Job Openings Are Up, but the Hires Rate Is Down

The August Job Openings and Labor Turnover Survey (JOLTS) data release this morning from the Bureau of Labor Statistics showed mixed results. While the job openings rose, the hires rate fell. Layoffs continue to trend downwards, while the quits rate remained flat—it’s been flat now since February.

The figure below shows the hires rate, the quits rate, and the layoffs rate. The first thing to note is that layoffs, which shot up during the recession, recovered quickly once the recession officially ended. Layoffs have been at prerecession levels for more than three years. This makes sense—the economy is in a recovery and businesses are no longer shedding workers at an elevated rate. And the continued trend downward in August is a good sign.

But for a full recovery in the labor market to occur, two key things need to happen: Layoffs need to come down, and hiring needs to pick up. Hiring is the side of that equation that, while generally improving, has not yet come close to a full recovery. The hires rate remains well below its prerecession level.

Another piece of the puzzle is voluntary quits (shown by the quits rate in the figure below). A larger number of people voluntarily quitting their job indicates a labor market in which hiring is prevalent and workers are able to leave jobs that are not right for them, and find new ones. The voluntary quits rate, which has been flat for the last seven months, is also nowhere near a full recovery. There are 14 percent percent fewer voluntary quits each month than there were before the recession began, and the quits rate is the same as it was last October. Low voluntary quits indicate that there are a large number of workers who are locked into jobs who would leave if they could.

