African American Youth Experienced the Largest Boost in Summer Labor Force Participation and Employment

As students head back to school this fall, today’s release of the August jobs numbers provides the first complete look at the summer job market for teens. As a whole, the stronger start to the 2015 summer jobs season (compared to last summer) signaled by the June youth employment numbers was sustained throughout the summer. According to seasonally unadjusted teen employment-to-population (EPOP) ratios, averaged for the months of June, July and August, African American youth experienced the largest boost to summer employment compared to last year. Summer employment was up 2.5 percentage points for black teens, compared to a 1.5 percentage point increase for Hispanic youth and a 1.2 percentage point increase for white teens, as shown in the figure below. Though black teens continue to have the lowest rates of employment, the 2015 summer youth employment rate for black teens was closer to its 2007 pre-Great Recession rate than were those of white and Hispanic youth.

Average teenage (16-19 years) summer employment to population ratio, 2007,2014, and 2015

| 2007 | 2014 | 2015 | |

|---|---|---|---|

| white | 43.9 | 34.3 | 35.5 |

| black | 23.0 | 19.3 | 21.8 |

| hispanic | 31.0 | 25.0 | 26.5 |

Source: EPI analysis of Current Population Survey

The Bottom Line of this Jobs Report: The Fed Should Hold the Line and Let the Economy Continue to Recover

The official unemployment rate (the U3) is only one data point—one that doesn’t include workers who have left the labor force because of weak opportunities or workers who want to be working full-time but can only get part-time work. The fact is that the economy is still not adding jobs fast enough, and the recovery is not creating strong wage growth. The best advice is for the Federal Reserve to continue doing what they’re rightfully doing—keeping rates low to let the economy recovery. Many pundits have been quick to encourage the Federal Reserve to raise rates, but a close look at the data shows that the economy still needs time to grow.

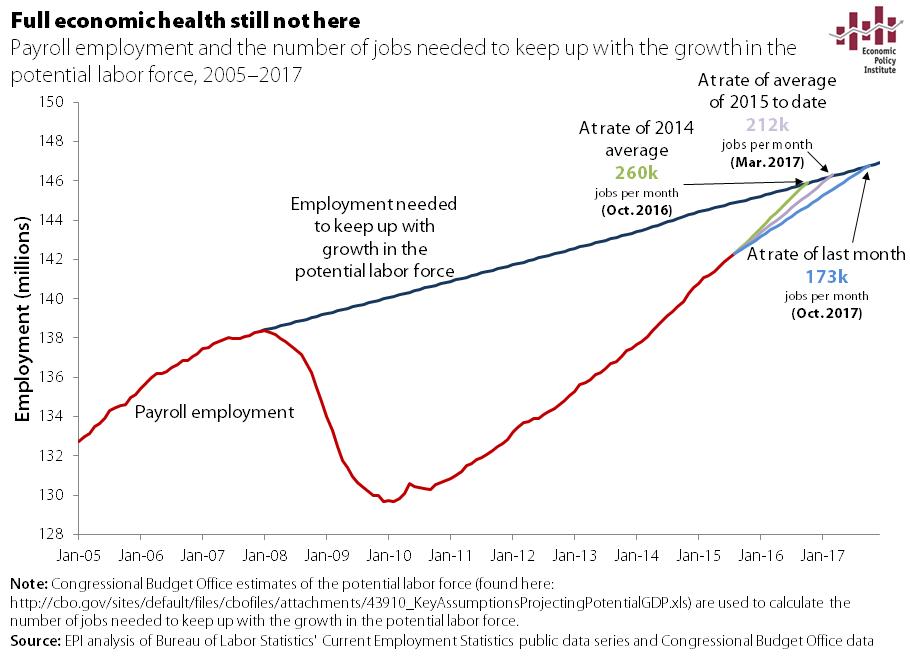

Nonfarm payroll employment rose by only 173,000 in August. While it’s best not to read too much into one month’s data, this brings average monthly job growth down to 212,000 so far in 2015. 2014 saw faster jobs growth: an average of 260,000. By that measure alone, we aren’t seeing an accelerating recovery. In fact, at this slower rate of growth, a full jobs recovery is still two years away.

A great example of just how slow this job recovery is going is the flat prime-age employment-to-population ratio (EPOP). This means the economy is only adding enough jobs to keep up with prime-age population growth—nothing more, nothing less. It means the economy is moving at a pace where we are not working off any of the joblessness that remains from the Great Recession. The prime-age EPOP in August (77.2 percent) is still below the lowest trough of the last two recessions (78.1 percent). We have a long way to go before this data point says recovery.

Why a Pro-Worker Agenda is an Anti-Poverty Agenda

This blog post originally appeared on TalkPoverty.org.

