The folly of the GOP’s ‘tax reform’ agenda

Mitt Romney and House Budget Committee Chairman Paul Ryan (R-Wis.) are both pushing “tax reform” plans that would lower marginal tax rates while broadening the base (curbing tax deductions, credits, and exclusions). Romney’s plan, for example, would reduce all individual income tax rates by a fifth—e.g., the top 35 percent rate would fall to 28 percent—and the revenue loss would be made up by limiting or eliminating unspecified tax expenditures. And he says he would do this without cutting taxes for high-income households (beyond continuing their Bush-era tax cuts), meaning that he would more or less preserve the progressivity of the current tax code (i.e., tax burden distribution).

For the moment, let’s leave aside the fact that these plans neglect to raise a dollar in additional revenue at a time when we need more revenue to put the government on a sustainable fiscal path. Why are these proposals pure folly? First, because they’re obviously not serious—if they were, the plans would lead with the tax expenditure reform rather than the rate cuts. Instead, they’re sold in manner suggesting that Romney and Ryan wanted to propose big across-the-board tax cuts but didn’t want to be seen as blowing up the deficit, so they included vague language on base-broadening in order to ignore the monumental cost of slashing tax rates.

But most importantly, these plans aren’t serious because their stated intent isn’t mathematically possible. In an analysis released Wednesday, researchers at Brookings and the Tax Policy Center analyzed a plan that is consistent with Romney’s proposal, including lowering rates by a fifth and eliminating the Alternative Minimum Tax. The researchers then attempted to construct a base-broadening approach to both make up the revenue lost from the rate cuts and maintain the progressivity of the current tax code. Read more

Potential failure

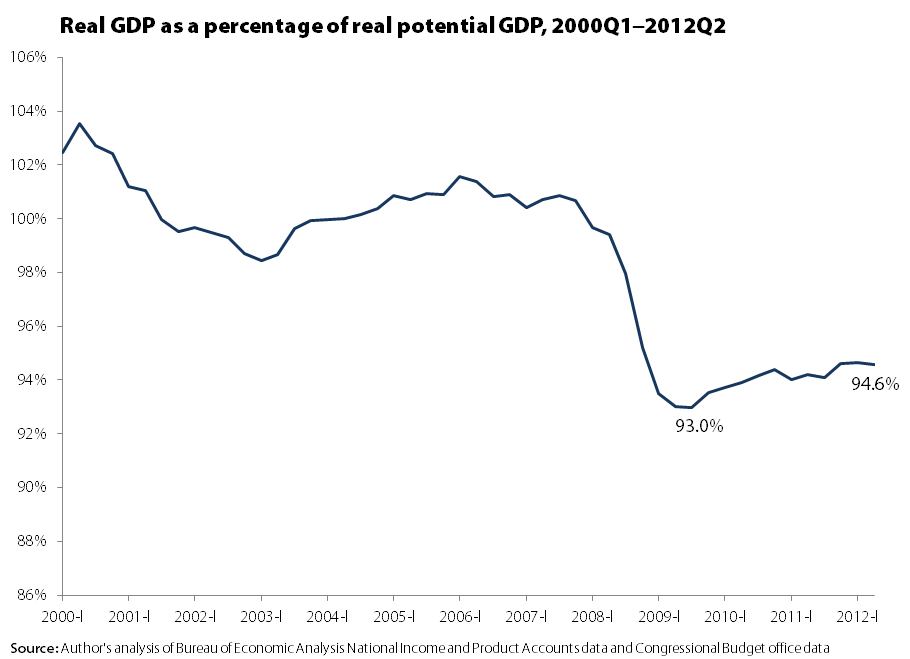

Today’s report on gross domestic product (GDP) came with more news of disappointing growth. The economy has grown at an average rate of 1.75 percent so far this year. While the economy is growing and we are not in a recession (and there’s no sign a recession is imminent), it is important to note that this slow growth is not moving the economy much closer to full health, and may even be doing real damage to that long-run health.

