On Substance, Martin O’Malley Was Right About American Wages: Don’t Let Nitpicks Convince You That There Is Not A Crisis in American Pay

Three separate sources have recently “fact-checked” claims that Martin O’Malley made about American wages in his recent speech announcing his candidacy for the Democratic nomination. The precise O’Malley quote was:

Today in America, 70 percent of us are earning the same or less than we were 12 years ago, and this is the first time that that has happened this side of World War II.

O’Malley has said that our research on wages provided a basis for his claim (examples can be found here and here).

First, let’s be clear on what our claim is and then I’ll talk about the fact checkers’ assessments of O’Malley’s use of the data.

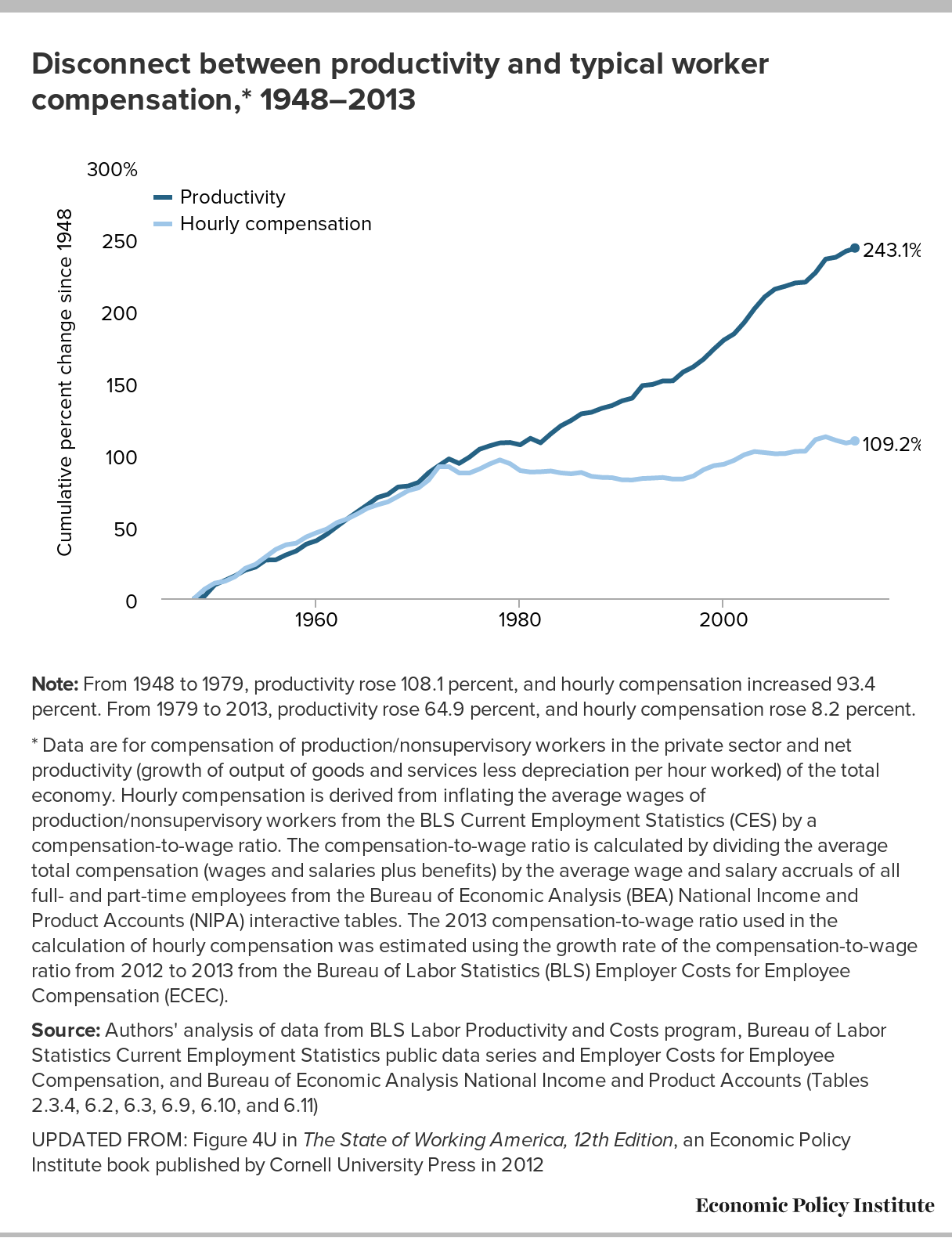

We have data on hourly wages by decile since 1973. Between 2002 and 2014, inflation-adjusted hourly wages for the bottom 7 deciles (i.e., 70 percent of the American workforce) fell. This is a remarkable economic fact and one that O’Malley is clearly right to highlight.

Further, between 1947 and 1973 there is almost certainly no 12-year period when the bottom 70 percent of wage earners saw hourly wage declines. Precise wage data by decile is sketchy over this period, but the circumstantial evidence on this is overwhelming. Just look at this graph, which shows hourly pay for a grouping reflecting the bottom 80 percent of the workforce rising sharply until the early 1970s.

{kind=link}

What Can the TPP Offer Canada? Not Much.

When Canada joined the Trans-Pacific Partnership talks in 2012 it did so somewhat reluctantly and, like Mexico, with strings attached. One of them was that Canadian negotiators could not reopen any closed text. So, in this sense, it’s been a bit of a raw deal for the Obama administration’s NAFTA partners from the beginning. Canada’s bigger business lobbies called it a defensive move, to “secure” NAFTA supply chains rather than offering any meaningful market access elsewhere. The Canadian public have almost no idea what’s going on. But as TPP countries appear to be close to the end game, people here are starting to ask the obvious questions: what’s in it for us, and what will we have to give up to get it. The answers are equally obvious if you look past the hype: not much, and quite a lot.

To begin with, Canada already has free trade deals in place with four of the larger TPP countries (Peru, Chile, the United States, and Mexico), and tariffs on trade with the others—representing 3 percent of imports and 5 percent of exports—are very low. Canada has a trade deficit with these non-FTA countries of $5 to $8 billion annually, and 80 percent of Canada’s top exports to these countries are raw or semi-processed goods (e.g., beef, coal, lumber), while 85 percent of imports are of higher value-added goods (e.g., autos, machinery, computer and electrical components). This Canadian trade deficit will likely widen if the TPP is ratified, as the United States found two years into its FTA with South Korea.

Tariff removal through the TPP is therefore likely to worsen the erosion of the Canadian manufacturing sector and jobs that has been taking place since NAFTA—a result, in part, of the limits free trade deals place on performance requirements and production-sharing arrangements. NAFTA-driven restructuring did not even have the promised effect of raising Canadian productivity levels, which languish at 70 percent of U.S. levels twenty years into the agreement. Instead, Canada has experienced greater corporate concentration, a significant decline in investment in new production, and rising inequality.

In short, there is little trade expansion upside for Canada in this negotiation. And yet the Canadian public will eventually be asked to make considerable public policy concessions to see the TPP through. As many U.S. commentators have argued, the trade impacts of TPP are far less important than the serious concerns it raises about excessive intellectual property rights, regulatory harmonization, and the perpetuation of a controversial investor-state dispute settlement (ISDS) regime that has been extremely damaging to democratic governance globally, not to mention quite humiliating for Canada.

