The Fed shouldn’t accept the “new normal” without a fight

Federal Reserve Chair Janet Yellen is testifying before Congress today and tomorrow, where she will be fielding questions about the state of the economy following the Fed’s recent rate hike.

Despite steady progress on some fronts, the economy is far from healthy. Yes, the unemployment rate fell below 5 percent for the first time since 2008 in January. But wage growth is still far below what a healthy target would be, and a glaring new weakness has appeared in the economic data in recent years—a significant slowdown in the pace of productivity growth. Productivity is essentially the value of income and output produced in an average hour of work in the U.S. economy—it provides the ceiling on how high living standards can rise. Productivity growth also provides a buffer against inflationary pressures. If American workers can produce 2 percent more income and output in a given hour of work from one year to the next, this means their hourly wages can rise 2 percent without putting any upward pressure on costs at all (to walk through the intuition, remember that while labor costs per hour have risen 2 percent, output per hour has also risen 2 percent, so labor costs per unit of output hence remain flat). These effects on living standards and inflation make productivity slowdowns particularly worrisome.

Historically, the combination of an unemployment rate low enough to spark Federal Reserve tightening and decelerating productivity growth would lead people to think that an overheating economy had pushed up inflation and interest rates, which crowded-out private sector investment. But this is definitely not the culprit behind recent productivity declines.

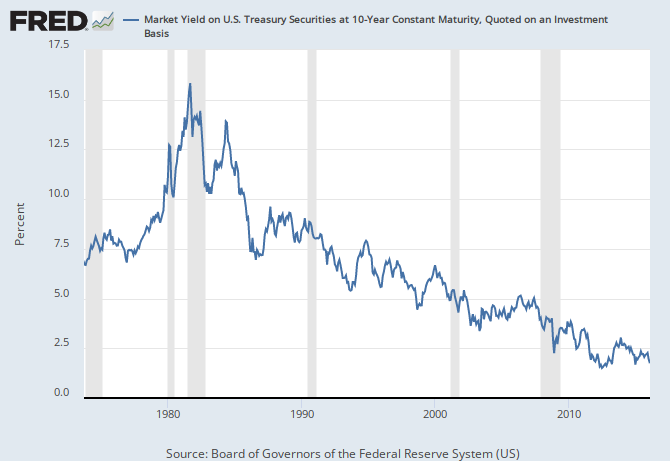

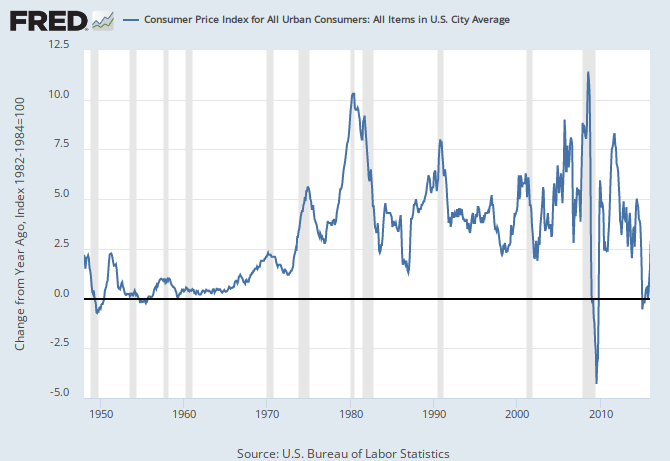

For one, interest rates and inflation remain historically low—and have shown no sign at all at lifting off the floor in recent years. It’s never been cheaper to borrow to make investments, so it’s not an overheating economy that has convinced private-sector firms to not invest.

{kind=link}

{kind=link}

So what has led to plunging productivity growth? It’s hard to know for sure, but we need to seriously consider the possibility that productivity growth (normally thought of by economists as a supply-side phenomenon) is just the last casualty of the chronic demand shortfall that brought on the Great Recession and which was never filled in sufficiently to push the economy back to full health.

How does weak demand eventually filter through and damage growth on the supply side? For one, about half of productivity improvements over time are the result of simple capital-deepening—the fact that business investments give workers more and better tools with which to do their jobs. For example, construction sites thirty years ago had a lot more shovels and far fewer earth-moving machines and cranes than today’s sites have. A key finding in empirical macroeconomics is that the number one determinant of business investment in plants and equipment is simply the underlying pace of economic growth. The falloff in business investment over the Great Recession was simply enormous—real, net investment in equipment and intellectual property by the private sector was negative in 2009, something that has never happened before. Investment has increased since, but it’s fair to say that American workers have less capital to work with today than they would have had absent the Great Recession.

Further, lots of business investment takes the form of research and development. And another key contributor to productivity growth is technological advance. This technological advance does not fall from the sky, rather it is the product of directed investment (R&D) and trial and error (workers learning by doing). When the pace of R&D investment is slow and output growth is slow enough to provide fewer opportunities for learning by doing, it is not shocking that technological advancement may slow. Further, there is ample evidence that firms boost labor-saving investments (which boost productivity) when labor costs are rising rapidly. Rapid labor cost growth has not been a feature of the recovery from the Great Recession. Between 2007 and 2014, real hourly pay for the median worker, for example, has slightly declined (see Table 1 here), and the share of corporate sector income accruing to capital owners rather than to employees reached historic highs. This labor market slack and weak wage growth has provided very little spur to boost productivity in the search for higher profits.

The stakes in how we interpret recent signs on weak productivity growth are huge. If productivity growth is simply a given, and cannot be boosted by further efforts to close the aggregate demand shortfall, this means we’re actually much closer to full employment than otherwise, and, it means that the level of wage growth consistent with a fully healthy economy is closer to 3 percent than 4 percent. And since wage growth is now running around 2.5 percent, we’re getting close to this long-run wage target and hence close to hitting the inflation barrier—that is, crossing the line into economic overheating that will cause prices to rise faster than the Fed’s 2 percent target.

If, instead, further boosts to demand will draw forth increases in the pace of productivity growth, we have a lot of room between today and running into the inflation barrier, and a 3.5-4 percent wage inflation target remains pretty sensible.

The evidence that demand shortfalls eventually bleed into destruction of productive capacity is strong. More importantly, if this evidence is right, then the risk of settling for today’s weak productivity growth and reeling back efforts to spur demand growth are just enormous. To see why, consider the Congressional Budget Office (CBO) forecasts of potential GDP—the income and output the U.S. economy could generate if all resources (including labor) were fully employed. The CBO’s estimate for potential output in 2016 that they released last month is a full $1.7 trillion lower than what they forecast for this year in their 2008 estimates. That is, since the Great Recession, CBO has lowered its estimate of the productive capacity of the U.S. economy by nearly 10 percent. This is a staggeringly large reduction in the economy’s capacity, and the timing suggests that the Great Recession (caused by a huge shortfall in demand) is the prime culprit.

These stakes are far too large to simply shrug and accept slower productivity growth as the “new normal” without at least experimenting to see if the damage that emerged during the demand slack of the Great Recession can be ameliorated with a period of rapid demand growth (or, “running the economy hot”). Federal Reserve hawks want to label the recent productivity slowdown as a sign from above that the economy can’t do much better than it’s doing today. This view ignores far too much economic evidence and threatens to become a self-fulfilling prophecy if they have their way and slow growth through further rate increases. If that happens, we will be a much poorer nation going forward.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.