The president’s jobs package would indeed create jobs

One of the best aspects of President Obama’s new budget plan is its near-term focus on job creation. This is a significant change from last year’s budget, where job creation was effectively ignored in favor of deficit reduction (likely in response to the GOP victory in the 2010 midterm elections, but that’s no excuse). This year, the president included $350 billion in job creation, $300 billion of which would hit the economy in the next year and a half. Here’s what’s in it though fiscal year 2013:

- $95 billion in the payroll tax cuts (employee-side)

- $80 billion in other business tax cuts (including a $25 billion hiring credit)

- $45 billion in emergency unemployment benefit extension

- $25 billion in transportation infrastructure investments ($50 billion over ten years)

- $20 billion in school facility repair and modernization

- $30 billion in retaining or rehiring teachers and first responders

- $25 billion miscellaneous neighborhood stabilization, job training, energy efficiency, VA conservation jobs, infrastructure bank, and manufacturing incentives

Last fall, the president proposed the American Jobs Act (AJA), a collection of policies designed to jump-start the economy. There are a few differences between the AJA and this jobs package—some policies were already enacted, some were scaled down, and there are a few new proposals—but this is essentially an updated and revised AJA.

And like the AJA, this jobs package would have an immediate positive impact on the economy and jobs. About 85 percent ($300 billion) of the package would hit the economy in the next year and a half. Using standard macroeconomic multipliers for the various policy categories, we find that the president’s job creation proposals would create 1.5 million jobs in fiscal year 2012 and 1.3 million jobs in fiscal year 2013 (through Sept. 2013).

The following graph shows by how much this proposal would lower unemployment relative to the unemployment levels under the Congressional Budget Office’s economic projections, if the historical relationship between GDP growth and unemployment held over the next two years. Note that CBO assumes that in Jan. 2013 the entirety of the Bush tax cuts will expire and the sequestration trigger will be implemented in full. A more realistic policy assumption that at least partially extends the Bush tax cuts and replaces the trigger would lower their projected unemployment levels. However, because the unemployment path under the jobs package was constructed off of the CBO baseline, the gap between the two would remain the same.

Some might argue that the full value of the $300 billion in the next year and half should not be included as “new” fiscal support, since the payroll tax cut is very likely to be extended for the full year (and full-year extension is included in the baseline of most macroeconomic forecasters’ models). In addition, the unemployment insurance extensions are also likely (though not guaranteed) to also run through all of 2012 (and many forecasts have some portion of these included in their baseline as well). Still, given the intense political pressure to move to immediate fiscal tightening, we think even just preserving the fiscal support already included in many forecast baselines is an important step in the president’s budget and should be highlighted.

For more on our job creation methodology, see our memo from last fall.

Morals, money and book promotion

Since an unexpected link from Noam Chomsky (whoa!) has brought it some attention, I may as well take the chance to introduce my book Failure by Design as a piece of evidence in the “morals versus money” debate going on.

David Brooks, channeling Charles Murray, argues that moral/social decay led to the poor economic performance in the bottom half of the income distribution in recent decades. Paul Krugman, Dean Baker, and Larry Mishel (I’m sure I’m missing others) demur – arguing that evidence for the poor economic performance is clear as day while evidence pointing to moral/social decay as an independent cause is awfully unpersuasive. (Wait! Don’t choose sides already based purely on teams – I have more evidence to offer!)

One thing that hasn’t been mentioned yet is that there’s plenty of reason to believe that things besides moral/social decay led to poor economic performance; policy changes alone just about guaranteed this poor performance. As Failure by Design notes, recent decades have seen: the inflation-adjusted value of the minimum wage fall for years (almost decades) at a stretch (leaving it still today below its late 1960s peak); an ongoing decline in the share of workers represented by a union (even while the share of workers desiring a union has not much moved); a much-larger share of the total U.S. economy accounted for by trade with much-poorer nations; and a Federal Reserve that has been less and less willing to push back hard against unemployment rates that rise above even their own conservative targets.

{kind=link}

{kind=link}

{kind=link}

Nobody, absolutely nobody, disputes that these things should’ve been expected to do anything but inflict disproportionate harm on low- and moderate-wage workers. The conservative case for making these policy changes was that they would improve overall economic performance and if one was so inclined to make sure that low- and moderate-income workers were not harmed by these policy changes, one could have used the tax/transfer system to redistribute some of these overall gains their way.

I’d complain that not enough of these overall gains have found their way to the bottom half of the income distribution – but it’s awfully hard to believe these overall gains happened at all. Measures of aggregate economic performance are really no better (and are mostly worse) in recent decades even as incomes are shifted.

Bad Apple labor practices: Promises have been made before

The New York Times‘ brilliant two-part investigation of the wretched treatment of Apple’s manufacturing workforce is the obvious cause of the announcement that Apple is submitting to outside monitoring of conditions in its suppliers’ factories. No one at Apple headquarters had a religious epiphany; they were disgraced in the pages of the world’s greatest newspaper, and the public was beginning to react. This is not to say that a public relations gambit can’t lead to real change. But Steven Greenhouse’s story in the Times yesterday raises fair questions about the depth of Apple’s new commitment to labor rights.

