The Fed shouldn’t accept the “new normal” without a fight

Federal Reserve Chair Janet Yellen is testifying before Congress today and tomorrow, where she will be fielding questions about the state of the economy following the Fed’s recent rate hike.

Despite steady progress on some fronts, the economy is far from healthy. Yes, the unemployment rate fell below 5 percent for the first time since 2008 in January. But wage growth is still far below what a healthy target would be, and a glaring new weakness has appeared in the economic data in recent years—a significant slowdown in the pace of productivity growth. Productivity is essentially the value of income and output produced in an average hour of work in the U.S. economy—it provides the ceiling on how high living standards can rise. Productivity growth also provides a buffer against inflationary pressures. If American workers can produce 2 percent more income and output in a given hour of work from one year to the next, this means their hourly wages can rise 2 percent without putting any upward pressure on costs at all (to walk through the intuition, remember that while labor costs per hour have risen 2 percent, output per hour has also risen 2 percent, so labor costs per unit of output hence remain flat). These effects on living standards and inflation make productivity slowdowns particularly worrisome.

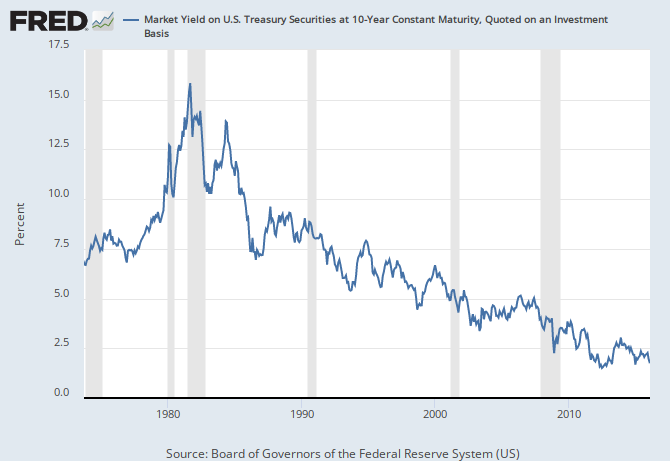

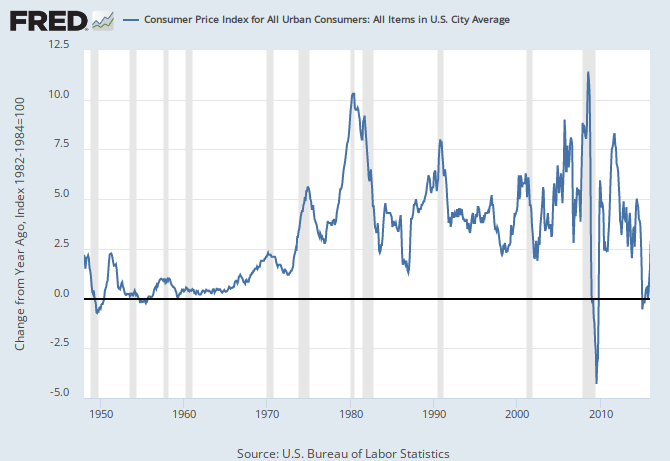

Historically, the combination of an unemployment rate low enough to spark Federal Reserve tightening and decelerating productivity growth would lead people to think that an overheating economy had pushed up inflation and interest rates, which crowded-out private sector investment. But this is definitely not the culprit behind recent productivity declines.

For one, interest rates and inflation remain historically low—and have shown no sign at all at lifting off the floor in recent years. It’s never been cheaper to borrow to make investments, so it’s not an overheating economy that has convinced private-sector firms to not invest.

{kind=link}

{kind=link}

So what has led to plunging productivity growth? It’s hard to know for sure, but we need to seriously consider the possibility that productivity growth (normally thought of by economists as a supply-side phenomenon) is just the last casualty of the chronic demand shortfall that brought on the Great Recession and which was never filled in sufficiently to push the economy back to full health.