This problem can be highlighted by looking at actual GDP as a percentage of “potential ” GDP, a figure provided by the Congressional Budget Office. Potential GDP can be thought of as a capacity utilization rate for the whole economy: If we were utilizing all of our resources, including labor and capital, how much economic output would we be able to produce?

You can see that in 2000, actual and potential were roughly similar (actual slightly exceeds potential, in fact, because the CBO has a too-conservative view of what is the lowest sustainable rate of unemployment), but then this ratio crashes as the Great Recession hits.

At the trough of the recession in the third quarter of 2009, the U.S. economy was operating at only 93 percent of potential. In the nearly three years since, we’ve only recouped an additional 1.6 percent of potential output. Although GDP has been growing in that period, potential has been growing too (and faster), because of our increasing potential labor force and productivity growth.

Investigations reveal forced labor of immigrants but Congress won’t allow the Labor Department to combat it

Congress holds the keys to fixing many of the problems in one of the main temporary foreign worker programs used by employers to displace U.S. workers, depress wages, and exploit foreign workers. The Department of Labor has already issued the important fixes, but they’ve been temporarily enjoined by a federal court. However, going forward, Congress is considering nullifying the rules entirely by denying funding for their implementation.

The program in question is the H-2B guest worker program. On Tuesday, I joined the Southern Poverty Law Center (SPLC), the AFL-CIO, and two H-2B guest workers from Central America at the National Press Club to call on Congress to help unemployed workers have increased access to jobs in a number of occupations—including landscaping, hospitality, forestry, and seafood processing—by allowing the DOL’s new rules governing the H-2B program to come into force. The new rules would require employers to first recruit unemployed workers before turning to foreign workers, ensure that U.S. and foreign workers are not underpaid, and protect guest workers from becoming victims of forced labor and human trafficking, as well as from being retaliated against if they attempt to assert their labor and employment rights.

Although the new rules include common sense protections for U.S. and foreign guest workers, they are far from extreme or burdensome. If anything, the rules and requirements on employers are quite basic and modest.

Recently, the scandalous side of the H-2B program received some well-deserved attention from the media. A few weeks ago, a New York Times editorial, “Forced Labor on American Shores,” offered a powerful and depressing reminder that the days of forced labor (also known as slavery) are still with us. In fact, the H-2B guest worker program helps facilitate it, and in the editorial’s case, forced labor was occurring for the benefit of Walmart, the largest private employer in the world, by C.J.’s Seafood, one of its suppliers. Walmart’s size and purchasing power give it leverage to demand the lowest prices possible from its vendors and manufacturers. This in turn, can motivate suppliers like C.J.’s in Louisiana to exploit and abuse their workers in order to bring down labor costs. Read more

Confirming the further redistribution of wealth upward

A new Congressional Research Service report by Linda Levine is the first update on the distribution of wealth (including that of the top 1 percent) I’ve seen based on the recently released Federal Reserve Board (FRB) data on wealth for 2010. Levine’s analysis (see two of her tables below) shows a large upward change in the distribution of wealth over 2007-2010, with losses in the bottom 90 percent and large gains for the top 10 percent. Specifically, the bottom 90 percent in 2010 had just 25.4 percent of all wealth, down from 28.5 percent in 2007. The gainers were primarily those in the 90-to-99th percentiles (up 2.3 percentage points) of wealth, though the top 1 percent saw gains (up 0.7 percentage points) too. Levine’s data goes back to 1989 and show the wealth share of the bottom 90 percent to be at its lowest in 2010, far lower than the 32.9 percent share in both 1989 and 1992.

Levine reports data directly from the FRB showing that average wealth is down from 2007 but still far greater in 2010 ( $498,800) than in 1989 ($313,600) or 1992 ($282,900). In contrast, the wealth of the median household (wealthier than half of households but less wealthy than the other half) in 2010 was $77,300, not much different than in 1989 ($79,100) or 1992 ($75,100). In other words, wealth grew 59 percent from 1989 to 2007, but the typical household’s wealth was actually 2 percent less.