Et Tu, Mickey Mouse? Disney Pads Record Profits by Replacing U.S. Workers with Cheaper H-1B Guestworkers

There was a lot to celebrate in the Magic Kingdom this year. The Disney Corporation had its most profitable year ever, with profits of $7.5 billion—up 22 percent from the previous year. Disney’s stock price is up approximately 150 percent over the past three years. These kinds of results have paid off handsomely for its CEO Bob Iger, who took home $46 million in compensation last year.

Disney prides itself on its recipe for “delighting customers,” a recipe it says includes putting employees first. They tout this as a key to their success in creating “a culture where going the extra mile for customers comes naturally” for employees. One method of creating this culture is referring to its employees as “cast members.” In fact, Disney is so proud of its organizational culture that it’s even created an institute to share its magic with other businesses (for a consulting fee, of course).

So, you would expect a firm that puts its employees first to share the vast prosperity that’s been created with the very employees who went above and beyond to help generate those record profits.

Well, how did Mr. Iger repay his workers—sorry, I mean cast members—for creating all this profit? Not with bonuses and a big raises. Instead, as the New York Times just detailed in a major report, he forced hundreds of them to train their own replacements—temporary foreign workers here on H-1B guestworker visas—before he laid them off.

Don’t Pop the Champagne Corks Yet: Putting Year-over-Year Hourly Earnings Growth in Perspective

Average hourly earnings hit $24.96 in May, an increase of 2.3 percent over May 2014. We’ve been tracking nominal wage growth over the recovery and at best we can find reason for only a very modest celebration. 2.3 percent growth is a move in the right direction, but it’s nowhere near the 3.5 to 4.0 percent growth we expect in a healthy labor market.

As shown in the figure below, average hourly wage growth has been teetering around 2.0 percent for the last five years. There has been a slight increase in the annual twelve-month growth trend this past month to 2.3 percent from the trends observed in earlier months this year, which hovered between 2.0 and 2.2 percent. This may be a temporary increase, as we’ve seen 2.3 percent before. Even more important is that a 2.3 percent annual growth in wages is far below target, as the graph shows.

Nominal wage growth has been far below target in the recovery: Year-over-year change in private-sector nominal average hourly earnings, 2007–2015

| All nonfarm employees | Production/nonsupervisory workers | |

|---|---|---|

| Mar-2007 | 3.5910224% | 4.1112455% |

| Apr-2007 | 3.2738095% | 3.8461538% |

| May-2007 | 3.7257824% | 4.1441441% |

| Jun-2007 | 3.8062284% | 4.1267943% |

| Jul-2007 | 3.4482759% | 4.0524434% |

| Aug-2007 | 3.4940945% | 4.0404040% |

| Sep-2007 | 3.2827046% | 4.1493776% |

| Oct-2007 | 3.2778865% | 3.7780401% |

| Nov-2007 | 3.2714844% | 3.8869258% |

| Dec-2007 | 3.1599417% | 3.8123167% |

| Jan-2008 | 3.1067961% | 3.8619075% |

| Feb-2008 | 3.0947776% | 3.7296037% |

| Mar-2008 | 3.0813674% | 3.7746806% |

| Apr-2008 | 2.8818444% | 3.7037037% |

| May-2008 | 3.0172414% | 3.6908881% |

| Jun-2008 | 2.6666667% | 3.6186100% |

| Jul-2008 | 3.0000000% | 3.7227950% |

| Aug-2008 | 3.3285782% | 3.8263849% |

| Sep-2008 | 3.2258065% | 3.6425726% |

| Oct-2008 | 3.3159640% | 3.9249147% |

| Nov-2008 | 3.6406619% | 3.8548753% |

| Dec-2008 | 3.5815269% | 3.8418079% |

| Jan-2009 | 3.5781544% | 3.7183099% |

| Feb-2009 | 3.2363977% | 3.6516854% |

| Mar-2009 | 3.1293788% | 3.5254617% |

| Apr-2009 | 3.2212885% | 3.2924107% |

| May-2009 | 2.8358903% | 3.0589544% |

| Jun-2009 | 2.7829314% | 2.9379157% |

| Jul-2009 | 2.5889968% | 2.7056875% |

| Aug-2009 | 2.3930051% | 2.6402640% |

| Sep-2009 | 2.3437500% | 2.7457441% |

| Oct-2009 | 2.3383769% | 2.6272578% |

| Nov-2009 | 2.0529197% | 2.6746725% |

| Dec-2009 | 1.8198362% | 2.5027203% |

| Jan-2010 | 1.9545455% | 2.6072787% |

| Feb-2010 | 1.9990913% | 2.4932249% |

| Mar-2010 | 1.7663043% | 2.2702703% |

| Apr-2010 | 1.8091361% | 2.4311183% |

| May-2010 | 1.9439421% | 2.5903940% |

| Jun-2010 | 1.7148014% | 2.5309639% |

| Jul-2010 | 1.8476791% | 2.4731183% |

| Aug-2010 | 1.7528090% | 2.4115756% |

| Sep-2010 | 1.8410418% | 2.2982362% |

| Oct-2010 | 1.8817204% | 2.5066667% |

| Nov-2010 | 1.6540009% | 2.2328549% |

| Dec-2010 | 1.7426273% | 2.0700637% |

| Jan-2011 | 1.9170753% | 2.1704606% |

| Feb-2011 | 1.8708241% | 2.1152829% |

| Mar-2011 | 1.8691589% | 2.0613108% |

| Apr-2011 | 1.9102621% | 2.1097046% |

| May-2011 | 1.9955654% | 2.1567596% |

| Jun-2011 | 2.1295475% | 1.9957983% |

| Jul-2011 | 2.2566372% | 2.3084995% |

| Aug-2011 | 1.8992933% | 1.9884877% |

| Sep-2011 | 1.9400353% | 1.9331243% |

| Oct-2011 | 2.1108179% | 1.7689906% |

| Nov-2011 | 2.0228672% | 1.7680707% |

| Dec-2011 | 1.9762846% | 1.7680707% |

| Jan-2012 | 1.7497813% | 1.3989637% |

| Feb-2012 | 1.8801924% | 1.4500259% |

| Mar-2012 | 2.0969856% | 1.7607457% |

| Apr-2012 | 2.0052310% | 1.7561983% |

| May-2012 | 1.8260870% | 1.3903193% |

| Jun-2012 | 1.9548219% | 1.5447992% |

| Jul-2012 | 1.7741238% | 1.3333333% |

| Aug-2012 | 1.8205462% | 1.3340174% |

| Sep-2012 | 1.9896194% | 1.4351615% |

| Oct-2012 | 1.5073213% | 1.2781186% |

| Nov-2012 | 1.8965517% | 1.4307614% |

| Dec-2012 | 2.1963824% | 1.7373531% |

| Jan-2013 | 2.1496131% | 1.8906490% |

| Feb-2013 | 2.1030043% | 2.0418581% |

| Mar-2013 | 1.9255456% | 1.8829517% |

| Apr-2013 | 2.0085470% | 1.7258883% |

| May-2013 | 2.0068318% | 1.8791265% |

| Jun-2013 | 2.1303792% | 2.0283976% |

| Jul-2013 | 1.9132653% | 1.9230769% |

| Aug-2013 | 2.2562793% | 2.1772152% |

| Sep-2013 | 2.0356234% | 2.1728146% |

| Oct-2013 | 2.2486211% | 2.2715800% |

| Nov-2013 | 2.2419628% | 2.3173804% |

| Dec-2013 | 1.8963338% | 2.1597187% |

| Jan-2014 | 1.9360269% | 2.3069208% |

| Feb-2014 | 2.1437579% | 2.4512256% |

| Mar-2014 | 2.1830395% | 2.3976024% |

| Apr-2014 | 1.9689987% | 2.3952096% |

| May-2014 | 2.1347844% | 2.4426720% |

| Jun-2014 | 2.0442219% | 2.3359841% |

| Jul-2014 | 2.0859408% | 2.4329692% |

| Aug-2014 | 2.2064946% | 2.4777007% |

| Sep-2014 | 2.0365752% | 2.2749753% |

| Oct-2014 | 2.0331950% | 2.2704837% |

| Nov-2014 | 2.1100538% | 2.2648941% |

| Dec-2014 | 1.8196857% | 1.8682399% |

| Jan-2015 | 2.2295623% | 2.0098039% |

| Feb-2015 | 1.975309% | 1.6601563% |

| Mar-2015 | 2.095316% | 1.853659% |

| Apr-2015 | 2.21857% | 1.900585% |

| May-2015 | 2.295082% | 2.043796% |

* Nominal wage growth consistent with the Federal Reserve Board's 2 percent inflation target, 1.5 percent productivity growth, and a stable labor share of income.

