Modest Income Growth in 2013 Puts Slight Dent in More than a Decade of Income Losses

Wage trends greatly determine how fast incomes at the middle and bottom grow, as well as the overall path of income inequality, as we argued in Raising America’s Pay. This is for the simple reason that most households, including those with low incomes, rely on labor earnings for the vast majority of their income. That is why my initial look at the data from the newly released Census Bureau report on income and, poverty in 2013 will look at wages and the incomes of working age households.

The Census data show that from 2012 to 2013, median household income for non-elderly households (those with a head of household younger than 65 years old) increased 0.4 percent from $58,186 to $58,448. However, that modest growth barely begins to offset the losses incurred during the Great Recession or the losses that prevailed in the prior business cycle from 2000 to 2007. Between 2007 and 2013, median household income for non-elderly households dropped from $63,527 to $58,448, a decline of $5,079, or 8.0 percent. Furthermore, the disappointing trends of the Great Recession and its aftermath come on the heels of the weak labor market from 2000-2007, where the median income of non-elderly households fell significantly, from $65,785 to $63,527, the first time in the post-war period that incomes failed to grow over a business cycle. Altogether, from 2000 to 2013, median income for non-elderly households fell from $65,785 to $58,448, a decline of $7,337, or 11.2 percent.

Real median household income, all and non-elderly, 1979–2013

| All households | Non-elderly households | |

|---|---|---|

| Jan-1979 | $49,225 | |

| Jan-1980 | $47,668 | |

| Jan-1981 | $46,876 | |

| Jan-1982 | $46,752 | |

| Jan-1983 | $46,425 | |

| Jan-1984 | $47,867 | |

| Jan-1985 | $48,761 | |

| Jan-1986 | $50,487 | |

| Jan-1987 | $51,121 | |

| Jan-1988 | $51,514 | |

| Jan-1989 | $52,432 | |

| Jan-1990 | $51,735 | |

| Jan-1991 | $50,249 | |

| Jan-1992 | $49,836 | |

| Jan-1993 | $49,594 | |

| Jan-1994 | $50,147 | $57,893 |

| Jan-1995 | $51,719 | $59,417 |

| Jan-1996 | $52,472 | $60,527 |

| Jan-1997 | $53,551 | $61,307 |

| Jan-1998 | $55,497 | $63,792 |

| Jan-1999 | $56,895 | $65,435 |

| Jan-2000 | $56,801 | $65,785 |

| Jan-2001 | $55,562 | $64,772 |

| Jan-2002 | $54,914 | $64,108 |

| Jan-2003 | $54,865 | $63,545 |

| Jan-2004 | $54,674 | $62,801 |

| Jan-2005 | $55,278 | $62,391 |

| Jan-2006 | $55,690 | $63,228 |

| Jan-2007 | $56,435 | $63,527 |

| Jan-2008 | $54,424 | $61,443 |

| Jan-2009 | $54,059 | $60,623 |

| Jan-2010 | $52,646 | $59,057 |

| Jan-2011 | $51,843 | $57,627 |

| Jan-2012 | $51,758 | $58,186 |

| Jan-2013 | $51,939 | $58,448 |

Note: Non-elderly households are those in which the head of household is younger than age 65. Data for non-elderly households are not available prior to 1994. Shaded areas denote recessions.

Source: EPI analysis of Current Population Survey Annual Social and Economic Supplement Historical Income Tables (Tables H-5 and HINC-02)

What to Look for in next Week’s Census Income Data: How Long Will It Take to Claw Back Lost Years of Income Growth?