Hires, quits, and layoff rates, December 2000–August 2014

| Month | Hires rate | Layoffs rate | Quits rate |

|---|---|---|---|

| Dec-2000 | 4.1% | 1.4% | 2.3% |

| Jan-2001 | 4.4% | 1.6% | 2.6% |

| Feb-2001 | 4.1% | 1.4% | 2.5% |

| Mar-2001 | 4.2% | 1.6% | 2.4% |

| Apr-2001 | 4.0% | 1.5% | 2.4% |

| May-2001 | 4.0% | 1.5% | 2.4% |

| Jun-2001 | 3.8% | 1.5% | 2.3% |

| Jul-2001 | 3.9% | 1.5% | 2.2% |

| Aug-2001 | 3.8% | 1.4% | 2.1% |

| Sep-2001 | 3.8% | 1.6% | 2.1% |

| Oct-2001 | 3.8% | 1.7% | 2.2% |

| Nov-2001 | 3.7% | 1.6% | 2.0% |

| Dec-2001 | 3.7% | 1.4% | 2.0% |

| Jan-2002 | 3.7% | 1.4% | 2.2% |

| Feb-2002 | 3.7% | 1.5% | 2.0% |

| Mar-2002 | 3.5% | 1.4% | 1.9% |

| Apr-2002 | 3.8% | 1.5% | 2.1% |

| May-2002 | 3.8% | 1.5% | 2.1% |

| Jun-2002 | 3.7% | 1.4% | 2.0% |

| Jul-2002 | 3.8% | 1.5% | 2.1% |

| Aug-2002 | 3.7% | 1.4% | 2.0% |

| Sep-2002 | 3.7% | 1.4% | 2.0% |

| Oct-2002 | 3.7% | 1.4% | 2.0% |

| Nov-2002 | 3.8% | 1.5% | 1.9% |

| Dec-2002 | 3.8% | 1.5% | 2.0% |

| Jan-2003 | 3.8% | 1.5% | 1.9% |

| Feb-2003 | 3.6% | 1.5% | 1.9% |

| Mar-2003 | 3.4% | 1.4% | 1.9% |

| Apr-2003 | 3.6% | 1.6% | 1.8% |

| May-2003 | 3.5% | 1.5% | 1.8% |

| Jun-2003 | 3.7% | 1.6% | 1.8% |

| Jul-2003 | 3.6% | 1.6% | 1.8% |

| Aug-2003 | 3.6% | 1.5% | 1.8% |

| Sep-2003 | 3.7% | 1.5% | 1.9% |

| Oct-2003 | 3.8% | 1.4% | 1.9% |

| Nov-2003 | 3.6% | 1.4% | 1.9% |

| Dec-2003 | 3.8% | 1.5% | 1.9% |

| Jan-2004 | 3.7% | 1.5% | 1.9% |

| Feb-2004 | 3.6% | 1.4% | 1.9% |

| Mar-2004 | 3.9% | 1.4% | 2.0% |

| Apr-2004 | 3.9% | 1.5% | 2.0% |

| May-2004 | 3.8% | 1.4% | 1.9% |

| Jun-2004 | 3.8% | 1.4% | 2.0% |

| Jul-2004 | 3.7% | 1.4% | 2.0% |

| Aug-2004 | 3.9% | 1.5% | 2.0% |

| Sep-2004 | 3.8% | 1.4% | 2.0% |

| Oct-2004 | 3.9% | 1.4% | 2.0% |

| Nov-2004 | 3.9% | 1.5% | 2.1% |

| Dec-2004 | 4.0% | 1.5% | 2.1% |

| Jan-2005 | 3.9% | 1.4% | 2.1% |

| Feb-2005 | 3.9% | 1.4% | 2.0% |

| Mar-2005 | 3.9% | 1.5% | 2.1% |

| Apr-2005 | 4.0% | 1.4% | 2.1% |

| May-2005 | 3.9% | 1.4% | 2.1% |

| Jun-2005 | 3.9% | 1.5% | 2.1% |

| Jul-2005 | 3.9% | 1.4% | 2.0% |

| Aug-2005 | 4.0% | 1.4% | 2.2% |

| Sep-2005 | 4.0% | 1.4% | 2.3% |

| Oct-2005 | 3.8% | 1.3% | 2.2% |

| Nov-2005 | 3.9% | 1.2% | 2.2% |

| Dec-2005 | 3.7% | 1.3% | 2.1% |

| Jan-2006 | 3.9% | 1.3% | 2.1% |

| Feb-2006 | 3.9% | 1.3% | 2.2% |

| Mar-2006 | 3.9% | 1.2% | 2.2% |

| Apr-2006 | 3.8% | 1.3% | 2.1% |

| May-2006 | 4.0% | 1.4% | 2.2% |

| Jun-2006 | 3.9% | 1.2% | 2.2% |

| Jul-2006 | 3.9% | 1.3% | 2.2% |

| Aug-2006 | 3.8% | 1.2% | 2.2% |

| Sep-2006 | 3.8% | 1.3% | 2.1% |

| Oct-2006 | 3.8% | 1.3% | 2.1% |

| Nov-2006 | 4.0% | 1.3% | 2.3% |

| Dec-2006 | 3.8% | 1.3% | 2.2% |

| Jan-2007 | 3.8% | 1.2% | 2.2% |

| Feb-2007 | 3.8% | 1.3% | 2.2% |

| Mar-2007 | 3.8% | 1.3% | 2.2% |

| Apr-2007 | 3.7% | 1.3% | 2.1% |

| May-2007 | 3.8% | 1.3% | 2.2% |

| Jun-2007 | 3.8% | 1.3% | 2.0% |

| Jul-2007 | 3.7% | 1.3% | 2.1% |

| Aug-2007 | 3.7% | 1.3% | 2.1% |

| Sep-2007 | 3.7% | 1.5% | 1.9% |

| Oct-2007 | 3.8% | 1.4% | 2.1% |

| Nov-2007 | 3.7% | 1.4% | 2.0% |

| Dec-2007 | 3.6% | 1.3% | 2.0% |

| Jan-2008 | 3.5% | 1.3% | 2.0% |

| Feb-2008 | 3.5% | 1.4% | 2.0% |

| Mar-2008 | 3.4% | 1.3% | 1.9% |

| Apr-2008 | 3.5% | 1.3% | 2.1% |

| May-2008 | 3.3% | 1.3% | 1.9% |

| Jun-2008 | 3.5% | 1.5% | 1.9% |

| Jul-2008 | 3.3% | 1.4% | 1.8% |

| Aug-2008 | 3.3% | 1.6% | 1.7% |

| Sep-2008 | 3.1% | 1.4% | 1.8% |

| Oct-2008 | 3.3% | 1.6% | 1.8% |

| Nov-2008 | 2.9% | 1.6% | 1.5% |

| Dec-2008 | 3.2% | 1.8% | 1.6% |

| Jan-2009 | 3.1% | 1.9% | 1.5% |

| Feb-2009 | 3.0% | 1.9% | 1.5% |

| Mar-2009 | 2.8% | 1.8% | 1.4% |

| Apr-2009 | 2.9% | 2.0% | 1.3% |

| May-2009 | 2.8% | 1.6% | 1.3% |

| Jun-2009 | 2.8% | 1.6% | 1.3% |

| Jul-2009 | 2.9% | 1.7% | 1.3% |

| Aug-2009 | 2.9% | 1.6% | 1.3% |

| Sep-2009 | 3.0% | 1.6% | 1.3% |

| Oct-2009 | 2.9% | 1.5% | 1.3% |

