Unemployment claims rise for second week in a row: Millions will lose federal unemployment benefits in December unless Senate Republicans act

Because of the Thanksgiving holiday this week, data on unemployment insurance (UI) claims—usually released on Thursdays—were released today. The data show that another 1.1 million people applied for UI benefits last week, including 778,000 people who applied for regular state UI and 312,000 who applied for Pandemic Unemployment Assistance (PUA). The 1.1 million who applied for UI last week was an increase of 22,000 from the prior week’s figures—the second week in a row that initial claims have risen. Further, last week was the 36th straight week total initial claims were greater than the worst week of the Great Recession. (If that comparison is restricted to regular state claims—because we didn’t have PUA in the Great Recession—initial claims last week were still greater than the second-worst week of the Great Recession.)

Most states provide 26 weeks of regular benefits, but this crisis has gone on much longer than that. That means many workers are exhausting their regular state UI benefits. In the most recent data, continuing claims for regular state UI dropped by 299,000, from 6.4 million to 6.1 million.

For now, after an individual exhausts regular state benefits, they can move onto Pandemic Emergency Unemployment Compensation (PEUC), which is an additional 13 weeks of regular state UI. However, PEUC is set to expire on December 26 (as is PUA—more on these expirations below).

Racism and the Economy: Focus on Employment

Valerie Wilson, director of the Economic Policy Institute Program on Race, Ethnicity, and the Economy, gave the keynote address at the Federal Reserve Symposium on Racism and the Economy. These are her remarks.

According to the Center for Assessment and Policy Development, racial equity is the condition that would be achieved if one’s racial identity no longer predicted, in a statistical sense, how one fares.

In reality, statistical analysis often reveals that racial identity is a measurable, significant, and persistent predictor of labor market outcomes. Let’s pause and think about that for a moment. Why should racial identity—something as arbitrary and superficial as physical appearance (skin color)—be statistically correlated with one’s likelihood of being employed or how much they are paid for their labor?

No improvement in initial unemployment claims as labor market gains falter

Another 1.1 million people applied for unemployment insurance (UI) benefits last week, including 742,000 people who applied for regular state UI and 320,000 who applied for Pandemic Unemployment Assistance (PUA). The 1.1 million who applied for UI last week was an increase of 55,000 from the prior week’s figures. Last week was the 35th straight week total initial claims were greater than the worst week of the Great Recession. (If that comparison is restricted to regular state claims—because we didn’t have PUA in the Great Recession—initial claims last week were still 3.3 times where they were a year ago.)

Most states provide 26 weeks of regular benefits, but this crisis has gone on much longer than that. That means many workers are exhausting their regular state UI benefits. In the most recent data, continuing claims for regular state UI dropped by 429,000, from 6.8 million to 6.4 million.

For now, after an individual exhausts regular state benefits, they can move on to Pandemic Emergency Unemployment Compensation (PEUC), which is an additional 13 weeks of regular state UI. However, PEUC is set to expire on December 26 (as is PUA).

In the latest data available for PEUC (the week ending October 31), PEUC rose by 233,000, from 4.1 million to 4.4 million, offsetting only about 60% of the 383,000 decline in continuing claims for regular state benefits for the same week. This is likely due in large part to the fact that many of the roughly 2 million workers who were on UI before the recession began, or who are in states with less than the standard 26 weeks of regular state benefits, are exhausting PEUC benefits at the same time others are taking it up. More than 1.5 million workers have exhausted PEUC so far (see column C43 in form ETA 5159 for PEUC here). Last week, 634,000 workers were on Extended Benefits (EB), which is a program that eligible unemployed workers in some states can get on if they’ve exhausted PEUC.

Learning during the pandemic: What decreased learning time in school means for student learning

One reflection of how much students have learned and developed since schools closed in March can be found in late Argentinian cartoonist Quino’s 2007 comic strip, in Manolito and his peers’ self-assessments of what they learned in school. When Manolito’s teacher asks, he replies: “From March to today, nothing.” (The implied message is: Others are learning, while he is stuck.)

Lavado, Joaquín Salvador, Quino. 2007. Toda Mafalda. Buenos Aires, Ediciones de la Flor.

As many parents and teachers have seen, these are the likely realities for students in 2020. Because learning time in school matters, and students’ learning and development tend to vary greatly even when schools operate in normal circumstances, challenges to learning were magnified when schools closed—due to prolonged cuts to learning time in school, the access to some “substitute” educational opportunities during the pandemic, and the many factors that influence out-of-school learning.