Apple had two obvious choices for outside monitor: the Fair Labor Association, a monitoring group funded by the corporations it monitors, or a truly independent organization like the Worker Rights Consortium, which does not accept contributions from any for-profit corporation, let alone the corporations it monitors. The fact that it chose the in-house alternative tells me that Apple is less than fully committed to its new cause.

It’s worth noting that Apple has gone down this route before, with lousy results. In 2007, after China Labor Watch and Chinese journalists reported serious abuses at Apple’s key supplier, Foxconn, Apple hired Verite to monitor Foxconn’s labor law compliance. Foxconn is the company where—three years after Verite was hired—workers began committing suicide to escape their servitude, inhumanly crowded conditions, and personal abuse.

There are other reasons to doubt that anything material will change. The Fair Labor Association’s Executive Director, Jorge Perez-Lopez, with whom I worked at the Department of Labor, is a very decent guy. But when he says Apple will have no influence on which factories will be inspected or when, it’s hard to believe, especially when Apple’s CEO made the announcement that the first inspections would be in Foxconn factories in Shenzen and Chengdu. Oops! What Mr. Perez-Lopez didn’t say is equally interesting: How will the findings be released? We have seen that public shame is a powerful motivator. Will Apple have any control over the timing or content of the monitor’s reports on conditions?

And most important, will the Fair Labor Association be allowed to investigate the causes of the poor conditions, which include the price Apple is willing to pay for its products? Apple, like Wal-Mart, is famous for squeezing its suppliers, leaving them less and less to pass down to the workers in wages. Scott Nova, Executive Director of the Worker Rights Consortium, estimates that Apple could triple the wages its suppliers pay and reduce its gigantic profits by only 7 percent. That might be the fastest and surest way to improve the lives of its 700,000 workers. But it wasn’t part of Monday’s announcement.

Labor Department tackles guest worker problems

On Friday, Feb. 10, the Department of Labor (DOL) announced a new set of rules for the H-2B program, the country’s main temporary foreign labor program for less-skilled workers in non-agricultural positions. The new rules are set to become effective in late April, and as the New York Times reported on Saturday, “the changes were hailed by advocates for guest workers, who said they would make it more difficult for businesses to exploit vulnerable foreign migrants and hire them to undercut Americans.”

I join in the applause for the H-2B rule changes. For several years, the H-2B program has operated in ways that defy common sense. For example, in the District of Columbia, where more than 30,000 people were unemployed in 2010 and the unemployment rate hovered around 10 percent, common sense tells you that hotels should have an easy time finding local residents to take jobs as maids or cooks. And if they really couldn’t find anyone from D.C. to clean hotel rooms, surely they’d find qualified applicants in Northern Virginia or Maryland.

Yet lodging giant Marriott Hotels claimed they couldn’t find anyone here or elsewhere in the United States for 48 hotel maid and cook positions. They got government approval to bring 48 H-2B workers from abroad to do work that local people (with a high school education or less) could have been trained to do very quickly.

How did Marriott do it? How did they convince the DOL that no one in the D.C. area was interested in and qualified for these jobs? One possibility is that Marriott might have dishonestly claimed that they tried to recruit U.S. workers but failed. Under the old program rules, DOL didn’t have to check the accuracy of Marriott’s claims; DOL in all likelihood simply accepted Marriott’s “attestation,” i.e., simply took their word for it. Widespread fraud and abuse, documented by government and news reports and legal cases, are the main reason DOL has done away with the attestation procedure in its new rule.

More likely, Marriott fully complied with the minimal recruiting requirements mandated by the current rules, and few qualified local residents responded, because few ever heard there were positions open and because the wages offered were well below the prevailing wage in the D.C. area.

Marriott offered to pay the cooks $9.80 an hour. Here are the median, mean (or average), and annual wages paid to cooks in D.C. in 2010. Marriott’s wage offer was $3.80 an hour less than the average paid to the lowest paid of the hotel, cafeteria, or restaurant cook occupations in D.C.

|

Marriott offered to pay the maids $8.50 an hour, even though the median wage for maids in D.C. was $14.58 and the mean was $14.44. Marriott’s offered wage was only 59 percent of the prevailing wage for maids in D.C. That might have been enough all by itself to discourage anyone in D.C. from applying for the jobs. It’s likely, however, that potential hotel maids in D.C. either didn’t see Marriott’s ad if it ran only for the required minimum of three days in some local paper, or if they did see it, it could have been months before the position was available and therefore job seekers ignored it.

|

If Marriott had been looking to employ cooks and maids in the broader, D.C.-Virginia-Maryland-West Virginia area, the prevailing wage would have been somewhat lower but still far above what the company actually offered.

|

It’s easy to see why employers like Marriott love the current H-2B program. They can legally pay temporary foreign workers less than the local market rate for essential jobs. Fixing this aspect of the H-2B program was the impetus for an earlier rule proposed by DOL, but that common sense rule was blocked by Congress after a lobbying firestorm. Employers claimed they’d go out of business if they were forced to pay the local average wage to maids and cooks (and especially landscapers), even though the employers they compete with are doing just that. But the fact that employers don’t have to document and prove their efforts to recruit U.S. workers—even at the below-average wages permitted by the H-2B program—exacerbates the problem and allows employers to ignore the employment needs of the local workforce where they do business, at the expense of the local workers’ ability to earn a living wage.