| Nov-2009 | 3.1% | 1.4% | 1.4% |

| Dec-2009 | 2.9% | 1.5% | 1.3% |

| Jan-2010 | 3.0% | 1.4% | 1.3% |

| Feb-2010 | 2.9% | 1.4% | 1.3% |

| Mar-2010 | 3.2% | 1.4% | 1.4% |

| Apr-2010 | 3.1% | 1.3% | 1.5% |

| May-2010 | 3.4% | 1.3% | 1.4% |

| Jun-2010 | 3.1% | 1.5% | 1.5% |

| Jul-2010 | 3.2% | 1.6% | 1.4% |

| Aug-2010 | 3.0% | 1.4% | 1.4% |

| Sep-2010 | 3.1% | 1.4% | 1.4% |

| Oct-2010 | 3.1% | 1.3% | 1.4% |

| Nov-2010 | 3.2% | 1.4% | 1.4% |

| Dec-2010 | 3.2% | 1.4% | 1.5% |

| Jan-2011 | 3.0% | 1.3% | 1.4% |

| Feb-2011 | 3.1% | 1.3% | 1.4% |

| Mar-2011 | 3.2% | 1.3% | 1.5% |

| Apr-2011 | 3.2% | 1.3% | 1.5% |

| May-2011 | 3.1% | 1.3% | 1.5% |

| Jun-2011 | 3.3% | 1.4% | 1.5% |

| Jul-2011 | 3.1% | 1.3% | 1.5% |

| Aug-2011 | 3.2% | 1.3% | 1.5% |

| Sep-2011 | 3.3% | 1.3% | 1.5% |

| Oct-2011 | 3.2% | 1.3% | 1.5% |

| Nov-2011 | 3.2% | 1.3% | 1.5% |

| Dec-2011 | 3.2% | 1.3% | 1.5% |

| Jan-2012 | 3.2% | 1.2% | 1.5% |

| Feb-2012 | 3.3% | 1.3% | 1.6% |

| Mar-2012 | 3.3% | 1.2% | 1.6% |

| Apr-2012 | 3.2% | 1.4% | 1.6% |

| May-2012 | 3.3% | 1.4% | 1.6% |

| Jun-2012 | 3.2% | 1.3% | 1.6% |

| Jul-2012 | 3.2% | 1.2% | 1.6% |

| Aug-2012 | 3.3% | 1.4% | 1.6% |

| Sep-2012 | 3.1% | 1.3% | 1.4% |

| Oct-2012 | 3.2% | 1.3% | 1.5% |

| Nov-2012 | 3.3% | 1.3% | 1.6% |

| Dec-2012 | 3.2% | 1.2% | 1.6% |

| Jan-2013 | 3.2% | 1.2% | 1.7% |

| Feb-2013 | 3.4% | 1.2% | 1.7% |

| Mar-2013 | 3.2% | 1.3% | 1.6% |

| Apr-2013 | 3.3% | 1.3% | 1.6% |

| May-2013 | 3.3% | 1.3% | 1.6% |

| Jun-2013 | 3.2% | 1.2% | 1.6% |

| Jul-2013 | 3.3% | 1.2% | 1.7% |

| Aug-2013 | 3.4% | 1.2% | 1.7% |

| Sep-2013 | 3.4% | 1.3% | 1.7% |

| Oct-2013 | 3.3% | 1.1% | 1.8% |

| Nov-2013 | 3.3% | 1.1% | 1.8% |

| Dec-2013 | 3.3% | 1.2% | 1.8% |

| Jan-2014 | 3.3% | 1.2% | 1.7% |

| Feb-2014 | 3.4% | 1.2% | 1.8% |

| Mar-2014 | 3.4% | 1.2% | 1.8% |

| Apr-2014 | 3.5% | 1.2% | 1.8% |

| May-2014 | 3.4% | 1.2% | 1.8% |

| Jun-2014 | 3.5% | 1.2% | 1.8% |

| Jul-2014 | 3.6% | 1.2% | 1.8% |

| Aug-2014 | 3.3% | 1.1% | 1.8% |

Note: Shaded areas denote recessions. The hires rate is the number of hires during the entire month as a percent of total employment. The layoff rate is the number of layoffs and discharges during the entire month as a percent of total employment. The quits rate is the number of quits during the entire month as a percent of total employment.

Source: EPI analysis of Bureau of Labor Statistics Job Openings and Labor Turnover Survey

How Do U.S. Retirees Compare with Those in Other Countries?

In Monday’s Wall Street Journal, Andrew Biggs and Sylvester Schieber cited these statistics from the Organisation for Economic Co-operation and Development (OECD):

“Despite a supposedly stingy Social Security program and ineffective retirement-savings vehicles, the average U.S. retiree has an income equal to 92% of the average American income, handily outpacing the Scandinavian countries (81%), Germany (85%), Belgium (77%) and many others.”

Meanwhile, in its Global AgeWatch Index released Tuesday, HelpAge International ranked the United States #8 among the best countries to grow old in, ahead of France (#18) but trailing Norway, Sweden, Switzerland, Canada, Germany, Netherlands, and Iceland (#1-7). Afghanistan (#96) was in last place.

It’s not hard to imagine how wealthy countries like Norway and the United States outrank poor and war-torn countries like Afghanistan. But the relative ranking of the wealthy countries comes as a surprise. How did the United States and other English-speaking countries like the United Kingdom and Australia, not known for their generous social insurance programs or employee benefits, come close to the Nordic cradle-to-grave welfare states and handily beat out France, with its famously generous pensions and high-quality affordable healthcare? Are older Americans really living in a retiree paradise?