Source: EPI analysis of Bureau of Labor Statistics Current Employment Statistics public data series

More Hope about the Labor Market Can Lead to a Higher Unemployment Rate

That’s what happened in May. We saw solid job growth in payroll employment (+280,000 jobs). At the same time, we saw a solid increase in the civilian labor force—nearly 400,000 more people in the labor force in May. It’s not surprising then that the unemployment rate (by definition, the number of unemployed people divided by the labor force) increased slightly (though not significantly, statistically speaking). Regardless, this “rise” is actually a positive sign.

The weak labor market has sidelined millions of “missing workers,” or potential workers who, because of weak job opportunities, are neither employed nor actively seeking a job. In other words, these are people who would be either working or looking for work if job opportunities were significantly stronger. An increase in optimism about the labor market leads to more people actively seeking employment. As expected, a rise in the labor force in May corresponded with a decline in the estimated number of missing workers.

* Potential workers who, due to weak job opportunities, are neither employed nor actively seeking work Note: Volatility in the number of missing workers in 2006–2008, including cases of negative numbers of missing workers, is simply the result of month-to-month variability in the sample. The Great Recession–induced pool of missing workers began to form and grow starting in late 2008. Source: EPI analysis of Current Population Survey public data seriesMillions of potential workers sidelined: Missing workers,* January 2006–May 2015

Date

Missing workers

2006-01-01

610,000

2006-02-01

160,000

2006-03-01

190,000

2006-04-01

300,000

2006-05-01

170,000

2006-06-01

110,000

2006-07-01

60,000

2006-08-01

-140,000

2006-09-01

90,000

2006-10-01

-130,000

2006-11-01

-380,000

2006-12-01

-650,000

2007-01-01

-670,000

2007-02-01

-480,000

2007-03-01

-420,000

2007-04-01

340,000

2007-05-01

200,000

2007-06-01

80,000

2007-07-01

90,000

2007-08-01

560,000

2007-09-01

150,000

2007-10-01

480,000

2007-11-01

-140,000

2007-12-01

-250,000

2008-01-01

-790,000

2008-02-01

-330,000

2008-03-01

-480,000

2008-04-01

-260,000

2008-05-01

-730,000

2008-06-01

-610,000

2008-07-01

-640,000

2008-08-01

-650,000

2008-09-01

-350,000

2008-10-01

-550,000

2008-11-01

-300,000

2008-12-01

-300,000

2009-01-01

-100,000

2009-02-01

-230,000

2009-03-01

210,000

2009-04-01

-130,000

2009-05-01

-200,000

2009-06-01

-260,000

2009-07-01

120,000

2009-08-01

410,000

2009-09-01

1,220,000

2009-10-01

1,350,000

2009-11-01

1,400,000

2009-12-01

2,100,000

2010-01-01

1,660,000

2010-02-01

1,540,000

2010-03-01

1,320,000

2010-04-01

770,000

2010-05-01

1,330,000

2010-06-01

1,710,000

2010-07-01

1,880,000

2010-08-01

1,490,000

2010-09-01

1,850,000

2010-10-01

2,320,000

2010-11-01

1,960,000

2010-12-01

2,390,000

2011-01-01

2,460,000

2011-02-01

2,630,000

2011-03-01

2,430,000

2011-04-01

2,500,000

2011-05-01

2,590,000

2011-06-01

2,670,000

2011-07-01

3,110,000

2011-08-01

2,520,000

2011-09-01

2,510,000

2011-10-01

2,540,000

2011-11-01

2,510,000

2011-12-01

2,470,000

2012-01-01

2,780,000

2012-02-01

2,540,000

2012-03-01

2,530,000

2012-04-01

2,890,000

2012-05-01

2,480,000

2012-06-01

2,240,000

2012-07-01

2,770,000

2012-08-01

2,830,000

2012-09-01

2,690,000

2012-10-01

2,130,000

2012-11-01

2,480,000

2012-12-01

2,060,000

2013-01-01

2,340,000

2013-02-01

2,690,000

2013-03-01

3,130,000

2013-04-01

2,880,000

2013-05-01

2,740,000

2013-06-01

2,580,000

2013-07-01

2,860,000

2013-08-01

3,010,000

2013-09-01

3,130,000

2013-10-01

3,810,000

2013-11-01

3,360,000

2013-12-01

3,550,000

2014-01-01

3,420,000

2014-02-01

3,200,000

2014-03-01

2,840,000

2014-04-01

3,670,000

2014-05-01

3,410,000

2014-06-01

3,320,000

2014-07-01

3,170,000

2014-08-01

3,260,000

2014-09-01

3,580,000

2014-10-01

3,060,000

2014-11-01

3,030,000

2014-12-01

3,230,000

2015-01-01

2,860,000

2015-02-01

3,110,000

2015-03-01

3,330,000

2015-04-01

3,140,000

2015-05-01

2,830,000

Yes, the Employment Report Was Decent. But No, The Labor Market Isn’t Strong.

Yes, this morning’s jobs report had some welcome news. Payroll employment was up 280,000 jobs, slightly above the trend of the previous six months. But the recovery is far from complete: there is still a three million job shortfall in the economy today.

The recent trends in job growth predict a slow march back to full recovery. If we continued to add 280,000 jobs a month into the future, we wouldn’t fill the jobs gap until August 2016—more than a year away. Over the last six months, average job growth was 236,000. If we continued to add jobs at that pace, the gap wouldn’t close until the end of 2016. The three month average of 207,000 jobs (much slower because of the poor March report) moves full recovery even farther into the future—at that pace, we wouldn’t return to pre-recession labor market health until April 2017.

Furthermore, it’s important to remember that the 2007 labor market is still a low bar and that recovery is not just about jobs. Nominal wage growth continues to be far below target. Yes, 2.3 percent wage growth is an improvement, but it’s nowhere near strong enough to call for rate hikes. The Fed should not feel comfortable raising rates in September—in fact, they shouldn’t even begin to think about having a conversation about raising rates until 2016.

Don’t Forget about High School Grads

Last week, we released The Class of 2015, our annual report examining the job and wage prospects for newly-minted high school and college graduates. When we release this study, the media tend to focus on the chances college graduates have for snagging a job. But I want to submit a humble plea: don’t forget about the high school grads. After all, they make up the majority of young people.

Only 9.7 percent of young people between the ages of 17 and 24 have a college degree or more. 52.7 percent, meanwhile, have a high school degree or less (as shown in Table 1), and another 37.6 percent have only some college experience. And this trend isn’t unique to young people—even when you look at workers who are a little bit older, college graduates are still a minority. A significant share of workers age 24–29 have only a high school degree (26.4 percent) or some college experience (30.7 percent) and only 34.1 percent have a bachelor’s or advanced degree.

