DHS initiative for young unauthorized immigrants is cost-effective and benefits American workers

Next week, about 1.2 million young people who reside in the United States without proper authorization—but who were brought here by their parents when they were children—will be eligible to apply to the Department of Homeland Security (DHS) for a discretionary grant of relief from removal (also known as deportation). This relief will be valid for two years and renewable in two-year increments. If granted, beneficiaries would also be eligible for an Employment Authorization Document, which would allow them to work legally in the United States with full labor and employment rights. This will clearly benefit the American workforce, and it’s unlikely to cost a dime of taxpayer money.

On Tuesday, the Migration Policy Institute (MPI) hosted a forum to discuss how DHS’s new process—known officially as the Deferred Action for Childhood Arrivals (DACA) initiative—will function in practice. The keynote speaker was Alejandro Mayorkas, Director of U.S. Citizenship and Immigration Services (USCIS), which is the DHS agency that will process and adjudicate DACA applications. Mayorkas outlined the programmatic aspects of the initiative and its requirements, and four immigration experts offered their thoughts in response. It was a valuable discussion that shed some much-needed light on DACA.

We know from multiple reports that many of those who will seek this type of relief from removal are some of the best and brightest students—and future workers—our country has to offer. They arrived in the United States through no fault of their own, and it would be unjust to send them to a country they barely know or do not remember, and where many would not even know the language. They deserve to stay here and to become Americans, and to be allowed to contribute to our labor market. But despite bipartisan support and a decade’s worth of bipartisan proposals in Congress, gridlock and obstructionism have blocked a solution that would grant them a permanent status. That’s one of the reasons why President Obama announced on June 15 that his administration would use its discretionary administrative authority to refrain from removing young unauthorized immigrants who are not criminals and pose no threat to national security.

However, it is clear that USCIS has quite a task on its hands. Read more

For-profit colleges have the poorest students and richest leaders

For-profit colleges prey on the poorest students while generating a great deal of wealth to shareholders, owners, and CEOs. Figure A shows that in 2008, the median family income of students attending for-profit colleges was $22,932. This amount is only slightly higher than the U.S. Census Bureau’s poverty threshold for a family of four. The families of students at public colleges had about twice as much income, and those at private non-profit colleges nearly three times as much.

Despite having the poorest student bodies, the CEOs running for-profit education companies earn far more than the richest leaders of traditional public and private colleges and universities. CEOs of publicly-traded for-profit education companies had an average compensation of $7.3 million in 2009, while the richest five leaders of private non-profit colleges and universities had an average compensation of $3 million (Figure B). The richest five leaders of public universities had an average compensation of $1 million.

For-profit colleges are so profitable because they charge very high tuition and invest rather little in education. Among for-profit college students, 96 percent take out student loans to pay for their education, a much higher rate than at other colleges. Since most of these loans are from the Department of Education financial aid program or U.S. military educational programs, it is ultimately taxpayers who are paying these CEOs’ salaries. These students who were already low-income often end up saddled with a very large amount of debt. Since student loan debt cannot be expunged even through bankruptcy, these debts can be “a lifelong drag on people who already are struggling.”

High cost and high debt for students at for-profit colleges

For-profit colleges tend to enroll students who are not familiar with traditional higher education. They are more likely to be low-income, African American or Latino. Significant numbers of veterans also enroll in these schools. The Senate Committee on Health, Education, Labor, and Pensions found that recruiters “were trained to locate and push on the pain in students’ lives.” Additionally, undercover recordings by the Government Accountability Office and other sources show that many for-profit college recruiters “misled prospective students with regard to the cost of the program, the availability and obligations of Federal aid, the time to complete the program, the completion rates of other students, the job placement rate of other students, the transferability of the credit, or the reputation and accreditation of the school.”

This combination of naïve students and misleading information allows for-profit colleges to set tuition in line with their profit goals (many of these colleges are publicly-traded companies) rather than in line with the cost of education. Figure A shows that the average cost of a certificate program at a for-profit college is 4.7 times the cost of an equivalent program at a public community college. The average cost of an associate degree is 4.2 times what it would cost at a typical community college. Bachelor’s degree programs average 19 percent higher at a for-profit college than at a flagship state public university.

