Sure, it’s weak, but this ‘so-called recovery’ is no weaker than the last one, Greg Mankiw

On Monday, EPI labor economist Heidi Shierholz pointed out that job growth during the current recovery has been stronger than job growth during the recovery following the 2001 recession. In addition, the jobs recovery from the Great Recession isn’t too far off the pace following the 1990 recession; private sector job growth 33 months into the 1990 recovery was 3.4 percent, while it’s 2.7 percent for the current recovery. Shierholz’s main point is that it’s the historic length and severity of the Great Recession, and not unprecedentedly poor job growth in the recovery, that explains why we’re still so far from full employment 33 months since the recession officially ended.

Greg Mankiw, however, isn’t about to highlight that fact. Mankiw, who was chairman of the Council of Economic Advisers under George W. Bush from 2003-05 and currently serves as an economic adviser to presidential candidate Mitt Romney, posted the graph below on his blog last weekend with the dismissive headline, Monitoring the So-called Recovery:

The graph shows the employment-to-population ratio (or EPOP) going back to 2004. We see the EPOP drop steeply during the Great Recession, followed by a mostly flat trajectory since. But let’s add a line to Mankiw’s graph for a direct comparison of this recovery to the last one:

It’s clear from the figure that EPOP fell much further and faster during the Great Recession than the 2001 recession. But looking to the right of the vertical line, we see that EPOP growth (or lack thereof) in the current recovery follows the same trend (i.e., flat) as the recovery after the 2001 recession. In other words, the key difference between EPOP at this point in the current recovery versus the same point in the last recovery (during which Mankiw chaired the CEA) is the length and severity of the recession that preceded them.

Yes, this recovery is slow, and certainly there is no excuse for the current complacency from policymakers about the jobs crisis, but the folks over at Angry Bear have a good adage for Mankiw: “People who live in glass houses should be careful about throwing rocks.”

With research assistance from Heidi Shierholz and Hilary Wething

The utter wrongness of people who complain about double-counting Medicare savings

In a post today, the Committee for a Responsible Federal Budget reiterated its position that it is double-counting to argue that the Affordable Care Act both reduces the deficit and extends the life of the Medicare trust fund. Chuck Blahous, the Medicare actuary who started this mess, and Peter Suderman over at Reason agree.

Their position is wrong, wrong, wrong. First, let’s clarify the baseline. CRFB points out, correctly, that there are two baselines to choose from. The Trust Fund Baseline, which is used by Blahous, assumes that a program’s spending is constrained by the resources in its trust fund. If the trust fund is gone, the spending will automatically be cut. The Unified Budget Baseline, on the other hand, assumes that spending on programs will continue as scheduled, and the federal government will simply borrow money to ensure that benefits are not cut.

As many pointed out, the Blahous baseline is ridiculous. If spending is constrained by the trust fund, then we don’t have a problem. But the main purpose of the Affordable Care Act—heck, why we’re talking about deficit reduction in the first place!—is the assumption that we do have a problem. And even if—as CRFB states—both baselines are equally valid, it’s clear from the administration’s rhetoric that it is using the latter.

So, how can it be that a dollar can both be used to reduce the deficit and extend the trust fund? Well remember that under the baseline we’re using, program outlays aren’t constricted by the trust fund. Outlays have nothing to do with the trust fund. So therefore, extending the trust fund doesn’t cost anything, because it’s an accounting identity with no programmatic relevance.

Now, you might say that the Obama administration is being misleading, talking about extending the life of a trust fund, when under its own assumptions, the trust fund doesn’t matter. But while it may not have any impact on spending levels, it does matter for other reasons. While the size of the trust fund doesn’t determine how much spending can be done, it does potentially impact how the spending is financed. In the case of Social Security, for example, the trust fund commits income taxes (a more progressive revenue stream) in the future to redeem past surpluses financed by payroll taxes (a less progressive revenue stream); so declaring the trust fund meaningless in this case would profoundly affect the distribution of Social Security’s costs.

Trust funds also have political relevance. Even if you assume that Medicare outlays will be unaffected by the trust fund, having an insolvent trust fund opens a program up to political attacks. We’re seeing that right now with Social Security. So even if the trust fund doesn’t matter to the program’s operation, it still matters to shore of the program’s political strength. That’s something that seniors—and really anyone fond of Medicare—should care about.

A rising tide for increasing minimum wage rates

On Monday, the New York Times reported on the growing groundswell to raise wages for the lowest-paid workers by increasing minimum wage rates. Legislators in New York, New Jersey, Massachusetts, Connecticut, and Illinois are all looking toward raising their state minimums. At the same time, Iowa Sen. Tom Harkin has introduced a bill that—among making other critical investments, strengthening worker protections, increasing tax fairness, and reducing the federal deficit—would raise the federal minimum wage to $9.80 per hour over three years and then index it to inflation.

As Table 1 shows, increasing the federal minimum wage in three steps to $9.80 per hour, as described in the Harkin bill, would raise the wages of 28 million Americans. About 19.5 million workers whose wages are between the current minimum and the proposed $9.80 rate would be directly affected. Another 8.9 million whose wages are just above the proposed minimum would also see a pay increase through “spillover” effects as employers adjust their overall pay scales.

