What to watch on jobs day: Expected future impact of COVID-19

As COVID-19—commonly known as the coronavirus—continues to spread throughout the world, it is likely to have a direct impact on the United States through the health and well-being of our population. It is also likely to have an impact on economic activity, as workers stop working to care for themselves or their families, and people generally reduce social spending. I’ll be watching this in tomorrow’s job report from the Bureau of Labor Statistics, and keeping an eye on it in the coming months. The first order of business, however, is to make sure that workers can follow the Centers for Disease Control and Prevention (CDC)’s recommendations to stay home and seek medical care—if they are lucky enough to have paid sick days and health insurance. While there are still very few reported cases in the United States, it is expected to spread and the effects may be far-reaching.

In terms of the economy, there has already been an impact on the manufacturing sector as inputs from China are delayed because of temporary factory closures. The Federal Reserve has cut interest rates in expectation of further economic disruptions. Many employers are making contingencies for workers to telecommute rather than risk illness. Unfortunately, this isn’t an option for millions of workers in direct service professions across the economy. Another likely side effect of the pandemic is a pull-back on social consumption. Either because people become sick themselves or are avoiding public spaces, there will likely be a drop in certain types of spending across the economy.Read more

Low-wage workers saw the biggest wage growth in states that increased their minimum wage between 2018 and 2019

Twenty-three states and the District of Columbia raised their minimum wage in 2019 through legislation, referendum, or because the minimum wage was indexed to inflation in those states. Low-wage workers in these states saw much faster wage growth than low-wage workers in states that did not increase their minimum wage between 2018 and 2019, as shown in EPI’s latest State of Working America Wages report. This blog post dives a bit deeper by dispelling some tempting explanations for what might be happening, such as stronger across-the-board wage growth in those states (didn’t happen) or employment losses (not borne out in the data).

Figure A shows in green the states with minimum wage increases that occurred through legislation or referendum in 2019, while states in blue had automatic increases resulting from indexing the minimum wage to inflation. Workers in states that increased their minimum wage between 2018 and 2019 account for about 55% of the U.S. workforce. The nominal minimum wage increases ranged from $0.05 (0.5%) in Alaska to $1.00 (9.1%−10.0%) in California, Massachusetts, and Maine.

The minimum wage increased in 23 states and the District of Columbia in 2019: States with minimum wage increases in 2019, by type of increase

| State | Abbreviation | Category |

|---|---|---|

| Alaska | AK | Indexed |

| Alabama | AL | No change |

| Arkansas | AR | Legislated or ballot measure |

| Arizona | AZ | Legislated or ballot measure |

| California | CA | Legislated or ballot measure |

| Colorado | CO | Legislated or ballot measure |

| Connecticut | CT | Legislated or ballot measure |

| District of Columbia | DC | Legislated or ballot measure |

| Delaware | DE | Legislated or ballot measure |

| Florida | FL | Indexed |

| Georgia | GA | No change |

| Hawaii | HI | No change |

| Iowa | IA | No change |

| Idaho | ID | No change |

| Illinois | IL | No change |

| Indiana | IN | No change |

| Kansas | KS | No change |

| Kentucky | KY | No change |

| Louisiana | LA | No change |

| Massachusetts | MA | Legislated or ballot measure |

| Maryland | MD | Legislated or ballot measure |

| Maine | ME | Legislated or ballot measure |

| Michigan | MI | Legislated or ballot measure |

| Minnesota | MN | Indexed |

| Missouri | MO | Legislated or ballot measure |

| Mississippi | MS | No change |

| Montana | MT | Indexed |

| North Carolina | NC | No change |

| North Dakota | ND | No change |

| Nebraska | NE | No change |

| New Hampshire | NH | No change |

| New Jersey | NJ | Legislated or ballot measure |

| New Mexico | NM | No change |

| Nevada | NV | No change |

| New York | NY | Legislated or ballot measure |

| Ohio | OH | Indexed |

| Oklahoma | OK | No change |

| Oregon | OR | Legislated or ballot measure |

| Pennsylvania | PA | No change |

| Rhode Island | RI | Legislated or ballot measure |

| South Carolina | SC | No change |

| South Dakota | SD | Indexed |

| Tennessee | TN | No change |

| Texas | TX | No change |

| Utah | UT | No change |

| Virginia | VA | No change |

| Vermont | VT | Indexed |

| Washington | WA | Legislated or ballot measure |

| Wisconsin | WI | No change |

| West Virginia | WV | No change |

| Wyoming | WY | No change |

Notes: Minimum wage increases passed through either legislation or ballot measure took effect on January 1, 2019, in Arkansas, Arizona, California, Colorado, Delaware, Maine, Massachusetts, Michigan, Missouri, New York, Rhode Island, and Washington. Alaska, Florida, Minnesota, Montana, New Jersey, Ohio, South Dakota, and Vermont increased their minimum wages in 2019 because of indexing to inflation. New Jersey, Oregon, and Washington, D.C., legislated minimum wage increases that took effect on July 1, 2019. Note that Connecticut legislated a minimum wage increase that took effect on October 1, 2019. This sample considers all changes after January 2018 and before December 2019; therefore, Maryland is included even though the legislated minimum wage increase for Maryland took effect on July 1, 2018. Note that after indexing to inflation on January 1, 2019, New Jersey legislated a minimum wage increase on July 1, 2019; therefore, New Jersey appears twice in these lists.