Investment, employment trends belie claims that regulation and ‘too much government’ impede recovery

The claim that an excess of regulatory activity is stifling the economy and jobs growth continues to ignore the roots of the economy’s problems (the collapse of the housing and financial sectors) and the reality of current economic trends. We will save discussion of the causes of the downturn for a different day, except for noting the irony that regulatory opponents are fighting implementation of the stronger financial rules that could help prevent future collapses. Instead, we will update key information from a previous EPI analysis of whether business decisions, specifically investments, are consistent with the excessive regulation story. The earlier report documented that “what employers are doing in terms of hiring and investment” was inconsistent with business claims that regulatory uncertainty under the Obama administration was impeding job growth. The new data include four additional quarters of results and also take into account revisions to the earlier data that were made available in late July (the Bureau of Economic Analysis annual benchmarking of the National Income and Product Accounts data leads to some revisions). Altogether, we are now able to compare investment trends during the first 12 quarters (or three years) of this recovery to the first 12 quarters of the three prior recoveries.

Of particular interest is whether businesses are holding back from investing in equipment and software because of fears of new or potential regulations. This investment category leaves out residential investment and investments in business “structures”—because those types of investments are clearly faltering as a result of the bursting of the residential and commercial real estate bubble (and not because of regulatory activity).

As a share of the economy, the data show that equipment and software investment has increased more in this recovery than in the three prior recoveries. Indeed, three years into this recovery the growth of 1.6 percentage points in the share of GDP going to investment in equipment and software is more than twice as large as the growth during the first three years of either the George W. Bush or the Reagan recoveries. That means that this recovery, with the Obama regulatory approach, is far more investment-led than the recoveries under the generally deregulatory Bush and Reagan administrations.

Keep your government hands on my Medicare!

Celebrating Medicare and Medicaid’s 47th birthday this week, here are some quick thoughts on government’s role in ensuring access to affordable health care:

- The United States spends nearly double what other countries spend. Americans spent a total of around $7,600 per person on health care in 2010, compared with around $3,900 on average for countries with similar standards of living, according to the Kaiser Family Foundation. Despite this higher spending, health outcomes are no better than in other developed countries.

- Government picks up nearly half the tab. As fewer Americans are covered by employer-sponsored insurance, government has taken up the slack. State and federal programs now directly or indirectly cover 45 percent of health care costs in the United States.

- High and rising health care costs are the biggest fiscal challenge our country faces. The Congressional Budget Office (CBO) projects that federal spending on major health programs will increase from 7.4 percent of GDP in 2022 to 10.4 percent in 2037 if current policies remain in place. Nearly two-thirds of this increase is due to the assumption that per capita health care expenditures will grow faster than per capita GDP. In the absence of this excess cost inflation, spending on these programs would increase to a more manageable 8.6 percent of GDP in 2037, largely reflecting the long-anticipated baby boomer retirement. Read more

The folly of the GOP’s ‘tax reform’ agenda

Mitt Romney and House Budget Committee Chairman Paul Ryan (R-Wis.) are both pushing “tax reform” plans that would lower marginal tax rates while broadening the base (curbing tax deductions, credits, and exclusions). Romney’s plan, for example, would reduce all individual income tax rates by a fifth—e.g., the top 35 percent rate would fall to 28 percent—and the revenue loss would be made up by limiting or eliminating unspecified tax expenditures. And he says he would do this without cutting taxes for high-income households (beyond continuing their Bush-era tax cuts), meaning that he would more or less preserve the progressivity of the current tax code (i.e., tax burden distribution).

For the moment, let’s leave aside the fact that these plans neglect to raise a dollar in additional revenue at a time when we need more revenue to put the government on a sustainable fiscal path. Why are these proposals pure folly? First, because they’re obviously not serious—if they were, the plans would lead with the tax expenditure reform rather than the rate cuts. Instead, they’re sold in manner suggesting that Romney and Ryan wanted to propose big across-the-board tax cuts but didn’t want to be seen as blowing up the deficit, so they included vague language on base-broadening in order to ignore the monumental cost of slashing tax rates.

