Fed should keep rates steady to keep targets from turning into ceilings

All eyes will be on the Federal Open Market Committee (FOMC) today as they decide whether or not to follow up December’s interest rate hike (the first since 2006) with another. A consensus seems to be firming that they will hold pat in March and instead are likely to raise in June. Holding still and not raising rates is likely the right decision for two reasons: it will help reverse past damage left over from the Great Recession and will also make the job of future FOMCs easier because it will build credibility.

Both of these benefits stem from the Fed’s inability to keep wage and price inflation from running consistently below healthy targets in recent years. The Fed’s dual mandate is to maximize job-growth and push down unemployment while maintaining stability in inflation. The Fed has adopted an inflation target of 2 percent for “core” prices (ie, excluding food and energy) in the personal consumption expenditures (PCE) deflator. Yet the PCE core deflator has seen annualized growth of less than 2 percent for years now, and there’s no sign yet in the data that it is even moving durably closer to this target.

Introducing the People’s Budget

The American economy faces two major and interrelated problems, and contrary to what one would expect given the newly resurgent cries of deficit hawks, more spending is essential to solving both.

First and foremost, the economy has still not fully recovered from the Great Recession. Since the enactment of the Budget Control Act of 2011, ongoing austerity measures have meant that now, six and a half years after the Great Recession officially ended, the economy still has some slack and demand for workers is still too low. Indeed, if public spending growth over the current recovery had simply matched that of the early 1980s recovery, the economic recovery would already be complete. Instead, pulling away fiscal support too soon led to unnecessarily depressed output and high unemployment that has persisted throughout the recovery.

But austerity hasn’t just blocked a recovery to pre-recession trends, as bad as that would be. A growing body of research strongly suggests that the decelerating productivity growth that’s shown up in economic data recently is driven in large part by the weak aggregate demand implied by austerity.

The fastest growth in wage inequality between men happened in 2015

In my new paper on trends in wages in 2015, I discuss the resurgence of the growth in inequality. The main story of 2015 wage trends is that they were very unequal—so much so that the fastest growth in wage inequality between men happened in 2015.

Wage inequality can be measured in a number of ways. For example, there’s the growth of the top 1 percent compared to the bottom 90 percent. For that, we can look at Social Security wage data and find that from 1979 to 2014, wages at the top grew nearly 150 percent, while the bottom grew less than 17 percent. That’s a really stark difference, but we don’t have data yet that would allow us to see what happened in 2015.

Using the Current Population Survey Outgoing Rotation Group (CPS-ORG), we can look at what happened to wages in 2015 at every decile and the 95th percentile (but no higher because of data limitations). There are two key ways gaps we can look at within those data limitations. One compares the middle to the bottom (the 50/10 wage ratio) and the other compares the top to the middle (the 95/50 wage ratio). In my paper, I show how the 50/10 wage ratio has been fairly steady for the last 15 years. In fact, for men, the 50/10 wage ratio for men was about the same in 2015 as it was in the late 1970s.

Durbin and Sessions agree H-1B guestworker program must be fixed to protect migrant and American tech workers

Senator Jeff Sessions (R-Ala.), a Tea Party favorite, and Senator Dick Durbin (D-Ill.), a progressive stalwart, rarely agree on immigration policy. But last week, they did. What’s the issue they agree on? The need to reform two temporary work visas, the H-1B and L-1, because corporations use them to keep wages low and indenture foreign guestworkers—and replace U.S. workers in the technology sector with those lower-paid indentured foreign workers. This isn’t the first time this kind of bipartisan agreement has happened though: last year, 10 senators from across the political spectrum, from Bernie Sanders to James Inhofe, signed on to a letter to the Departments of Justice, Homeland Security, and Labor, asking them to investigate abuses of the H-1B program.