Source: EPI analysis of state minimum wage laws. See EPI’s minimum wage tracker for the most current state-level minimum wage information.

Figure B compares 10th-percentile wage growth in states with minimum wage increases compared with those without increases. Growth at the 10th percentile in states without minimum wage increases was much slower (0.9%) than in states with any kind of minimum wage increase (4.1%). This result holds true for both men and women. The 10th-percentile men’s wage grew 3.6% in states with minimum wage increases, compared with 0.7% growth in states without any minimum wage increases, while women’s 10th-percentile wages grew 2.8% in states with minimum wage increases and 1.4% in states without.

Wage growth at the bottom was strongest in states with minimum wage increases in 2019: 10th-percentile wage growth, by presence of 2019 state minimum wage increase and by gender, 2018–2019

| States with minimum wage increases | States without minimum wage increases | |

|---|---|---|

| Overall | 4.1% | 0.9% |

| Men | 3.6% | 0.7% |

| Women | 2.8% | 1.4% |

Notes: Minimum wage increases passed through either legislation or ballot measure took effect on January 1, 2019, in Arkansas, Arizona, California, Colorado, Delaware, Maine, Massachusetts, Michigan, Missouri, New York, Rhode Island, and Washington. Alaska, Florida, Minnesota, Montana, New Jersey, Ohio, South Dakota, and Vermont increased their minimum wages in 2019 because of indexing to inflation. New Jersey, Oregon, and Washington, D.C., legislated minimum wage increases that took effect on July 1, 2019. Note that Connecticut legislated a minimum wage increase that took effect on October 1, 2019. This sample considers all changes after January 2018 and before December 2019; therefore, Maryland is included even though the legislated minimum wage increase for Maryland took effect on July 1, 2018. Note that after indexing to inflation on January 1, 2019, New Jersey legislated a minimum wage increase on July 1, 2019; therefore, New Jersey appears twice in these lists.

Sources: Author’s analysis of EPI Current Population Survey Extracts, Version 1.0 (2020), https://microdata.epi.org, and EPI analysis of state minimum wage laws. See EPI’s minimum wage tracker for the most current state-level minimum wage information.

Economic policy and COVID-19—Mitigate harm and plan for the future: A list of considerations for policymakers

The direct cost that COVID-19 inflicts on human health is obviously its most important effect on society. But this direct cost can be worsened by flawed economic and policy structures. And the indirect damage the disease causes through economic ripple effects could be large, so policymakers should do everything they can to minimize them.

Past decisions that have weakened our economic policy infrastructure will hamper our response to COVID-19; this is already baked into the cake. But there are some short-run ameliorative actions we can take that might help, and there are long-run policy changes that will aid our response to future epidemics.

In technical economic terms, COVID-19 combines potential supply shocks with sector-specific demand shocks. Basically, supply shocks hamper our ability to produce goods and services, and demand shocks are sharp cutbacks in spending from households, businesses, or governments. Below I provide a list for policymakers of what could/should be considered to deal with some of these.

The supply shocks come from disrupted global value chains, as, for example, Chinese production of inputs used by U.S. manufacturing and construction firms are not delivered on time because Chinese factories have temporarily closed. In countries where schools are shut down for long periods of time, a shock to labor supply can occur as working parents have to stay home to care for kids.

The potential sector-specific demand shock is to businesses where consumption is largely social—done with other people around. Think bars, restaurants, grocery stores, and malls. As people avoid social contact to minimize disease transmission, this leads to less activity in these sectors.

These effects mean it will be hard indeed for policymakers to spare the economy any pain from this.

There’s very little that can be done about the supply-side shocks—particularly in the short run. Demand-side shocks are generally easier to address with policy (in theory—policymakers still often fumble the ball in this regard), but the specific nature of the demand shocks associated with COVID-19 make them slightly harder to address. Simply giving households more money won’t boost consumption much in the sectors likely to be affected—the pullback in consumption is not driven by income constraints, but due to concerns over catching the illness.

EPI President Thea Lee testifies before the House Committee on Ways and Means on U.S.–China Trade and Competition (Video)

On February 26, EPI President Thea Lee testified before the House Committee on Ways and Means on the impact of the imbalanced U.S.–China economic relationship on U.S. jobs, wages, businesses, and long-term growth.

In her testimony, Lee discussed the history of U.S. trade policy toward China, problems with Trump’s “phase one” deal with China, and fundamental flaws in the U.S.–China economic relationship. According to new EPI research, the growing U.S.–China trade deficit was responsible for the loss of 3.7 million U.S. jobs between 2001 and 2018. These job losses are spread across all 50 states and the District of Columbia—and every congressional district in America.