*Total estimated workers is estimated from the CPS respondents for whom either a valid hourly wage is reported or one can be imputed from weekly earnings and average weekly hours. Consequently, this estimate tends to understate the size of the full workforce. **Directly Affected workers will see their wages rise as the new minimum wage rate will exceed their current hourly pay. ***Indirectly affected workers currently have a wage rate just above the new minimum wage (between the new minimum wage and the new minimum wage plus the dollar amount of the increase). They will receive a raise as employer pay scales are adjusted upward to reflect the new minimum wage. Source: EPI Analysis of 2011 Current Population Survey, Outgoing Rotation GroupWorkers affected by proposed federal minimum wage increase

Federal minimum increased to $9.80 per hour in three increases of 85 cents, modeled for July 2012, 2013, and 2014

Total estimated workers in third year*

127,361,000

Directly affected**

19,485,000

Indirectly affected***

8,869,000

Total (directly & indirectly) affected

28,354,000

Table 2 highlights some demographic characteristics of the affected workers. Fifty-four percent are women and 54 percent work full-time. The overwhelming majority (87.9 percent) are at least 20 years old. This may come as a surprise to some, as minimum-wage workers are often portrayed as teenagers working part-time. The reality is that only 12 percent of those who would be affected by the raise are teenagers and only 15 percent work fewer than 20 hours per week.

*Directly Affected workers will see their wages rise as the new minimum wage rate will exceed their current hourly pay. **Indirectly affected workers currently have a wage rate just above the new minimum wage (between the new minimum wage and the new minimum wage plus the dollar amount of the increase). They will receive a raise as employer pay scales are adjusted upward to reflect the new minimum wage. Source: EPI Analysis of 2011 Current Population Survey, Outgoing Rotation GroupDemographic characteristics of affected workers

Directly affected*

Indirectly affected**

Total affected

% of total affected

Total

19,485,262

8,868,654

28,353,916

100.0%

Female

10,924,035

4,527,632

15,451,666

54.5%

Male

8,561,228

4,341,022

12,902,250

45.5%

Part-time (<20hrs/week)

3,327,498

918,690

4,246,187

15.0%

Mid-time (20-34hrs/week)

6,599,616

2,167,363

8,766,979

30.9%

Full-time (35+ hrs/week)

9,558,149

5,782,601

15,340,750

54.1%

Age 20 +

16,509,188

8,421,003

24,930,191

87.9%

Under 20

2,976,074

447,651

3,423,725

12.1%

White

10,959,722

4,960,138

15,919,860

56.1%

African American

2,741,079

1,285,583

4,026,662

14.2%

Hispanic

4,654,719

2,035,908

6,690,626

23.6%

Asian

1,129,742

587,025

1,716,767

6.1%

Furthermore, low-wage workers tend to spend rather than save an additional dollar earned, often because they have little other choice. The additional household consumption generated by this boost to low-wage workers’ paychecks would benefit the labor market as a whole, because the resulting economic activity translates into job growth. After controlling for a reduction in corporate profits resulting from the minimum wage increase, and assuming some of the business expense of paying higher wages is passed on to consumers, the net effect of the proposed minimum wage increase is an increase in economic activity of over $25 billion over the next three years, which would generate roughly 100,000 new jobs.

Economic effects of proposed federal minimum wage increase

| Federal minimum increased to $9.80 per hour in three increases of 85 cents, modeled for July 2012, 2013, and 2014 | |

|---|---|

| Increased wages for directly & indirectly affected* | $39,677,170,000 |

| GDP Impact** | $25,115,648,697 |

| Jobs Impact*** | 103,000 |

*Increased wages: Total amount of increased wages for directly and indirectly affected workers.

**GDP and job stimulus figures utilize a national model to estimate the GDP impact of workers' increased earnings, after controlling for reductions to corporate profits.

***The jobs impact total represents full-time equivalent employment.The increased economic activity from additional wages adds not just jobs but also hours for people who already have jobs. Full-time employment takes that into account, by essentially taking the number of total hours added (including both hours from new jobs and more hours for people who already have jobs) and dividing by 40, to get full-time-equivalent jobs added. Jobs numbers assume full-time employment requires $115,000 in additional GDP.

Source: EPI Analysis of 2011 Current Population Survey, Outgoing Rotation Group. Job impact estimation methods can be found in: Hall, Doug and Gable, Mary. 2012. The benefits of raising Illinois' minimum wage. Washington, D.C.: Economic Policy Insitutute; and Bivens, Josh L. 2011. Method memo on estimating the jobs impact of various policy changes. Washington, D.C.: Economic Policy Institute.

In a historical context, the increase proposed by the Harkin bill is long overdue. As John Schmitt and Janelle Jones at the Center for Economic and Policy Research explain, the real value of the minimum wage is far below its historical levels, despite the fact that the low-wage workforce is older and better educated than ever before. Congress has had to raise the minimum wage 17 times since its peak value in 1968 in order to combat inflation. Indexing the minimum wage, as 10 states have already done, would fix this problem once and for all.