Sessions, who chairs the Senate Subcommittee on Immigration and the National Interest, held a hearing on February 25 to highlight H-1B abuses, especially the scandal surrounding the Walt Disney Company. Disney received much attention last year after the New York Times reported on its practice of laying off American workers and forcing them to train their own replacements on H-1B visas. The hearing was a substantive discussion about what’s wrong with the H-1B program and how to fix it. (The L-1 visa, which is also abused by the same companies and for the same occupations as the H-1B, but has fewer rules and virtually no enforcement, did not get nearly as much attention.) For anyone interested in U.S. immigration policy relating to skilled workers, the hearing is well worth watching in its entirety, but a few moments are worth highlighting.

Sessions and Durbin agreed that the system is being abused, and used primarily in ways that were not originally intended. Namely, most H-1B visas are not used to fill labor shortages or to bring in the best and brightest workers from abroad, or to put them on a path to lawful permanent residence. Instead, they are mainly used by temporary employment agencies that have an offshore outsourcing business model. This means that the H-1B workers who come to work in the United States are rented out to third-party companies, learn their job, and then transfer as much of the work as they can to the foreign offices of their staffing company. These outsourcing companies get about half of the 85,000 H-1B visas that are allotted each year to for-profit firms, and data show they apply for permanent residence for only a minuscule share of their workers. That means their H-1B workers aren’t on a path to permanently benefit U.S. labor market, but instead are being used as temporary, cheap labor and constantly rotated back to their home countries.

What to watch on Jobs Day: No evidence for another rate hike

Data on employment and unemployment in February will be released this coming Friday by the Bureau of Labor Statistics. Notably, this is the last jobs official jobs data we’ll get before the Federal Reserve meets in two weeks to decide whether or not to follow up December’s quarter point interest rate increase with another rate hike.

Forecasters are expecting Friday’s report to show quite weak performance in February, driven in large part by the major snowstorms that hit the East Coast during the week when jobs data was collected. However, even aside from expected temporary weakness, Friday’s jobs report is extremely unlikely to provide any strong evidence that the December rate hike should be followed with another increase in two weeks when the Fed meets again. In fact, data since the December hike contain mixed messages at best regarding the pace of recovery.

For example, after the December rate hike, data was released showing that gross domestic product grew at less than a 1 percent annualized rate in the last three months of 2015. Other data showed that the employment cost index, a closely-watched indicator of trends in labor costs pressure, grew just 2 percent year-over-year for the last quarter of 2015. And job growth in January was 151,000, down from the average monthly rate of 228,000 that the economy saw in 2015.

There have been encouraging (but quite small) upticks in some other economic data. Retail sales were strong in January. Core price inflation as measured by the consumer price index grew year-over-year in January at 2.2 percent, the fastest rate since 2012. (though Dean Baker highlights the role of rental price inflation in driving this, and the fact that attacking rental price inflation with higher interest rates is a flawed strategy).

Inflation makes proposed minimum wage increases more modest than they appear

This November, voters in several states will consider ballot measures to raise their state minimum wages. Because all of the proposals would incrementally phase in the higher minimum wages over a period of several years, it is important to look beyond the headline dollar amounts proposed, and consider what the new minimum wages would equal for someone in today’s economy. In other words, voters should evaluate proposed minimum wages after accounting for the inflation that will likely occur as the increases are gradually implemented.

Of course, it’s impossible to know what future inflation is going to be, but a variety of forecasters in both the public and private sector do make an attempt. The table at the bottom of this post shows the schedule of proposed minimum wage changes in California (under two possible ballot initiatives), Colorado, the District of Columbia, Maine, and Washington. It also shows the value of each proposed minimum wage in constant 2016 dollars1 using three different forecasts for consumer inflation—projections for the Consumer Price Index (CPI-U) from the Office of Management and Budget (OMB), the Congressional Budget Office (CBO), and Moody’s Analytics.2

As the table shows, a $12 minimum wage in 2020—proposed in Colorado and Maine—would have a current dollar value between roughly $11 and $10.75, depending on whose projections for inflation you believe. In Colorado, where the minimum wage is currently $8.31, this amounts to a real (inflation-adjusted) increase of between 29 and 32.5 percent over the current minimum. In Maine, where the minimum wage is currently $7.50, the proposed hike amounts to an increase of roughly 43 to 47 percent after inflation.