Watch her testimony:

Lack of paid sick days and large numbers of uninsured increase risks of spreading the coronavirus

COVID-19—commonly known as the coronavirus—is now a potential threat for the United States and we all “need to be preparing for significant disruption of our lives,” warned the Centers for Disease Control and Prevention (CDC) this week.

Unfortunately, preparing for the “significant disruption” will be economically unimaginable for one group of Americans—the millions of people in the United States who do not have access to paid sick days or have health insurance with a regular health care provider.

The CDC released very clear instructions to help prevent the spread of respiratory diseases, including staying home when you are sick. Not everyone has that option.

Overall, just under three-quarters (73%) of private-sector workers in the United States have the ability to earn paid sick time at work. And, as shown in Figure A, below, access to paid sick days is vastly unequal. The highest-wage workers are more than three times as likely to have access to paid sick leave as the lowest-paid workers. Whereas 93% of the highest-wage workers had access to paid sick days, only 30% of the lowest-paid workers are able to earn sick days. In this way, access to paid sick days increases with wages among workers, disproportionately denying workers at the bottom this important security. And low-wage workers are more likely to be found in occupations where they have contact with the public—think early care and education workers, home health aides, restaurant workers, and food processors. When workers or their family members are sick, they shouldn’t have to decide between staying home from work to care for themselves or their dependents and paying rent or putting food on the table. But that is the situation our policymakers have put workers in.

Black-white wage gaps are worse today than in 2000

This week, my colleagues hosted a discussion on the policies that the 2020 presidential candidates should focus on in order to help black workers in the economy. One of the challenges that the presidential candidates should discuss is how to reduce the black–white wage gap—which has stubbornly persisted over the last four decades. Black-white wage gaps are large and have gotten worse in the last 20 years.

The latest findings on wage growth as documented in EPI’s State of Working America Wages 2019 report indicate wages in general are slowly improving with the growing economy, but wage inequality has grown and wage gaps have persisted, and in some cases, worsened. In this post, I will highlight the worsening black-white wage gap and look at it from multiple dimensions. Since 2000, by any way it’s measured, the wage gap between black and white workers has grown significantly.

The figure below compares wages for black and white workers over the last 19 years, highlighting the gaps in wages in 2000, the last time the economy was closest to full employment, 2007, the last business cycle peak before the Great Recession, and 2019, the latest data available. Against these benchmarks, I illustrated the growth in the average gap, the gap for low-, middle-, and high-wage workers, the gap for workers with a high school diploma, a college degree, and an advanced degree, and a regression-adjusted wage gap (controlling for age, gender, education, and region).

Black–white wage gaps widen across multiple measures: Black–white wages gaps at different points in the wage distribution, by education, and regression-based, 2000, 2007, and 2019

| 2000 | 2007 | 2019 | |

|---|---|---|---|

| Average | 21.8% | 23.5% | 26.5% |

| 10th percentile | 6.2% | 8.7% | 9.0% |

| Median | 20.8% | 22.3% | 24.4% |

| 95th percentile | 28.0% | 28.3% | 34.7% |

| High school | 15.3% | 17.4% | 18.3% |

| College | 17.2% | 19.2% | 22.5% |

| Advanced degree | 12.5% | 16.7% | 17.6% |

| Regression-based | 10.2% | 12.2% | 14.9% |

Notes: Sample based on all workers ages 16 and older. The xth-percentile wage is the wage at which x% of wage earners earn less and (100-x)% earn more. Educational attainment is based on mutually exclusive categories: e.g., high school is high school only, etc. Similar results are found for those with less than high school or some college. The regression-adjusted black–white wage gap controls for education, age, gender, and region.

Source: Author’s analysis of EPI Current Population Survey Extracts, Version 1.0 (2020), https://microdata.epi.org.

The black–white wage gap is smallest at the bottom of the wage distribution, where the minimum wage serves as a wage floor. The largest black–white wage gap as well as the one with the most growth since the Great Recession, is found at the top of the wage distribution, explained in part by the pulling away of top earners generally as well as continued occupational segregation, the disproportionate likelihood for white workers to occupy positions in the highest-wage professions.

It’s clear from the figure that education is not a panacea for closing these wage gaps. Again, this should not be shocking, as increased equality of educational access—as laudable a goal as it is—has been shown to have only small effects on class-based wage inequality, and racial wealth gaps have been almost entirely unmoved by a narrowing of the black–white college attainment gap, as demonstrated by William Darity Jr. and others.

Black workers can’t simply educate their way out of the gap. Across various levels of education, a significant black–white wage gap remains. Even black workers with an advanced degree experience a significant wage gap compared with their white counterparts. And after controlling for age, gender, education, and region, black workers are paid 14.9% less than white workers.