Labor Day is a time to honor America’s workers and their contributions to our economy. It is also a time to reflect upon the state of workers’ economic position, and how that position has faltered in recent decades. Except for a short period of across-the-board wage growth in the late 1990s, 2015 marks a general 36-year trend of broad-based wage stagnation and rising inequality in our country, which has had real, adverse effects on low- and middle-income households. This anemic wage growth is closely tied to the stalled progress in reducing poverty since 1979, as many poor people work and their incomes are increasingly dependent upon work. Therefore, along with strengthening the safety net, the goals of anti-poverty advocates should be one in the same with pro-worker advocates: to reverse the decades-long trend of wage stagnation and promote real wage growth for all Americans.

Despite dramatic gains in educational attainment, wages have failed to grow for those at the bottom (and middle) over the last four decades. At the same time, low income household incomes have become increasingly dependent on wages. The figure below shows the major sources of income for non-elderly households in the bottom fifth of the income distribution from 1979 to 2011, using the CBO’s measure of comprehensive income. It shows that incomes of the bottom fifth are increasingly dependent on ties to the workforce. Wages, employer-provided benefits, and tax credits that are dependent on work (such as the EITC) made up 68.3 percent of non-elderly bottom-fifth incomes in 2011, compared with only 58.2 percent in 1979. While government in-kind benefits from sources such as the Supplemental Nutrition Assistance Program (formerly food stamps) and Medicaid increased from 13.2 percent of these bottom-fifth incomes in 1979, to 19.5 percent in 2011, cash transfers such as welfare payments have declined 9.2 percentage points (from 18.6 percent to 9.4 percent).

Netflix’s Paid Parental Leave Policy Reflects a Sad Reality Facing Working Families

At the beginning of August, Netflix announced that it would grant its employees “unlimited” parental leave during the first year after a child’s birth or adoption. After the initial praise, though, a darker side of the announcement was revealed: only “salaried streaming employees”—the roughly 2,000 white-collar workers who work in the company’s streaming division—will be covered by the new policy. Employees of Netflix’s DVD distribution centers, meanwhile, will not receive the benefit of paid parental leave.

A few have asked whether or not Netflix’s paid parental leave policy will set a new standard in the American workplace. Unfortunately, the exclusion of its lower-paid workers from the policy already reflects a harsh reality facing U.S. workers: paid family leave is a rarity, and when it is offered, the recipients are much more likely to be high-wage earners.

As the figure above shows, only 12 percent of private sector workers in the United States receive paid family leave, a number that puts us behind our international peers. (Among the 34 OECD nations, for example, the United States is the only nation that does not mandate paid maternity leave.) Which workers receive paid family leave is heavily determined by how much they earn—just like Netflix’s policy. While 23 percent of workers at the top of the wage distribution have access to paid family leave, only 4 percent of workers at the bottom receive the benefit.

What to Watch on Jobs Day: The Economy Needs to Simmer for a While, Not Cool Off

This month, the Federal Open Market Committee (FOMC) will meet to decide whether to raise interest rates in order to slow down the economy and ward off incipient inflation, and I know I sound like a broken record, but, the stakes are too high not to keep repeating the same message over and over again. So let me say it again: the economy doesn’t need to cool off. It needs to simmer a while longer. Unfortunately, a serious look at the economy suggests slow growth, and not a hint of acceleration—making a rate hike terribly premature.

In light of the upcoming Federal Reserve decision, the two measures I’ll be closely watching on Friday, when the Bureau of Labor Statistics releases its monthly jobs report, are nominal hourly wage growth and the prime-age employment-to-population ratio (EPOP).

Nominal wage growth is one of the top indicators the Fed should watch as it considers whether or not to raise rates, and I don’t see much positive news there. Wage growth has been pretty flat for the last five years, as shown in the chart below. Lately, it’s been teetering in the 1.8 to 2.2 percent range. By any standard, that’s anemic. And there has certainly not been any sign of acceleration in these data.

NLRB Decision in Browning-Ferris Restores Employer Accountability for Wages and Working Conditions

Last week’s decision by the National Labor Relations Board regarding Browning-Ferris Industries of California (BFI) is a big victory for working people and labor advocates. By holding that BFI is a joint employer with the staffing agency that provides all but a few of the workers at one of BFI’s recycling centers, the decision closes one of the many loopholes corporations use to avoid paying decent wages, Social Security and Medicare taxes, worker’s compensation premiums and unemployment insurance taxes, and to avoid even providing a safe workplace.

Millions of people work for employers that want their time, their sweat, and their creativity —but don’t want to treat them as employees. The companies have put middle-men between themselves and their workers and—– thanks to Reagan-era legal changes—have avoided their responsibilities, including the duty to recognize and bargain with employee unions. Now, after 30 years of watching corporations evade these obligations with the government’s blessing, the key labor agencies of the federal government are saying, “enough is enough.” The NLRB is following the lead of David Weil, the Department of Labor’s Wage and Hour Division administrator, who has begun cracking down on phony independent contractor arrangements.

This victory, like most labor victories these days, is bittersweet. On the one hand, whenever a government agency protects or expands the rights of workers to organize and bargain collectively, or holds a corporation accountable for its treatment of workers, it is a cause for celebration. On the other hand, all the BFI decision does is restore the law regarding joint employers to where it was until 1984. Things weren’t going all that well for the labor movement even before the Reagan era, and the BFI joint employer doctrine won’t level the playing field between workers and corporations. It just turns back the clock to a fairer set of rules.