* Data reflect 12-month moving average as of March 2015. Note: Race/ethnicity categories are mutually exclusive (i.e., white non-Hispanic, black non-Hispanic, and Hispanic any race). Source: EPI analysis of basic monthly Current Population Survey microdataHighest degree earned, by age and demographic, 2015*

Age 17–24

Age 24–29

All

Men

Women

White

Black

Hispanic

All

Men

Women

White

Black

Hispanic

Less than high school

24.8%

26.1%

23.5%

22.5%

26.6%

30.9%

8.9%

9.7%

8.0%

4.6%

9.2%

21.6%

High school

27.9%

30.1%

25.7%

26.1%

32.2%

32.1%

26.4%

29.9%

22.9%

23.8%

33.0%

32.5%

Some college

37.6%

35.8%

39.5%

39.2%

35.9%

32.9%

30.7%

29.4%

32.0%

30.4%

36.7%

29.9%

Bachelor’s degree

9.0%

7.5%

10.5%

11.5%

4.9%

3.8%

26.6%

24.6%

28.5%

32.5%

17.2%

13.3%

Advanced degree

0.7%

0.6%

0.9%

0.8%

0.5%

0.3%

7.5%

6.4%

8.5%

8.6%

4.0%

2.8%

When you look at the wages that young people with a high school degree are making, they are far less than what college grads can expect. The average young high school graduate who does not enroll in further schooling makes $10.40 an hour, which has declined 5.5 percent from the $11.01 they were making in 2000. $10.40 an hour translates to an average full-time, full-year worker salary of just $21,632 for high school graduates. To put that in perspective, that is less than is needed to lift a four-person family above the poverty line and less than the amount needed for a one adult, one child family to get by in every area in the United States.

What to Watch on Jobs Day: What’s at Stake at the Upcoming FOMC Meeting and the Outlook for Young Workers

In tomorrow’s release of the Employment Report, I’m primarily looking for evidence confirming that the Federal Reserve should continue to stay the course through its June (and most likely September) meetings. I’ll also be looking more closely at the labor market for young people: specifically, youth entering the labor market in the summer and prospects for recent high school grads.

When the Federal Open Market Committee meets in two weeks, they will almost surely continue their current agenda and resist pressure to raise interest rates. Raising interest rates prematurely would slow the recovery, which is still in much need of oxygen. Job growth sputtered in March, but picked up again in April. If the economy continues to grow at an average of 191,000 jobs a month (as it has for the past three months), it will return to pre-Great Recession labor market health by August 2017. If you want to downplay the very weak March data, then the average job growth over the past six months (255,000 jobs per month) moving forward gets us back to prerecession health by October 2016.

All measures point to a slowly recovering economy, but an economy that is still far from the health of 2007, let alone the health of the far-stronger economy of 2000. The employment-to-population ratio remains seriously depressed, and there are still over 3 million potential workers sidelined by the weak labor market. Further, wage growth has continued to fall flat—nominal hourly wage growth has remained at around 2 percent over the last five years, far below any reasonable target.

Now that the college graduating class of 2015 has begun to try their luck in the labor market, it’s time to consider how 2015’s high school graduates are expected to do as they graduate this month. Extensive details on the specifics of the high school graduates—including underemployment and wages—are available here. Below is a chart of the unemployment rates of everyone in the labor force versus those under 25 years old and the youngest potential workers, those between 16 and 19 years old. While the unemployment rates for all groups have declined precipitously during the recovery, two other facts are readily apparent. First, the unemployment rates for any of them have not fully recovered (and it’s important to remember that this measure of unemployment fails to include those working part-time that want full time jobs or those who may have just recently given up looking for work). Second, the younger the potential labor mark entrant, the higher the unemployment rate—and the farther those younger cohorts are from a healthy unemployment rate. Unfortunately, this does not bode well for young workers looking for summer employment or their first job out of high school or college.

Note: Shaded areas denote recessions. Data are seasonally adjusted. Source: Economic Policy Institute analysis of Bureau of Labor Statistics Current Population Survey public data seriesUnemployment rate of workers by age group, 1969–2015