But most importantly, these plans aren’t serious because their stated intent isn’t mathematically possible. In an analysis released Wednesday, researchers at Brookings and the Tax Policy Center analyzed a plan that is consistent with Romney’s proposal, including lowering rates by a fifth and eliminating the Alternative Minimum Tax. The researchers then attempted to construct a base-broadening approach to both make up the revenue lost from the rate cuts and maintain the progressivity of the current tax code. Read more

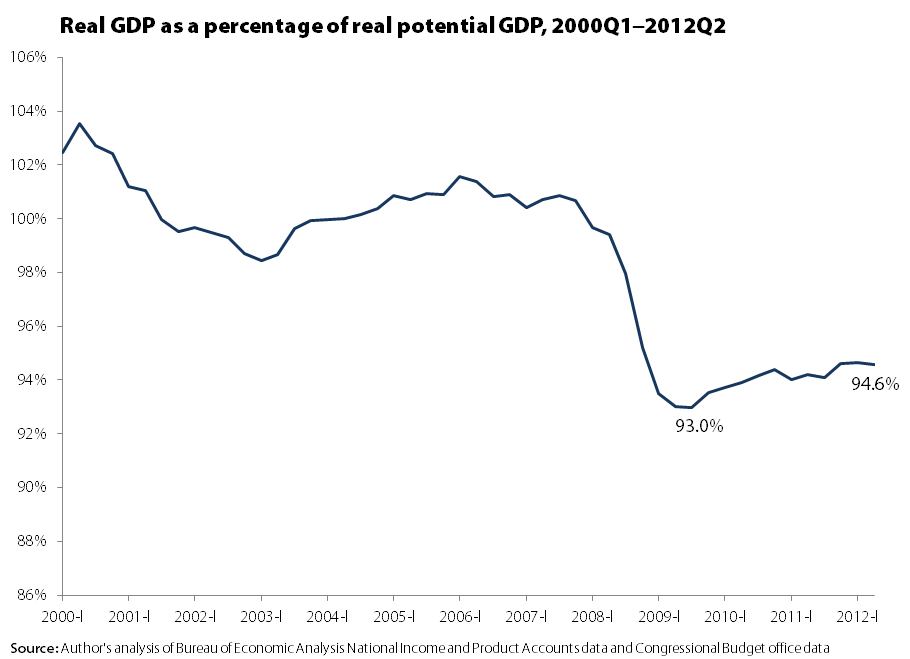

Potential failure

Today’s report on gross domestic product (GDP) came with more news of disappointing growth. The economy has grown at an average rate of 1.75 percent so far this year. While the economy is growing and we are not in a recession (and there’s no sign a recession is imminent), it is important to note that this slow growth is not moving the economy much closer to full health, and may even be doing real damage to that long-run health.

This problem can be highlighted by looking at actual GDP as a percentage of “potential ” GDP, a figure provided by the Congressional Budget Office. Potential GDP can be thought of as a capacity utilization rate for the whole economy: If we were utilizing all of our resources, including labor and capital, how much economic output would we be able to produce?

You can see that in 2000, actual and potential were roughly similar (actual slightly exceeds potential, in fact, because the CBO has a too-conservative view of what is the lowest sustainable rate of unemployment), but then this ratio crashes as the Great Recession hits.

At the trough of the recession in the third quarter of 2009, the U.S. economy was operating at only 93 percent of potential. In the nearly three years since, we’ve only recouped an additional 1.6 percent of potential output. Although GDP has been growing in that period, potential has been growing too (and faster), because of our increasing potential labor force and productivity growth.

Investigations reveal forced labor of immigrants but Congress won’t allow the Labor Department to combat it

Congress holds the keys to fixing many of the problems in one of the main temporary foreign worker programs used by employers to displace U.S. workers, depress wages, and exploit foreign workers. The Department of Labor has already issued the important fixes, but they’ve been temporarily enjoined by a federal court. However, going forward, Congress is considering nullifying the rules entirely by denying funding for their implementation.

The program in question is the H-2B guest worker program. On Tuesday, I joined the Southern Poverty Law Center (SPLC), the AFL-CIO, and two H-2B guest workers from Central America at the National Press Club to call on Congress to help unemployed workers have increased access to jobs in a number of occupations—including landscaping, hospitality, forestry, and seafood processing—by allowing the DOL’s new rules governing the H-2B program to come into force. The new rules would require employers to first recruit unemployed workers before turning to foreign workers, ensure that U.S. and foreign workers are not underpaid, and protect guest workers from becoming victims of forced labor and human trafficking, as well as from being retaliated against if they attempt to assert their labor and employment rights.

