What to Watch on Jobs Day: A 2015 Wrap Up

With the last jobs report for 2015 coming out tomorrow, let’s step back and put it in the context of the entire year—and of the recovery as a whole. If December’s numbers come in as expected (analysts are predicting job growth around 215,000), that will be an indication of a relatively strong labor market in 2015, especially compared with the Great Recession and the beginning of the recovery. While the economy has improved, when you look at the peak in 2007 or the stronger economy of 2000, it is clear we still have a way to go before we reach full employment.

Job gains in 2015 were slower than 2014, but they remained solid—slowly eating away at the slack created by the Great Recession. The unemployment rate, and the long-term unemployment rate, measurably declined. The unemployment rate fell from a January to November average of 6.2 percent in 2014 to 5.3 percent in 2015, while the long-term unemployment rate fell from 33.5 percent to 28.1 percent over the same period.

Another key indicator is the employment-to-population ratio (EPOP) of prime age workers (25-54 years old). While prime-age EPOP increased in 2014, it has barely budged since January of 2015, even as the unemployment rate continued to fall. A flat EPOP would mean we’re only adding enough jobs to absorb new prime age population growth. Job growth has to be stronger, and sustained for a longer period, before we return to recovery level EPOPs. If job growth continues in 2016, prime-age EPOPs should start rising again, continuing their march toward recovery.