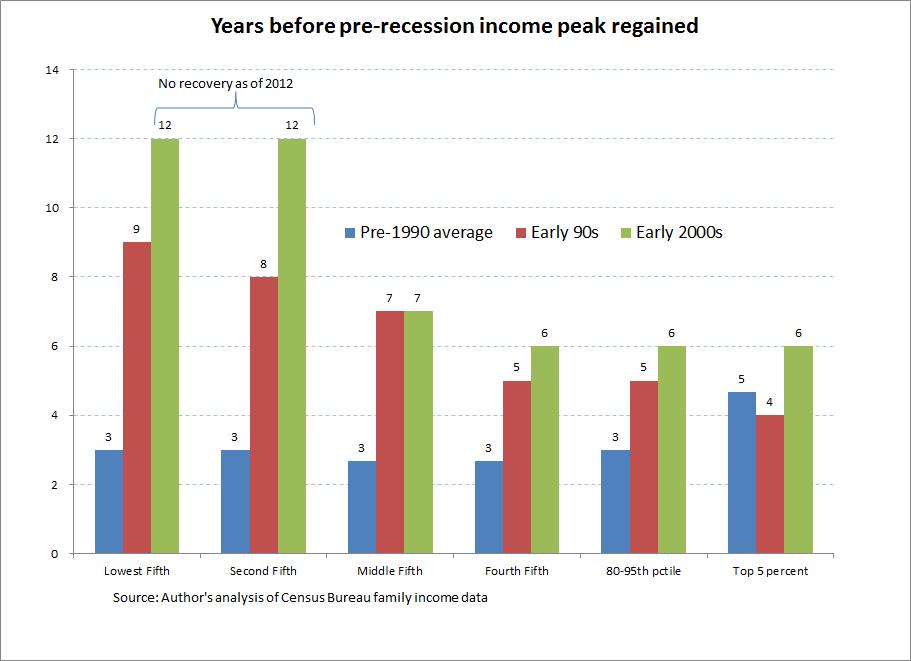

Next week will see the release of Census data on family income (as well as poverty and health insurance coverage) for 2013. Before the data are released, it’s worth reminding ourselves of one thing that last year’s data showed clearly: economic recoveries in recent recessions have been increasingly unequal, largely mirroring the generation-long upwards march of income inequality more generally. And this pattern seems poised to continue in the recovery from the Great Recession.

The figure below shows these unequal recoveries from recessions in a potentially new way. It essentially looks at just how many years of income growth were lost by each income grouping in various recessions. It measures this by simply counting how many years it took after a recession for each group to regain its previous income peak. For example, incomes for the middle fifth saw a peak in 1989 at $62,212. The recession in the following year led average income for these middle-fifth families to fall for a time, and the 1989 peak of $62,212 was not re-gained for these families until 1996, meaning that essentially seven years (from 1989 to 1996) of income growth for this group was stalled by the recession of the early 1990s. The figure below shows this number of lost years of income growth by income grouping across a range of recessions.

NAM’s “Cost of Regulations” Estimate: An Exercise in How Not to Do Convincing Empirics

The latest effort to scaremonger about a rising regulatory burden on U.S. business was released yesterday by the National Association of Manufacturers (NAM). The report, by W. Mark Crain and Nicole V. Crain (C&C, henceforth) purports to (among other things) estimate the total cost of U.S. regulations. The claimed price tag is enormous—$2.1 trillion. The bulk of these costs (75 percent) are estimated using a cross-country regression analysis. This cross-country analysis, however, is completely unconvincing and should be ignored.

An earlier C&C study used a similar methodology as yesterday’s release—that study was shown to be deeply flawed by an EPI analysis. Yet, the methodology of the current study is largely the same. In fact, if anything, the current analysis is less robust and convincing than the previous one.

C&C undertake a cross-country regression analysis across 34 OECD countries for the years 2006–2013. This obviously leads to a first reason for being wary of results—one would expect the economic performance of rich countries during the 2006–2013 period to be utterly dominated by the Great Recession and its aftermath. C&C use dummy variables to control for the years 2008 and 2009, presumably to capture the official years of the Great Recession. But most of the OECD remains operating far below potential even in 2013 due simply to a shortfall of demand. Unless one is making the case that regulations impede recovery from recessions (a claim that they do not make) then it is extraordinarily hard to make large inferences about the effects of regulations on long-run economic performance in this short sample period.

NAM Publishes Bogus Regulatory Cost Estimates

The National Association of Manufacturers (NAM) is a cynical organization. It knows that few journalists will read a lengthy paper on the cost of regulation and realize that it is dressed-up junk economics, so it has published a re-run of the truly meretricious report that Mark Crain and Nicole Crain issued four years ago. The new report is even worse than its predecessor, in the sense that the authors have chosen not to respond to any of the criticism of their earlier work—even though it has been shown to be based on bad research, unreviewable and probably biased data, and faulty assumptions about the relationship between regulation and GDP.

EPI’s Josh Bivens and others will deal with the main methodological problems with the Crains’ analysis. I want to focus just on the Crains’ re-use of the same indefensible research concerning the cost of OSHA regulation, which we first exposed in 2011. The Crains claim that OSHA regulations cost businesses $71 billion a year, even though the cost for new regulations since 2001 is only $733 million. How is it that the previous years’ regulation cost nearly 100 times as much? The Crains don’t have an explanation—they simply rely on someone else’s discredited work.

