy, albeit for all the wrong reasons (in other words, it would be rather like breaking windows to boost the economy). In the long run, you’d have to factor in an upward redistribution of wealth to high-income households who benefit the most from these accounts and whose higher saving rate would be a drag on our demand-constrained economy.

Perhaps Edward Hicks' "Peaceable Kingdom" is the kind of earthly paradise Andrew Biggs envisions.

You can see how it gets complicated. Not for Biggs, though. For him, increasing savings in private accounts would lead to an earthly paradise, making Americans “not only richer, but also happier, healthier, more familial, smarter, and more active citizens.”

He said this back in the day when he was promoting President George W. Bush’s plan to partially privatize Social Security. Of course, Biggs took into account the cost in the form of reduced guaranteed benefits…

Actually, he didn’t. Which gets back to Biggs’ habit of accusing others of sins he’s committed. Maybe he feels trapped by Dean Baker in a crystal palace of Social Security privatization, and this is the only way he can think of getting out?

Price of a diploma: Class of 2012 faces tough job market, rising costs, and increasing debt

There was a great article in Monday’s Wall Street Journal that discussed the tough job market the Class of 2012 is facing. Many of these new graduates will be competing with the graduating classes of 2011 and 2010 just to get on the bottom rungs of the career ladder. While it’s well-documented that graduating into a depressed labor market lowers lifetime earnings potential on average, today’s young graduates have additional hurdles to worry about: rising higher education costs and crippling student debt.

At EPI, we, with economist Heidi Shierholz, recently released an analysis of the labor market for recent high school and college graduates. The results are predictably grim, with unemployment rates for both sets of graduates spiking at the beginning of the Great Recession and falling very slowly in the recovery.