How we can save $17 billion in public assistance—annually

This post originally appeared on TalkPoverty.org.

Note to conservatives: Want to know the best way to find savings in government assistance programs? Here’s a hint—it’s not by cutting nutrition assistance to working people who are struggling.

It’s by paying them fairly for their labor.

A new report from the Economic Policy Institute indicates that raising the federal minimum wage to $12 by 2020 would lift wages for more than 35 million workers nationwide and generate about $17 billion annually in savings to government assistance programs.

This report shouldn’t come as a surprise. In contrast to the stereotypes and lies about people with low incomes, the reality is that a majority of public assistance recipients either have a job or have an immediate family member who is working. In fact, 41.2 million working Americans—or 30 percent of the workforce—receive means-tested public assistance. Nearly half of them work full-time.

Not surprisingly, workers who receive public assistance are concentrated in jobs that pay low hourly wages, like the retail, food services, and leisure and hospitality industries. A majority (53 percent) of workers earning $12.16 per hour or less—or the bottom 30 percent of wage earners—rely on public assistance. As wages go down, the percentage of workers relying on public assistance gets higher: 60 percent of workers earning less than $7.42—only slightly higher than the $7.25 federal minimum wage—receive some form of means-tested public assistance. Overall, 70 percent of the benefits in programs meant to aid non-elderly low-income households—programs like food stamps, Medicaid, and the Earned Income Tax Credits—go to working families.

Republicans (and two Democrats) in Congress want to derail commonsense protections for workers

Dozens of Republican members of Congress and two Democrats—Collin Peterson (D-Minn.) and Brad Ashford (D-Neb.)—have signed a letter to Secretary of Labor Thomas Perez about the Department of Labor’s (DOL) proposed rule on overtime pay for salaried employees, calling on him “to reconsider moving forward with this rule as drafted.” Oddly, a good part of the letter complains about provisions that are not in the proposed rule “as drafted.” The signers should be thanking the secretary, rather than complaining.

In particular, the letter complains that even though the proposed rule makes no change in the current regulation’s “duties test,” which identifies whether an employee’s job duties are those of an executive, professional, or administrative employee who might be exempt from overtime pay, the secretary does not spell out his future intentions. The signers worry, for example, that DOL is considering a common-sense tightening of the test to limit exemptions to employees who spend most of their time engaged in exempt duties. (The current duties test allows exemption of employees who spend nearly 100 percent of their time doing routine chores such as serving customers, running a cash register, stocking shelves, sweeping floors, and cleaning bathrooms.)

But, for better or worse, that change is not in the rule “as drafted.”

Workers, and honest employers, need a strong OSHA

Every day, events remind us why Congress created and continues to fund the Occupational Safety and Health Administration (OSHA). Cranes collapsing in New York and Cincinnati, mill explosions in Georgia, a foundry worker crushed in Ohio, construction workers falling to their deaths throughout the United States. When OSHA was created in 1970, 14,000 workers were killed on the job. Today in a much larger workforce, the number of on-the-job fatalities is less than 5,000 a year. Workplaces are undeniably safer today, in large part because of the training and education OSHA has provided and required employers to provide, its grants to union and non-profit worker safety training programs, the mandatory health and safety standards and guidance it issues, and its enforcement efforts. But they aren’t safe enough. In addition to the toll of deaths, nearly 4 million work-related injuries and illnesses are reported each year, and many more go unreported.

Enforcement is essential because standards and rules mean nothing if they aren’t followed, and a stubborn minority of businesses just don’t care enough about their employees to work safely and protect them from known hazards. Even hazards we’ve known about for a thousand years are routinely ignored by greedy contractors trying to cut corners and squeeze more profit out of their employees’ work.

Nothing better illustrates why workers need a strong enforcement effort from OSHA than trenching violations, such as putting workers into ten-foot deep trenches in loose soil without shoring the sides or protecting them with a metal trench box. Year after year, two to three dozen workers are killed when trench walls cave in, burying them in tons of dirt and rock, crushing their lungs. A single cubic yard of soil can weigh up to 3,000 pounds, and a worker caught by a cave-in can die even when his heads is not buried.