Date

All

16–24

16–19

1969-01-01

3.4%

8.2%

12.0%

1969-02-01

3.4%

8.1%

11.9%

1969-03-01

3.4%

8.3%

12.3%

1969-04-01

3.4%

8.2%

12.0%

1969-05-01

3.4%

8.3%

12.4%

1969-06-01

3.5%

8.3%

12.2%

1969-07-01

3.5%

8.7%

12.8%

1969-08-01

3.5%

8.2%

12.2%

1969-09-01

3.7%

8.9%

12.6%

1969-10-01

3.7%

8.8%

12.6%

1969-11-01

3.5%

8.2%

11.6%

1969-12-01

3.5%

8.4%

11.8%

1970-01-01

3.9%

9.3%

13.5%

1970-02-01

4.2%

9.8%

13.3%

1970-03-01

4.4%

9.6%

13.4%

1970-04-01

4.6%

10.4%

14.7%

1970-05-01

4.8%

10.4%

14.2%

1970-06-01

4.9%

11.2%

16.3%

1970-07-01

5.0%

11.0%

14.7%

1970-08-01

5.1%

11.4%

15.7%

1970-09-01

5.4%

12.1%

16.2%

1970-10-01

5.5%

12.2%

16.7%

1970-11-01

5.9%

12.9%

17.4%

1970-12-01

6.1%

12.8%

17.1%

1971-01-01

5.9%

12.6%

16.8%

1971-02-01

5.9%

12.5%

16.3%

1971-03-01

6.0%

12.8%

16.9%

1971-04-01

5.9%

12.5%

16.3%

1971-05-01

5.9%

13.0%

16.8%

1971-06-01

5.9%

13.2%

17.7%

1971-07-01

6.0%

12.9%

17.7%

1971-08-01

6.1%

12.8%

16.8%

1971-09-01

6.0%

12.4%

16.7%

1971-10-01

5.8%

12.4%

16.9%

1971-11-01

6.0%

13.0%

16.9%

1971-12-01

6.0%

12.7%

16.9%

1972-01-01

5.8%

12.7%

16.9%

1972-02-01

5.7%

12.8%

18.0%

1972-03-01

5.8%

12.8%

17.2%

1972-04-01

5.7%

12.4%

16.5%

1972-05-01

5.7%

11.8%

15.3%

1972-06-01

5.7%

11.8%

15.9%

1972-07-01

5.6%

12.0%

15.6%

1972-08-01

5.6%

12.1%

16.5%

1972-09-01

5.5%

12.0%

16.3%

1972-10-01

5.6%

12.0%

15.8%

1972-11-01

5.3%

11.5%

15.7%

1972-12-01

5.2%

11.3%

15.6%

1973-01-01

4.9%

10.2%

13.7%

1973-02-01

5.0%

10.9%

15.3%

1973-03-01

4.9%

10.4%

14.3%

1973-04-01

5.0%

11.0%

15.5%

1973-05-01

4.9%

10.7%

14.9%

1973-06-01

4.9%

10.4%

13.8%

1973-07-01

4.8%

10.6%

14.3%

1973-08-01

4.8%

10.3%

14.0%

1973-09-01

4.8%

10.7%

14.7%

1973-10-01

4.6%

10.0%

14.4%

1973-11-01

4.8%

10.4%

15.0%

1973-12-01

4.9%

10.5%

14.6%

1974-01-01

5.1%

10.8%

14.6%

1974-02-01

5.2%

11.0%

14.9%

1974-03-01

5.1%

10.7%

14.9%

1974-04-01

5.1%

10.5%

14.3%

1974-05-01

5.1%

11.3%

15.4%

1974-06-01

5.4%

11.8%

16.3%

1974-07-01

5.5%

12.1%

16.8%

1974-08-01

5.5%

11.7%

14.9%

1974-09-01

5.9%

12.6%

17.0%

1974-10-01

6.0%

12.5%

17.2%

1974-11-01

6.6%

13.4%

17.8%

1974-12-01

7.2%

14.2%

18.2%

1975-01-01

8.1%

15.1%

19.5%

1975-02-01

8.1%

15.6%

19.4%

1975-03-01

8.6%

16.2%

19.9%

1975-04-01

8.8%

16.5%

19.9%

1975-05-01

9.0%

16.9%

20.4%

1975-06-01

8.8%

16.3%

20.9%

1975-07-01

8.6%

16.6%

20.7%

1975-08-01

8.4%

16.3%

20.7%

1975-09-01

8.4%

16.1%

19.5%

1975-10-01

8.4%

16.1%

19.8%

1975-11-01

8.3%

15.7%

19.0%

1975-12-01

8.2%

15.6%

19.8%

1976-01-01

7.9%

15.4%

19.6%

1976-02-01

7.7%

14.7%

19.0%

1976-03-01

7.6%

14.6%

18.9%

1976-04-01

7.7%

14.9%

19.5%

1976-05-01

7.4%

14.3%

18.6%

1976-06-01

7.6%

14.5%

18.5%

1976-07-01

7.8%

14.2%

18.3%

1976-08-01

7.8%

15.0%

19.6%

1976-09-01

7.6%

14.4%

18.6%

1976-10-01

7.7%

14.9%

19.0%

1976-11-01

7.8%

14.9%

19.2%

1976-12-01

7.8%

14.8%

19.1%

1977-01-01

7.5%

14.3%

18.9%

1977-02-01

7.6%

14.5%

18.4%

1977-03-01

7.4%

14.2%

18.6%

1977-04-01

7.2%

13.7%

18.0%

1977-05-01

7.0%

13.7%

17.8%

1977-06-01

7.2%

14.0%

18.8%

1977-07-01

6.9%

13.3%

17.5%

1977-08-01

7.0%

13.7%

17.4%

1977-09-01

6.8%

13.5%

18.0%

1977-10-01

6.8%

13.0%

17.2%

1977-11-01

6.8%

13.1%

17.2%

1977-12-01

6.4%

12.2%

15.5%

1978-01-01

6.4%

12.9%

16.7%

1978-02-01

6.3%

13.0%

17.2%

1978-03-01

6.3%

13.0%

17.3%

1978-04-01

6.1%

12.6%

16.6%

1978-05-01

6.0%

11.8%

16.0%

1978-06-01

5.9%

11.7%

15.4%

1978-07-01

6.2%

12.5%

16.5%

1978-08-01

5.9%

11.7%

15.7%

1978-09-01

6.0%

12.1%

16.4%

1978-10-01

5.8%

11.5%

16.1%

1978-11-01

5.9%

11.9%

16.3%

1978-12-01

6.0%

12.1%

16.7%

1979-01-01

5.9%

11.6%

16.1%

1979-02-01

5.9%

11.7%

16.1%

1979-03-01

5.8%

11.6%

15.9%

1979-04-01

5.8%

11.6%

16.3%

1979-05-01

5.6%

11.6%

16.1%

1979-06-01

5.7%

11.5%

15.7%

1979-07-01

5.7%

11.6%

15.6%

1979-08-01

6.0%

12.2%

16.5%

1979-09-01

5.9%

12.1%

16.5%

1979-10-01

6.0%

12.1%

16.5%

1979-11-01

5.9%

11.6%

15.9%

1979-12-01

6.0%

12.4%

16.2%

1980-01-01

6.3%

12.6%

16.5%

1980-02-01

6.3%

12.5%

16.6%

1980-03-01

6.3%

12.3%

16.3%

1980-04-01

6.9%

13.1%

16.2%

1980-05-01

7.5%

14.7%

18.6%

1980-06-01

7.6%

14.7%

18.9%

1980-07-01

7.8%

14.9%

19.1%

1980-08-01

7.7%

14.7%

18.9%

1980-09-01

7.5%

14.3%

18.0%

1980-10-01

7.5%

14.5%

18.4%

1980-11-01

7.5%

14.4%

18.5%

1980-12-01

7.2%

13.7%

17.6%

1981-01-01

7.5%

14.5%

19.1%

1981-02-01

7.4%

14.6%

19.3%

1981-03-01

7.4%

14.5%

19.2%

1981-04-01

7.2%

14.5%

18.8%

1981-05-01

7.5%

15.1%

19.1%

1981-06-01

7.5%

14.9%

19.8%

1981-07-01

7.2%

14.1%

18.6%

1981-08-01

7.4%

14.5%

18.8%

1981-09-01

7.6%

14.9%

19.7%

1981-10-01

7.9%

15.3%

20.3%

1981-11-01

8.3%

15.9%

21.3%

1981-12-01

8.5%

16.1%

21.1%

1982-01-01

8.6%

16.5%

22.0%

1982-02-01

8.9%

17.0%

22.6%

1982-03-01

9.0%

16.9%

21.8%

1982-04-01

9.3%

17.4%

22.8%

1982-05-01

9.4%

17.3%

22.8%

1982-06-01

9.6%

17.5%

22.9%

1982-07-01

9.8%

18.0%

24.0%

1982-08-01

9.8%

18.1%

23.7%

1982-09-01

10.1%

18.2%

23.6%

1982-10-01

10.4%

18.5%

23.7%

1982-11-01

10.8%

19.0%

24.1%

1982-12-01

10.8%

18.9%