While the wage gaps differ depending on measure, what is obvious from the trends displayed is that the gaps widened in the full business cycle 2000–2007 and continued to grow in the Great Recession and its aftermath. Even though the black unemployment rate has fallen precipitously over the last several years, wage growth has remained particularly weak for black workers.

As always, it’s important to remember the historical and social contexts for differences in black and white labor market experiences and labor market outcomes (see Razza). Workers’ ability to claim higher wages rests on a host of social, political, and institutional factors outside of their control. The systematic social deprivation and economic disadvantage is maintained and reinforced by those with economic and political power. Furthermore, occupational segregation plays a significant role in these gaps, for both black men and black women. And, black women, in particularly, can face larger wages gaps with white men than the sum of their parts, meaning the black women face a double wage penalty for their race and gender. The trends in black–white wage gaps found here are supported by other important research that shows that black-white wage gaps expanded with rising inequality from 1979 to 2015.

Given a long history of excluding black Americans from social and political institutions that boost wage growth, the stubbornness of racial wage gaps is less surprising. However, the fact that they are getting worse is troubling. The good news is that policy can make a difference.

We see in the figure that the minimum wage keeps the lowest-wage black workers from even lower wages. In states that increased in the minimum wage between 2018 and 2019, low-wage workers saw stronger wage growth than in states that had no increase in their minimum wage in that period. Raising the federal minimum wage would disproportionately benefit black workers because they are overrepresented among low-wage workers and are less likely to live in states or localities that have passed a minimum wage that is higher than the current federal minimum.

Aside from strengthening and enforcing labor standards such as the minimum wage, making it easier for workers to form unions can narrow the black–white wage gap. Black workers are more likely to be in a union than white and get a bigger wage boost to being in a union than white. Therefore, unions can help shrink the black–white wage gap. Related, research has shown that the decline of unionization led to an expansion of the black–white wage gap.

Using all fiscal and monetary policy levers to achieve and maintain high-pressure labor markets can improve relative labor market outcomes for black workers, including participation in the labor force and work hours as well as wage growth. The U.S. certainly saw this stronger across the board growth in the tight labor market of the late 1990s.

In 2019, black wages exceeded their 2000 and 2007 levels across the wage distribution for the first time in this recovery. I’m hopeful that as the economy continues to move toward genuine full employment, black workers will see their wages rise. But it will take more than a couple of years of a full-employment economy to close racial wage gaps and compensate for years of lower wages, lower incomes, and lower wealth.