The new H-2B rules will help local workers find jobs at the prevailing wage for the work that they do. They will help put more unemployed Americans back to work, and also prevent the undercutting of employers who pay a living wage. Unfortunately, H-2B employers are already up in arms about these common sense reforms. Congress should not allow the desire of H-2B employers to lower American wages trump the need of unemployed workers to earn a decent wage.

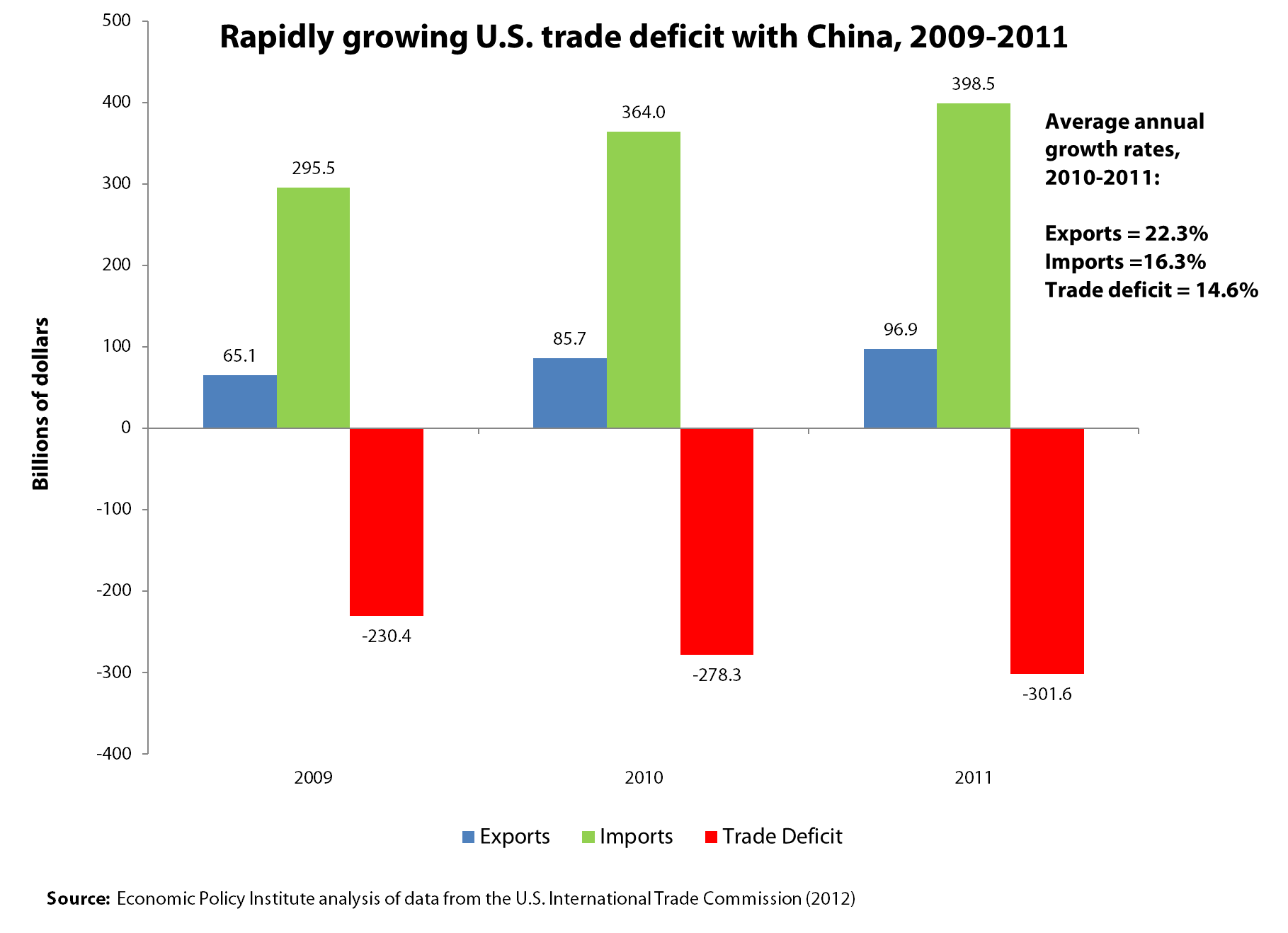

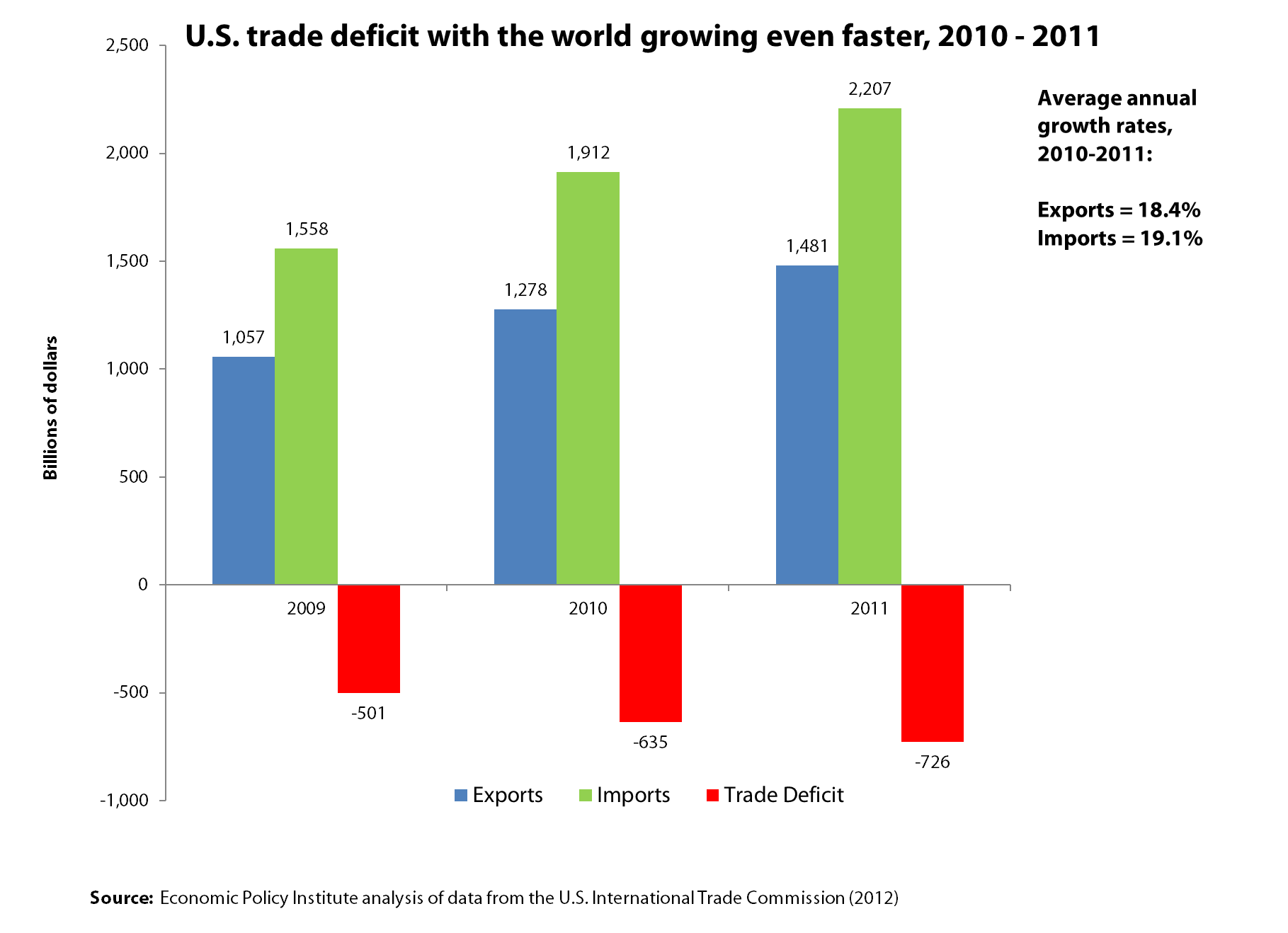

Exports and growth: Running harder and falling behind

In his 2010 State of the Union address, President Obama pledged to double exports over the next five years, which would “support two million jobs.” How’s that working out? Not so well, despite claims to the contrary from the White House. In this year’s SOTU address, the president pointed to newly signed Free Trade Agreements (FTAs) with South Korea, Colombia and Panama as policies that will generate more exports, and they are, but the U.S trade deficit with those countries also increased last year. In short, it’s hard to argue that the Obama administration has taken any serious steps to make trade flows move from a minus to a plus in generating growth and employment in coming years.

Their rhetoric often suggests otherwise. Just last week, Deputy National Security Advisor for International Economic Affairs Michael Froman claimed that “last year our exports of goods alone to China exceeded $100 billion, and have been growing almost twice as fast as our exports to the rest of the world.” While this was a nice welcome for China’s Vice President Xi Jinping, who visits the White House today, it turns out that this nice round (and arbitrary number) was only reached if one is willing to overlook some key issues in trade data.