The lingering effects of the recession make this an even more critical time to raise the wage floor. Even as employment has slowly picked up in the recovery, wage growth is still painfully weak. Moreover, recent reports show that low-wage work has been driving much of the recent job growth. (This also means that the figures here may actually understate the number of people who would be affected by an increase in the federal minimum.) The Harkin bill, and similar state proposals, would give much-needed help to these workers and provide additional stimulus to the U.S. economy – all without costing anything to taxpayers.

Since when does each and every budget policy proposal have to singlehandedly eliminate the deficit?

In all seriousness, when did singlehandedly “fixing the deficit” become a necessary criterion for each and every tax and budget policy proposal? David Fahrenthold and David Nakamura invoke this strange new rule in an article in today’s Washington Post.

“Neither [the Paul Ryan budget nor the Buffett Rule] will fix the deficit problem anytime soon: The GOP’s proposal wouldn’t balance the budget until 2040. By itself, the Buffett Rule wouldn’t do it ever.”

There is a lot wrong in this sentence.

First, comparing a comprehensive budget proposal to a single tax reform is an apples-to-oranges (or apple-to-bushel-of-apples) comparison. Second, the Ryan budget doesn’t actually balance the budget until … well ever. The too-often cited Congressional Budget Office’s long-term analysis evoked here is based on the false premise that revenue will magically hold at 19 percent of GDP, ignoring the trillions of dollars of budget-busting, gimmicky tax cuts (Ryan assures that this money and more can be made up by “broadening the base” of taxation but offers no specifics). Lastly, nobody invokes the Buffett Rule as the single instrument for balancing the budget—very few fiscal policies have that reach. Take an extreme example: Immediately abolishing the Department of Defense would not balance the budget within a decade, relative to current policies. That’s besides the point–cutting more than $7 trillion in non-interest spending over a decade would produce a sustainable fiscal trajectory (ignoring sizable second-order cyclical budget effects from the massive hit to aggregate demand). The trajectory for debt held by the public is the relevant metric of fiscal sustainability, not a binary for budget deficit/budget surplus.

Fahrenthold and Nakamura double-down on brushing off non-trivial budgetary savings, also missing the broader fiscal implications of the Buffett Rule: “Even if it passed, the [Buffett Rule] would not likely make a serious dent in the country’s deficit. It might add up to $162 billion over 10 years. The national debt grows fast enough to wipe that out within two months.”

So $162 billion in budgetary savings is something to laugh at? I’ll remember that next time conservatives propose to reduce the deficit by drug-testing unemployment insurance recipients, eliminating the National Endowment for the Arts, or defunding Planned Parenthood. To be more concrete, these savings would more than supplant the draconian $134 billion 10-year cut to the Supplemental Nutrition Assistance Program (SNAP, formerly food stamps) proposed in the Ryan budget.

Further, the criticism that $162 billion is dwarfed by this year’s budget deficit is doubly misleading. For one, budget deficits have swelled in recent years because the economy is so weak. Comparing a 10-year cost-estimate of just about anything to the sizable but cyclical budget deficits spurred by the worst economic downturn since the Great Depression is unhelpful. Further, policymakers shouldn’t be concerned at all with reducing this year’s budget deficit; serious concerns about budget imbalance are about stabilizing debt in the medium and long-term, after the economy has recovered. Revenue from implementing the Buffett Rule would be weighted toward the out years, where savings will be larger relative to projected budget deficits than today, and that’s exactly how it should be.

Senator Orrin Hatch (R-Utah) echoed this very same misguided sentiment in a statement on the Buffett Rule: “The President’s so-called Buffett Rule is a dog that just won’t hunt. It was designed for no other reason than politics – there is no economic rationale for it. It would do little to bring down the debt…” This specious “if it doesn’t fix the entire problem, it’s not worth doing,” objection to raising more revenue and increasing tax progressivity was similarly trotted out in defense of the upper-income Bush-era tax cuts, the expiration of which would raise $849 billion over a decade. Luckily, Jon Stewart decided to smack at this bad argument. He probably won’t have time to go after this latest Washington Post article, which is a shame because it’s about as silly.

It’s true, the Buffett Rule won’t lower unemployment by itself (but it’s still worth doing)

The National Journal’s Jim Tankersley correctly points out that the Buffett Rule will not, by itself, solve the most pressing economic problem in front of us: the still far too high unemployment rate. Then, bizarrely for Beltway writers talking about the unemployment rate, he also correctly points out what would help lower this rate: increased aggregate demand.

But it doesn’t follow from here that the Buffett Rule is bad policy. In fact, for those who think that we should aggressively target a lower unemployment rate in the near-term while also simultaneously locking in commitments to reduce longer-run budget deficits, the Buffett Rule should be seen as a huge win. However, this is if (and only if) it is accompanied in the next couple of years with aggressive fiscal job-creation measures such as infrastructure spending, aid to states and local governments, and making sure that existing fiscal support (unemployment insurance, food stamps, targeted tax cuts) does not fade away.

Of course, I’m not one of those who think we must only pair near-term measures to lower unemployment with longer-term measures to close the deficit. I’d be happy to take the near-term measures, well, in the near-term and deal with longer-run issues when we can.