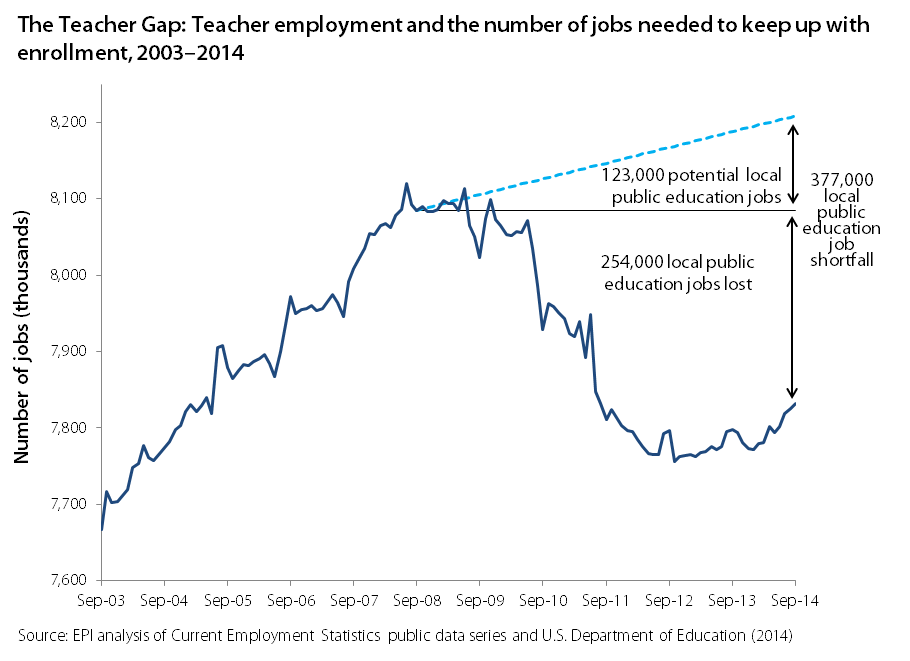

Strong Jobs Numbers for Teachers in September, but Large Jobs Gap Remains

In September, public-sector employment increased by 12,000, with the majority of that growth coming from local government education—an increase of 6,700 jobs. Local government education is largely jobs in public K-12 education (the majority of which are teachers, but also teacher aides, librarians, guidance counselors, administrators, support staff, etc.).

While this is clearly a positive sign, unfortunately, the number of teachers and related education staffers fell dramatically in the recession and has failed to get anywhere near its pre-recession level, let alone the level that would be required to keep up with the expanding student population. The figure below breaks down the teacher gap. The dark blue line illustrates the level of teacher employment. While the most recent positive trend is obvious, the longer term losses are also readily apparently.

Along with dismal trends in public sector employment in general, about a quarter million public education jobs were lost in the great recession and its aftermath. If we add to that the number of public education jobs that should have been added simply to keep up with growing enrollment, then we are currently experiencing a 377,000 job shortfall in local public education. The costs of a significant teacher gap are measurable: larger class sizes, fewer teacher aides, fewer extracurricular activities, and changes to the curriculum.

The Unemployment Rate Fails to Take into Account Missing Workers

Let’s put the pieces of the puzzle together. The unemployment rate fell in September by 0.2 percent points, from 6.1 to 5.9 percent. There was also a decrease in the sheer number of unemployed people—down 329,000 from August. On its face, this sounds like good news.

At the same time, the employment-to-population ratio has remained 59.0 percent for four months running. If the unemployment rate dropped and the employment-to-population ratio remained the same, the missing part of the puzzle is the labor force participation rate. In September, the labor force participation rate dropped to 62.7 percent. The last time the labor force participation rate was this low was February 1978. And, the biggest drop in labor force participation was among prime-age workers, 25-54 years old.

Over the last year, the labor force participation rate fell 0.5 percentage points. Therefore, it’s not surprising that missing workers—potential workers who are neither working nor actively seeking work due to the weak labor market—are at an all-time-high of 6.3 million. The vast majority of them (3.4 million) are 25 to 54 years old.

To put the official unemployment rate in perspective, the figure below shows the actual unemployment rate and the unemployment rate if the missing workers were in the labor force looking for work and thus counted as unemployed. The unemployment rate including the missing workers sits at 9.6 percent, the same rate for the last four months. Perhaps, this is a better indication of the slack in the labor market and the reason why wage growth has remained so sluggish even with a falling unemployment rate.