On the broader question of export growth, while exports to China and the world have been growing rapidly, the volume of U.S. imports increased much more rapidly – and this means that U.S. trade deficits with China and the world have increased rapidly over the past two years. This increasing trade deficit has generated a net loss in trade-related jobs with both China and the world as a whole. Thus, while export growth may have supported some new U.S. jobs, the growth in imports has displaced a much larger number of jobs. Between 2008 and 2010, the growth of U.S. trade deficits with China alone resulted in the loss of 453,100 U.S. jobs. A thorough jobs analysis of U.S. trade in the 2009-2011 period has not yet been completed. However, the U.S. trade deficit in non-oil manufactured goods, the most labor intensive portion of U.S. goods trade, increased by $129.3 billion in this period, displacing hundreds of thousands of U.S. manufacturing jobs.

Exports to China increase at a relatively brisk pace of 22.3 percent on average over the past two years (since President Obama’s announced goal of doubling exports), as shown in the figure below. While this number sounds great in isolation, it was more than offset by the growth of imports from China, as shown in the figure; and U.S. trade deficits with China have soared.¹ So, even though exports to China are growing rapidly, the base (their initial level) is tiny compared with imports, which exceeded exports by more than 4-to-1 throughout this period. Therefore, in order to merely stabilize our trade deficit with China, exports would have to grow at least four times as fast as imports. In fact, imports from China grew nearly as fast as our exports to that country, and our bilateral deficit has increased 14.6 percent per year on average over the past two years.

U.S. exports to the world have increased at a slightly slower rate of 18.4 percent per year over the past two years. Although this is slightly lower than the rate of growth of exports to China, at this rate, exports will double between 2009 and 2013, one year ahead of the goal set by President Obama. Time for a celebration and a tour of all those shiny new factories shipping exports to China, right? Not if we care about jobs. If imports and exports continue to grow at present rates, the U.S. global trade deficit will more than double by 2013 to more than $1 trillion. Millions more jobs will be lost, most of them in manufacturing. Again, the story is simple: Trade flows have two sides, imports and exports. Counting only one side tells you nothing about how policy has aided or hindered U.S. competitiveness in the global economy.

Readers will note that exports to China have grown only slightly faster than exports to the world over the past two years.Read more

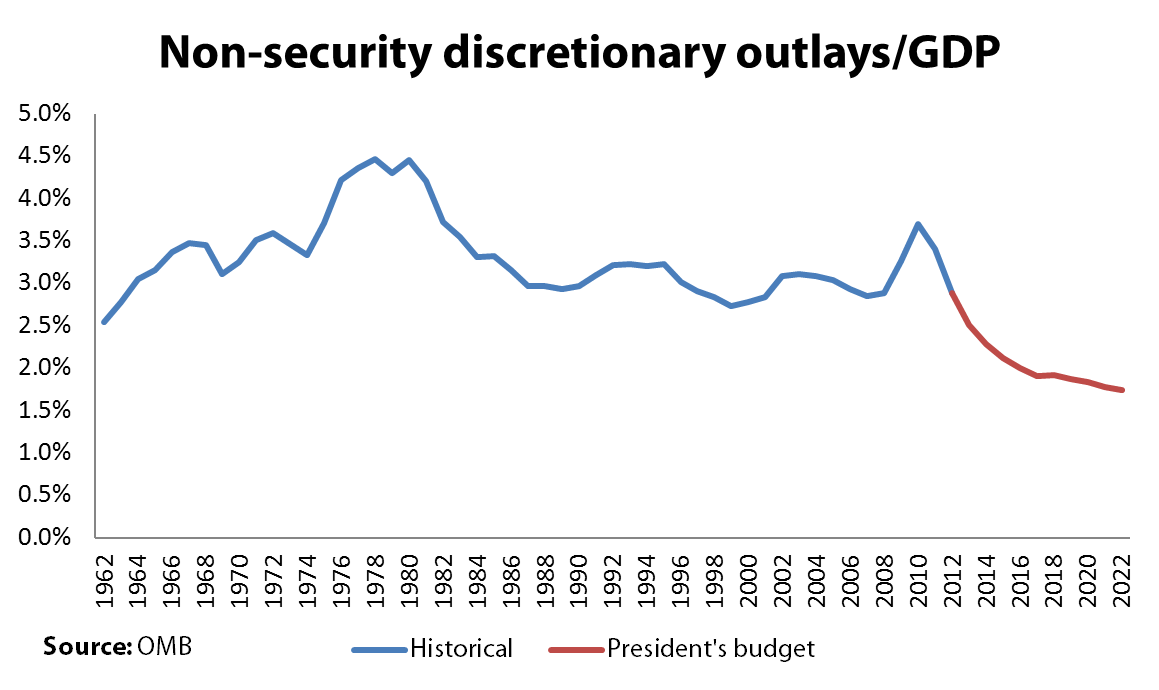

Don’t cut the non-security discretionary budget!