And, in fact, it would be optimal from a pure economics perspective to finance aggressive near-term fiscal support with debt in the short-term, rather than (even Buffett Rule-rule style) tax increases. But given the near-universally misplaced D.C. obsession with closing budget deficits, always and everywhere, financing job-creation efforts with the Buffett Rule and other high-income tax cuts makes plenty of sense to me.

Permanent tax increases on upper-income households provide very little drag on near-term recovery, whereas the intelligently-directed fiscal supports noted above have quite large effects. Moody’s Analytics chief economist Mark Zandi pegs the fiscal multiplier (i.e., the increase in GDP stemming from a dollar of spending increases or tax cuts) for infrastructure spending at $1.44, versus $0.35 for permanently extending all the Bush-era tax cuts. This implies that a dollar of infrastructure investment financed by a dollar of permanent tax increases would generate on net $1.09 in economic activity (a balanced-budget-multiplier).

Tankersley concludes his piece, “If the Buffett Rule was a serious pitch to help the jobless, it would deal with one of those main drivers of unemployment. It would boost persistently weak aggregate demand or incentivize business investment.”

Nobody agrees with this general sentiment more than us at EPI – really. But given the mad rush to cut deficits, throwing the Buffett Rule on the table seems awfully smart. It minimizes short-run damage to jobs and growth from reducing the deficit, it can be paired with effective fiscal support to yield extra economic activity and jobs without increasing the deficit, and it locks in a policy that will make our tax system fairer, more efficient, and capable of generating the revenue needed to fund government in the long-run.

Panel on tax fairness and reform helps address common misperceptions

I had the opportunity to participate in an Americans for Democratic Action panel discussion yesterday on tax fairness. The panel, called “Tax Equity: Paying Fair,” was moderated by John Nichols of The Nation and included panelists Bob McIntyre of Citizens for Tax Justice, Mike Lapham of United for a Fair Economy, Dean Baker of the Center for Economic and Policy Research, Elspeth Gilmore of Resource Generation, and Chuck Marr of the Center on Budget and Policy Priorities. It was an honor to participate alongside them.

The panel covered a number of topics, including the Buffett Rule, the Paul Ryan budget, the George W. Bush-era tax cuts, the equalization of tax rates for capital and labor income, corporate tax dodging, and a financial transactions tax. But beyond the wonkier side of tax policy, Baker raised an important point that merits highlighting. He talked about people’s misperceptions regarding how much federal income tax they actually pay—in other words, confusion of marginal tax rates for (lower) effective rates. For example, the second highest tax bracket (33 percent) is assessed for single filers on taxable income between $174,400 and $379,150 (for the tax year 2011 returns due April 17). If you are a single filer with $180,000 in annual taxable income, you do not pay 33 percent on all of your income—as is widely misperceived. You would pay 33 percent only on your total income (less the personal exemption, deductions, and exclusions) exceeding $174,400. In this case, only $5,600 of your total income would be subject to the 33 percent rate.

I was really glad to see Dean Baker bring up the point of marginal versus effective tax rate confusion, because I think widespread misperception unduly adds to public fears of returning to Clinton-era tax rates. Raising the top tax bracket from 35 percent to 39.6 percent will only very marginally impact what high earners pay. Most Americans simply do not make enough to be subject to top income tax rates; President Obama’s proposal to extend the Bush tax cuts for households with less than $200,000 ($250,000 for joint filers) in adjusted gross income—letting only the top two rates expire—would result in a tax increase for only 2.1 percent of households. I was hoping to make a similar point to Baker’s, had there been more time for that in our conversation. I was recently struck by a portrayal of tax rate perceptions and reality in Bruce Bartlett’s new book on tax reform, The Benefit and the Burden. Bartlett draws from a CBS News/New York Times poll from April 14, 2010, that asks the following:

On average, about what percentage of their household incomes would you guess most Americans pay in federal income taxes each year: less than 10 percent, between 10 and 20 percent, between 20 and 30 percent, between 30 and 40 percent, between 40 and 50 percent, or more than 50 percent, or don’t you know enough to say?

The results are depicted below. The respondents indicated they believed 5 percent of Americans pay less than 10 percent of their income in federal income taxes. The reality is 86.5 percent of Americans actually did, in 2010. Additionally, respondents indicated they believed 38 percent of Americans pay over 20 percent of their income in federal income taxes. The reality: Only 0.6 percent of Americans pay over 20 percent of their income in federal income taxes.

| Tax percentage/income | Perception | Reality |

| Less than 10% |

5% |

86.5% |

| 10-20% |

26% |

12.9% |

| 20-30% |

25% |

0.6% |

| 30-40% |

10% |

|

| 40-50% |

2% |

|

| More than 50% |

1% |

|

| Don’t know |

31% |

n/a |

Source: The Benefit and the Burden, 2012

Thank God for trial lawyers

For many years, Corporate America has been waging a campaign to vilify the lawyers who bring suits against them. After decades of knowingly exposing workers and consumers to potentially fatal asbestos, the companies that had profited tried to kill asbestos litigation when lawsuits began to bankrupt them. When tort suits helped workers get real compensation for disabling injuries from unsafe machinery, the corporations moved to bar the suits. When class-action lawsuits proved to be an effective way to bring claims against giant corporate wrongdoers, Congress passed new laws to make such suits more difficult. And when doctors and hospitals began to pay heavily for medical malpractice, they started campaigns in every state and in Congress to limit the damages that could be awarded against them.