The unemployment rate is vastly understating weakness in today's labor market: Unemployment rate, actual and if missing workers* were looking for work, January 2006–November 2014

| Date | Actual | If missing workers were looking for work |

|---|---|---|

| 2006-01-01 | 4.7% | 5.0% |

| 2006-02-01 | 4.8% | 4.8% |

| 2006-03-01 | 4.7% | 4.8% |

| 2006-04-01 | 4.7% | 4.9% |

| 2006-05-01 | 4.6% | 4.8% |

| 2006-06-01 | 4.6% | 4.7% |

| 2006-07-01 | 4.7% | 4.8% |

| 2006-08-01 | 4.7% | 4.6% |

| 2006-09-01 | 4.5% | 4.6% |

| 2006-10-01 | 4.4% | 4.4% |

| 2006-11-01 | 4.5% | 4.4% |

| 2006-12-01 | 4.4% | 4.1% |

| 2007-01-01 | 4.6% | 4.4% |

| 2007-02-01 | 4.5% | 4.4% |

| 2007-03-01 | 4.4% | 4.3% |

| 2007-04-01 | 4.5% | 4.9% |

| 2007-05-01 | 4.4% | 4.8% |

| 2007-06-01 | 4.6% | 4.8% |

| 2007-07-01 | 4.7% | 4.9% |

| 2007-08-01 | 4.6% | 5.1% |

| 2007-09-01 | 4.7% | 4.9% |

| 2007-10-01 | 4.7% | 5.2% |

| 2007-11-01 | 4.7% | 4.9% |

| 2007-12-01 | 5.0% | 5.1% |

| 2008-01-01 | 5.0% | 4.8% |

| 2008-02-01 | 4.9% | 5.0% |

| 2008-03-01 | 5.1% | 5.1% |

| 2008-04-01 | 5.0% | 5.2% |

| 2008-05-01 | 5.4% | 5.4% |

| 2008-06-01 | 5.6% | 5.6% |

| 2008-07-01 | 5.8% | 5.7% |

| 2008-08-01 | 6.1% | 6.0% |

| 2008-09-01 | 6.1% | 6.3% |

| 2008-10-01 | 6.5% | 6.5% |

| 2008-11-01 | 6.8% | 7.1% |

| 2008-12-01 | 7.3% | 7.5% |

| 2009-01-01 | 7.8% | 8.2% |

| 2009-02-01 | 8.3% | 8.7% |

| 2009-03-01 | 8.7% | 9.3% |

| 2009-04-01 | 9.0% | 9.4% |

| 2009-05-01 | 9.4% | 9.7% |

| 2009-06-01 | 9.5% | 9.9% |

| 2009-07-01 | 9.5% | 10.1% |

| 2009-08-01 | 9.6% | 10.4% |

| 2009-09-01 | 9.8% | 10.9% |

| 2009-10-01 | 10.0% | 11.3% |

| 2009-11-01 | 9.9% | 11.2% |

| 2009-12-01 | 9.9% | 11.7% |

| 2010-01-01 | 9.7% | 11.3% |

| 2010-02-01 | 9.8% | 11.4% |

| 2010-03-01 | 9.9% | 11.3% |

| 2010-04-01 | 9.9% | 11.0% |

| 2010-05-01 | 9.6% | 11.1% |

| 2010-06-01 | 9.4% | 11.1% |

| 2010-07-01 | 9.5% | 11.3% |

| 2010-08-01 | 9.5% | 11.1% |

| 2010-09-01 | 9.5% | 11.3% |

| 2010-10-01 | 9.5% | 11.5% |

| 2010-11-01 | 9.8% | 11.7% |

| 2010-12-01 | 9.4% | 11.6% |

| 2011-01-01 | 9.1% | 11.4% |

| 2011-02-01 | 9.0% | 11.4% |

| 2011-03-01 | 9.0% | 11.3% |

| 2011-04-01 | 9.1% | 11.4% |

| 2011-05-01 | 9.0% | 11.4% |

| 2011-06-01 | 9.1% | 11.5% |

| 2011-07-11 | 9.0% | 11.7% |

| 2011-08-20 | 9.0% | 11.4% |

| 2011-09-01 | 9.0% | 11.3% |

| 2011-10-11 | 8.8% | 11.2% |

| 2011-11-20 | 8.6% | 11.0% |

| 2011-12-30 | 8.5% | 11.0% |

| 2012-01-12 | 8.2% | 10.8% |