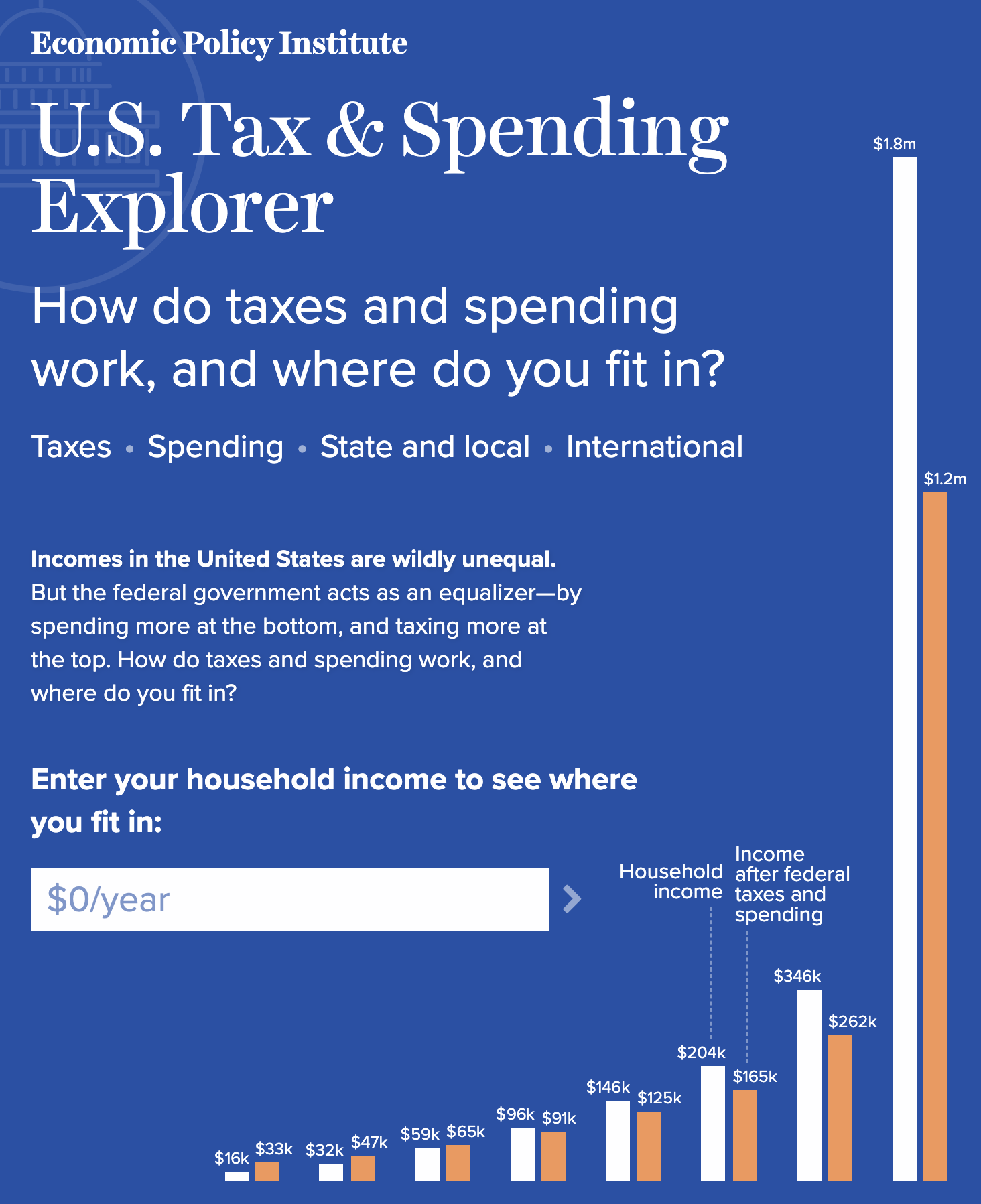

The U.S. federal tax and spending system is the biggest tool to combat inequality, but it could do much more

Last week, we launched the U.S. Tax & Spending Explorer on the EPI website. It’s an interactive web feature designed to shed light on how the government (mostly the federal government) raises and spends money and how changes in taxes and spending over time either increase or decrease income inequality.

There’s enough granular detail in the feature that everybody might have different takeaways from visiting it. But here’s what strikes me looking at this data:

- Together, taxes and spending significantly reduce inequality at any given point in time relative to a world with a much smaller federal footprint. That’s the good news. The bad news is that since 1979 the inequality-reducing effect of taxes and spending hasn’t grown that much—but inequality has grown, a lot. We should use the proven inequality-fighting lever of a larger tax and spending system to combat the inequality that has risen so fast in recent decades.

Medicare4All C-Span discussion sheds light on its impact

Economic Policy Institute’s Director of Research Josh Bivens and American Enterprise Institute’s Jospeh Antos addressed the issue of Medicare for All, and the larger role health care policy is playing in Campaign 2020 on C-Span’s Washington Journal Saturday.

The United States needs movement forward on healthcare that makes it accessible and affordable, said Bivens during the discussion.

“I think there’s a real hunger out there for something for health reform,” he explained. “Health care is something that Americans worry about the most, not just their health but would means for financial security and that worry is well-placed. We have a uniquely dysfunctional health care system.

“We spend on a per capita basis about $10,000 per person, we have some great health systems in the world, number one in terms of health outcomes as France and the Netherlands who spend literally half of what we spend. One of the reasons why a single-payer plan would be expensive is because we still have 27 million uninsured people and 60 million underinsured people. So, yeah, it would be more expensive to give health care to people who need it, but that’s the virtue of a fundamental reform. Keeping costs down by keeping people excluded, seems to me as not the way to go.”

Bivens is the author of a soon-to-be released paper on the impact of fundamental health care reform, including Medicare for All, on wages and job quality.

Sign up here for EPI’s newsletter so you don’t miss the report’s release, or any other essential labor research, analysis and trends from EPI’s research team.

The Trump budget doesn’t spare seniors

President Trump’s proposed 2021 budget claims to help the “most vulnerable populations,” including seniors. But vulnerable older Americans are among those who would be most hurt if this draconian budget were ever enacted.

The budget would slash Medicaid and non-defense discretionary spending, eliminating or drastically shrinking programs targeted at low-income people, including programs benefiting seniors, such as the Low Income Home Energy Assistance Program. At first glance, the administration appears to spare middle-class seniors, a group with high voter turnout that tends to support the president and his party. Despite the president’s hints that Social Security and Medicare will be on the chopping block after the election, the budget would spare retirement benefits (except those for federal employees) and claims to achieve Medicare savings only by eliminating “excessive spending and distortionary payment incentives” while “preserv[ing] benefits and access to care.”

Some Medicare provisions in the president’s budget, such as site-neutral payments across different types of facilities, address genuine problems in how Medicare is administered. But the nearly half trillion in proposed savings from Medicare over 10 years includes provisions that would indirectly affect Medicare beneficiaries’ access to care, such as reducing payments to partially cover unpaid medical bills for Medicare beneficiaries. Since unlimited out-of-pocket expenses are a major cause of bankruptcy for older Americans in poor health, reducing these reimbursements would cause some providers to avoid treating Medicare patients who have expensive conditions and limited resources—and would surely lead to hospital and clinic closures in underserved areas. Middle-class seniors and providers who treat them wouldn’t be spared, since lower-middle-class seniors ineligible for Medicaid are those most likely to spend a high share of their income on health care. The problem of uncompensated care would be compounded by the administration’s attempts to roll back Medicaid expansion under the Affordable Care Act (ACA), which has helped hospitals treating low-income and uninsured patients in expansion states.