24.1%

1983-01-01

10.4%

18.5%

23.1%

1983-02-01

10.4%

18.4%

22.8%

1983-03-01

10.3%

18.2%

23.5%

1983-04-01

10.2%

18.0%

23.4%

1983-05-01

10.1%

17.7%

22.8%

1983-06-01

10.1%

17.8%

24.0%

1983-07-01

9.4%

16.8%

22.8%

1983-08-01

9.5%

17.3%

22.9%

1983-09-01

9.2%

16.4%

21.7%

1983-10-01

8.8%

16.2%

21.4%

1983-11-01

8.5%

15.4%

20.2%

1983-12-01

8.3%

14.9%

19.9%

1984-01-01

8.0%

14.8%

19.5%

1984-02-01

7.8%

14.3%

19.4%

1984-03-01

7.8%

14.4%

19.8%

1984-04-01

7.7%

14.5%

19.2%

1984-05-01

7.4%

13.6%

18.7%

1984-06-01

7.2%

13.2%

18.2%

1984-07-01

7.5%

13.7%

18.8%

1984-08-01

7.5%

14.1%

18.7%

1984-09-01

7.3%

14.0%

19.2%

1984-10-01

7.4%

13.6%

18.6%

1984-11-01

7.2%

13.2%

17.7%

1984-12-01

7.3%

13.7%

18.8%

1985-01-01

7.3%

13.6%

18.8%

1985-02-01

7.2%

13.6%

18.3%

1985-03-01

7.2%

13.6%

18.2%

1985-04-01

7.3%

13.2%

17.5%

1985-05-01

7.2%

13.6%

18.5%

1985-06-01

7.4%

13.5%

18.5%

1985-07-01

7.4%

14.2%

20.2%

1985-08-01

7.1%

13.3%

17.9%

1985-09-01

7.1%

13.3%

17.9%

1985-10-01

7.1%

14.1%

20.0%

1985-11-01

7.0%

13.5%

18.3%

1985-12-01

7.0%

13.5%

19.1%

1986-01-01

6.7%

13.0%

18.1%

1986-02-01

7.2%

13.6%

18.8%

1986-03-01

7.2%

13.2%

18.2%

1986-04-01

7.1%

13.7%

19.2%

1986-05-01

7.2%

13.7%

18.6%

1986-06-01

7.2%

13.5%

19.2%

1986-07-01

7.0%

13.3%

18.4%

1986-08-01

6.9%

13.1%

18.0%

1986-09-01

7.0%

13.6%

18.4%

1986-10-01

7.0%

13.0%

17.7%

1986-11-01

6.9%

12.8%

18.1%

1986-12-01

6.6%

13.0%

17.5%

1987-01-01

6.6%

13.0%

17.7%

1987-02-01

6.6%

13.1%

18.0%

1987-03-01

6.6%

12.8%

17.9%

1987-04-01

6.3%

12.6%

17.3%

1987-05-01

6.3%

12.5%

17.4%

1987-06-01

6.2%

12.3%

16.5%

1987-07-01

6.1%

11.8%

15.8%

1987-08-01

6.0%

11.7%

15.9%

1987-09-01

5.9%

11.8%

16.2%

1987-10-01

6.0%

11.8%

17.3%

1987-11-01

5.8%

11.5%

16.6%

1987-12-01

5.7%

11.2%

16.0%

1988-01-01

5.7%

11.5%

16.1%

1988-02-01

5.7%

11.3%

15.6%

1988-03-01

5.7%

11.8%

16.6%

1988-04-01

5.4%

11.2%

16.0%

1988-05-01

5.6%

11.3%

15.3%

1988-06-01

5.4%

10.5%

14.2%

1988-07-01

5.4%

10.8%

14.8%

1988-08-01

5.6%

11.0%

15.4%

1988-09-01

5.4%

10.8%

15.5%

1988-10-01

5.4%

10.8%

15.1%

1988-11-01

5.3%

10.5%

13.9%

1988-12-01

5.3%

10.8%

14.8%

1989-01-01

5.4%

11.8%

16.4%

1989-02-01

5.2%

10.6%

15.0%

1989-03-01

5.0%

10.1%

13.9%

1989-04-01

5.2%

10.6%

14.6%

1989-05-01

5.2%

10.4%

14.8%

1989-06-01

5.3%

11.2%

15.7%

1989-07-01

5.2%

10.6%

14.2%

1989-08-01

5.2%

10.9%

14.6%

1989-09-01

5.3%

11.1%

15.2%

1989-10-01

5.3%

11.0%

15.0%

1989-11-01

5.4%

11.3%

15.5%

1989-12-01

5.4%

11.2%

15.3%

1990-01-01

5.4%

10.8%

14.8%

1990-02-01

5.3%

10.7%

15.0%

1990-03-01

5.2%

10.6%

14.3%

1990-04-01

5.4%

11.1%

14.7%

1990-05-01

5.4%

10.8%

15.0%

1990-06-01

5.2%

10.4%

14.3%

1990-07-01

5.5%

10.7%

15.0%

1990-08-01

5.7%

11.5%

16.3%

1990-09-01

5.9%

11.7%

16.4%

1990-10-01

5.9%

11.8%

16.5%

1990-11-01

6.2%

12.0%

17.1%

1990-12-01

6.3%

12.0%

17.4%

1991-01-01

6.4%

12.6%

18.6%

1991-02-01

6.6%

12.8%

17.4%

1991-03-01

6.8%

13.1%

18.3%

1991-04-01

6.7%

12.7%

17.8%

1991-05-01

6.9%

13.6%

18.8%

1991-06-01

6.9%

13.6%

18.5%

1991-07-01

6.8%

13.8%

19.4%

1991-08-01

6.9%

13.5%

18.9%

1991-09-01

6.9%

13.4%

18.8%

1991-10-01

7.0%

13.9%

19.1%

1991-11-01

7.0%

13.8%

19.0%

1991-12-01

7.3%

14.6%

20.3%

1992-01-01

7.3%

13.9%

19.2%

1992-02-01

7.4%

14.2%

20.1%

1992-03-01

7.4%

14.1%

20.3%

1992-04-01

7.4%

13.6%

18.5%

1992-05-01

7.6%

14.4%

20.1%

1992-06-01

7.8%

15.2%

23.0%

1992-07-01

7.7%

14.5%

20.8%

1992-08-01

7.6%

14.2%

19.9%

1992-09-01

7.6%

14.5%

21.0%

1992-10-01

7.3%

13.5%

18.3%

1992-11-01

7.4%

14.3%

20.5%

1992-12-01

7.4%

14.2%

19.8%

1993-01-01

7.3%

14.0%

19.9%

1993-02-01

7.1%

14.1%

19.7%

1993-03-01

7.0%

13.6%

19.7%

1993-04-01

7.1%

13.8%

19.5%

1993-05-01

7.1%

14.2%

19.8%

1993-06-01

7.0%

13.7%

19.9%

1993-07-01

6.9%

13.1%

18.4%

1993-08-01

6.8%

13.0%

18.4%

1993-09-01

6.7%

12.6%

18.2%

1993-10-01

6.8%

13.0%

18.7%

1993-11-01

6.6%

12.9%

18.5%

1993-12-01

6.5%

12.5%

17.9%

1994-01-01

6.6%

13.4%

18.3%

1994-02-01

6.6%

12.9%

18.0%

1994-03-01

6.5%

13.1%

18.0%

1994-04-01

6.4%

13.3%

19.1%

1994-05-01

6.1%

12.5%

18.0%

1994-06-01

6.1%

12.4%

17.6%

1994-07-01

6.1%

12.4%

17.6%

1994-08-01

6.0%

12.5%

17.3%

1994-09-01

5.9%

12.1%

17.5%

1994-10-01

5.8%

12.0%

17.5%

1994-11-01

5.6%

11.4%

15.6%

1994-12-01

5.5%

11.5%

17.0%

1995-01-01

5.6%

11.4%

16.5%

1995-02-01

5.4%

11.7%

17.4%

1995-03-01

5.4%

11.6%

16.1%

1995-04-01

5.8%

12.0%

17.5%

1995-05-01

5.6%

11.9%

17.5%

1995-06-01

5.6%

12.0%

17.1%

1995-07-01

5.7%

12.5%

18.2%

1995-08-01

5.7%

12.5%

17.3%

1995-09-01

5.6%

12.7%

17.6%

1995-10-01

5.5%

12.4%

17.4%

1995-11-01

5.6%

12.0%

17.5%

1995-12-01

5.6%

12.4%

18.0%

1996-01-01

5.6%

12.8%

17.7%

1996-02-01

5.5%

12.2%

16.8%

1996-03-01

5.5%

12.2%

17.1%

1996-04-01

5.6%

12.0%

17.1%

1996-05-01

5.6%

12.2%

16.8%

1996-06-01

5.3%

11.8%

16.2%

1996-07-01

5.5%

12.4%

17.1%

1996-08-01

5.1%

11.6%

16.8%

1996-09-01

5.2%

11.4%

15.6%

1996-10-01

5.2%

11.6%

16.3%

1996-11-01

5.4%

11.9%

16.8%

1996-12-01

5.4%

11.8%

16.6%