| 2012-02-12 | 8.3% | 10.7% |

| 2012-03-12 | 8.2% | 10.7% |

| 2012-04-12 | 8.2% | 10.9% |

| 2012-05-12 | 8.2% | 10.6% |

| 2012-06-12 | 8.2% | 10.5% |

| 2012-07-12 | 8.2% | 10.8% |

| 2012-08-12 | 8.1% | 10.8% |

| 2012-09-12 | 7.8% | 10.4% |

| 2012-10-12 | 7.8% | 10.0% |

| 2012-11-12 | 7.8% | 10.3% |

| 2012-12-12 | 7.9% | 10.3% |

| 2013-01-12 | 7.9% | 10.4% |

| 2013-02-12 | 7.7% | 10.5% |

| 2013-03-12 | 7.5% | 10.6% |

| 2013-04-12 | 7.5% | 10.5% |

| 2013-05-12 | 7.5% | 10.3% |

| 2013-06-12 | 7.5% | 10.3% |

| 2013-07-12 | 7.3% | 10.2% |

| 2013-08-12 | 7.2% | 10.3% |

| 2013-09-12 | 7.2% | 10.3% |

| 2013-10-12 | 7.2% | 10.7% |

| 2013-11-12 | 7.0% | 10.3% |

| 2013-12-12 | 6.7% | 10.2% |

| 2014-01-12 | 6.6% | 10.0% |

| 2014-02-12 | 6.7% | 10.0 |

| 2014-03-12 | 6.7% | 9.8% |

| 2014-04-12 | 6.3% | 9.9% |

| 2014-05-12 | 6.3% | 9.7% |

| 2014-06-12 | 6.1% | 9.6% |

| 2014-07-12 | 6.2% | 9.6% |

| 2014-08-12 | 6.1% | 9.6% |

| 2014-09-12 | 5.9% | 9.6% |

| 2014-10-12 | 5.8% | 9.1% |

| 2014-11-12 | 5.8% | 9.2% |

* Potential workers who, due to weak job opportunities, are neither employed nor actively seeking work

Source: EPI analysis of Mitra Toossi, “Labor Force Projections to 2016: More Workers in Their Golden Years,” Bureau of Labor Statistics Monthly Labor Review, November 2007; and Current Population Survey public data series

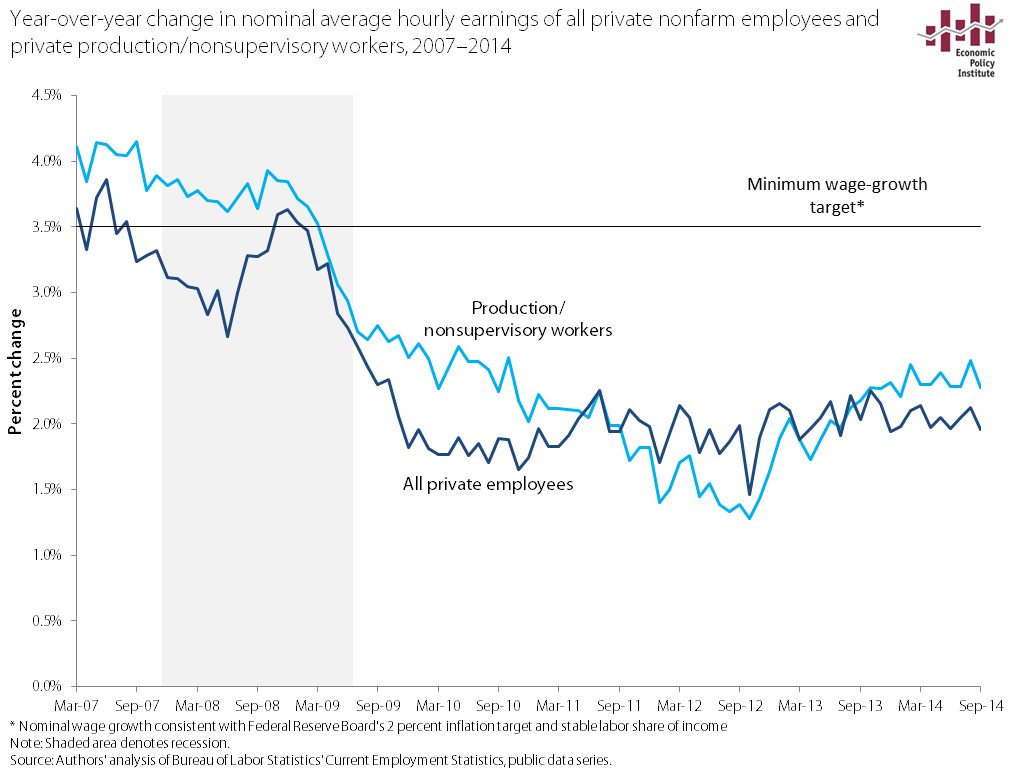

Wage Growth Continues to be Sluggish

While the BLS reported positive overall jobs numbers for September, one notable downside of this morning’s release is that wages grew not at all in the last month. Average hourly earnings of all employees on nonfarm payrolls were little changed (a one cent decline) and average hourly earnings of production and nonsupervisory employees on private nonfarm payrolls saw zero growth. That said, I’d caution reading too much into one month’s numbers because monthly changes can be volatile and longer term trends are more indicative of the overall health of the economy. The fact is that wage growth for both series has been hovering just above 2 percent over the last year.

As shown in the figure below, wage growth is far below the 3.5 percent rate consistent with the Federal Reserve Board’s inflation target of 2 percent. It’s clear that Fed policymakers should abandon notions of slowing the economy. (For a longer analysis of what to watch for in upcoming months on wage growth, see this explainer.)