All of the harm that corporations and other actors have done to the public—the subjects of so much litigation—could have been better controlled by regulation with real teeth and effective enforcement. Asbestos could have been banned decades ago, as it was in most of Europe. Machines could have been required to have better lock-out mechanisms and better guarding as they were manufactured, to ensure that employees would never be maimed or killed. Drug tests could have been required to be conducted with more independence and transparency, with conflicts of interest prevented. And hospitals could be regulated to prevent unnecessary infections, misadministration of medicines, and surgery on the wrong patient or wrong limb.

But our political culture resists regulation, and even when we have regulation, the government does not always enforce it energetically. Thus, we do have a law and regulations that forbid for-profit employers from employing workers without paying them the minimum wage. And those regulations forbid the employment of students or anyone else as interns (except in very limited circumstances) without paying the minimum wage. The Department of Labor, however, does almost nothing to enforce the law in this area. Moreover, the token penalties in this and most areas of labor law lead companies to treat them as a cost of doing business.

So I was delighted to see the trial bar take this issue on, with a highly respected New York law firm suing Fox Searchlight and Hearst Corporation for failing to pay various employees the corporations called “interns,” including college graduates and even a CPA.

The effect of these suits has been salutary! Already, the media report that other employers have taken notice and law firms are now advising clients not to break the law. One USA Today headline read, “Fewer Unpaid Internships to Be Offered.”

I hope the headline is accurate, and if it is, it will be due to the efforts of Outen and Golden, LLP. The New York law firm is doing the work our government ought to be doing.

Thank God for trial lawyers.

Robert Lawrence misleads the New York Times on manufacturing

Last week, Eduardo Porter wrote in the New York Times’ Economix blog about a response he received on his recent piece on manufacturing from Robert Lawrence of the Kennedy School. Porter should have dug into the topic further because what Lawrence wrote was rather misleading. Here are Porter’s words:

“Prof. Robert Lawrence from Harvard makes an interesting point in response to my Wednesday column about our misplaced hopes in manufacturing as a source of new jobs: even if every single thing we bought was “made in America” — if we stopped multinationals from outsourcing production to China and closed our doors to imports — even then, manufacturing employment would lag.