Top five Valentine’s Day gifts ideas for U.S. workers: Nothing spells ‘romance’ like a fair wage and quality jobs

That’s why we decided to sum up what we think are the top five Valentine’s Day gifts ideas for working people across the country.

Power through collective action!

Our economy is out of balance. Corporations and CEOs hold too much power and wealth, and working people know it. Workers are mobilizing, organizing, protesting, and striking at a level not seen in decades, and they are winning pay raises and other real change by using their collective voices.

But, the fact is, it is still too difficult for working people to form a union at their workplace when they want to. The law gives employers too much power and puts too many roadblocks in the way of workers trying to organize a union. The Protecting the Right to Organize (PRO) Act will go a long way toward restoring workers’ right to join together to bargain for better wages and working conditions by streamlining the process when workers form a union, ensuring that they are successful in negotiating a first agreement, and holding employers accountable when they violate labor law. The U.S. Senate should join the House of Representatives and pass the PRO Act in order to restore power to working people.

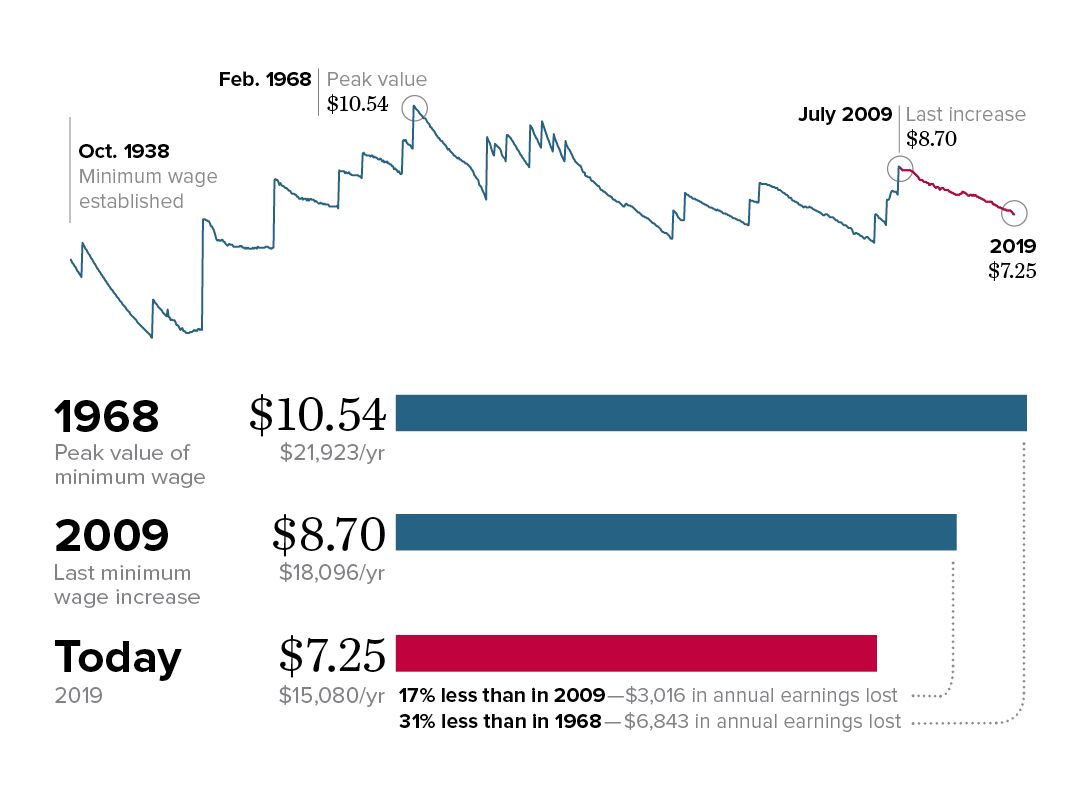

Affording bread…and roses

The real (inflation-adjusted) minimum wage is now roughly 30 percent lower than it was in 1968, and it has been more than 10 years since congress raised the minimum wage—the longest stretch in history. To end this shameful streak, it is incumbent upon the Senate to take up and pass the Raise the Wage Act immediately. Raising the federal minimum wage to $15 by 2025 would lift wages for 33.5 million workers across the country—more than one-fifth of the wage-earning workforce. The increase would boost total annual wages for these low-wage workers by $92.5 billion, lifting annual earnings for the average affected year-round worker by $2,800. Recent survey data have shown that 74% of U.S. workers live paycheck to paycheck. Policymakers should give working people the ability to make ends meet—but also the ability to treat themselves occasionally.

Failure to raise the federal minimum wage has taken thousands of dollars out of the pockets of minimum wage workers: The real value of the minimum wage (adjusted for inflation) is 17% less than 10 years ago and 31% less than in 1968

Note: All values are in June 2019 dollars, adjusted using the CPI-U-RS.