Joseph M. Johnson published “A Review and Synthesis of the Cost of Workplace Regulations” in 2005. Johnson’s paper makes many serious mistakes, but the biggest is the application of a cost “multiplier” derived from yet another analyst’s work. Harvey S. James, Jr. estimated that the true cost of OSHA rules is not the cost estimated by the agency at the time of rulemaking (which often turns out, in reality, to be too high), but a cost 5.5 times greater because of “fines for violations and the costs of the many non-major regulations for which no cost estimates exist.” This multiplier is ludicrous on its face, both because OSHA fines have never amounted to very much (even today the maximum fine that can be assessed for a willful or repeat violation is only $70,000, and the amount paid is usually far less than what is initially assessed) and because the costs of non-compliance should not be double-counted as compliance costs.

Here’s Why We Need to Legalize the Undocumented Immigrant Workforce

The Tennessean reported yesterday on the miserable work life of a 17-year old migrant worker named Ivan Alvarez, who lost three fingers when a tobacco farmer’s makeshift shearing machine sliced them off. How did the farmer treat him? He gave him a check for $100 and fired him. No worker’s compensation, no disability insurance, and no compassion.

Young Alvarez was one of six migrant teenagers working at Marty Coley Farms in Macon County, Tennessee. He lived with 13 adult men in a vermin-infested three-bedroom house, and was paid less than minimum wage for six days a week of work. Why did Alvarez and the others put up with such mistreatment? As undocumented immigrants, they were trapped.

A recorded conversation between the farm’s owner and one of the employees after the amputation shows how employers use the threat of deportation to oppress their workers and drive labor standards to the bottom. When the worker said he was leaving to take a better-paying job at another farm, the farmer, Marty Coley (one of the largest tobacco growers in the county), threatened him with deportation.

“I’ll tell you what,” Coley said. “You all go there and I’m going to call immigration and clean the whole damn bunch out.”

It adds insult to injury to learn that, as The Tennessean reported, Marty Coley Farms has received more than half a million dollars in federal tobacco price support subsidies over the past ten years.

One often hears that employers hire undocumented migrants because no American wants to do the kind of work they’re hired to do. Clearly, no American wants to live in overcrowded and disgusting quarters, be paid a subminimum wage, and have his fingers cut off. The answer isn’t to let this kind of exploitation continue—it’s to improve pay and working conditions enough that Americans will do the work, and to give immigrants the right to reject a job that degrades rather than rewards their labor. As long as the undocumented workforce is subjected to the threat of deportation, Marty Coley Farms and other low-road employers will continue to abuse and exploit them, to the detriment of every American.

The Leisure and Hospitality Sector has the Largest Gap between CEO and Worker Pay

Last week, fast food workers across the nation went on strike to demand higher wages, more regular schedules, and the right to collectively bargain. These fast food workers are a part of the restaurant industry, which Heidi Shierholz recently investigated and found to be characterized by low wages, few benefits, and high rates of poverty. But how does the experience of workers in the restaurant industry compare to its CEOs?

In 2013, CEOs of top restaurant chains in the United States made an average of $10.9 million, which is 721 times more than the minimum wage workers they employ. Restaurant are a part of the wider Leisure and Hospitality sector, which is also characterized by high rates of CEO pay and low rates of worker pay. In fact, CEOs at Leisure and Hospitality companies made, on average, 370 times the pay of a “typical” worker in that sector in 2013—making Leisure and Hospitality the worst sector in terms of disparity between CEO and worker pay. This ratio is far above the average CEO-to-worker pay ratio at all top companies, which in 2013 was 295.9-to-1. It’s also much higher than the next most disparate industry, Information, which has a CEO-to-worker pay ratio of 180-to-1, and the one after that, Trade, Transportation, and Utilities, which has a ratio of 178-to-1.

Blockbuster Report on Construction Industry Tax and Wage Cheating

For 12 months, McClatchy reporters have been carefully digging into a pit of corruption, gathering payroll records in 28 states and interviewing hundreds of workers and business owners about an epidemic of tax cheating, wage theft, and exploitation in the construction industry. The extraordinary report of their investigation was published Thursday, and it’s hair-raising. More than one-third of the employees working on federally-funded projects in Texas and Florida, overseen by public housing authorities and monitored by the U.S. Department of Labor, were improperly classified as independent contractors. The contractors misclassified them in order to escape paying worker’s compensation premiums, unemployment insurance taxes, and FICA taxes, to avoid complying with immigration document requirements, and to avoid liability for labor law violations. In just Florida, Texas, and North Carolina, McClatchy estimates that half a million workers were misclassified, and that the state and federal governments were cheated out of approximately $2 billion in taxes as result.