1997-01-01

5.3%

12.2%

16.8%

1997-02-01

5.2%

11.8%

17.1%

1997-03-01

5.2%

11.7%

16.4%

1997-04-01

5.1%

11.6%

15.9%

1997-05-01

4.9%

11.1%

16.0%

1997-06-01

5.0%

11.4%

16.8%

1997-07-01

4.9%

11.2%

17.1%

1997-08-01

4.8%

11.1%

16.1%

1997-09-01

4.9%

11.2%

16.1%

1997-10-01

4.7%

11.0%

15.1%

1997-11-01

4.6%

10.8%

14.8%

1997-12-01

4.7%

10.5%

14.0%

1998-01-01

4.6%

10.9%

13.9%

1998-02-01

4.6%

10.6%

14.5%

1998-03-01

4.7%

10.5%

14.8%

1998-04-01

4.3%

9.7%

13.5%

1998-05-01

4.4%

10.3%

14.8%

1998-06-01

4.5%

10.6%

14.9%

1998-07-01

4.5%

10.6%

14.6%

1998-08-01

4.5%

10.8%

14.7%

1998-09-01

4.6%

11.0%

15.0%

1998-10-01

4.5%

10.5%

15.7%

1998-11-01

4.4%

9.8%

14.7%

1998-12-01

4.4%

9.6%

13.5%

1999-01-01

4.3%

10.2%

15.2%

1999-02-01

4.4%

10.1%

13.9%

1999-03-01

4.2%

9.9%

14.2%

1999-04-01

4.3%

10.0%

14.2%

1999-05-01

4.2%

9.6%

13.3%

1999-06-01

4.3%

10.0%

13.9%

1999-07-01

4.3%

9.9%

13.4%

1999-08-01

4.2%

9.6%

13.3%

1999-09-01

4.2%

10.2%

14.8%

1999-10-01

4.1%

10.0%

13.8%

1999-11-01

4.1%

9.9%

13.9%

1999-12-01

4.0%

9.6%

13.4%

2000-01-01

4.0%

9.4%

12.7%

2000-02-01

4.1%

9.9%

13.8%

2000-03-01

4.0%

9.6%

13.3%

2000-04-01

3.8%

9.2%

12.6%

2000-05-01

4.0%

9.8%

12.8%

2000-06-01

4.0%

9.3%

12.3%

2000-07-01

4.0%

9.3%

13.4%

2000-08-01

4.1%

9.3%

14.0%

2000-09-01

3.9%

8.9%

13.0%

2000-10-01

3.9%

8.9%

12.8%

2000-11-01

3.9%

9.1%

13.0%

2000-12-01

3.9%

9.2%

13.2%

2001-01-01

4.2%

9.6%

13.8%

2001-02-01

4.2%

9.6%

13.7%

2001-03-01

4.3%

9.8%

13.8%

2001-04-01

4.4%

10.2%

13.9%

2001-05-01

4.3%

9.9%

13.4%

2001-06-01

4.5%

10.4%

14.2%

2001-07-01

4.6%

10.2%

14.4%

2001-08-01

4.9%

11.2%

15.6%

2001-09-01

5.0%

10.8%

15.2%

2001-10-01

5.3%

11.5%

16.0%

2001-11-01

5.5%

11.6%

15.9%

2001-12-01

5.7%

12.2%

17.0%

2002-01-01

5.7%

12.1%

16.5%

2002-02-01

5.7%

11.8%

16.0%

2002-03-01

5.7%

12.5%

16.6%

2002-04-01

5.9%

12.3%

16.7%

2002-05-01

5.8%

11.6%

16.6%

2002-06-01

5.8%

11.8%

16.7%

2002-07-01

5.8%

12.1%

16.8%

2002-08-01

5.7%

12.0%

17.0%

2002-09-01

5.7%

11.7%

16.3%

2002-10-01

5.7%

11.8%

15.1%

2002-11-01

5.9%

12.1%

17.1%

2002-12-01

6.0%

12.1%

16.9%

2003-01-01

5.8%

12.0%

17.2%

2003-02-01

5.9%

12.1%

17.2%

2003-03-01

5.9%

12.0%

17.8%

2003-04-01

6.0%

12.6%

17.7%

2003-05-01

6.1%

12.9%

17.9%

2003-06-01

6.3%

13.2%

19.0%

2003-07-01

6.2%

13.0%

18.2%

2003-08-01

6.1%

12.3%

16.6%

2003-09-01

6.1%

12.8%

17.6%

2003-10-01

6.0%

12.2%

17.2%

2003-11-01

5.8%

12.1%

15.7%

2003-12-01

5.7%

11.7%

16.2%

2004-01-01

5.7%

12.0%

17.0%

2004-02-01

5.6%

11.7%

16.5%

2004-03-01

5.8%

12.0%

16.8%

2004-04-01

5.6%

11.6%

16.6%

2004-05-01

5.6%

12.1%

17.1%

2004-06-01

5.6%

12.0%

17.0%

2004-07-01

5.5%

12.1%

17.8%

2004-08-01

5.4%

11.5%

16.7%

2004-09-01

5.4%

11.7%

16.6%

2004-10-01

5.5%

12.1%

17.4%

2004-11-01

5.4%

11.5%

16.4%

2004-12-01

5.4%

11.7%

17.6%

2005-01-01

5.3%

11.6%

16.2%

2005-02-01

5.4%

12.4%

17.5%

2005-03-01

5.2%

11.8%

17.1%

2005-04-01

5.2%

11.8%

17.8%

2005-05-01

5.1%

11.7%

17.8%

2005-06-01

5.0%

11.1%

16.3%

2005-07-01

5.0%

10.7%

16.1%

2005-08-01

4.9%

11.1%

16.1%

2005-09-01

5.0%

10.8%

15.5%

2005-10-01

5.0%

10.8%

16.1%

2005-11-01

5.0%

11.1%

17.0%

2005-12-01

4.9%

10.5%

14.9%

2006-01-01

4.7%

10.4%

15.1%

2006-02-01

4.8%

10.8%

15.3%

2006-03-01

4.7%

10.5%

16.1%

2006-04-01

4.7%

10.3%

14.6%

2006-05-01

4.6%

10.0%

14.0%

2006-06-01

4.6%

10.4%

15.8%

2006-07-01

4.7%

10.9%

15.9%

2006-08-01

4.7%

10.7%

16.0%

2006-09-01

4.5%

10.6%

16.3%

2006-10-01

4.4%

10.6%

15.2%

2006-11-01

4.5%

10.6%

14.8%

2006-12-01

4.4%

10.0%

14.6%

2007-01-01

4.6%

10.3%

14.8%

2007-02-01

4.5%

9.9%

14.9%

2007-03-01

4.4%

10.0%

14.9%

2007-04-01

4.5%

10.3%

15.9%

2007-05-01

4.4%

9.9%

15.9%

2007-06-01

4.6%

10.6%

16.3%

2007-07-01

4.7%

10.5%

15.3%

2007-08-01

4.6%

10.7%

15.9%

2007-09-01

4.7%

11.2%

15.9%

2007-10-01

4.7%

10.7%

15.4%

2007-11-01

4.7%

10.8%

16.2%

2007-12-01

5.0%

11.7%

16.8%

2008-01-01

5.0%

11.7%

17.8%

2008-02-01

4.9%

11.4%

16.6%

2008-03-01

5.1%

11.4%

16.1%

2008-04-01

5.0%

11.0%

15.9%

2008-05-01

5.4%

13.0%

19.0%

2008-06-01

5.6%

12.9%

19.2%

2008-07-01

5.8%

13.5%

20.7%

2008-08-01

6.1%

13.1%

18.6%

2008-09-01

6.1%

13.5%

19.1%

2008-10-01

6.5%

13.6%

20.0%

2008-11-01

6.8%

14.0%

20.3%

2008-12-01

7.3%

14.8%

20.5%

2009-01-01

7.8%

15.0%

20.7%

2009-02-01

8.3%

16.0%

22.3%

2009-03-01

8.7%

16.5%

22.2%

2009-04-01

9.0%

16.7%

22.2%

2009-05-01

9.4%

17.6%

23.4%

2009-06-01

9.5%

18.0%

24.7%

2009-07-01

9.5%

17.9%

24.3%

2009-08-01

9.6%

18.1%

25.0%

2009-09-01

9.8%

18.4%

25.9%

2009-10-01

10.0%

19.1%

27.2%

2009-11-01

9.9%

19.2%

26.9%

2009-12-01

9.9%

18.8%

26.7%

2010-01-01

9.8%

18.8%

26.1%

2010-02-01

9.8%

18.7%

25.6%

2010-03-01

9.9%

18.8%

26.2%

2010-04-01

9.9%

19.5%

25.4%

2010-05-01

9.6%

18.1%

26.5%

2010-06-01

9.4%

18.2%

25.9%

2010-07-01

9.4%

18.4%

25.9%

2010-08-01

9.5%

17.7%

25.5%

2010-09-01

9.5%

17.9%

25.8%

2010-10-01

9.4%

18.7%

27.2%

2010-11-01

9.8%

18.5%

24.8%

2010-12-01

9.3%

17.9%

25.3%

2011-01-01

9.2%

18.1%

25.7%