In this blog post, we review the consequences of reduced learning time in school settings during the pandemic, and what the evidence tells us to do about it when we begin to control the spread of the virus. (For a detailed review of the challenges COVID-19 brought to education and our policy recommendations, see “COVID-19 and student performance, equity, and U.S. education policy: Lessons from pre-pandemic research to inform relief, recovery, and rebuilding.”)

With unemployment benefits for millions of workers set to expire in December, Senate Republicans must stop blocking aid

More than 1.0 million people applied for unemployment insurance (UI) benefits again last week, including 709,000 people who applied for regular state UI and 298,000 who applied for Pandemic Unemployment Assistance (PUA). PUA is the federal program that provides up to 39 weeks of benefits for workers who are not eligible for regular unemployment insurance, like the self-employed. Without congressional action, PUA will expire on December 26 (more on that below).

The 1.0 million who applied for UI last week was a decline of 112,000 from the prior week’s figures. Last week was the 34th straight week total initial claims were far greater than the worst week of the Great Recession. (If that comparison is restricted to regular state claims—because we didn’t have PUA in the Great Recession—initial claims last week were still more than 3.0 times where they were a year ago.)

Most states provide 26 weeks of regular benefits, but this crisis has gone on much longer than that. That means many workers are exhausting their regular state UI benefits. In the most recent data, continuing claims for regular state UI dropped by 436,000, from 7.2 million to 6.8 million.

For now, after an individual exhausts regular state benefits, they can move onto Pandemic Emergency Unemployment Compensation (PEUC), which is an additional 13 weeks of regular state UI. However, like PUA, PEUC is set to expire on December 26 (more on that below).

Voters chose more than just the president: A review of important state ballot initiative outcomes

With enormous attention focused—understandably—on the outcome of the presidential and congressional races on November 3, it’s easy to forget that voters also decided on nearly 6,000 state legislative races and a host of ballot measures in states and localities, including many with important implications for workers, economic justice, racial equity, and the fight against climate change.

There were 120 statewide measures considered by voters across the country. In this post, we briefly highlight some of the notable measures that would have a meaningful impact on the welfare of workers, families, and communities; the power of workers and communities to have a voice in economic policy decisions; and the ability of all people to achieve economic security, regardless of race, ethnicity, or gender. We also call attention to the advocacy and research of Economic Analysis and Research Network (EARN) members in these states, whose work in many cases was critical in explaining the implications of the measures for workers, families, and communities.

The Job Openings and Labor Turnover Survey shows declines in hires: As winter hits, the Biden administration will be facing a mounting, not waning, crisis

Last week, the Bureau of Labor Statistics (BLS) reported that, as of the middle of September, the economy was still 10 million jobs below where it was in February. Job growth slowed considerably over the last few months and the jobs deficit in October was easily over 11.6 million from where we would have been if the economy had continued adding jobs at the pre-pandemic pace.

Today’s BLS Job Openings and Labor Turnover Survey (JOLTS) reports job openings changed little at 6.4 million in September while hires and layoffs fell. While the slowdown in layoffs is promising from 1.5 million to 1.3 million, the softening in hires is a concern (6.0 million to 5.9 million). The U.S. economy is seeing a significantly slower pace of hiring than we experienced in May or June—hiring is roughly where it was before the recession, which is a big problem given that we have more than 11.6 million jobs to make up. And job openings are now substantially below where they were before the recession began (6.4 million at the end of September, compared to 7.1 million on average in the year prior to the recession). No matter how it is measured, the U.S. economy is facing a huge job shortfall.

One of the most striking indicators from today’s report is the job seekers ratio, that is, the ratio of unemployed workers (averaged for mid-September and mid-October) to job openings (at the end of September). On average, there were 11.8 million unemployed workers while there were only 6.4 million job openings. This translates into a job seeker ratio of about 1.8 unemployed workers to every job opening. Another way to think about this: for every 18 workers who were officially counted as unemployed, there were only available jobs for 10 of them. That means, no matter what they did, there were no jobs for 5.4 million unemployed workers. And this misses the fact that many more weren’t counted among the unemployed. The economic pain remains widespread with more than 25 million workers hurt by the coronavirus downturn. Without congressional action to stimulate the economy, we are facing a slow, painful recovery.Read more