This is yet another dimension of the same old story about the economy being able to provide for most people but failing to do so, a story that will be told more fully in the forthcoming State of Working America (being released in late August). The new edition will include a more detailed report on wealth distribution from 1962 to 2010, based on an analysis by New York University’s Edward Wolff (see the last report, written by Sylvia Allegretto).

Happy birthday, CFPB

Tomorrow, the Consumer Financial Protection Bureau completes its first year of operation. Created under the Dodd-Frank Act, we’re starting to see the benefits of a strong federal agency that protects consumers from the dangers posed by an unchecked financial industry.

The CFPB notched its first enforcement action—and hopefully, the first of many—yesterday with the announcement that Capital One will pay up to $210 million to settle federal charges that it violated consumer protection requirements. According to CFPB charges, Capital One used “deceptive practices” to sell unnecessary add-ons to credit card holders. Between $140 million and $150 million will be paid to the two million customers affected. Capital One will pay another $60 million in fines, with $25 million going to the CFPB and $35 million to the bank-regulating Office of the Comptroller of the Currency.

Today, the CFPB followed up this victory with the release of a report on the private student loan industry, to which American consumers owe more than $150 billion in debt. The extensive report identifies several consumer protection issues in the private student loan marketplace. Importantly, though, the report doesn’t just stop there: It includes strong congressional policy recommendations by CFPB Director Richard Cordray and Secretary of Education Arne Duncan.

These actions by the CFPB are encouraging, but the history of financial regulation teaches us that the real challenge is maintaining vigilance over time. This means keeping up with financial intermediaries’ attempts to arbitrage between different regulatory agencies, bypass current regulatory structures, and capture regulating agencies. The CFPB had a good first year, but the real challenges will appear in the years to come.

Nearly 3 years, and counting: Minimum wage increase helps working families and the economy

At the end of March, Iowa Sen. Tom Harkin introduced the Rebuild America Act, a bill that contains important provisions to strengthen the economy and improve the well-being of working Americans. Among the many worthy elements of this bill is a proposal to increase the federal minimum wage to $9.80 by July 1, 2014. Next week will mark the third anniversary of the most recent increase in the federal minimum wage. Rather than increase the federal minimum wage annually to allow low-income workers to maintain their standard of living and share in the fruits of their ever-more productive labor as should be the case, Congress too often raises the minimum wage and then puts the well-being of low-wage workers on the back burner for years at a stretch.

As my colleague David Cooper wrote in April, increasing the federal minimum wage to $9.80 by July 1, 2014 would benefit over 28 million workers and increase national GDP by over $25 billion, in the process creating over 100,000 jobs. Given the lackluster recovery that continues to cast a pall over the nation, this positive step should be embraced by all those who care about the well-being of working families.

In a forthcoming paper, I’ll be detailing the demographic characteristics of those affected by increasing the minimum wage as proposed by Harkin (a proposal that has been mirrored in Conn. Rep. Rosa DeLauro’s Rebuild America Act and in a bill for which Calif. Rep. George Miller is currently gathering support). This paper will also highlight the state level impact of the proposed increase, breaking out state-specific demographic impacts and also highlighting the economic and employment impacts.

Here are a few graphs to whet your collective appetites:

Figure 1: Educational attainment

As seen in Figure 1, over three-quarters of those affected by the proposed increase to $9.80 have completed high school or more, including 42.3 percent who have completed some college, have an associates degree, a bachelor’s degree, or more. Read more

80% of jobs created since the recession’s end have gone to men?

The U.S. economy has created 2.6 million net jobs since the end of the Great Recession in June 2009. According to a Los Angeles Times analysis of Bureau of Labor Statistics data, men have filled 2.07 million of these new jobs. There are several possible explanations for this, and a couple of important points to keep this disparity in context:

- Men suffered higher levels of job loss during the recession than women, and their level of employment today relative to pre-recession levels is still lower than women’s.