Source: Adapted from Figure C in David Cooper, Elise Gould, and Ben Zipperer, Low-Wage Workers Are Suffering from a Decline in the Real Value of the Federal Minimum Wage, Economic Policy Institute, August 2019).

Source: Adapted from Figure C in David Cooper, Elise Gould, and Ben Zipperer, Low-Wage Workers Are Suffering from a Decline in the Real Value of the Federal Minimum Wage, Economic Policy Institute, August 2019). The figure reflects EPI analysis of historical minimum wage data in the Fair Labor Standards Act and amendments.

Pay workers for their hours worked, or give them their time back

The U.S. Department of Labor announced in September its final overtime rule, which will set the salary threshold under which salaried workers are automatically entitled to overtime pay to $35,568 a year. The rule leaves behind millions of workers who would have received overtime protections under the much stronger rule, published in 2016, that Trump administration chose to abandon. A stronger overtime protection would pay more workers for working more than 40 hours a week, or allow them extra time with their families.

Seven states have already taken steps to raise the overtime threshold, but without further action, it’s estimated that 8.2 million workers who would have benefited from the 2016 rule will be left behind by the Trump administration’s rule, including 3.2 million workers who would have gotten new overtime protections under the 2016 rule and 5.0 million who would have gotten strengthened overtime protections under the 2016 rule. States should follow suit and extend the overtime protections so workers don’t continue to lose out on their hard-earned wages.

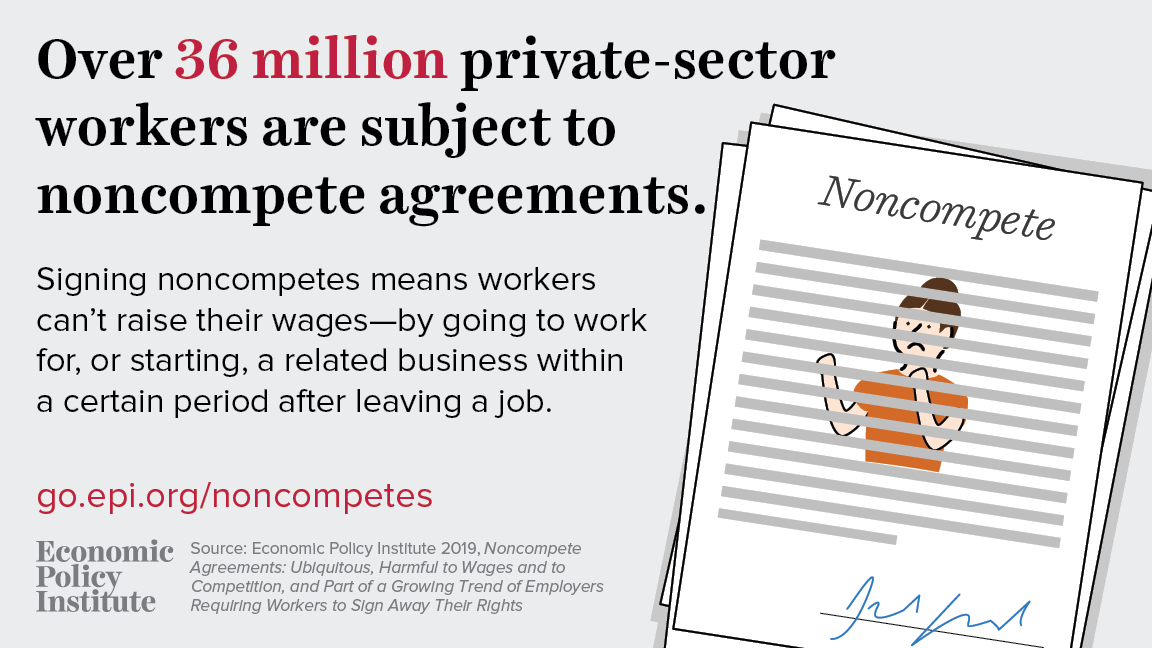

Let your workers move on

At least 36 million workers—27.8% of the private-sector workforce—are required to enter noncompete agreements. Noncompete agreements are employment provisions that ban workers at one company from going to work for, or starting, a competing business within a certain period of time after leaving a job. Establishments with high pay or high levels of education among workers are more likely to use noncompetes, but noncompetes agreements are also common in workplaces with low pay and low levels of education. More than a quarter (29.0%) of private-sector workers with an average hourly wage below $13.00 require noncompetes for all their workers. Noncompetes are part of a disturbing trend of employers requiring workers to sign away their rights. Noncompetes may be contributing to weak wage growth, given that changing jobs is how workers often get a raise. And given that noncompetes limit the ability of individuals to start businesses or take other jobs, it also is not difficult to see that noncompetes may be contributing to the declines in dynamism in the U.S. labor market. Congress should pass the bipartisan legislation, the Workforce Mobility Act of 2019, to prohibit noncompete agreements.