The stories make the damage this does to the labor market utterly clear. Construction wages were lower in 2012 than they were in 1980, despite rising productivity and huge profits in the industry. Even skilled tradesmen like plumbers and electricians earned 12 to 14 percent less than thirty years ago. Labor law offers no protection to independent contractors, who are not entitled to the minimum wage, overtime pay, or the right to join a union and bargain collectively. Exploited workers—many of them undocumented immigrants who live in fear of deportation—work without adequate safety protections, sometimes receive far less than the pay they were promised, and are deprived of the safety net’s protections if they lose their jobs, are injured or disabled, or reach retirement age. They often live in slum conditions, even while working on luxurious and glitzy new housing.

Unemployment Rate Continues To Be Elevated Across the Board

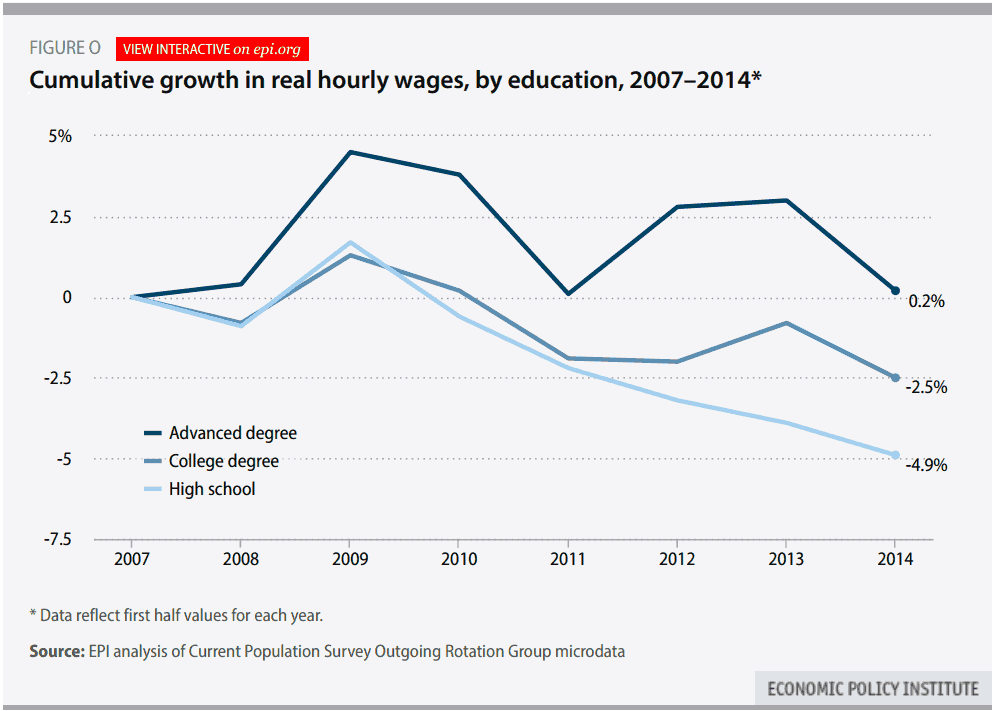

The jobs numbers today, along with a closer look at unemployment rates by demographic groups, point to considerable slack in the labor market across the board. A couple weeks back, I examined real (inflation adjusted) wages across the wage distribution. One of my findings was that real wages fell for all education groups between the first half of 2013 and the first half of 2014. As you can see in the figure below, real hourly wages fell even for those with a college or advanced degree.

And, when we look at these declining real wages hand in hand with the unemployment rates of those with a college or advanced degree, it is obvious that the existence of any sort of skill mismatch is a myth.