When quitting is a good thing

This morning’s Job Openings and Labor Turnover Survey (JOLTS) report came in pretty much in line with other economic indicators that suggested a solid finish the 2015 labor market. Most notably, the hires and quits rates saw small upticks in December, a positive sign for an economy continuing to recovery. Unfortunately, those stronger results were somewhat tempered by January’s employment numbers, so the big question will be whether the upticks in today’s report will hold or will return back to their lower values. If these trends continue, it will mean we are still on the road towards full employment. Regardless, we need to stay on that road by encouraging the Federal Reserve to keep their foot off the brakes and encouraging policymakers at all levels of government to abandon austerity in favor of boosting local and state economies through increased investments and public sector employment.

While jobs day brings a whole series of great measures to analyze labor market slack, from the prime-age employment-to-population ratio to nominal wage growth, my favorite indicator on JOLTS day is the quits rate. A high quits rate is important because it means that workers feel confident enough in the economy to quit jobs that are not right for them and search for ones that are. It means a stronger labor market, where job opportunities abound and workers can find a better match. We often talk about all those workers who have been discouraged by economy, who aren’t seeing opportunities for them in the labor market or getting the hours they want. The quits rate is a similar measure. In a stronger economy, we should see the underemployment rate tick down while the quits rate ticks up. As you can see in the figure below, the quits rate has recently been moving up, but it’s still below a fully recovered rate and certainly below a full employment rate.

Despite seemingly stable U.S. trade balance, rapidly growing trade deficits in non-oil goods could lead to American job losses

The U.S. Census Bureau reported that the annual U.S. trade deficit in goods and services increased from $508.3 billion to $531.5 billion from 2014 to 2015, an increase of $23.2 billion (4.6 percent). The slow growth of the overall U.S. trade deficit hides massive underlying shifts in the trade deficit in petroleum products (which declined $157.3 billion, or 55.3 percent), compared with the trade deficit in all other goods, which increased from $547.7 billion to $673.1 billion—an increase of $125.4 billion, or 22.9 percent. In other words, the sharp decline in the petroleum trade deficit masked a large increase in the non-oil goods trade deficit, which could result in substantial U.S. job losses in the future.

Most U.S. goods trade consists of manufactured products. In 2015, manufacturing constituted 86.9 percent of total U.S. goods trade, and 94.3 percent of total trade in non-oil goods. Because manufacturing is such a large employer, rapidly growing trade deficits in non-oil goods are a threat to future employment in this sector. The growing trade deficit in manufactured products rose to 3.8 percent of GDP, only 0.7 percent (7 tenths) of a percentage point below the maximum reached in 2005. The manufacturing trade deficit also reached a record high of $681 billion in 2015, well in excess of the previous peak $619.7 in 2007. Rapidly growing manufacturing trade deficits were responsible for most, if not all, of the 4.8 million U.S. manufacturing jobs lost between December 2000 and December 2015, and there’s every reason to believe that these job losses will continue if the non-oil trade deficits keeps growing.

This analysis is primarily concerned with shifts in goods trade. The U.S. balance of trade in services declined slightly in 2015, falling from a trade surplus of $233.1 billion in 2014 to $227.4 billion in 2015. Trade in goods continues to dominate overall trade flows for the United States—trade in services totaled only 24.1 percent of total U.S. goods and services trade in 2015.

Should we care about slow nominal wage growth when price inflation is slow? YES.

Nominal wages for American workers rose by 2.6 percent in the 12 months ending in December 2015. Over the same time, prices have risen just under 0.7 percent (held down mostly by falling oil prices). This mean that real (that is, inflation-adjusted) wages have grown 1.9 percent in that year. In historical perspective, this is a very healthy rate of real wage growth (for example, real hourly wages for the bottom 70 percent of workers have averaged well under 0.5 percent annually since 1979).

{kind=link}

Since it is this real, not nominal, wage growth that influences living standards, shouldn’t we be perfectly happy with this constellation of wage and price inflation? Not really, for a number a reasons.