Walgreens’s ‘No Overtime’ Rule: Why I Support Raising the Overtime Threshold

My name is Caleb Sneeringer, and I worked for Walgreens for six years. I was first hired in 2008 as an assistant manager, and in 2010 I was promoted to executive assistant manager—my first salaried position with Walgreens. I earned a salary of $46,000 and was scheduled for 45 hours a week.

Unfortunately, 45 hours a week quickly turned into 55–70 hours. You see, around the time of my promotion, Walgreens implemented a “no overtime” rule for hourly employees. In my store this and other budget cuts resulted in a loss of approximately 150 hours a week among hourly employees—and their work and responsibilities were shifted to salaried staff. This created a more unpredictable scheduling situation, and many store associates were forced to use SNAP assistance (i.e., food stamps) to meet their basic needs.

Right now, the U.S. Department of Labor is considering an important rule change that would affect salaried workers and overtime pay. If implemented, the overtime salary threshold will be raised from $23,660 to $50,440. For me, my former coworkers at Walgreens, and millions of workers across the country, this rule change will mean the right to receive the overtime pay we are owed.

Victory for Home Care Workers Bodes Well for Overtime Rule

After the Department of Labor (DOL) issued regulations last year requiring third-party providers of home care services to pay the minimum wage and overtime to their employees, various employer groups filed suit in federal court in an attempt to have the new rules struck down. In short, they argued that the Secretary of Labor didn’t have the legal authority under the Fair Labor Standards Act (FLSA) to change the definition of “companionship services” it had used in the regulations it promulgated in 1975 to set wage and hour rules for home care workers. The U.S. District Court judge who heard the case, Richard Leon, didn’t just agree with the employers, he wrote a vituperative opinion expressing his outrage that the Department of Labor was arrogantly usurping congressional powers.

Calling on his inner George W. Bush, the judge declared that the Department of Labor was trying to “seize unprecedented authority to impose overtime and minimum wage obligations in defiance of the plain language of Section 213. It cannot stand.”

Last week, in Home Care Association v. Weil, a unanimous three-judge panel of the U.S. Court of Appeals for the District of Columbia Circuit disagreed with Judge Leon about the “plain language” of the statute and overruled him, finding that “the Department’s authority [to change its regulations] is clear.” The appeals court pointed out that the Supreme Court had already decided that Section 213 of the Fair Labor Standards Act doesn’t unambiguously compel any conclusion about whether third-party providers of home care services are exempt from the overtime and minimum wage requirements. Judge Leon forgot that the issue was so far from plain that back in 1975 that DOL considered covering third-party employers, before choosing not to. (How he forgot, since he cited DOL’s hesitation himself, is another story.)

Why Recent Stock Volatility Shouldn’t Factor Into Interest-Rate Hikes

This blog post originally appeared on Wall Street Journal Think Tank.

Recent volatility in stock markets in the U.S. and globally has led many economic observers to conclude that the Federal Reserve is less likely to begin raising short-term interest rates at its September meetings. I’ve been on Team Don’t Raise for a while now, but I’m not excited about those joining the cause in light of recent stock market swings.

As a general principle, the Fed should not react to short-term movements in the financial markets. For one thing, the labor market is much more important to the lives of most Americans, and it is more relevant to the Fed’s mandate of securing maximum employment with inflation stability.

Then consider this: More than 80% of stock wealth in the U.S. is owned by the wealthiest 10% of Americans, and more than half of Americans own no stocks at all (either directly or through retirement or other accounts). In short, movements in the stock markets do not have much effect on the spending power of most U.S. households. That means that movements in the stock markets—especially short-term volatility that is likely to largely dissipate—provides little information about the overall state of economic health.

How Worried Should We Be About the Stock Market’s Recent Declines?

The stock market has taken a hit in the past few days, with concern over the Chinese economy driving a big selloff. How worried should we be? The short answer is: not very.

My assessment of the underlying health of the U.S. economy hasn’t really changed over the past week, even as the stock market has declined pretty spectacularly in recent days. Why this equanimity?

A couple of things. First, stock market movements significantly change the wealth of only a small sliver of the U.S. population. Roughly 90 percent of stocks are held by the wealthiest 10 percent of the population. This means that the spending power of the vast majority of American households isn’t significantly affected by changes in stock prices.

Second, while stocks were pretty expensive in the past week, it doesn’t seem to me that there was an obvious market-wide bubble that would mean these declines were inevitable and will be enduring. Yes, some sectors and stocks (tech and “sharing economy” stocks) do look awfully bubbly. But when graded on things like price/earnings ratios—especially given today’s very low interest rates—the market overall looks expensive but not like an obvious bubble. What all this means is that recent stock market declines are most likely to redistribute wealth from today’s stock owners to tomorrow’s stock owners (who are buying up cheap stocks today).

All in all, the stock market is a terrible gauge of overall economy-wide health, so even large swings in it by themselves do not provide much of a signal for how to assess this broader health.