The Fed shouldn’t accept the “new normal” without a fight

Federal Reserve Chair Janet Yellen is testifying before Congress today and tomorrow, where she will be fielding questions about the state of the economy following the Fed’s recent rate hike.

Despite steady progress on some fronts, the economy is far from healthy. Yes, the unemployment rate fell below 5 percent for the first time since 2008 in January. But wage growth is still far below what a healthy target would be, and a glaring new weakness has appeared in the economic data in recent years—a significant slowdown in the pace of productivity growth. Productivity is essentially the value of income and output produced in an average hour of work in the U.S. economy—it provides the ceiling on how high living standards can rise. Productivity growth also provides a buffer against inflationary pressures. If American workers can produce 2 percent more income and output in a given hour of work from one year to the next, this means their hourly wages can rise 2 percent without putting any upward pressure on costs at all (to walk through the intuition, remember that while labor costs per hour have risen 2 percent, output per hour has also risen 2 percent, so labor costs per unit of output hence remain flat). These effects on living standards and inflation make productivity slowdowns particularly worrisome.

Historically, the combination of an unemployment rate low enough to spark Federal Reserve tightening and decelerating productivity growth would lead people to think that an overheating economy had pushed up inflation and interest rates, which crowded-out private sector investment. But this is definitely not the culprit behind recent productivity declines.

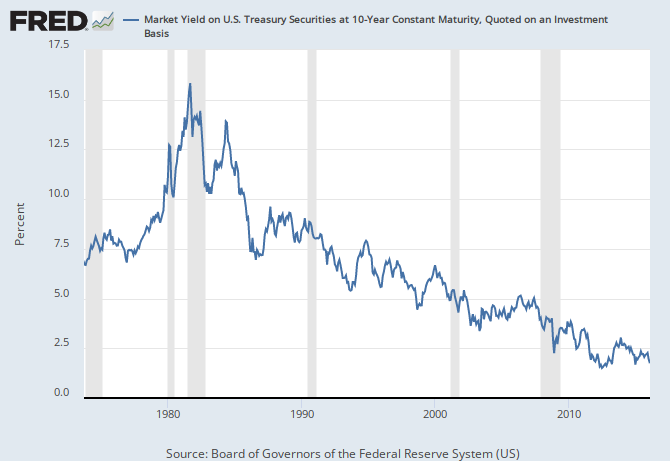

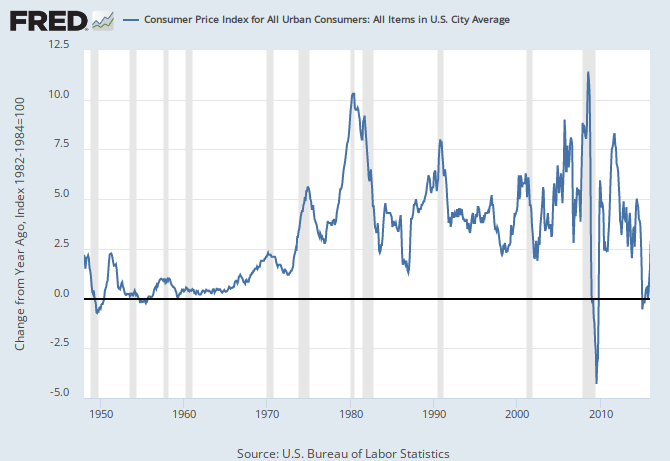

For one, interest rates and inflation remain historically low—and have shown no sign at all at lifting off the floor in recent years. It’s never been cheaper to borrow to make investments, so it’s not an overheating economy that has convinced private-sector firms to not invest.

{kind=link}

{kind=link}

So what has led to plunging productivity growth? It’s hard to know for sure, but we need to seriously consider the possibility that productivity growth (normally thought of by economists as a supply-side phenomenon) is just the last casualty of the chronic demand shortfall that brought on the Great Recession and which was never filled in sufficiently to push the economy back to full health.