2011-02-01

9.0%

17.7%

24.1%

2011-03-01

9.0%

17.6%

24.4%

2011-04-01

9.1%

17.6%

24.6%

2011-05-01

9.0%

17.3%

23.9%

2011-06-01

9.1%

17.1%

24.6%

2011-07-11

9.0%

17.3%

24.7%

2011-08-20

9.0%

17.4%

25.0%

2011-09-01

9.0%

17.3%

24.4%

2011-10-11

8.8%

16.7%

24.2%

2011-11-20

8.6%

17.1%

24.2%

2011-12-30

8.5%

16.7%

23.3%

2012-01-12

8.3%

16.1%

23.7%

2012-02-12

8.3%

16.5%

23.8%

2012-03-12

8.2%

16.3%

25.0%

2012-04-12

8.2%

16.5%

24.8%

2012-05-12

8.2%

16.1%

24.3%

2012-06-12

8.2%

16.3%

23.4%

2012-07-12

8.2%

16.3%

23.6%

2012-08-12

8.0%

16.7%

24.3%

2012-09-12

7.8%

15.4%

23.7%

2012-10-12

7.8%

16.1%

23.9%

2012-11-12

7.7%

15.9%

24.0%

2012-12-12

7.9%

16.6%

24.1%

2013-01-12

8.0%

16.8%

23.9%

2013-02-12

7.7%

16.2%

25.2%

2013-03-12

7.5%

16.1%

24.1%

2013-04-12

7.6%

16.1%

24.1%

2013-05-12

7.5%

16.2%

24.2%

2013-06-12

7.5%

16.1%

23.3%

2013-07-12

7.3%

15.5%

23.2%

2013-08-12

7.2%

15.5%

22.5%

2013-09-12

7.2%

15.0%

21.1%

2013-10-12

7.2%

15.0%

22.2%

2013-11-12

7.0%

14.2%

20.9%

2013-12-12

6.7%

13.5%

20.4%

2014-01-12

6.6%

14.3%

20.8%

2014-02-12

6.7%

14.3%

21.3%

2014-03-12

6.6%

14.5%

20.9%

2014-04-12

6.2%

12.8%

19.1%

2014-05-12

6.3%

13.2%

19.2%

2014-06-12

6.1%

13.3%

20.7%

2014-07-12

6.2%

13.6%

20.0%

2014-08-12

6.1%

13.0%

19.4%

2014-09-12

5.9%

13.7%

19.8%

2014-10-12

5.7%

12.7%

18.7%

2014-11-12

5.8%

12.7%

17.5%

2014-12-12

5.6%

12.4%

16.8%

2015-01-12

5.7%

12.2%

18.8%

2015-02-12

5.5%

11.9%

17.1%

2015-03-12

5.5%

12.3%

17.5%

2015-04-12

5.4%

11.6%

17.1%

New Research Does Not Provide Any Reason to Doubt that CEO Pay Fueled Top 1% Income Growth

A new paper, Firming up Inequality, has been receiving substantial attention in the media for its claim that wage inequality is not occurring within firms but only occurs between firms. The authors claim that their results disprove the claim made by me and others, such as Thomas Piketty and Emmanuel Saez, that the growth of top 1 percent incomes was driven by the pay of executives and those in the financial sector. Though the authors present valuable new data, which offers the possibility of great insights, their current analysis does not disprove that executive pay has fueled top 1 percent income growth. In fact, the study neither examines nor rebuts claims about executive pay.

The authors also offer a “we live in the best possible world” interpretation of their findings—inequality is due to high productivity growth of “superfirms.” This is pure speculation and is completely disconnected from their actual empirical work. A similar study examined productivity trends and contradicts their narrative about superfirms.

Last, there are reasons to be skeptical of their findings because they imply huge wage disparities have opened up between median workers across firms within an industry that are implausible.

1. The paper neither examines nor rebuts the claim that executive pay was a major factor in the doubling of the income share of the top 1 percent.

The paper characterizes itself as a critique of the findings that executive pay (and financial sector pay) has fueled the growth of top 1 percent incomes, citing my work with Natalie Sabadish, as well as Piketty’s:

In the absence of comprehensive evidence on wages paid by firms, it is frequently asserted that inequality within the firm is a driving force leading to an increase in overall inequality. For example, according to Mishel and Sabadish (2014), “a key driver of wage inequality is the growth of chief executive officer earnings and compensation.” Piketty (2013) (p. 315) agrees, noting that “the primary reason for increased income inequality in recent decades is the rise of the supermanager.”

Strong Wage Growth Would Complement the Safety Net in Reducing Poverty

Last week, we published Broad-Based Wage Growth Is a Key Tool in the Fight Against Poverty, which argued that our fight against poverty over the last few decades has been missing a key element: strong wage growth for the majority of workers. To substantiate this claim, we simulated the impacts on poverty rates in a few scenarios in which wages grew across the board according to different benchmarks (e.g., average wage growth, productivity, and productivity and full employment).

Judging by a recent blog post, Matt Bruenig seems unimpressed. He spends a large part of the first part of his post suggesting that efforts to boost market incomes (i.e., wages) will necessarily fall short because the majority of those who are in poverty (namely, the elderly, children, the disabled, and caregivers) do not work. He ends by assessing the result of our simulation as uninspiring largely because the “employable” poor make up only a minority of those in poverty. Given the alleged ineffectiveness of wage-growth, he calls for increased transfers to fight poverty.

We think Bruenig overlooks two key aspects of the role of wages in reducing overall poverty. First, we believe he ignores the extent to which children would benefit from the spillover of increased wages for their parents. Second, he ignores the fact that people move in and out of poverty—by raising the income floor for many families, broad-based wage growth plays an important role in preventing more of them from falling under the poverty line.