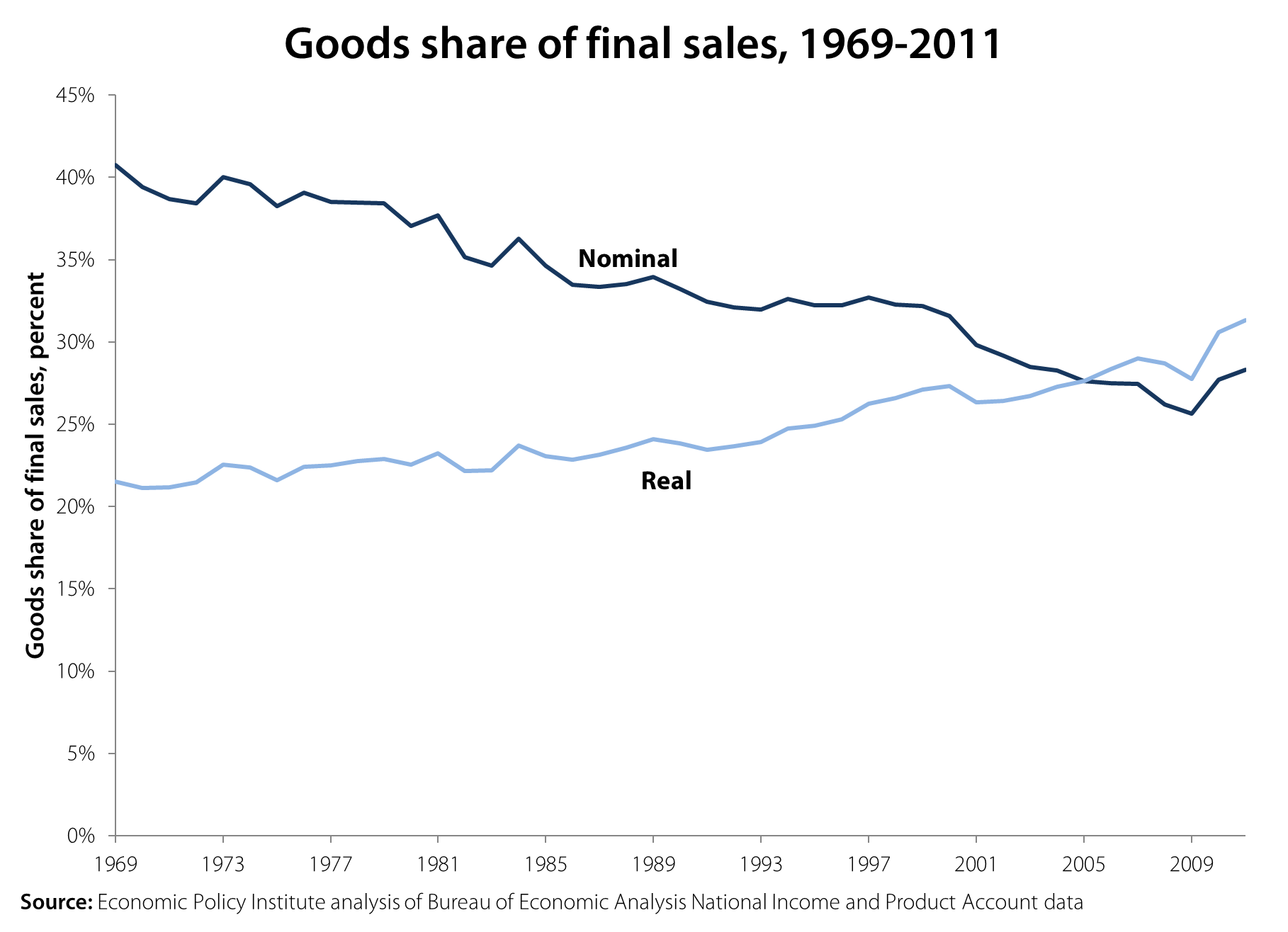

The reason is simple: we are spending less and less on goods and more and more on services. In 1969, American consumers were allocating half of all their spending on consumption to goods. By 2010, that share had fallen to one-third.”

Lawrence clearly wants people to believe that manufacturing jobs are declining because “we” just don’t buy much manufactured stuff anymore, or, in economic terms that there’s less demand for goods now than in the past. But that’s wrong, for a couple of reasons. First, goods are not only produced for household consumption, they are also produced for business and public investment, and for export. Second, and more importantly, the prices of goods have fallen relative to other types of products, so the goods share of total nominal (not inflation-adjusted) spending might fall, but the share in real (inflation-adjusted) spending might not follow. Or, to put it simply, people might have more TVs in their homes than ever before even while the share of their total income they spend on TVs has fallen. But, nobody would describe this state as a declining demand for TVs.

The following graph shows the share of goods in final sales of domestic products (the Bureau of Economic Analysis provides data on major types of products, dividing final sales into goods, services and structures. See NIPA Tables 1.2.5 and 1.2.6). The goods share of final sales in nominal terms did fall from 40.8 percent in 1969 to 28.3 percent in 2011, a roughly 30 percent decline in relative spending. However, the share of goods in real final sales actually rose 50 percent from 21.5 percent in 1969 to 31.3 percent in 2011. This means that the economy was even more goods-intensive in 2011 than in 1969 and that it was not a relative decline in the demand for goods that caused the shrinkage of manufacturing employment.

In the end, manufacturing employment is a horse race between demand for manufactured goods (which boosts jobs) and productivity (which, all else equal, means fewer jobs are needed in the sector). One thing that this analysis should remind us of is that even faster productivity has its upside: As prices fall because productivity rises in this sector, people demand more manufactured goods.

It should be noted, however, that neither Porter nor Lawrence denies that lowering the trade deficit would boost jobs. Rather, Porter says that even without any imports, manufacturing employment would lag. Lawrence, meanwhile, says that even without a trade deficit, goods employment would fall. In reality, closing the trade deficit would provide millions of jobs and boost the economy. For instance, my colleague Robert Scott has shown that growing trade deficits with China eliminated 2.8 million U.S. jobs between 2001 and 2010 alone, including 1.9 million jobs displaced from manufacturing. Similarly, correcting the currency imbalances with China, Hong Kong, Taiwan, Singapore, and Malaysia could add up to $285.7 billion (1.9 percent) to U.S. GDP, create up to 2.25 million jobs over the next 18 to 24 months (most in manufacturing), and reduce U.S. budget deficits by up to $71.4 billion per year.

Moreover, as Scott’s recent blog post notes, the recent recession was especially hard on manufacturing (we lost 2.3 million jobs between 2007 and Jan. 2010) and we can get those jobs back in a robust recovery.

So, sure, manufacturing employment will not return to 25 percent of employment. Nevertheless, we can gain a lot of manufacturing jobs by strengthening the recovery and through appropriate trade and currency policy. This would provide millions of good jobs, aid many communities, and be good for the nation. No head-fakes about household consumption shares should distract us from these facts.

Latinos versus the Census Bureau: When racial categorizations clash

People create races, not nature. Different societies tend to have different systems of racial categorization. Even within the same society, there can be significant changes in racial categorization over time. We can get a sense of this from the fact that U.S. Census Bureau has made changes to the rules for racial classification system in nearly every census.

The guidelines for the 1940 Census (the full data of which was recently released to the public) instructed enumerators that “any mixtures of white and nonwhite blood” should be classified as nonwhite. Additionally, people of “mixed Negro and Indian blood should be reported as Negro” while “other mixtures of nonwhite parentage should be reported according to the race of the father.” These rules only make sense when embedded in the specific U.S. political economy of slavery and Jim Crow.

Today, in post-Civil-Rights-era America, individuals define their own race, not the Census enumerators. Also, in response to lobbying for multiracial categorization, since 2000 the Census Bureau has allowed individuals to select more than one race. In 1940, multiracial categorization in Census data was not possible.