The worst part of the Fed’s rate increase? It wasn’t data-driven

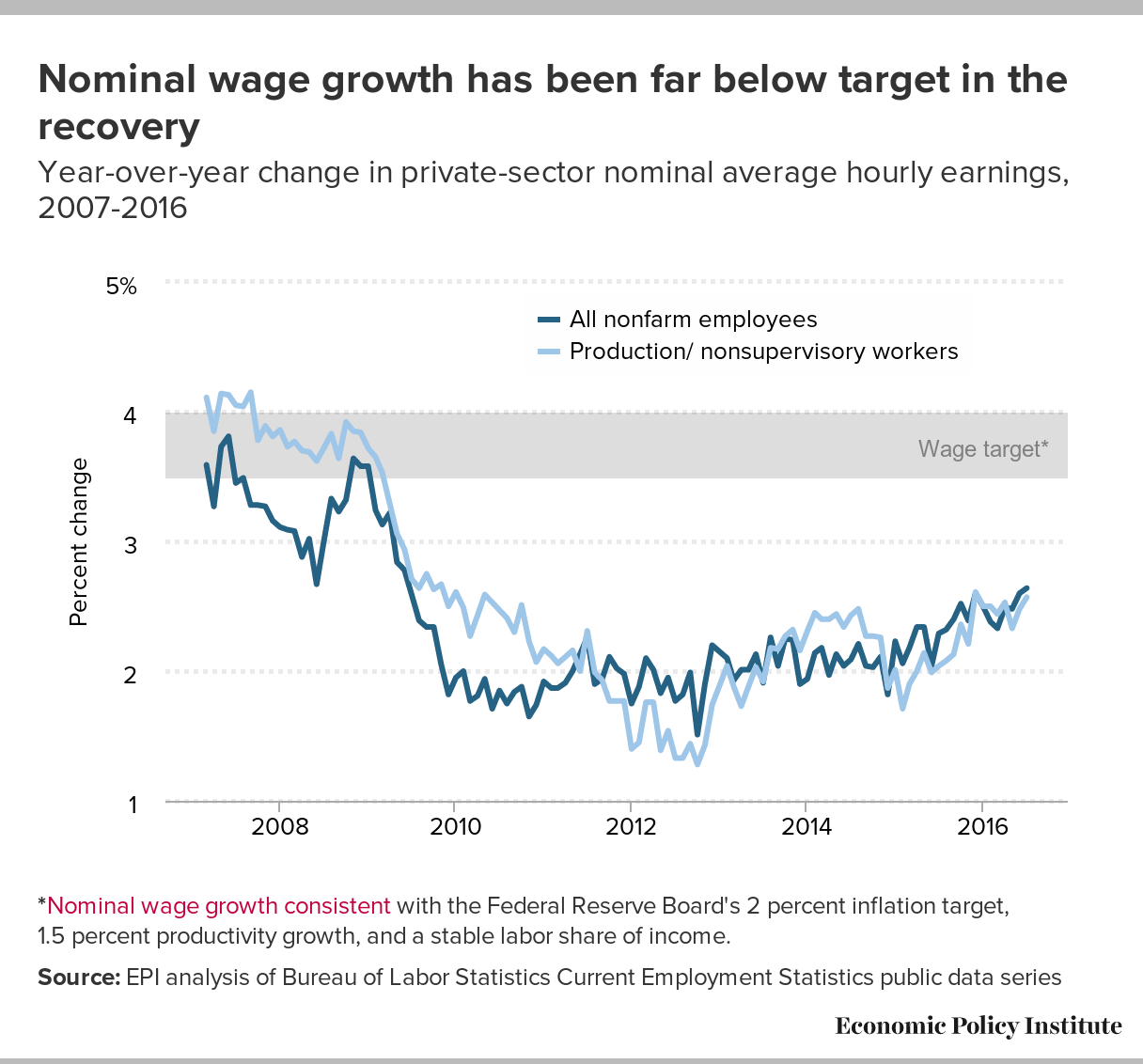

The Federal Reserve’s decision to begin nudging up interest rates in the clear absence of any inflationary pressures in economic data is disappointing. Interest rate increases should be a tool used to slow the pace of economic growth and halt downward progress on unemployment when there are clear signs of economic overheating that threaten to unsustainably push up wage and price inflation. There are no such signs in today’s economy.

{kind=link}

If last week’s hike presages a regular round of increases and monetary tightening going forward, the cost would be immense—millions of Americans would have fewer work opportunities and tens of millions would see smaller wage increases 12-18 months from now. Further, these costs would be strongly regressive, disproportionately harming low and moderate-wage workers and communities of color.

Over the past generation in the American economy, only genuine full employment like we achieved in the late 1990s has delivered strong and equitable wage growth. Because other policy decisions made over this time have eroded most sources of American workers’ bargaining power (inflation-adjusted minimum wages are low, unionization rates are low, and exposure to global competition is high), low and moderate wage workers need extraordinarily tight labor markets to achieve decent rates of hourly pay increases. A full-employment economy is particularly vital for African American and Latino workers, who continue to experience significantly higher rates of unemployment and lower rates of wage growth than other workers, but who have seen larger drops in unemployment as the recovery has proceeded.

Sen. Mikulski wrecks labor standards in H-2B guestworker program

Senator Barbara Mikulski wants the public to believe that replacing U.S. workers with lower-paid foreign guestworkers is somehow good for us and good for the economy. That’s nonsense. The economy needs good-paying jobs for U.S. workers, not jobs that pay $5 an hour less and get filled by indentured workers recruited from foreign countries.

Sen. Mikulski claims that her efforts to gut the Department of Labor’s H-2B visa program regulations are all about trying to protect the Maryland seafood industry, which she claims is at risk because few Americans are willing to take oyster and crab-shucking jobs for minimum wage. What she doesn’t tell the public is that the H-2B visa program she’s expanding—while simultaneously gutting all of its rules—is used mostly to bring in landscape laborers and gardeners, not crab pickers. Her claim that bringing in one poorly paid gardener creates four jobs in the U.S. economy—a claim concocted by a conservative think tank—is utter baloney. You can find some economist somewhere who will defend almost any claim, but that particular claim is indefensible. Bringing in landscape laborers on H-2B visas who are indentured to their employers and can’t bargain for better wages and working conditions lowers wages for Americans who would otherwise get those jobs, and it leaves more money in the employer’s pocket, but it doesn’t create additional jobs. As EPI has shown, there are no labor shortages in landscaping or other H-2B occupations, but employers want H-2B workers instead of Americans because they can control them and keep them in shocking conditions.

H-2B visas are also used to bring in indentured construction laborers at wages far below prevailing wages. Ask a construction worker in Baltimore what he thinks about seeing what used to be decent-paying construction jobs go to people from thousands of miles away when thousands of Maryland construction workers are still unemployed.

If Sen. Mikulski weren’t so concerned about the corporations itching to bring in another 200,000 guestworkers, she could guarantee an adequate supply of seafood workers by restricting the 66,000 H-2B visas already available to jobs where a real labor shortage has been found—where employers offer higher wages and still can’t find qualified workers—rather than supporting an amendment that drastically cuts wages and labor protections and opening the gates for a race to the bottom.

Labor Department’s common sense fiduciary rule survives the House of Representatives

The Obama administration deserves the nation’s thanks for standing up to the financial industry and its army of lobbyists on a matter of principle as well as practical importance: holding financial advisers accountable to their clients. Secretary of Labor Tom Perez refused to back down from a rule he proposed that would require financial advisers to act in the best interests of their clients. The rule simply requires advisors to provide what most clients probably already think they are receiving: advice about their retirement plans untainted by conflicts of interest. It would prohibit common practices such as steering investments to companies that pay the adviser a commission.

This rule would seem to be a no-brainer, but the industry makes billions of dollars from conflicted advice, and it’s used to getting its way. So the outcome of its efforts to kill the fiduciary rule was uncertain until yesterday, when it was revealed that an amendment to block the fiduciary rule was left out of the House omnibus appropriations bill.