For one, the extraordinarily low rates of price inflation won’t continue. They’ve been driven by large declines in commodity prices. The gains to real living standards are genuine—cheap gas really does make paychecks stretch further (though how good cheap gas is in the long run for climate change is a whole other story), but we know that commodity prices are volatile and are likely to stabilize or even rise in the next year. If either of these things happens, the overall rate of inflation in the next year will rise.

Further, even if commodity prices remained depressed forever and overall price inflation really did permanently shift to a slower pace, it is far from clear that this would be a good outcome or that the real wage growth seen in the past year would continue.

What to Watch on Jobs Day: Will we finally reach full employment in 2016?

We’ve seen solid growth in employment over the past couple of years, and the unemployment rate has come down dramatically, but by any reasonable definition we are still not that close to genuine full employment. So, what is full employment? In a great book (pdf), Jared Bernstein and Dean Baker define full employment as “the level of employment at which additional demand [injected into] the economy will not create more employment.” Full employment should show up in indicators on both the quantity and the price side (i.e., wages) of the labor market. Unemployment is low during periods of full employment, and due to high demand for labor, employed workers have more bargaining power—as a result they will be better able to negotiate higher wages and get the hours they want.

Let’s look at some measures of employment on the quantity side. A good measure of slack in employment and hours is the BLS’s U6 measure of labor underutilization. It measures total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force. Basically, people who want to work, plus employed people who want to work more hours, plus people who have looked for work in the last year but stopped looking for some reason in the last four weeks and are hence not classified as currently “in the labor force.”

The figure below shows these data by race, which demonstrates that, as with the unemployment rate, the underemployment rate is much higher for people of color. While the U6 has come down substantially but it is still elevated and has a ways to go before it gets to pre-recession levels. (And these pre-recession levels are elevated relative to the last time we had unambiguous full employment in the late 1990s and 2000.)

NPR report reveals the real reason why agricultural employers prefer guestworkers

A recent story from NPR’s Dan Charles titled “Guest Workers, Legal Yet Not Quite Free, Pick Florida’s Oranges,” provides a crucial glimpse into what it’s like being a guestworker in the United States. As the title suggests, it’s not pretty. The headline is probably using the word “free” as a double entendre: guestworkers are not free in the sense of the free market, nor in the sense of someone who has personal freedom and agency; i.e., is not a slave.

Guestworkers are foreign workers who are temporarily authorized to work in the United States with nonimmigrant visas. EPI and civil rights groups, farmworker advocates, and numerous media reports have highlighted how employers often prefer to employ guestworkers instead of Americans because they can be paid less and are indentured to their employers. Often, employers claim that guestworkers are doing “dirty jobs,” which Americans find so unappealing that they just flat out won’t do them. There’s plenty of evidence out there to suggest that the real reasons are much different. For instance, two recent investigative reports from Buzzfeed paint a bleak picture of the H-2A and H-2B programs (two guestworker programs that allow employers to hire temporary foreign workers for agricultural and non-agricultural jobs, respectively), documenting the ways in which these workers are indentured servants with few rights or labor protections. This happens because 1) guestworkers often arrive heavily in debt to labor recruiters who connect them to their temporary jobs, and 2) their employer controls the visa status, which means that 3) guestworkers do not have the legal right to switch employers if they don’t get paid an appropriate fair wage or if their boss breaks the law or exploits them in some other way. Ultimately, the result for guestworkers is a reasonable fear that if they complain about low pay or unsafe work conditions, they’ll get fired, which renders them deportable and means they won’t have a chance to earn back the thousands of dollars they had to borrow to pay the recruiter.

The labor rights of four million migrants hang in the balance at the Supreme Court

The Supreme Court deserves praise for agreeing to review United States v. Texas, a case that will determine the fate of the most significant of the executive immigration actions announced by the president on November 20, 2014. The Court will review a lower court’s decision that temporarily blocked President Obama’s Department of Homeland Security (DHS) guidance directive that “establish[es] a process for considering deferred action for certain aliens who have lived in the United States for five years and either came here as children or already have children who are U.S. citizens or permanent residents” (hereinafter referred to simply as “Guidance”). The Supreme Court will decide whether the president overstepped the bounds of his legal authority when DHS issued this Guidance.