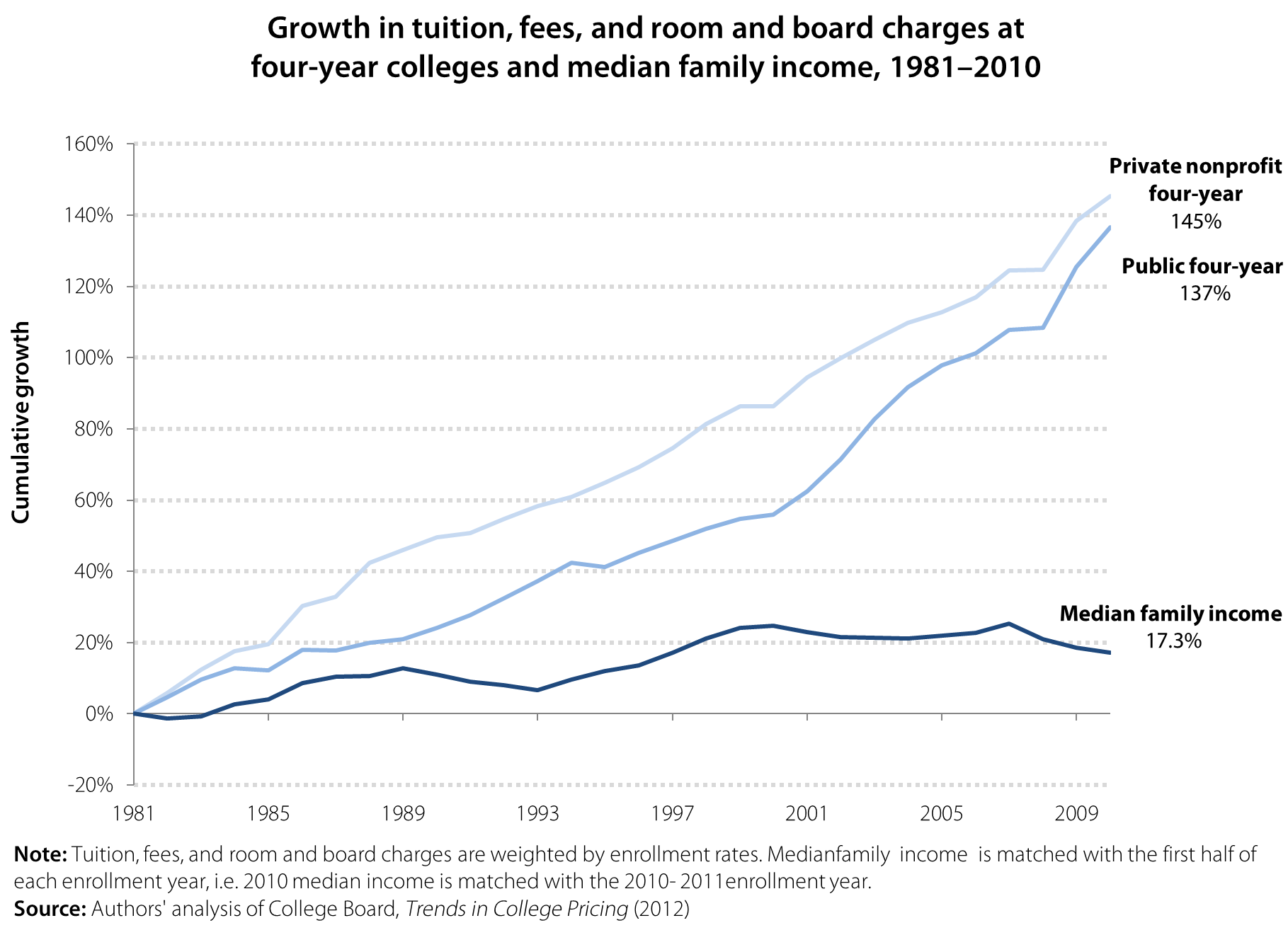

The report also highlighted the rising cost of obtaining a college degree. The figure below shows that the cost of higher education has been rising faster than family incomes for decades, making it harder for families to pay for college. From the 1981–82 enrollment year to the 2010–11 enrollment year, the cost of a four-year education increased 145 percent for private school and 137 percent for public school. Median family income only increased 17.3 percent from 1981–2010, far below the increases in the cost of education, leaving families and students unable to pay for most colleges and universities in full.

Unsurprisingly, a large majority of students and recent graduates take on debt to pay for college. Two-thirds of recent college graduates have student loans, and trends indicate that the number of student loans is increasing. Between 1993 and 2008, average student debt for graduating seniors increased 68 percent, from $14,410 to $24,238. Average debt for graduating seniors at public universities was $21,105 in 2008, and average debt for graduating seniors at private non-profit universities was $28,888 (authors’ analysis of Project on Student Debt 2010). In taking on these loans, students are taking a risk and hoping that they will be able to quickly secure work to begin paying them off after graduation. In recent years, and through no fault of their own, a growing number of graduates have been on the wrong side of this risk, with harsh consequences. Although most student loans have a grace period of six months before repayment begins, recent graduates who do not find a stable source of income may be forced to postpone payment though deferment or forbearance, miss a payment, or worst of all, default altogether on their loans. Deferment and forbearance are short-term fixes, however, and ultimately increase the amount borrowers owe once each period ends. Missed payments and default can ruin young workers’ credit scores and set them back years when it comes to saving for a house or a car.

Even worse, these young workers do not have a strong safety net on which to rely during the volatile job-seeking process.

Young workers are often ineligible for unemployment insurance, for example, because they must first meet state wage and work minimums during an established reference period—a reference period during which they are often in school and not working. Many new graduates are likely turn to their families for assistance. In 2011, 54.6 percent of 18- to 24-year-olds were living with their parents, an increase of 3.4 percentage points since 2007. This option is not, obviously, available to all young graduates. In short, young workers are being squeezed from multiple angles and their plight constitutes yet another instance of how damaging our tolerance of an underperforming economy truly is.

Additional findings and more analysis on the labor market facing young high school and college graduates can be found in our report, The Class of 2012: Labor market for young graduates remains grim.