- Women hold the majority of jobs in the public sector, which is by far the sector that has seen the worst performance since the recovery began.

- Male-dominated manufacturing is recovering, albeit slowly.

- Men are taking jobs in sectors that women have traditionally been the majority in.

The construction sector suffered the largest job losses of any industry during the recession, followed by manufacturing. These sectors are overwhelmingly male, meaning that their initial losses in the recession outpaced losses for women. Even today, unemployment among men is 8.4 percent, while for women it’s 8.0 percent.

Because women have historically filled the majority of public-sector jobs, they’ve been disproportionately affected by state and local governments’ decisions to cut positions in the wake of state fiscal troubles—a phenomenon that has largely occurred since the recession’s end. An EPI report from May found that of the 765,000 public-sector jobs lost between 2007 and 2011, 70 percent were jobs held by women. While the private sector has slowly recovered some of the jobs it lost during the recession, the public sector is still cutting them at a rapid rate; 2011 was the worst public-sector job decline on record. This public-sector employment loss is almost surely the single largest reason for women’s comparative struggles since the recovery began. Read more

The five serious flaws of Bowles-Simpson

Yesterday, a selection of past members of the Bowles-Simpson commission, anti-deficit groups like the Peterson Foundation and the Committee for a Responsible Federal Budget, and a handful of retired politicians launched the Fix the Debt Campaign in order to push a deficit reduction package in line with the original Bowles-Simpson framework (full disclosure: I served on the Bowles-Simpson commission staff in fall 2010). The event was characterized by high-minded rhetoric about coming together and solving problems and little in the way of specific policies, a reflection of the fact that in the year-and-a-half since its initial release, the Bowles-Simpson proposal has become more a symbol of seriousness and bipartisanship than an actual set of discrete recommendations that can be analyzed. This is unfortunate because the proposal itself is pretty detailed, and although it has some good components, it also has some major flaws that—without serious revision—should render it an inappropriate template for deficit reduction.

1) It would weaken the economy by cutting way too fast

The proposal admits that Congress should not cut too soon “in order to avoid shocking the fragile economy,” but addresses this by “waiting until 2012 to begin enacting programmatic spending cuts, and waiting until fiscal year 2013 before making large nominal cuts.” Given the current weak state of the economy, it’s clear that this timetable was way off. But it’s not like this was unexpected: In Aug. 2010 (three months before the Bowles-Simpson proposal was released) the Congressional Budget Office projected that the unemployment rate would be still be 8.4 percent in fiscal year 2012. Of course, it was possible that the economy would outperform this projection, but it was also possible it would underperform. Given this uncertainty, the proposal should have included an economic trigger and not just a simple-minded timeline—for example, the cuts would only take effect if the economy was experiencing healthy growth and well on its way to full recovery. At the time, EPI had recommended this trigger be set at 6 percent unemployment for six months, which in retrospect looks quite prescient.

2) It had an unbalanced ratio of spending cuts to revenue increases

The advertised ratio of spending cuts to revenue increases was 3-to-1. This isn’t totally accurate: Excluding interest savings (which are a function of both spending and revenue decisions) and including the additional revenue assumed in the baseline (i.e., the assumed conditions against which the proposal is measured) from the expiration of the high-income Bush tax cuts, the ratio was closer to 55-to-45.

But that’s still too heavily weighted towards spending cuts. Over the last two decades, budget deals have skimped on tax increases in favor of heavy spending cuts, and the most recent deal—the Budget Control Act—was 100 percent spending cuts. Furthermore, the Bush tax cuts themselves account for nearly half of the total debt accrued during this period. Finally, spending cuts exacerbate the massive and growing income inequality in this country by generally falling on middle- and low-income households (Paul Ryan’s budget, for example) while federal tax increases can be designed to ensure that high-income individuals pay their fair share. Read more

Inequality, exhibit A: Walmart and the wealth of American families

Two weeks ago saw the 50th anniversary of the opening of the first Walmart. And just a week before that, the Federal Reserve released the underlying data on family wealth from the Survey of Consumer Finances (SCF). The SCF is the survey that reported the median wealth of American families (that is, the wealth of that American family that is exactly wealthier than half of all families and less wealthy than half) fell by 38.8 percent between 2007 and 2010.