Although the new rules include common sense protections for U.S. and foreign guest workers, they are far from extreme or burdensome. If anything, the rules and requirements on employers are quite basic and modest.

Recently, the scandalous side of the H-2B program received some well-deserved attention from the media. A few weeks ago, a New York Times editorial, “Forced Labor on American Shores,” offered a powerful and depressing reminder that the days of forced labor (also known as slavery) are still with us. In fact, the H-2B guest worker program helps facilitate it, and in the editorial’s case, forced labor was occurring for the benefit of Walmart, the largest private employer in the world, by C.J.’s Seafood, one of its suppliers. Walmart’s size and purchasing power give it leverage to demand the lowest prices possible from its vendors and manufacturers. This in turn, can motivate suppliers like C.J.’s in Louisiana to exploit and abuse their workers in order to bring down labor costs. Read more

Confirming the further redistribution of wealth upward

A new Congressional Research Service report by Linda Levine is the first update on the distribution of wealth (including that of the top 1 percent) I’ve seen based on the recently released Federal Reserve Board (FRB) data on wealth for 2010. Levine’s analysis (see two of her tables below) shows a large upward change in the distribution of wealth over 2007-2010, with losses in the bottom 90 percent and large gains for the top 10 percent. Specifically, the bottom 90 percent in 2010 had just 25.4 percent of all wealth, down from 28.5 percent in 2007. The gainers were primarily those in the 90-to-99th percentiles (up 2.3 percentage points) of wealth, though the top 1 percent saw gains (up 0.7 percentage points) too. Levine’s data goes back to 1989 and show the wealth share of the bottom 90 percent to be at its lowest in 2010, far lower than the 32.9 percent share in both 1989 and 1992.

Levine reports data directly from the FRB showing that average wealth is down from 2007 but still far greater in 2010 ( $498,800) than in 1989 ($313,600) or 1992 ($282,900). In contrast, the wealth of the median household (wealthier than half of households but less wealthy than the other half) in 2010 was $77,300, not much different than in 1989 ($79,100) or 1992 ($75,100). In other words, wealth grew 59 percent from 1989 to 2007, but the typical household’s wealth was actually 2 percent less.

This is yet another dimension of the same old story about the economy being able to provide for most people but failing to do so, a story that will be told more fully in the forthcoming State of Working America (being released in late August). The new edition will include a more detailed report on wealth distribution from 1962 to 2010, based on an analysis by New York University’s Edward Wolff (see the last report, written by Sylvia Allegretto).

Happy birthday, CFPB

Tomorrow, the Consumer Financial Protection Bureau completes its first year of operation. Created under the Dodd-Frank Act, we’re starting to see the benefits of a strong federal agency that protects consumers from the dangers posed by an unchecked financial industry.

The CFPB notched its first enforcement action—and hopefully, the first of many—yesterday with the announcement that Capital One will pay up to $210 million to settle federal charges that it violated consumer protection requirements. According to CFPB charges, Capital One used “deceptive practices” to sell unnecessary add-ons to credit card holders. Between $140 million and $150 million will be paid to the two million customers affected. Capital One will pay another $60 million in fines, with $25 million going to the CFPB and $35 million to the bank-regulating Office of the Comptroller of the Currency.

Today, the CFPB followed up this victory with the release of a report on the private student loan industry, to which American consumers owe more than $150 billion in debt. The extensive report identifies several consumer protection issues in the private student loan marketplace. Importantly, though, the report doesn’t just stop there: It includes strong congressional policy recommendations by CFPB Director Richard Cordray and Secretary of Education Arne Duncan.

These actions by the CFPB are encouraging, but the history of financial regulation teaches us that the real challenge is maintaining vigilance over time. This means keeping up with financial intermediaries’ attempts to arbitrage between different regulatory agencies, bypass current regulatory structures, and capture regulating agencies. The CFPB had a good first year, but the real challenges will appear in the years to come.