One of the most overlooked items of the federal budget is the non-security discretionary budget. Despite accounting for only about 15 percent of federal expenditure, it includes some pretty important government functions. Half of the non-security discretionary budget accounts for the entirety of the federal government’s role in economic development, consumer protection, public safety, environmental protection, as well as portions of the safety net. The other half is made up of vital public investments in infrastructure, education, and research and development, which are necessary to keep the economy strong and globally competitive for decades to come. In fact, the non-security discretionary budget is practically the sole provider of these investments, with few existing elsewhere in the budget.

We’ve given good marks to President Obama’s 2013 budget for its upfront job creation proposals, efforts to promote tax fairness, and for realistically stabilizing the debt-to-GDP ratio over the second half of the decade (as the output gap shrinks). But unfortunately, his budget proposal achieves much of its savings by maintaining the non-security discretionary cuts in the first phase of the Budget Control Act, the debt ceiling deal that established 10-year caps on discretionary spending. As a result, his budget forces non-security discretionary outlays down to their lowest level as a share of GDP ever recorded (the data begins at 1962). That’s even lower than the Bowles-Simpson proposal!

The president has admirably made public investments a high priority, promoting increases in transportation, school facility repair and modernization, job training, R&D, and college access. But this vision is hard to reconcile with a rapidly shrinking non-security discretionary budget, as it will lead to even steeper reductions to everything else, with disastrous consequences.

Working spouses cause inequality? Can this emerging zombie lie be killed?

A major new zombie lie is being launched: The claim that high inequality is due to more working spouses in high-income households and well-off people increasingly marrying other well-off people. This was part of James Q. Wilson’s recent op-ed in the Washington Post, which I addressed in an earlier blog post (though not on this point). My zombie lie detector went wild, however, after reading a very good New York Times article detailing new research showing “the [education] achievement gap between rich and poor children is widening, a development that threatens to dilute education’s leveling effects.” At the end of the article are two statements by conservative public intellectuals, one from Douglas Besharov and one from Charles Murray, attributing income inequality to working spouses.

To recall, here’s what Wilson wrote: “Affluent people, compared with poor ones, tend to have greater education and spouses who work full time.” Wilson then suggests that if these are the drivers of inequality, then it is best not to do anything about the problem, since, in his words, “We could reduce income inequality by trying to curtail the financial returns of education and the number of women in the workforce—but who would want to do that?”

Here’s what the Times‘ Sabrina Tavernise attributed to Murray in her piece:

The growing gap between the better educated and the less educated, he [Murray] argued, has formed a kind of cultural divide that has its roots in natural social forces, like the tendency of educated people to marry other educated people, as well as in the social policies of the 1960s, like welfare and other government programs, which he [Murray] contended provided incentives for staying single.”

And here’s what Besharov told Tavernise:

There are no easy answers, in part because the problem is so complex… . Blaming the problem on the richest of the rich ignores an equally important driver, he [Besharov] said: two-earner household wealth, which has lifted the upper middle class ever further from less educated Americans, who tend to be single parents. The problem is a puzzle, he [Besharov] said. “No one has the slightest idea what will work. The cupboard is bare.”

The basic claim, it seems, is that well-off families are more likely to have working spouses and that the spouses in well-off families are both more likely to have high earnings. Presumably this phenomenon has been growing, or else it cannot explain growing inequality. I address the issue of the role of the growth of two-earner households and inequality in this post but do not address the issue of assortative mating (rich marrying rich). Also, my focus is whether the “working spouses factor” contributes at all to our understanding of the key dynamic of income inequality, the growing income gap between the top 1 percent and the middle class.

To these folks demographic, rather than economic, trends are generating income inequality. Consequently, economic policy has had no role in causing inequality and can not ameliorate inequality either. Of course, this is only the latest effort to reduce inequality to a demographic phenomenon: The State of Working America has addressed other such claims going back to the first edition in 1988.

To explain inequality is to explain first and foremost the tremendous growth of income, wages and wealth that have accrued to the top 1 percent and the top 0.1 percent since 1979. How does the “working spouse” explanation hold up?

The first thing to note is that the presence of a working spouse, even a highly paid one, can potentially impact household income inequality but says nothing about the tremendous divergence of individual wages over the last few decades. Household incomes aggregate the labor income of all household members (which depends on how many members work, how much they work and how much they are paid), non-labor income (capital gains and so on) and any pensions, government transfers and other income. As we know, the top 1 percent of households managed to more than double its share of national income between 1979 and 2007. Josh Bivens and I have argued that the dynamics underlying growing household income inequality are rising wage inequality, rising inequality in receipt of capital income (capital gains, dividends and so on) and the shift toward more capital income and less wage income. The demographic factor of working spouses is about how people combine into households and does not address and certainly cannot explain the huge increase in the wage growth of the top 1 percent of wage earners versus every other group. Here is the chart on wage growth showing the top 1 percent gaining 131 percent between 1979 and 2010 while those in the bottom 90 percent saw their annual wages rise by 15 percent (mostly in the late 1990s).

