On Substance, Martin O’Malley Was Right About American Wages: Don’t Let Nitpicks Convince You That There Is Not A Crisis in American Pay

Three separate sources have recently “fact-checked” claims that Martin O’Malley made about American wages in his recent speech announcing his candidacy for the Democratic nomination. The precise O’Malley quote was:

Today in America, 70 percent of us are earning the same or less than we were 12 years ago, and this is the first time that that has happened this side of World War II.

O’Malley has said that our research on wages provided a basis for his claim (examples can be found here and here).

First, let’s be clear on what our claim is and then I’ll talk about the fact checkers’ assessments of O’Malley’s use of the data.

We have data on hourly wages by decile since 1973. Between 2002 and 2014, inflation-adjusted hourly wages for the bottom 7 deciles (i.e., 70 percent of the American workforce) fell. This is a remarkable economic fact and one that O’Malley is clearly right to highlight.

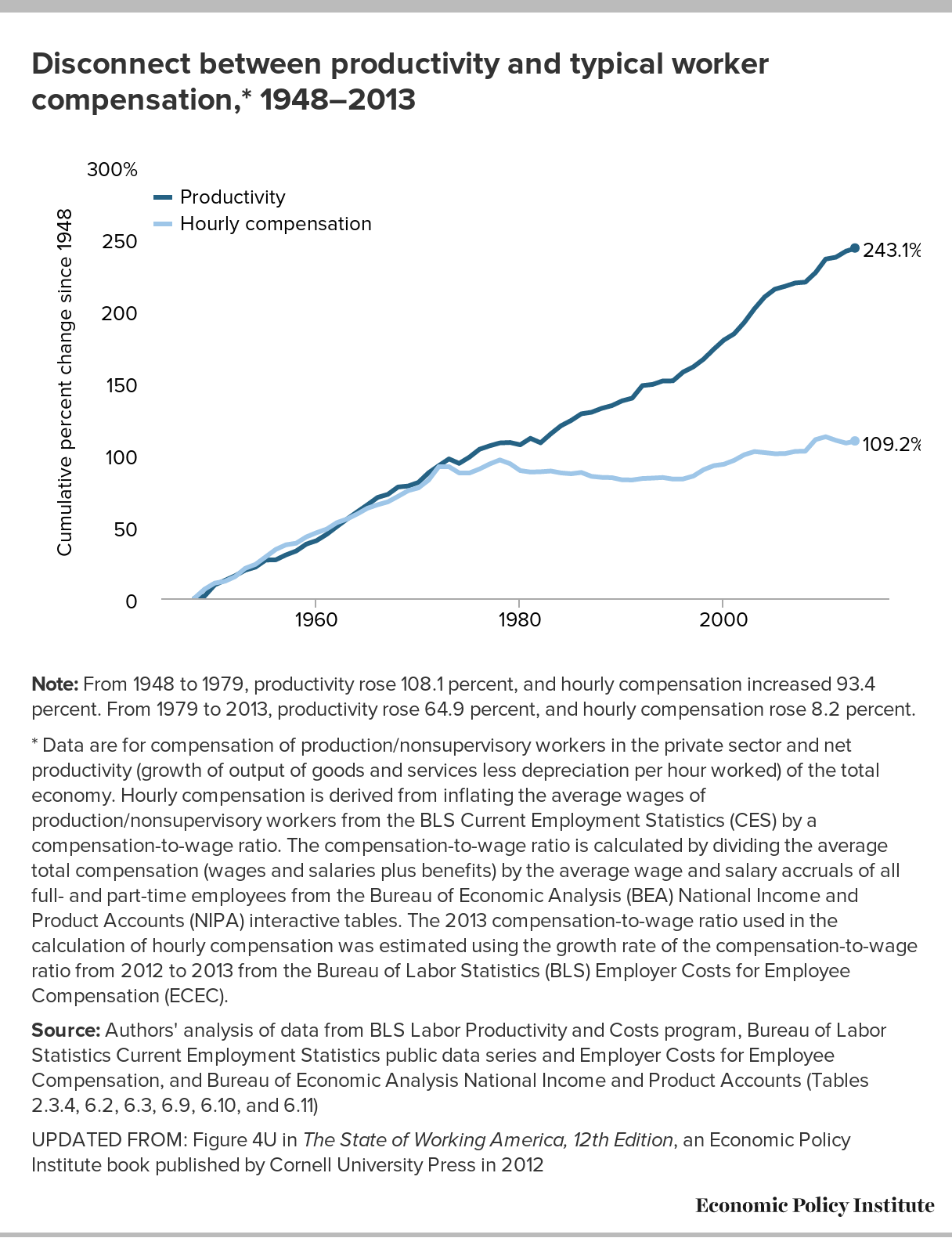

Further, between 1947 and 1973 there is almost certainly no 12-year period when the bottom 70 percent of wage earners saw hourly wage declines. Precise wage data by decile is sketchy over this period, but the circumstantial evidence on this is overwhelming. Just look at this graph, which shows hourly pay for a grouping reflecting the bottom 80 percent of the workforce rising sharply until the early 1970s.