More specifically, the Guidance in question would defer the deportation of unauthorized immigrants who are the parents of children who are either U.S. citizens or legal permanent residents, have resided in the United States for at least five years, and are not a DHS enforcement priority for deportation. This is known as the “DAPA” initiative, Deferred Action for the Parents of Americans and Legal Permanent Residents. The Guidance would also update and expand “DACA,” the Deferred Action for Childhood Arrivals initiative (in place since 2012), which to date has provided deferred action to over 660,000 persons who entered the country as young people without authorization. Combined, over five million persons could be eligible for DAPA, DACA, and expanded DACA (sometimes referred to as DACA+), out of a total unauthorized immigrant population of 11 million.

The Obama administration pushes for a better response to unemployment

President Obama has announced a package of reforms to repair some of the damage done in recent years to the unemployment insurance system and to provide more help to workers at risk of losing jobs—incentives for employers to retain workers, more income support for job losers, and more help getting retrained and back to work. Reforms are needed, and most of the president’s proposals are obviously helpful.

Background

When the economy crashed in 2007 the federal-state system of unemployment insurance (UI) was far from ready. States had had five years since the previous recession to replenish their UI trust funds, improve coverage (with the help of generous federal grants provided during the Bush administration) and plan for the next downturn. Yet when the crash came and the unemployment rate rose to 10 percent, UI trust funds had not been refilled. Many states had unwisely cut taxes rather than accumulate surpluses that could be drawn down in a recession. By 2007, only 17 states were minimally solvent. Some states—but not many—had extended coverage to workers with unstable employment histories, seasonal workers, and poorly paid individuals who previously would not have qualified for benefits. If you had to give the states a grade on preparedness, a D+ would be generous.

The result was a disaster. Thirty-six states ran out of money and had to borrow in order to pay benefits, with the loans peaking at $47 billion in 2010. Most of the state UI trust funds are still in bad shape, and—according to the White House—only 20 states have sufficient reserves to weather a single year of recession. As of January 13, 2016, California still owes $6.5 billion to the Federal Unemployment Account, Ohio owes $773 million, and Connecticut owes $100 million.

The Lilly Ledbetter Act is part of a more ambitious women’s economic agenda

This Friday is the anniversary of the Lilly Ledbetter Fair Pay Act of 2009, a reminder that a significant pay gap still exists between men and women in the United States. At the median, hourly pay for women is only 82.9 percent of men’s median wage ($15.21 versus $18.35). While over the last several decades women have made gains in terms of education attainment and labor force participation, compared to men, they are still paid less, are more likely to hold low wage jobs, and are more likely to live in poverty. This economic gap exists to a greater degree for women of color and remains persistent across women of varying education levels and working in different occupations.

But the gender wage gap is only one way the economy shortchanges women. At the same time the gender wage gap has persisted, hourly wages for the vast majority of workers have stagnated, as the fruits of increased productivity and a growing economy have accrued to those at the top. It hasn’t always been this way: pay rose with productivity in the three decades following World War II. But since the 1970s, pay and productivity have grown further apart, as the result of intentional policy decisions that eroded the leverage of the vast majority of workers to secure higher wages.

A progressive women’s economic agenda, one that seeks to truly maximize women’s economic potential, must focus on both closing the gender wage gap and raising wages more generally.

14 states raised their minimum wage at the beginning of 2016, lifting the wages of more than 4.6 million working people

At the beginning of the year, 14 states raised their minimum wages, lifting wages for over 4.6 million workers in states across the country. Unlike last year’s increases, the majority of these increases (12) were scheduled increases initiated by legislation or approved by voters through ballot measures. The other two (Colorado and South Dakota) were changed as a result of inflation indexing—a process adopted by 15 states by which the minimum wage is automatically adjusted each year to match increases in prices.

