The worst part of the Fed’s rate increase? It wasn’t data-driven

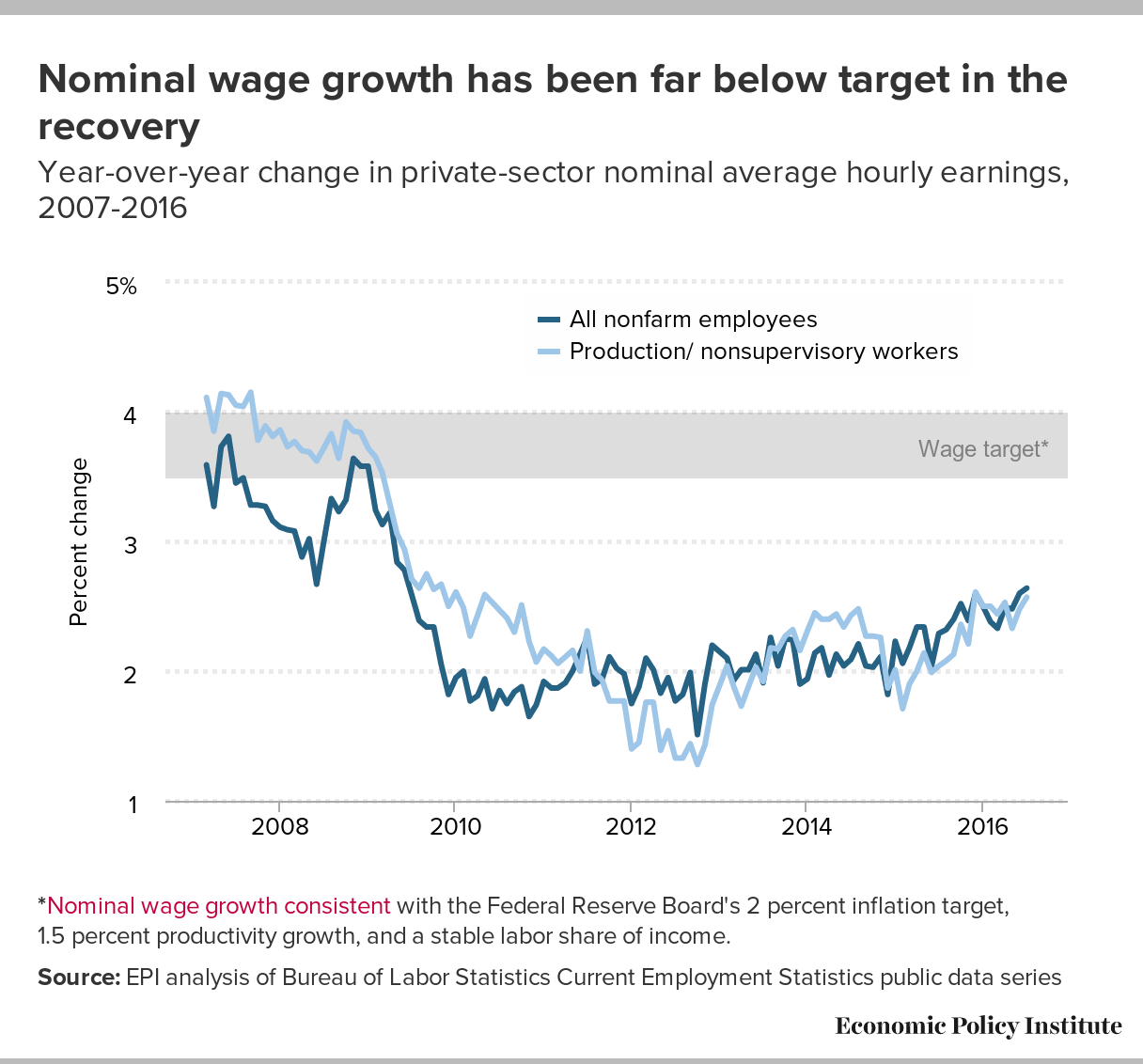

The Federal Reserve’s decision to begin nudging up interest rates in the clear absence of any inflationary pressures in economic data is disappointing. Interest rate increases should be a tool used to slow the pace of economic growth and halt downward progress on unemployment when there are clear signs of economic overheating that threaten to unsustainably push up wage and price inflation. There are no such signs in today’s economy.

{kind=link}

If last week’s hike presages a regular round of increases and monetary tightening going forward, the cost would be immense—millions of Americans would have fewer work opportunities and tens of millions would see smaller wage increases 12-18 months from now. Further, these costs would be strongly regressive, disproportionately harming low and moderate-wage workers and communities of color.

Over the past generation in the American economy, only genuine full employment like we achieved in the late 1990s has delivered strong and equitable wage growth. Because other policy decisions made over this time have eroded most sources of American workers’ bargaining power (inflation-adjusted minimum wages are low, unionization rates are low, and exposure to global competition is high), low and moderate wage workers need extraordinarily tight labor markets to achieve decent rates of hourly pay increases. A full-employment economy is particularly vital for African American and Latino workers, who continue to experience significantly higher rates of unemployment and lower rates of wage growth than other workers, but who have seen larger drops in unemployment as the recovery has proceeded.

Some will argue that last week’s hike does not presage a relatively rapid series of rate increases to follow. We certainly hope not. But because the hike happened despite the lack of any discernible inflationary pressure, we worry that decisions are being driven less by data and more by who has the best access to Fed decision makers. In particular, the 12 regional Federal Reserve bank presidents are chosen by boards of directors that are weighted heavily towards finance and the corporate sector. Of the 108 regional Fed board seats, 42 are held by representatives from the finance sector, 53 from non-financial business, and only 12 by representatives from community or consumers groups, academics, and organized labor combined.

Finance hates unexpected upticks in inflation because they transfer wealth from lenders to debtors. And genuine full employment that boosts wages for low and moderate-wage workers would nibble into the historically thick profit margins of non-financial corporations. In short, the majority of regional bank board members represent the constituency least invested in aggressively plumbing the depths of how low unemployment can really go without sparking a durable inflation.

The Fed Up campaign (with which both authors are affiliated) was started in 2014 precisely to insure that the Fed hears from a broader range of stakeholders. This coalition of community-based organizations and progressive policy groups worried that decisions about balancing the benefits of lower unemployment against the risk of inflation were too heavily weighted by the interests of finance and corporations. Last week’s decision hardly allays that fear.

The Fed’s actions from 2008 until last week have consistently aimed to spur recovery, even while Congress effectively smothered it with austerity in recent years. But their job is not yet done and the clear priority should be targeting genuine full employment, not fighting a phantom inflation. And last week’s decision highlights that there needs to be a stronger constituency that exists to demand this from the Fed.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.