Walton Family Net Worth is a Case Study Why Growing Wealth Concentration Isn’t Just an Academic Worry

Earlier this year, economist Thomas Piketty caused a stir with a book arguing that the future in advanced economies could see a relentless concentration of wealth among a small sliver of families, whose fortunes would increasingly dwarf those of the typical citizen. The last couple of weeks have seen the release of a couple of key barometers of wealth inequality in America, and combining them, it’s easy to see that this hypothesis of ever-concentrating wealth seems likely indeed. In the past month, the Federal Reserve released its triennial Survey of Consumer Finance (SCF) for 2013, while Forbes magazine released their annual list of the 400 wealthiest Americans.

The SFC is the most comprehensive and high-quality measure of Americans’ wealth up and down the distribution. It makes a special effort to sample very high wealth American households, but actually explicitly excludes listed members of the Forbes 400 (for reasons of confidentiality). The Forbes 400, as is well known, puts a dollar value on the net worth of the 400 wealthiest Americans. There is plenty of material in these releases to assess the current state of wealth inequality in America.

Take one example, that we’ve calculated before: comparing the family wealth of six of the wealthiest members of the Walton family (reported at just under $145 billion in 2013) with the number of American families that you could add together and still have their net worth come in less than the 6 Walton heirs: 52.5 million, or 42.9 percent of American families.

Some have objected to this statistic on the grounds that the negative net worth families (11.5 percent of all American families) somehow shouldn’t count in this calculation. So, try another statistic: how many families that held the median wealth would you need to add together to equal the holdings of the six Walton heirs: more than 1.7 million. The median wealthholder in the United States, remember, has more wealth than half of all American families and less wealth than half (around $81,200 in 2013).

So, what this statistic means is that you’d essentially need a large city’s worth of these typical American families to equal the wealth of the six Walton heirs. And this number has grown steadily over time, as the figure below shows. The falling wealth of the median family (driven largely by the housing bubble burst) and the steadily rising wealth at the very top—including the Walton heirs—have combined to make the gap between them larger and larger over time.

Myths and Facts about Corporate Taxes, Part 1: Do American Corporations Pay the Highest Taxes in the World?

It’s become conventional wisdom that American corporate tax rates are the highest in the developed world, leaving American businesses at a competitive disadvantage—and that the only solution is fundamental tax reform (a phrase used by both Republicans and Democrats). Just yesterday, the Washington Post reported offhandedly that U.S. businesses “currently labor under the highest corporate tax rate in the developed world.” The fact is there are a lot of myths about the corporate tax code—myths that are repeated by corporations that stand to benefit from them. So, let’s look at the facts.

Myth: American corporations pay more in taxes than their competitors in any other country.

Fact: Any claim that the United States has the highest corporate tax rate in the world should be accompanied by a clarification that the rate American companies actually pay, on average, is comparable to what their foreign competitors pay.

Yes, the tax rates on the books (the “statutory” rates) in the United States are high relative to our international peers, but the U.S. corporate tax code has become so riddled with loopholes—and American corporations so adept at exploiting them—that the total amount of taxes actually paid by U.S. corporations (the “effective” corporate tax rate) is far less.

The Government Accountability Office found that large, profitable American corporations pay an effective rate of less than 13 percent in U.S. federal taxes; when state and foreign taxes are included, the rate only increases to 17 percent—a far cry from the statutory 39 percent. Meanwhile, the Congressional Research Service found that the effective rate here is nearly identical to the weighted average of corporate taxes in the world’s other most developed economies. (EPI’s Thomas Hungerford found the same thing.)

What to Watch on Jobs Day: Nominal Wages, Teacher Gap, and Upward Revisions

Tomorrow, the Bureau of Labor Statistics will release the September numbers on employment, unemployment, and nominal wages. While the report contains a host of data, there are three particular numbers I’m going to be watching closely.

First, the overall employment numbers from the payroll survey were lower than expected last month. Consensus estimates had projected job growth of about 230,000, but they came in at only 142,000. The consensus so far for September is again in the low 200,000s. So, two key things to watch: whether there are any upward revisions to the August employment numbers and whether the September numbers come in below consensus two months in a row. Last month, I suggested that slow job growth should make those arguing that policymakers need to worry about an overheating economy and inflationary pressures reconsider. Tomorrow, we will get some more information that can inform the question of whether we are at a new lower trend, which I hope not, or whether last month was a blip in a jobs picture that has otherwise been consistent for much of this year.

Second, with kids heading back to the classroom, it’s worth re-examining the teacher gap—the gap between actual local public education employment and what is needed to keep up with growth in the student population. During the recession, thousands of local public education jobs were lost, and those losses continued deep into the official economic recovery (as did public sector jobs in general). The costs of a significant teacher gap are measurable: larger class sizes, fewer teacher aides, fewer extracurricular activities, and changes to the curriculum. And, in sheer numbers, the teacher gap can explain a non-trivial part of the overall jobs gap. On Friday, I will compare where jobs in public education should be, using the precession ratio, student population growth, and the most recent jobs numbers.