Second, we can look directly at the two–earner phenomenon among the upper 1 percent and the top 0.1 percent from the work of Jon Bakija, Adam Cole and Bradley T. Heim who analyzed tax returns from 1979 to 2005.Read more

David Brooks’ bad example

Update (4:10 p.m. ET): Here’s some data (from EPI analysis of the Current Population Survey) on the share of those employed lacking a high school diploma or a GED certificate, labeled “less than high school,” by race/ethnicity and immigration status:

Share of employment with ‘less than high school’ education, 2011 |

|||

|

Race/ethnicity |

All | Native | Immigrant |

| All | 8.4% | 5.1% | 25.9% |

| White* | 4.2% | 4.1% | 6.0% |

| Black* | 7.2% | 6.7% | 10.6% |

| Hispanic | 28.6% | 11.6% | 44.3% |

| * Excluding Hispanics | |||

Note that just 4.1 percent of the native born white workforce is in this category. Only 5.1 percent of employment of all native-born Americans lacks a high school degree or a GED, with a slightly higher share among employed native-born blacks (6.7 percent).

Original post: I was struck by David Brooks’ example of bad behavior in his New York Times column today, writing, “I don’t care how many factory jobs have been lost, it still doesn’t make sense to drop out of high school.” Paul Krugman was struck by that same sentence. Brooks’ assumption, I guess, is that many workers have low wages because they never completed high school. He’s not alone in thinking that there are a lot of high school dropouts, but this is definitely not true. As the graph shows, the share of the workforce (ages 18-64) who have neither a high school or further degree (including a GED) has dropped tremendously in the last four decades, from 28.5 percent in 1973 to just 8.4 percent in 2011, a trend true among men as well as women. Oh, by the way, half of the “high school dropouts” in the workforce are immigrants, many of whom did not go to school in the United States and came here in their teens or later. You definitely can’t blame the erosion of workers’ wages on their failure to graduate from high school, since the vast majority did.

In fact, the education levels of our workforce have grown tremendously. As another example, the share of the workforce with a college degree or further education has doubled since 1973, growing from 14.6 percent in 1973 to one-third in 2011. And, by the way, the wages of those with a college degree (but no further education) have not increased in inflation-adjusted terms in 10 years, neither in the last recovery between 2002 and 2007 nor since. I wonder what bad behavior on their part caused this to happen.

A budget for adults (especially those who’d like a job)

President Obama’s FY2013 budget request, released today, is bound to get ample criticism from the right (and center-right) for not going far enough on near-term deficit reduction. As a few different articles have already highlighted today (for instance here and here), the president’s budget request does not honor a pledge he made to halve the deficit by the end of his first term. In reality, we’d all be in pretty big trouble if this budget chose to focus on promises as opposed to economic realities. Instead, the budget put forth by the administration today is a remarkably serious one – particularly given that Obama is running for reelection this year. The administration could have relied on gimmicks and austerity measures to focus solely on deficit reduction; instead we got a document that both emphasizes job creation and manages to hit fairly reasonable fiscal targets in the medium term.

The budget includes about $350 billion in temporary tax relief and investments to create jobs and jump-start growth. These investments are heavily front-loaded between FY2012-FY2014 – in fact, 96 percent of the proposed spending on these measures takes place in those years. Much of this investment in job creation is familiar, including policies such as:

- $94 billion for an extension of the payroll tax holiday for two years

- $44 billion for reforming and extending unemployment insurance for two years

- $30 billion to modernize schools over four years

- $30 billion for teacher stabilization and supporting first responders

- $50 billion to fund surface transportation priorities through 2022, with the investment front-loaded in the first three years

As we’ve stated before, this job creation package should be evaluated based on its scale, the difference it will make in the coming few years, its effectiveness and efficiency, and the way in which it is funded. The $350 billion figure is a decent amount to be spending on job creation, an amount that would raise employment levels significantly in 2012 and 2013. That is more than we can expect to see Rep. Paul Ryan (R-Wisc.) propose in this year’s House Budget resolution. But with an 11 million jobs deficit, it still falls short of what’s needed.

Though not perfect, the investments highlighted in the budget are fairly well-targeted. Macroeconomic multipliers show that across-the-board, spending on public investments, income-support payments, state-and-local fiscal support, food stamps, infrastructure projects, unemployment insurance, and targeted refundable tax credits garner a much larger bang-per-buck than spending on various tax cuts and credits. And since our economic problems generally still stem from a lack of demand, it makes sense that boosting the ability of consumers to spend should be a top priority for the administration.

The president’s budget “funds” this investment by proposing a greater level of taxation on those who can most afford to pay – rhetoric we have been hearing from Obama for a while now. This includes around $1.5 trillion over 10 years from upper-income tax provisions, which include, among other things, letting the George W. Bush-era tax cuts expire and taxing qualified dividends as ordinary income for those making above $250,000 per year ($200,000 single filers).