Table 1 below shows the magnitude of the minimum wage increase in each state, ranging from an increase of 5 cents in South Dakota to 1 dollar in four states (Alaska, California, Massachusetts, and Nebraska). Because inflation was very low in 2015, nine of the 11 states with inflation indexing set to go into effect at the beginning of the year did not adjust their minimum wages in 2016. Colorado and South Dakota were the only exceptions, yet their increases were small, and thus the increases affected relatively small shares of each state’s workforce: 2.1 percent and 3.4 percent, respectively. Minimum wage increases affected a much larger portion of the workforce in states that initiated larger increases through legislation. For example, California’s $1.00 minimum wage increase lifted wages for 18.6 percent of the state workforce.

All together, these increases will provide 4.6 million workers over $3.5 billion in higher annual wages. This additional pay, though modest, represents a significant boost to the spending power of low-wage workers and their families. For example, a worker in Nebraska who was previously earning the state minimum wage of $8.00 an hour in 2015 will see their hourly pay increase by 12.5 percent.

States with minimum wage increases effective January 1, 2016

| States with minimum wage increase | Amount of wage increase | New wage on Jan. 1, 2016 | Reason for change | Directly affected workers1 | Indirectly affected workers2 | Total affected workers | Share of state’s wage-earning workforce | Total wage increases for affected workers3 |

|---|---|---|---|---|---|---|---|---|

| Alaska | $1.00 | $9.75 | Legislation | 15,000 | 18,000 | 33,000 | 10.7% | $23,476,000 |

| Arkansas | $0.50 | $8.00 | Legislation | 45,000 | 45,000 | 90,000 | 7.8% | $38,036,000 |

| California | $1.00 | $10.00 | Legislation | 1,748,000 | 1,172,000 | 2,920,000 | 18.6% | $2,703,126,000 |

| Colorado | $0.08 | $8.31 | Inflation adjustment | 44,000 | 6,000 | 50,000 | 2.1% | $14,429,000 |

| Connecticut | $0.45 | $9.60 | Legislation | 79,000 | 27,000 | 106,000 | 6.7% | $57,813,000 |

| Hawaii | $0.75 | $8.50 | Legislation | 23,000 | 27,000 | 50,000 | 8.6% | $23,576,000 |

| Massachusetts | $1.00 | $10.00 | Legislation | 181,000 | 175,000 | 356,000 | 11.4% | $266,335,000 |

| Michigan | $0.35 | $8.50 | Legislation | 184,000 | 98,000 | 283,000 | 6.9% | $77,857,000 |

| Nebraska | $1.00 | $9.00 | Legislation | 58,000 | 42,000 | 101,000 | 11.5% | $67,741,000 |

| New York4 | $0.25 | $9.00 | Legislation | 273,000 | 213,000 | 486,000 | 5.9% | $143,521,000 |

| Rhode Island | $0.60 | $9.60 | Legislation | 37,000 | 27,000 | 64,000 | 13.5% | $32,186,000 |

| South Dakota | $0.05 | $8.55 | Inflation adjustment | 8,000 | 5,000 | 13,000 | 3.4% | $3,108,000 |

| Vermont | $0.45 | $9.60 | Legislation | 15,000 | 3,000 | 18,000 | 6.3% | $8,768,000 |

| West Virginia4 | $0.75 | $8.75 | Legislation | 49,000 | 26,000 | 75,000 | 11.5% | $46,700,000 |

| Total | 2,760,000 | 1,886,000 | 4,646,000 | $3,506,675,000 |

1. Directly affected workers will see their wages rise as the new minimum wage rate will exceed their current hourly pay.

2. Indirectly affected workers have a wage rate just above the new minimum wage (between the new minimum wage and the new minimum wage plus the dollar amount of the increase in the previous year's minimum wage). They will receive a raise as employer pay scales are adjusted upward to reflect the new minimum wage.

3. Total annual amount of increased wages for directly and indirectly affected workers.

4. Changes went into effect 12/31/2015.

Note: Totals may not sum due to rounding. "Legislation" indicates that the new rate was determined by legislature or ballot vote. "Inflation adjustment" indicates that the new rate was based on some measure of inflation.

Source: EPI analysis of Current Population Survey Outgoing Rotation Group microdata 2014Q4-2015Q3