{kind=link}

So, the general thrust of O’Malley’s remarks—that wage growth for the bottom 70 percent of American workers has been dismal in recent decades and has actually been outright negative for the most recent 12 years—is clearly correct.

But some fact checkers have dinged him on some specifics. One of these criticisms is technically true, but ironically just bolsters O’Malley’s contentions about economic policy choices. Others just seem strangely nitpicky.

First, the true one. Both the Washington Post fact checker and Politifact ding O’Malley for saying this is the only time this has happened (the bottom 70 percent of wages falling over a 12-year period) since World War II—claiming instead that there have been some other 12-year periods when the bottom 70 percent experienced wage declines over this post-1973 period (1973-1985 and 1979-1991).

This is true—the 1980s and early 1990s were a wage disaster for American workers. So technically, O’Malley can be properly chastised for not remembering just how bad the American economy was for most workers during the Reagan and George H.W. Bush administrations. However, this only seems to strengthen his larger point. Policies favored by many in the GOP then and now—putting pressure on the Federal Reserve to push down inflation at the expense of pushing up unemployment, tax cuts for high-income households, deregulation, erosion of the minimum wage, and assaults of workers’ rights to bargain collectively—have had the entirely predictable effect of suppressing wages for the vast majority, and this claim is largely validated by the wage growth in these earlier periods.

Now, on to some less compelling criticisms. The Washington Post fact checker says that “The percentile data [from EPI] do not reflect individual Americans’ wages, and instead shows the distribution of wages.” That’s flat wrong. Our data absolutely reflect individuals’ wages. What she means is that it’s not a panel dataset—it doesn’t follow the same individuals over time. Instead it is a repeated cross-section of American workers. This means that if O’Malley had said “the bottom 70 percent of American workers make less than 12 years ago” it would have been perfectly accurate. By saying instead that 70 percent “of us” saw wage declines, O’Malley opens the issue of individual workers getting older and potentially making more money as they get promotions and gain experience throughout their career.

Looking at individual workers’ wages over time to rebut a story about economy-wide wage stagnation artificially raises the bar. After all, people do tend to see their wages rise as they accumulate skills and experience, earning more in their thirties than in their twenties, more in their forties than in their thirties, and so on. This is called the age-earnings profile. Wage stagnation for the large majority of Americans (let’s focus on workers lacking a four-year college degree, for example) has manifested itself in lower (or stagnant) wages for new workers as they enter the labor market—earning less in their twenties than an earlier cohort – and seeing smaller wage growth (or flatter age-earnings profiles) as they age.

The result is that wages for workers in their forties, for instance, are rising more slowly relative to earlier periods, and the gap between the wages of workers in their forties today relative to forty-something workers in decades past is much smaller than it would have been if overall wage growth had been broad based, rather than concentrated at the very top. So, in age-earnings profile terms, broad-based wage stagnation manifests itself as these profiles starting lower (or being stagnant) and flattening over time. The simple fact that someone who is forty years old earns more today than she did in her twenties is not a sign of a healthy economy or acceptable economy-wide wage performance. It does mean that many individual workers don’t experience actual wage declines or stagnation even if the working class as a whole does. The labor force as a whole does not have a significant age-earnings profile because younger workers constantly filter in and replace retiring older workers.1

Further, O’Malley’s analysis of wages by percentile is much more relevant to the question he’s speaking about: rising inequality. We could have wages rising over any specific workers’ lifetimes with overall wages not rising at all in the economy, as was just explained. But so long as wages for the bottom 70 percent of American workers fail to rise, this leads to a divergence between typical workers’ pay and productivity growth, which in turn leads to a sharp rise in economic inequality. And this is exactly what has happened to the U.S. economy in recent decades.