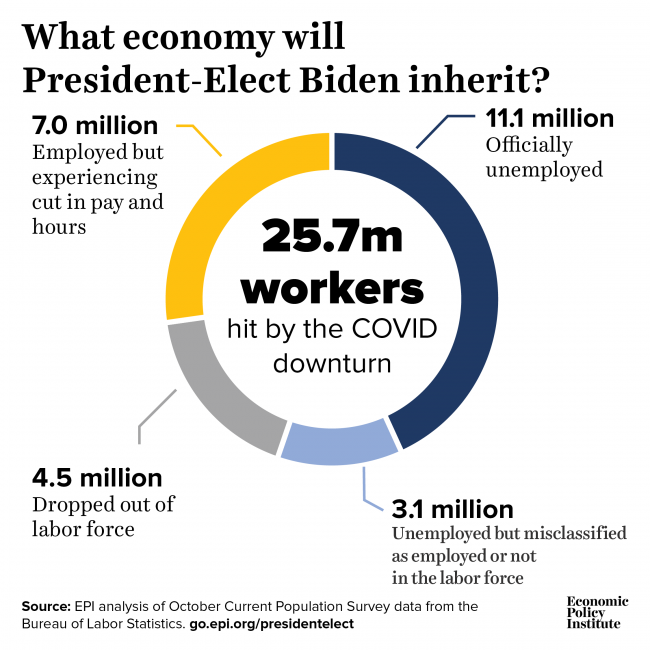

What the next president inherits: More than 25 million workers are being hurt by the coronavirus downturn

Some of the most frequent questions I’ve gotten in the last few months are, “How many workers are being hurt by the coronavirus recession?” and “What kind of economy will the next president inherit?”

There is a huge amount of confusion about the number of workers impacted by this downturn because two major, completely separate, government data sets that address these questions are reporting very different numbers. Specifically, the Bureau of Labor Statistics (BLS) reported that the official number of unemployed workers in October, from the Current Population Survey, was 11.1 million. But during the reference week for the October monthly unemployment figure—the week ending October 17—the Department of Labor (DOL) reported that there were a total of 21.5 million people claiming unemployment insurance (UI) benefits in all programs. The UI number is compiled by DOL from reports it receives from state unemployment insurance agencies.

What is going on? In a nutshell: The BLS official number of unemployed workers vastly understates the number of workers who have faced the negative consequences of the coronavirus recession, and DOL’s UI number overstates the number of workers receiving unemployment benefits.

Let’s first look at UI. One straightforward way that the weekly UI numbers are higher than the monthly unemployment numbers is that the UI numbers include both Puerto Rico and the Virgin Islands, and the monthly unemployment numbers include only the 50 states and the District of Columbia. The number of people on UI (regular state benefits, Pandemic Unemployment Assistance, Pandemic Emergency Unemployment Compensation, or Extended Benefits) for the week ending October 17 was 294,000 in Puerto Rico and 4,000 in the Virgin Islands, for a total of nearly 300,000 UI claims outside of the 50 states and the District of Columbia.

Over a million people still filed initial unemployment claims last week with no COVID-19 relief in sight

Another 1.1 million people applied for unemployment insurance (UI) benefits last week, including 751,000 people who applied for regular state UI and 363,000 who applied for Pandemic Unemployment Assistance (PUA). PUA is the federal program that provides up to 39 weeks of benefits for workers who are not eligible for regular unemployment insurance, like the self-employed. Without congressional action, PUA will expire in less than two months (more on that below).

The 1.1 million who applied for UI last week was little changed (a decline of 3,000) from the prior week’s revised figures. Last week was the 33rd straight week total initial claims were far greater than the worst week of the Great Recession. (If that comparison is restricted to regular state claims—because we didn’t have PUA in the Great Recession—initial claims last week were still 3.6 times where they were a year ago.)

Most states provide 26 weeks of regular benefits, but this crisis has gone on much longer than that. That means many workers are exhausting their regular state UI benefits. In the most recent data, continuing claims for regular state UI dropped by 538,000, from 7.8 million to 7.3 million.

For now, after an individual exhausts regular state benefits, they can move onto Pandemic Emergency Unemployment Compensation (PEUC), which is an additional 13 weeks of regular state UI. However, PEUC is set to expire in less than two months (more on that below).

Older workers are voting with an eye on the economy

Recent polls have shown that older Americans and women appear to have turned against President Trump, and the reasons aren’t hard to grasp. The administration’s mishandling of the COVID-19 pandemic has been especially deadly for older Americans, while women have borne the brunt of the economic downturn, with greater job losses and caregiving responsibilities.

One factor has received less attention: Older Americans, too, have been hard hit in the economic downturn. Senior women (women ages 65 and older) have seen a steep decline in employment—almost as steep as that of young women just entering the labor force (see Table 1). Senior men also saw a steep decline in employment early in the pandemic but rebounded faster than senior women.