Over the past few decades, the United States has seen a significant increase in the Latino population. Many of these Latinos are immigrants from other countries with other systems of identity and racial classification. These systems of classification may be in conflict with the official directives of the Census Bureau.

According to the Census Bureau, being Hispanic or Latino is an ethnic classification, not a racial classification. For perhaps as much as half of the Latino population, however, Latino is a racial category. A new survey from the Pew Hispanic Center illustrates this fact. When asked “Which of the following describes your race?”, 25 percent of Latinos answered “Hispanic or Latino.” Another 26 percent chose “Some other race”–rejecting the Census-Bureau-recognized racial categories of “white,” “black,” and “Asian.” While some of these “Some other races” may have been looking for “American Indian,” it is doubtful that all or even a majority of them were. They were looking for some racial category that the Census Bureau does not offer.

For many Latinos, “Latino” is understood as a racial category or as something other than an ethnic category in the sense that the Census Bureau intends. The idea of a cultural racial category is not an uncommon one. Nazi Germany, notoriously, institutionalized the category of a Jewish race. In Japan, there is the idea of a Japanese race which would distinguish them not only from non-Asian groups, but from other Asians as well. Groups that are conceptualized as cultural in the United States can be conceptualized as racial elsewhere.

Recently, NPR described George Zimmerman as a “white Latino,” but many of their listeners were confused by the term. This is interesting since according to data from the 2010 census 53 percent of Latinos are white.

The Pew Hispanic Center survey shows us that many Latinos see their group as something akin to a racial group. But the survey does not tell us how non-Latinos perceive and classify Latinos. Do non-Latinos perceive Latinos to be a separate race, an ethnic group, or something else? Latinos’ future in the United States depends not only on how they perceive themselves, but also on how others perceive, classify, and ultimately treat them. One hopes that a future Pew Hispanic Center survey will ask these questions.