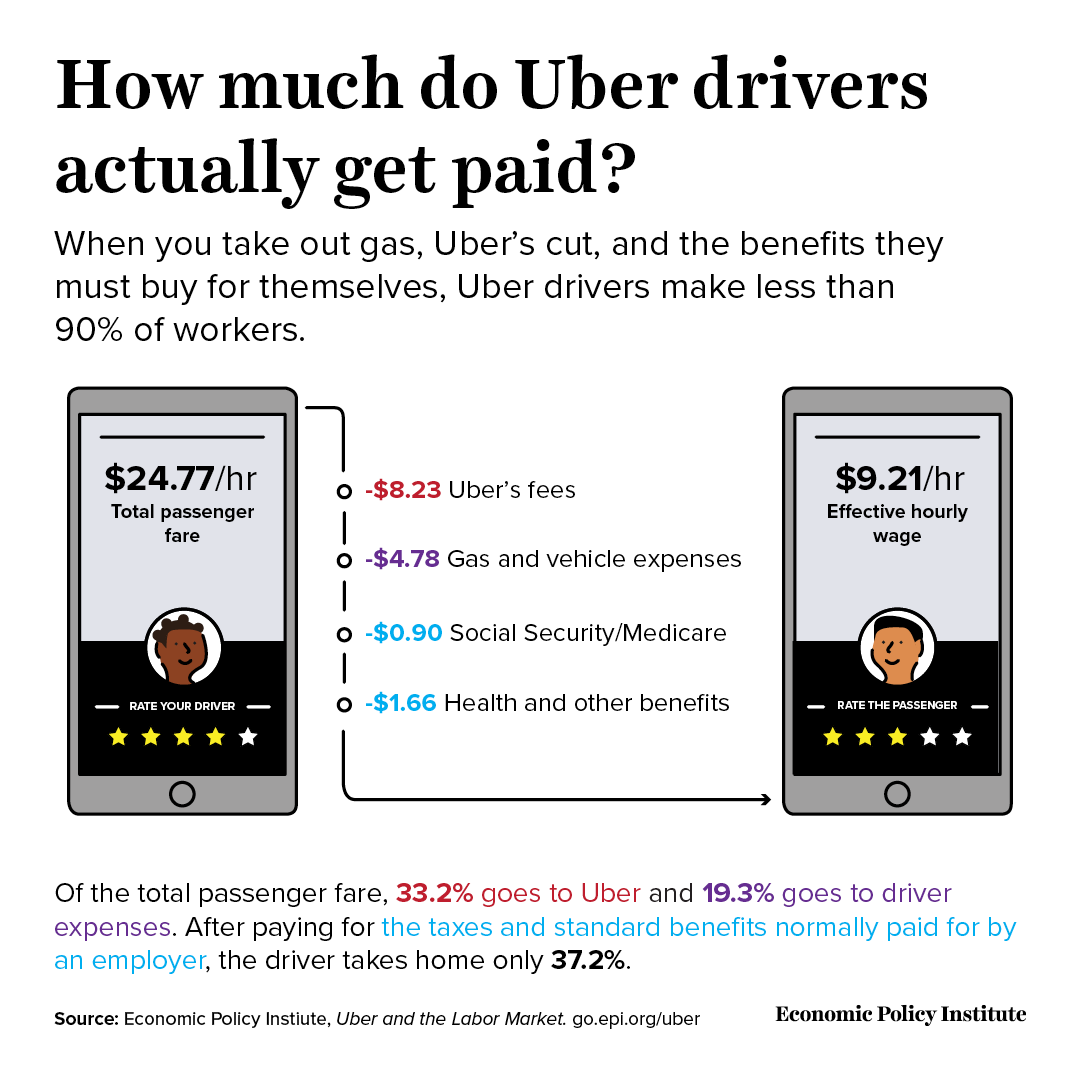

Labor protections for Uber drivers shuttling around Valentine’s couples

The General Counsel of the National Labor Relations Board recently released a memo claiming that Uber drivers are independent contractors, not employees of Uber. The reality is that these drivers have very little entrepreneurial freedom: Drivers can’t raise revenues because they can’t control prices or expand their customer base through marketing. Unlike a typical enterprise, Uber drivers do not build earnings as they get more experience. Uber drivers are not able to choose their customers—drivers are penalized for rejecting or not accepting trips. And after accounting for Uber’s commissions and fees and vehicle expenses, and taking into account the cost of a modest package of health insurance and other benefits equivalent to those earned by W-2 workers, Uber drivers earn the equivalent of $9.21 in hourly wages—less than what is earned by 90% of all other wage and salary earners, and below the minimum wage in 13 of the 20 major urban markets where Uber operates.

Recently, AB5 went into effect in California, a set of protections aimed at combatting the misclassification of workers as independent contractors, helping ensure that California’s employees have access to basic labor and employment protections denied to independent contractors including: minimum wage and overtime protections, paid sick days and family leave, workers’ compensation benefits, and unemployment insurance benefits. Policymakers across the country should take notice and provide similar protections to workers in their states.