No evidence of labor shortages but Congress considering giving H-2B employers access to more exploitable and underpaid guestworkers

Expanding and deregulating the H-2B visa program (a temporary foreign worker program that allows U.S. employers to hire low-wage guestworkers from abroad temporarily for seasonal, non-agricultural jobs, mostly in landscaping, forestry, seafood processing, and hospitality) has been a top goal for business groups including the U.S. Chamber of Commerce, ImmigrationWorks USA, landscaping and seafood employers, and the Essential Worker Immigration Coalition (EWIC)—lobbyists representing employers claiming they can’t find U.S. workers willing to mow lawns, plant trees, or pick crabmeat.

These lobbyists have never presented a credible case regarding labor shortages in H-2B jobs. But H-2B employers have spent millions of dollars on litigation, lobbying, and campaign contributions; anything it takes to keep wages from rising and to prevent their access to low-paid indentured foreign workers with few rights from ever being restricted.

And it’s happening again. To avoid a government shutdown, Congress has to pass appropriations legislation soon to fund the entire federal government. Whenever that happens, members of Congress attempt to insert “riders,” legislative provisions tucked into appropriations bills that amend the law in substantive ways that have nothing to do with appropriations. Thanks to the aforementioned corporate lobbyists, the current 2016 fiscal year appropriations negotiations have included discussions about riders to remake the H-2B program. The omnibus bill introduced in the House on the evening of December 15 included riders that would: 1) vastly increase the size of the H-2B program, 2) eliminate protections that keep workers from being idled without work or pay for long periods of time, and 3) prevent U.S. workers from having a fair shot at getting hired for job openings by preventing enforcement of the rules that require employers to recruit workers already present in the United States before they can hire an H-2B worker. Finally—and worst of all—if the House appropriations bill becomes law it will also dramatically lower the wage rates employers are required to pay, which would permit employers to pay their H-2B workers much less than American workers employed in the same jobs and local area. Needless to say, the lower wages H-2B workers will be paid create a huge incentive to hire temporary foreign workers instead of the local U.S. workers who reside in communities where the jobs are located.

In addition, legislation in the House and Senate has been introduced that would permanently implement these changes, including reducing H-2B wage rates, expanding the size of the H-2B program to about 200,000, and repealing all of the protections for foreign and American workers that the Obama administration just implemented in April 2015, after fighting opposition to them from corporate lobbyists and Congress for the past five years.

States and districts must fulfill the promise of more equity in education offered by new education law

For many of the nation’s schools, this week feels distinctly festive. Congress finally passed, and the President signed, the Every Student Succeeds Act (ESSA), reauthorizing the Elementary and Secondary Education Act (ESEA), wrapping up a nearly eight year effort.

There’s much to celebrate in the new bill. First, no more No Child Left Behind, the 2001 iteration of ESEA that shifted our flagship federal education legislation from a civil rights law supporting the nation’s neediest schools and students to one that penalized those same schools for failing to meet higher standards, while withholding many of the supports they need to do so. Second, the newly reauthorized law returns key aspects of education policy to state and local authority, making it easier for schools to target interventions and resources based on their unique contexts. Third, by incorporating such strategies as pre-kindergarten and wraparound supports for disadvantaged students, it recognizes that students’ needs—and education itself—extend beyond K-12 and the school day.

At the same time, skeptics rightly point out that many of the states and localities celebrating their renewed authority have historically used that authority pretty badly. Under ESSA, state and local education agencies must practice due diligence and recognize that with increased flexibility and autonomy comes increased responsibility. The skeptics also point out that ESSA is still a far cry from what is needed to level the education playing field. Substantially improving education and narrowing gaps requires, at a minimum, funding levels that enable ESSA to serve as a real equalizer and implementation that extends that equalizing potential at the state and local levels.

Remarks by Josh Bivens on why it is too soon for the Fed to slow the economy

On Wednesday, December 16, the Federal Reserve is expected to announce that it is raising interest rates above zero for the first time in seven years. In recent briefings and presentations, EPI Research and Policy Director Josh Bivens has argued that a rate increase would be a mistake. The following is a rough transcript of remarks delivered at events including a December 1 briefing with Rep. John Conyers.