Depressing graph of the day: The long-term unemployed

The Pew Fiscal Analysis Initiative has released an addendum to its 2010 report A Year or More: The High Cost of Long-Term Unemployment, and the update isn’t pretty. Using data from the Bureau of Labor Statistics’ Current Population Survey, Pew’s addendum finds that 29.5 percent of unemployed Americans in the first quarter of 2012 have been jobless for a year or more. That means 3.9 million working-age Americans haven’t been able to find a job in 12-plus months.

In 2008, during the first quarter of the Great Recession, 9.5 percent of the unemployed had been jobless for at least a year. While this percentage of the long-term unemployed peaked at 31.8 percent in the third quarter of 2011, it’s still very high and remains more than three times greater than at this point four years ago. Note also that BLS defines long-term unemployment as someone who has been unemployed for more than half a year (27 weeks or more). By this measure, 41.3 percent of the jobless still qualify as long-term unemployed.

Some other findings from the Pew analysis:

- Age: Older workers are less likely to lose their jobs, but much more likely to be jobless for a year or more once they do (see Figure 3 in the addendum).

- Education: Workers with higher levels of education are less likely to lose their jobs, but they’re no better off once they do as long-term joblessness is fairly even across all education levels (see Figure 5).

- Industry: No industry or occupation has gone unscathed due to long-term unemployment (see Table 3).

Continued high levels of long-term unemployment have a damaging impact on the economic situations of both individuals and families, and more broadly, on the economy as a whole. As EPI has documented before, the outcome of such long-term joblessness is “scarring,” which carries severe and long-lasting consequences for our economy and society.

What we should talk about when we talk about Social Security

Love?

That’s the original word in the Raymond Carver short story collection paraphrased in this blog title, and in a perfect world, that’s all we’d need to say: Americans love Social Security because it takes care of the people they love.

But this is Washington, so that won’t cut it. Fortunately, our friends at Social Security Works have hired some smart people to think about why we’re losing the messaging war on Social Security, despite the program’s popularity and the fact that transparently partisan attacks (“Ponzi scheme”) haven’t found much traction.

What has gotten traction: a decades-long and lavishly-funded campaign to convince younger workers that Social Security won’t be there when they retire, which opens the door to all sorts of shenanigans. Many Washington insiders, from across the political spectrum, have bought into the idea that Social Security is on an unsustainable course, and a willingness to slash benefits has become a “badge of fiscal seriousness” inside the Beltway, as Paul Krugman has noted.

Once the myth that Social Security is in trouble has taken root, attempts to dispel it with facts can inadvertently reinforce it, because the issue becomes technical and confusing, and people tend to assume that if you’re arguing about a problem, then it must exist. (If-there’s-smoke-there-must-be-fire logic isn’t always wrong, by the way: The Federal Reserve’s repeated attempts to pooh-pooh the existence of housing and stock bubbles should have put people on alert long before the bubbles burst in 2007.)

The good news, as John Neffinger of KNP Communications explained at a recent meeting of Social Security advocates, is that positive messages about Social Security can stick if presented the right way and in the right order.

Here are some DOs and DON’Ts, according to Neffinger:

- DON’T fight on their terrain (“Social Security isn’t going broke”).

- DO focus on the fact that Social Security is the only secure pillar of our retirement system (“If the middle class can’t count on Social Security in their retirement years, what can it count on? Not home equity, or 401(k)s or IRAs…”). In this vein, push for strengthening the program, as Michael Hiltzik does in this recent Los Angeles Times article.

- DO explain attacks on Social Security as attempts to dismantle the system for private gain (“Wall Street stands to make billions from managing more private accounts”) or political ideology (“They take their marching orders from someone who wants to shrink government to the size that they can drown it in a bathtub”).

- DO address the solvency issue by showing that simple adjustments can maintain the system (“Scrap the cap, so everyone pays the same percentage of their income in payroll tax”).

- But DON’T lead with the last two points, or you risk sounding partisan and reinforcing the myth that Social Security is in crisis.

The beauty of this framework, at least in theory, is that it avoids talking points that can backfire, like accusing Congress of raiding Social Security. It also sidesteps confusing topics like the trust fund that are hard to explain in a sound bite. Read more