Along with addressing the jobs crisis, this budget also puts the federal government on a sustainable fiscal path. The president’s budget achieves primary balance in 2018, meaning that, excluding interest payments, spending does not exceed revenues. Primary balance is a good measure for two reasons. First, interest payments are essentially payments on past—rather than current—policy decisions, so primary balance allows us to use a measure that doesn’t punish current presidents for debt that may have been incurred by past presidents. Second, primary balance also results in a stabilized debt as a share of GDP, and this budget stabilizes debt at 76.5 percent in 2022 after peaking at 78.4 percent of GDP in 2014 and gradually coming down. And while the budget does propose around $4 trillion in deficit reduction over 10 years, around $850 billion of these savings comes from capping Overseas Contingency Operations, and a good deal more comes from pursuing high-income tax cuts and other revenue proposals. Additionally, the president proposes achieving around $600 billion of that deficit reduction through health and other mandatory initiatives, almost half of which would come from Medicare providers.

As we said in a statement earlier today, this budget is not perfect and particularly disappoints when it comes to non-defense discretionary spending levels. Despite this reality, this budget does a pretty good job of investing in job growth while at the same time promoting greater fairness and responsibility.

President Obama’s FY 2013 budget: The Buffett Rule and progressive tax reform

The tax policies in President Obama’s budget request for fiscal year 2013 more closely resemble those proposed for the Joint Select Committee on Deficit Reduction (i.e., the Super Committee) last September than those included in last year’s budget request. Consequently, this year’s budget raises more revenue (ostensibly to finance job creation) and does more to restore tax progressivity than previous budgets. Like the administration’s Super Committee proposals, the president’s 2013 budget proposes comprehensive tax reform, which would aim to raise $1.5 trillion over a decade, relative to current policies, from businesses and households making over $200,000 ($250,000 for joint filers).

In his recommendations to the Super Committee, President Obama proposed that tax reform should be guided by the Buffett Rule – that “no household making over $1 million annually should pay a lower share of its income in taxes than middle-class families pay.” The 2013 budget adopts a more clearly defined Buffett Rule from the president’s State of the Union address, which stated: “If you make more than $1 million a year, you should not pay less than 30 percent in taxes.” In a progressive tax code, effective tax rates are intended to rise with income, but tax code loopholes—overwhelmingly the preferential treatment of capital income over labor income—allow some millionaires and billionaires to pay lower tax rates than middle-class households. While short on details, the president’s 2013 budget suggests that the Buffett Rule would be implemented as a new minimum tax for millionaires, replacing the existing alternative minimum tax (which falls predominantly on upper-middle-class households). The budget also suggests that the Buffett Rule would give some deference to millionaires’ charitable contributions, but would nonetheless likely ensure that tax rates rise with ability to pay.

A recent Congressional Research Service report noted: “Tax reforms that are consistent with the Buffett rule would likely include raising tax rates on capital gains and dividends.” The president’s 2013 budget moves further in this direction than his previous budget requests. The 2013 budget again proposed ending the carried interest loophole and restoring the top rate on capital gains to 20 percent, but this budget also proposes taxing upper-income households’ qualified dividends as ordinary income (instead of a preferential 20 percent rate, as previously proposed). Again equalizing the tax treatment of income derived from work and that derived from investments should be at the core of progressive tax reform. This focus reflects income and inequality trends and raises revenue from those households best able to contribute to deficit reduction (the same households that disproportionately benefit from the last decade’s regressive, deficit-financed tax cuts).

To steer Congress toward tax reform, the president’s budget identifies revenue increases of $1.9 trillion, almost $1.6 trillion of which would come from sunsetting the upper-income George W. Bush-era tax cuts, capping the rate at which tax preferences reduce tax liability for upper-income households, and reinstating the estate tax at 2009 parameters, again all relative to current policy. The remaining tax proposals include closing business tax loopholes, ending fossil fuel preferences, and reforming the international tax code, which look quite familiar. (See For Joint Select Committee, many good options: Progressive revenue proposals would narrow budget gap by trillions for an analysis of the president’s tax proposals for the Super Committee.) Relative to current policies, the tax proposals in the 2013 budget would increase revenue as a share of GDP by 1.5 percentage points over the next decade – nowhere close to restoring revenue adequacy, but nonetheless an improvement over last year’s proposed 1.3 percentage point revenue increase.

Critically, the president’s tax proposals for 2013 appear to raise more revenue than those in his previous budget requests in order to finance a slew of job creation proposals closely resembling the American Jobs Act (which the president proposed financing with many of the progressive tax reforms in this budget, including caps on a wider range of tax preferences for upper-income households). The emphasis on near-term fiscal support gradually financed by tax increases on upper-income households—which will have a relatively small adverse impact on economic activity, unlike spending cuts—is good economic and fiscal policy. Federal tax and budget policy should accommodate bigger deficits today and reduce deficits as the output gap shrinks. The president’s tax policy proposals move in the right direction on this front, but they would also help to restore fairness to the tax code and begin to temper Gilded Age-levels of income inequality.