It’s a near lock that the Fed will raise the short-term interest rates it controls off of zero this week—where they’ve been sitting since the end of 2008. I think this is a mistake. You should raise interest rates only when you think you need to start slowing the pace of economic growth because you’re worried that fast growth and falling unemployment will spark too-rapid wage growth that will bleed into rapid price inflation. But there’s no reason to think that the pace of economic growth today is excessive and needs to be slowed because of incipient inflation.1

And the stakes to getting this tradeoff between low unemployment and stable inflation wrong are huge. Since 1979, the bottom 70 percent of American workers have essentially seen one multi-year episode of strong, equitable growth in hourly pay. That occurred in the late 1990s and early 2000s, when unemployment fell far below what existing estimates said it could without sparking inflation—it bottomed out at 3.8 percent for a month in 2000, and averaged 4.1 percent for two solid years in 1999 and 2000. This led to the only serious period of strong, equitable wage growth in the past 35 years. The bottom 70 percent saw trivial wage growth (or wage declines) in the entire rest of that period. The figure below shows wage growth in the late 1990s/early 2000s compared to the rest of the 1979-2013 period for various points in the wage distribution. Besides the top 5 percent, it can be seen that most wages grew much faster during the late 1990s high-pressure labor markets than in other periods post-1979.

Republicans and some Democrats defend financial advice that’s not worth getting

What if the next time you went for a medical checkup, you were accosted by a pharmaceutical rep waiting for her expense-account lunch with the doctor. But instead of saving her pitch for the doctor—a sleazy enough practice—the drug rep began telling everyone in the room that they should take an expensive drug that has no advantage over a generic version and is approved only for medical conditions no one there has.

Illegal? Yes. But imagine that this was actually legal and that President Obama, with the support of progressives in his party, had issued a proposed rule intended to curb such practices by requiring that anyone offering advice to patients in a doctor’s office have the patient’s best interest at heart.

Here’s what would happen: Republicans in Congress would start parroting industry talking points about this having a chilling effect on urgently-needed advice people are receiving for free and can’t afford to pay for. A substantial minority of congressional Democrats would claim to agree with the president in principle, but find one reason or another to delay the rule indefinitely with quibbles and questions. The industry lobby would continue to shower Republicans with campaign donations, while the hand-wringing Democrats would avoid being singled out by the industry in their quest for reelection. Pundits would treat it as a complicated issue where there is serious risk of unintended consequences, and Americans would continue to be suckered into paying exorbitant prices for risky products they shouldn’t be buying in the first place.

The labor market still recovering: We should let it

The Job Openings and Labor Turnover Survey (JOLTS) report released today by the Bureau of Labor Statistics shows signs of a continued slow recovery. Job openings fell slightly to 5.4 million, and the quits rate remained, stubbornly, at 1.9 percent, where it has been for most of the last year. Along with last Friday’s jobs report, today’s report provides more evidence of a recovering but still weak economy. While most indicators have been trending in the right direction, nominal wage growth and the prime-age employment-to-population ratio remain far outside of target ranges, and provide ample evidence that the economy has a way to go before reaching full employment.

In October, there were 1.5 unemployed workers for every job opening, a slight tick up from last month. That means they for every 15 jobs, there are five potential workers who won’t be able to find a job no matter how hard they look. And the job-seekers-to-job-openings ratio is higher among certain sectors. Notably, there are still 45 unemployed construction workers for every 10 job openings in construction.

The sluggish quits rate is particularly troubling. At 1.9 percent, the quits rate was still 9.2 percent lower than it was in 2007, before the recession began. This is evidence that workers are stuck in jobs that they would leave if they could. A larger number of people voluntarily quitting their jobs would indicate a strong labor market—one in which workers are able to leave jobs that are not right for them and find new ones. Hopefully we will see a return to pre-recession levels of voluntary quits, but given that the rate has stayed flat, we are obviously not there yet.

December Interest Rate Increase: Will the Fed Raise Rates vs. Should It

This piece originally appeared in the Wall Street Journal’s Think Tank blog.

Our friend and former colleague Jared Bernstein has mounted a small but strategic retreat in the campaign to have the Fed continue focusing on full employment. He has written that Friday’s jobs report, though not stellar, was good enough to make a December increase in interest rates a near-certainty. He then argues that this might not be the worst thing in the world:

Even while I do not see much rationale for an increase, especially given elevated underemployment and the stark lack of inflationary pressures, given their recent messaging, a non-liftoff in December would suggest the economy is a lot worse than they thought in some secret way they’ve been keeping from us. Such a negative surprise would be ill-advised.

Presuming that they won’t want to go there, it’s now all about the ‘path to normalization:’ how fast they raise. … [I]f I’m Chair Yellen, my message to the hawks is: ‘OK, you got your rate liftoff even though the data weren’t really there for it. Now back…off and let’s go back to being data-driven about future increases.’ ”

Jared is right that the larger economic question is not just about a 25-basis-point increase this month but about how rapidly interest rates climb over the next year or so. But we’re still really uncomfortable with starting lift-off before the data support it. Once you start indulging faith-based arguments about monetary policy, you’ve lowered the bar for data-driven analysis, making smart policy choices harder and harder to sustain.