Third, I’ll continue to track nominal wages. Last month, Josh Bivens and I explained how very far we are from the kind of wage growth that would suggest that the Federal Reserve can put the brakes on the economy. On Friday, we will put the latest nominal wage trends in perspective, both historically and against target level wage growth. These numbers on nominal wage growth are likely to be the single most important indicator in coming months driving Federal Reserve decisions.

What’s Up (or Down) With the Boomers’ Retirement Savings?!

The recent release of the Federal Reserve’s triennial Survey of Consumer Finances has many retirement researchers scratching their heads. As expected, GenXers’ savings (shaded blue lines in Figure 1) benefited from the rebound in stock prices and the economic recovery. Meanwhile, Silent Generation retirees (dashed red and yellow lines) saw a surprisingly large bounce in retirement savings. But Baby Boomers (solid purple, black and green lines) who were approaching retirement when the housing bubble burst saw weak gains or even losses between 2010 and 2013. Those who were born between 1949 and 1954, for example, saw a decline in mean retirement account savings from $176,000 in 2010 to $167,000 in 2013 (values are in 2013 dollars rounded to the nearest $1,000). This is far below the $199,000 their predecessors—older Boomers born between 1943 and 1948—had accumulated at the same age in 2007.

It’s not news that the Boomers’ retirement savings took a hit during the downturn. What’s more surprising is that they have fared so poorly in the recovery compared to younger workers and retirees. One explanation is simply that the Boomers, unlike older retirees, were hit by both the stock and labor market downturns and didn’t benefit as much from the subsequent rebound in stock prices as younger workers who were heavily invested in stocks through target date funds.

Mean retirement account balances by birth cohort , 1989–2013

| 1931–1936 | 1937–1942 | 1943–1948 | 1949–1954 | 1955–1960 | 1961–1966 | 1967–1972 | 1973–1978 | |

|---|---|---|---|---|---|---|---|---|

| 1989 | $56,383 | $44,937 | $30,369 | $27,428 | $7,419 | |||

| 1992 | $68,060 | $75,678 | $44,749 | $22,920 | $12,552 | $7,176 | ||

| 1995 | $64,254 | $90,781 | $75,262 | $50,090 | $22,642 | $16,480 | ||

| 1998 | $113,886 | $114,908 | $91,373 | $64,166 | $48,084 | $29,458 | $11,059 | |

| 2001 | $124,634 | $162,156 | $155,809 | $91,203 | $75,722 | $40,706 | $18,841 | |

| 2004 | $111,834 | $149,322 | $158,827 | $128,848 | $81,818 | $54,205 | $27,100 | $11,640 |

| 2007 | $109,709 | $164,654 | $199,218 | $161,187 | $114,482 | $69,036 | $41,928 | $18,436 |

| 2010 | $80,091 | $138,102 | $209,317 | $175,697 | $138,713 | $85,454 | $48,472 | $25,864 |

| 2013 | $88,944 | $168,828 | $214,277 | $166,597 | $154,630 | $103,838 | $75,433 | $46,593 |

Source: EPI's analysis of the Federal Reserve's Survey of Consumer Finance

TIP: For apples-to-apples comparisons, look at how successive 6-year birth cohorts fared at 6-year intervals (2013, 2007, and 2001), ignoring intervening surveys.

LA Hotel Workers Win $15.37 Minimum Wage: a New Day for Labor in the United States?

The Los Angeles City Council’s vote to raise the minimum wage for hotel workers is another herald of big changes coming in the way the United States deals with low wages and inequality. The Council voted 12 to 3 to raise the minimum wage for workers at large hotels to $15.37 an hour by 2017, which is more than the national median wage for women ($15.10 in 2013). Mayor Eric Garcetti will sign the bill after it receives a confirming second vote next week.

The LA County AFL-CIO, UNITE HERE Local 11 (the LA area union of hospitality workers), and the Los Angeles Alliance for a New Economy, which led the campaign, don’t intend to rest on their laurels and will push for an across-the-board minimum wage increase to $13.25 an hour, far above the national minimum wage of $7.25 an hour. Mayor Garcetti strongly supports that bill, too.

As in Seattle, where a union-led coalition won a $15 minimum wage, the people of Los Angeles realize that many businesses will not share revenues fairly with their workers unless they are required to do so. Even businesses that want to pay their employees a living wage feel constrained by their competitors: How can they compete with a competitor paying its workers $5.00 an hour less? The only way to break through these constraints is to reset labor standards to a level that provides a decent living. As Franklin Roosevelt said when he first sent minimum wage legislation to Congress in 1933: “No business which depends for existence on paying less than living wages to its workers has any right to continue in this country… By living wages, I mean more than a bare subsistence level. I mean the wages of decent living.”