Slow Job Growth Should Give Us Pause

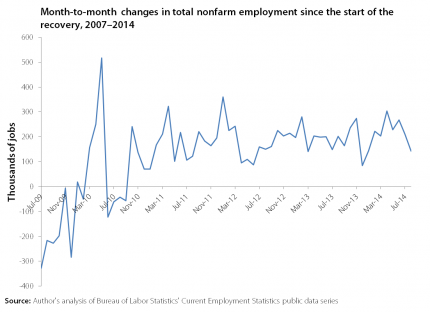

Today’s jobs report showed the economy added 142,000 jobs in August, far below expectations of job growth closer to 230,000. Prior to August, monthly job growth averaged 226,000 this year. The figure below charts monthly job growth since the start of the recovery in July 2009. While the general trend has gone up, this month’s job growth was disappointingly below trend. We haven’t seen job growth this slow since December of last year.

While it’s yet to be seen whether this slower job growth is an anomaly or a new trend, these numbers should give us pause. Adding in this month’s disappointing numbers, job growth this year is still above last year’s average at this time. Job growth has averaged 215,000 jobs a month thus far in 2014, compared to 197,000 in the first eight months of 2013. We need to be consistently adding jobs at a much faster rate to return to the labor market conditions before the recession began. Arguably, that standard is a low bar as the labor market at that time still had considerable slack.

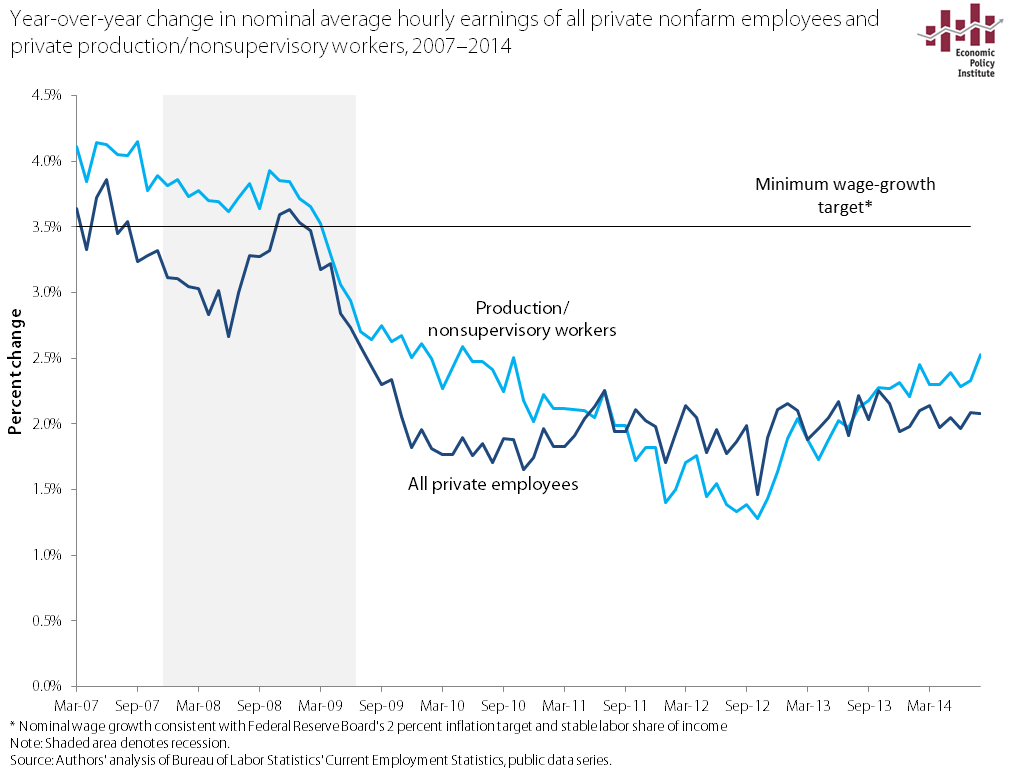

Wages Are Growing Far Below the Fed’s Target

Despite fears from some inflation hawks, the fact is that the weak labor market of the last seven years has put enormous downward pressure on wages, and there has been no significant pickup in nominal wage growth in recent years. As shown in the figure below, wage growth is far below the 3.5 percent rate consistent with the Federal Reserve Board’s inflation target of 2 percent. It’s clear that Fed policymakers should abandon notions of slowing the economy. (For a longer analysis of what to watch for in upcoming months on wage growth, see this explainer.)

What is more than obvious is that employers just don’t have to offer big wage increases to get and keep the workers they need, when hiring rates and net job creation remain far slower than what’s needed to generate healthy labor market outcomes. The result is that over the last year slow nominal wage growth, and inflation-adjusted wage stagnation (or even outright declines), have continued.