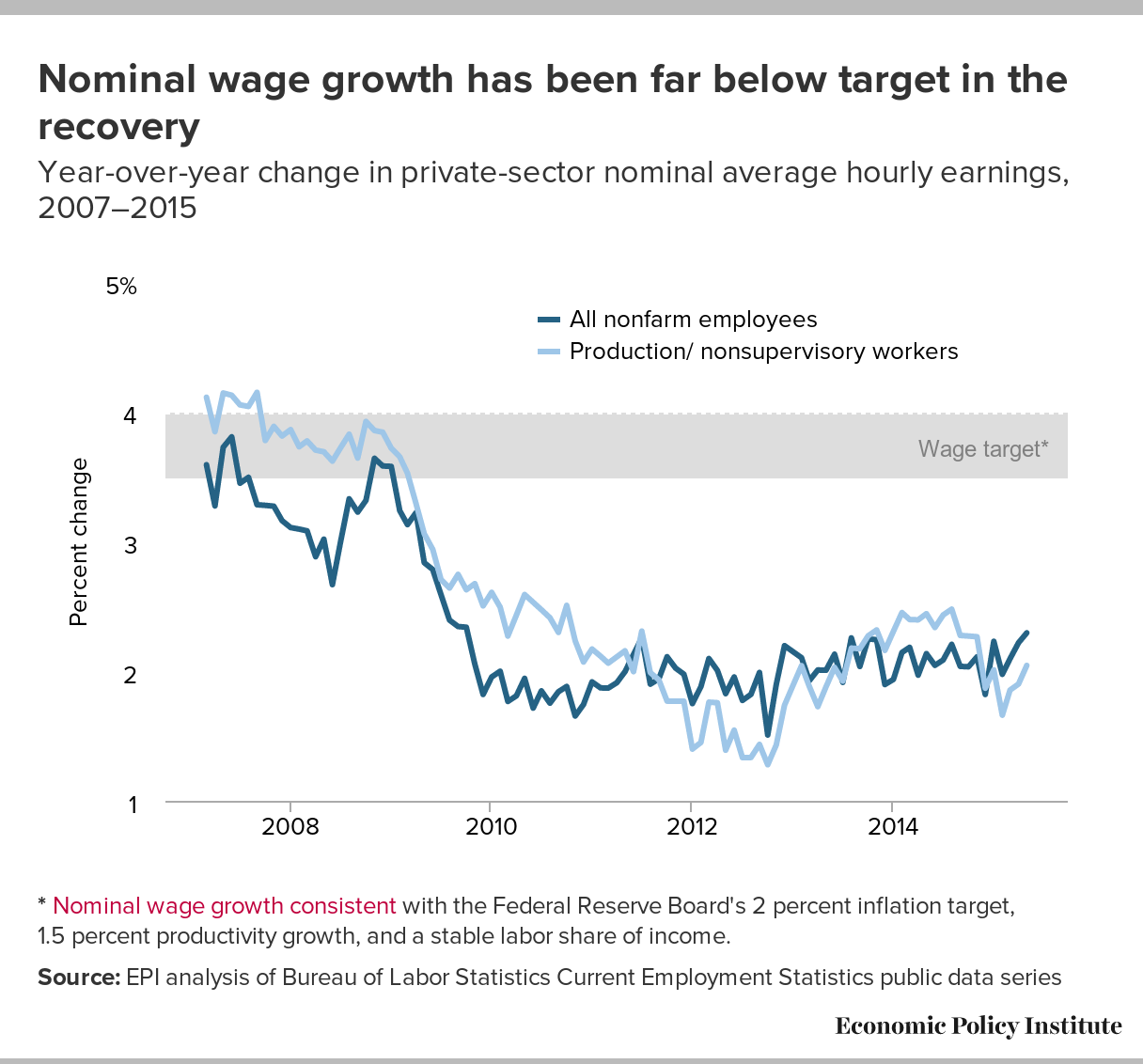

Meanwhile, Brooks Jackson at FactCheck dings O’Malley for not using volatile monthly data that reflects the clearly temporary fall in energy oil price inflation over the past year, when oil-price induced deflation lifted inflation-adjusted wages enough by April 2015 to make them about 6.2 percent higher than they were in 2003. However, April 2003 was tied for the highest unemployment rate that we had seen in nearly a decade at that point, and had seen year-over-year energy prices rise by 12.3 percent, rather than fall by 18.9 percent, as occurred in April 2015. Simply put, very few economists would argue that using month-by-month data to make strong points on wage trends is analytically correct. Inflation is volatile and short-term movements can lead to artificial spikes up or down in inflation-adjusted wages. We know that wage growth, without any inflation adjustment, has been consistently low over the last five years, growing at roughly two percent or a bit above. We will never see shared prosperity with that type of wage growth.

{kind=link}

All-in-all, the judgement of the fact checkers on the overall truth of O’Malley’s claims are awfully nitpicky. O’Malley is claiming that policies embraced by many in the GOP are bad for wage growth, and he cites a correct statistic that wages for the bottom 70 percent of American workers have been stagnant or worse for a dozen years. That’s also important for demonstrating that wage stagnation occurred in the last recovery (2001-2007) as well as in the current recovery, and is not simply a Great Recession phenomenon .

Did O’Malley wordsmith it perfectly from our perspective? No, but EPI isn’t running a campaign. We would note the broad-based wage stagnation of the past 12 years but also note the longer-term stagnation (other than the exception of the late 1990s and the spillover into 2000-02). But there’s nothing misleading about O’Malley’s claims—it has indeed been a terrible 12-year period for wage growth for the vast majority of American workers, and this poor wage growth is a clear root cause of rising inequality.

1. In fact, the terrible performance of American wages that O’Malley references is likely even buoyed a bit by the general aging of the workforce in the aggregate. All else equal, a workforce that is older and better-educated on average should see higher wages. Yet rising age and educational attainment of typical American workers has not been enough to boost wages for the bottom 70 percent.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.