Memo to the Times: Hold the funeral march for U.S. manufacturing

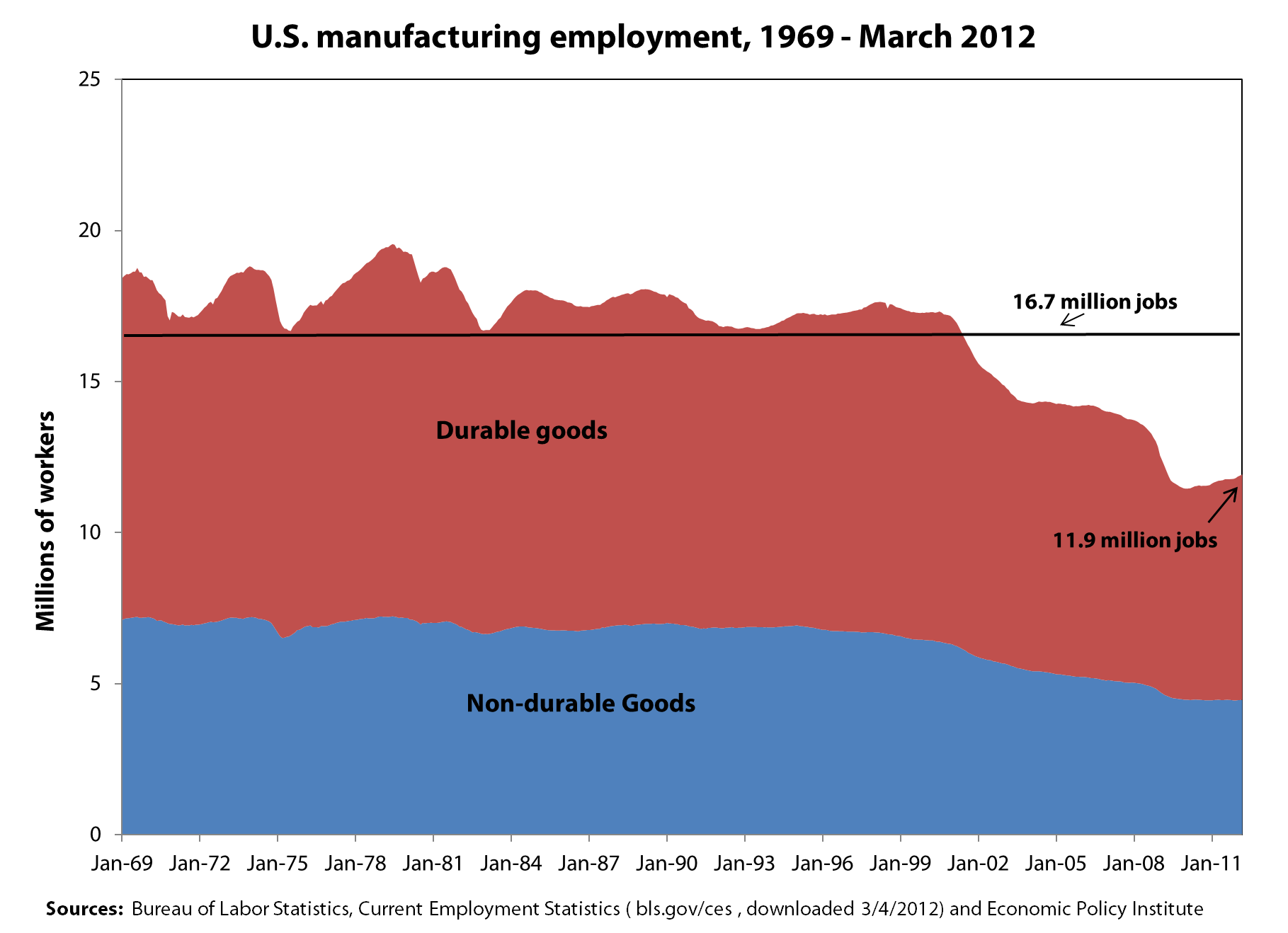

A recent commentary by Eduardo Porter in the New York Times claims that a “revolution in manufacturing employment seems far-fetched,” despite the recent recovery of manufacturing employment. Porter then proceeds to pound nails in manufacturing’s supposed coffin, claiming that “most of the factory jobs lost over the last three decades in this country are gone for good. In truth, they are not even very good jobs.” Perhaps not for a physicist like Porter, but manufacturing does provide excellent wages and benefits for many working Americans. And, with 11.9 million jobs today, U.S. manufacturing is very much alive and kicking.

Laura D’Andrea Tyson got the wage issue right in Why Manufacturing Still Matters, a post she wrote for the Times’ Economix blog in February. She notes that manufacturing jobs are “high-productivity, high value-added jobs with good pay and benefits.” According to Tyson, in 2009, “the average manufacturing worker earned $74, 447 in annual pay and benefits, compared with $63,122 for the average non-manufacturing worker.”1 Manufacturing wages and benefits are particularly attractive for workers without a college degree, for whom the alternative is often a job at low pay with no benefits.

Porter is also wrong to suggest that manufacturing employment has been on a downward trend for three decades (see graph below). In fact, manufacturing employment was relatively stable between 1969 and 2000, generally ranging between 16.7 million and 19.6 million workers. During this period, employment in big-ticket, durable goods industries such as autos and aerospace was more volatile than employment in non-durable goods. Starting from a peak in early 1998, U.S. manufacturing declined rapidly after the Asian financial crisis (which caused widespread devaluations in Asia), and total employment in both durable and non-durable goods began a sharp drop. This decline was associated with the rapid growth of the U.S. trade deficit, especially with China. Growing trade deficits with China eliminated 2.8 million U.S. jobs between 2001 and 2010 alone, including 1.9 million jobs displaced from manufacturing. Thus, U.S. job losses in manufacturing are really just a phenomenon of the past decade.2

Manufacturing has been hit with two distinct waves of job losses since 2000. Between 2000 and 2007, growing trade deficits were largely responsible for the loss of 3.9 million manufacturing jobs. In this period, employment declined in both non-durables (-20.3 percent) and durables (-19.8 percent) at similar rates. The great recession eliminated another 2.3 million jobs between 2007 and Jan. 2010 as the demand for cars and other manufactured goods collapsed. Employment in durable goods was hit especially hard by the recession, falling an additional 19.7 percent, while employment in durables fell 11.3 percent. However, since the end of the recession, employment in the two sectors has behaved in very different ways, as shown in the graph. Non-durable employment has remained essentially flat, adding only 5,000 jobs (0.1 percent) over the past 26 months, while durable goods industries have added 454,000 jobs (6.7 percent).

It does seem unlikely that the U.S. will recover many jobs in apparel or footwear. However, the non-durables sector also includes chemicals, pharmaceuticals, and petroleum refining. The U.S. exports large amounts of those commodities, and they certainly support the kind of high value-added, high-wage jobs Tyson described.

Durable goods industries such as aerospace products, machine tools, electronics, and motor vehicles and parts also support lots of exports, and those industries could grow with support of appropriate trade and industrial policies. Countries such as Japan and Germany have managed to support large and growing trade surpluses, especially in those sectors, because the vast majority of their exports are manufactured products. And, contrary to Porter’s assertions, they have lost a much smaller share of their manufacturing jobs than the United States. According to OECD statistics, between 2000 and 2009 (from peak to the trough of the recession), Germany lost fewer than 700,000 manufacturing jobs (an 8.3 percent decline). Japan lost 2.1 million (-17.4 percent), and the United States lost 5.7 million (-30.2 percent). The U.S. suffered nearly twice as much manufacturing job loss as Japan, and nearly four times as much as Germany.

Manufacturing employment in each of these countries has been hurt by the recession (although Germany, for example, did much more to prevent manufacturing job loss during the downturn), but the big difference is trade. In the German “Kurzarbeit,” or short work program, firms cut workers’ hours rather than make big layoffs, and the government helps make up the difference in workers’ paychecks (rather than paying unemployment compensation), thus limiting mass unemployment and stabilizing the economy. Growing trade deficits eliminated millions of manufacturing jobs in the United States, while growing trade surpluses helped support manufacturing jobs in Japan and Germany. It didn’t have to be that way, and we can recover lost manufacturing jobs in the future, especially in high-wage, durable goods industries. Read more