We have argued previously that Walmart is a useful archetype for trends in the larger American economy over the past three decades. Its enormous size and bargaining power has led to fabulous wealth for its owners (most notably the Walton family), while the compensation it pays its employees is generally low, even by retail standards; and the ubiquity of Walmart stores means that it is effectively the marginal employer in many U.S. counties. And its role as this marginal employer often serves to drive down workers’ wages county-wide.

The three years of wealth data from 2007 to 2010 just provides an extreme example of how the economic fortunes of Walmart’s owners have diverged from those of typical American households. Concretely, between 2007 and 2010, while median family wealth fell by 38.8 percent, the wealth of the Walton family members rose from $73.3 billion to $89.5 billion (note that the 2007 wealth number is slightly larger than was reported at the time—to provide an inflation-adjusted comparison, I converted the 2007 wealth value of $69.7 billion to 2010 dollars using the consumer price index (the CPI-U-RS, to be specific)).

In 2007, it was reported that the Walton family wealth was as large as the bottom 35 million families in the wealth distribution combined, or 30.5 percent of all American families.

And in 2010, as the Walton’s wealth has risen and most other Americans’ wealth declined, it is now the case that the Walton family wealth is as large as the bottom 48.8 million families in the wealth distribution (constituting 41.5 percent of all American families) combined.

It’s hardly a surprise that the economic circumstances of the Walton family and that of most Americans are moving in opposite directions, but some have attempted to quibble with the use of this particular statistic by noting that nearly 13 million American families have negative net worth—meaning that they have outstanding debts greater than the value of their assets. This is a bit of a strange objection—of course, many American families have negative net worth, but this is an economic reality, not a statistical fluke. Read more

Wages and Social Security

In a 2011 briefing paper, I estimated that weak and unequal wage growth accounted for more than half the projected Social Security shortfall that has emerged since 1983. Despite their importance, wages have received much less attention than life expectancy, a relatively minor factor hyped by alarmists like former Senator Alan Simpson, co-chair of President Obama’s Fiscal Commission.

Demographic trends affecting the worker-to-beneficiary ratio are often presented as inexorable, though many are influenced by public policies. Neo-Malthusian arguments exaggerating the challenges posed by a growing dependent (in this case elderly) population are used to argue that social insurance is increasingly unaffordable, ignoring productivity growth and other positive trends while falsely suggesting that policymakers have few alternatives to benefit cuts.

The Social Security system requires periodic adjustments to maintain fiscal balance and keep up with changing times. The only unusual thing about the current situation is the fact that a distant and relatively modest projected shortfall has been labeled a “crisis.” Though there have been 21 contribution rate increases in Social Security’s history, none have been legislated since the Social Security Amendments of 1983 ushered in a period of retrenchment.1

The 2012 Trustees Report puts the 75-year shortfall at just under 2.7 percent of taxable payroll, meaning that an immediate increase in employer and employee contribution rates of 1.4 percentage points (from 6.2 to 7.6 percent) would be more than enough to close the shortfall,2 as would a gradual increase in the contribution rate from 6.2 to 9.4 percent over the 75-year projection period.3 To put this in perspective, average real wages are projected to grow by a cumulative 140 percent in inflation-adjusted terms by the end of this period.4 Thus, an increase in the contribution rate would still leave future workers significantly better off than today’s workers while preventing a further erosion of the Social Security replacement rate, which is already declining from 49 percent in 1980 to 36 percent in 2080 for the prototypical “medium earner” retiring at 65. In contrast, the plan proposed by Simpson and his Fiscal Commission co-chair Erskine Bowles would result in Social Security benefits replacing just 28 percent of wages for medium earners in 2080.5 Read more