Household income growth slowed markedly in 2017 and was stronger for those at the top, while earnings declined slightly

Today’s report from the Census Bureau shows a marked slowdown in median household income growth relative to previous years. Median household incomes rose 1.8 percent, after an impressive 5.1 percent gain in 2015 and a 3.1 percent gain in 2016; median non-elderly household income saw a similar rise of 2.5 percent this year after gaining 4.6 percent and 3.6 percent in the prior two years, respectively. However, inflation-adjusted full-time annual earnings for both men and women fell by 1.1 percent in 2017. Men’s earnings are still below their 2007 level (by 2.5 percent points), while women’s earnings are now 0.9 percent above. This year’s report is hence a bit discouraging; earnings for low and middle-income workers need to make strong and sustained gains if we are to have an economy that works for typical American households and not just for the well-off.

While the gains in household income are markedly slower than in previous years, they nonetheless represent another small step toward reclaiming the lost decade of income growth caused by the Great Recession. Part of this year’s slowdown in income growth relative to 2016 is likely driven by a small increase in the pace of inflation. In 2017, year-over-year inflation was 2.2 percent compared to 1.3 percent in 2016. However, as discussed below, this year’s report reminds us that the vast majority of household incomes (when corrected for a break in the data series in 2013) have still not fully recovered from the deep losses suffered in the Great Recession.

Non-elderly household incomes improve

The Census data show that from 2016–2017, inflation-adjusted median household incomes for non-elderly households (those with a head of household younger than 65 years old) increased 2.5 percent, from $67,917 to $69,628. Median non-elderly household income is an important measure of an improving economy, as those households depend on labor market income for the vast majority of their income. This continued, albeit slower, increase after large gains in the prior two years is a welcome trend. Median household income for non-elderly households, which finally recovered to its pre-recession level in 2017, was 0.8 percent, or $530, above its level in 2007. It’s important to note that the Great Recession and its aftermath came on the heels of a weak labor market from 2000–2007, during which the median income of non-elderly households fell significantly, from $71,577 to $69,098—the first time in the post-war period that incomes failed to grow over a business cycle. Altogether, from 2000–2017, the median income for non-elderly households fell from $71,577 to $69,628, a decline of $1,949, or 2.7 percent. In short, the last three years should not make us forget that incomes for the majority of Americans have experienced a lost 17 years of growth.Read more

By the Numbers: Income and Poverty, 2017

Jump to statistics on:

• Earnings

• Incomes

• Poverty

• Policy / SPM

This fact sheet provides key numbers from today’s new Census reports, Income and Poverty in the United States: 2017 and The Supplemental Poverty Measure: 2017. Each section has headline statistics from the reports for 2017, as well as comparisons to the previous year, to 2007 (the final year of the economic expansion that preceded the Great Recession), and to 2000 (the historical high point for many of the statistics in these reports.) All dollar values are adjusted for inflation (2017 dollars).

Earnings

Median annual earnings for men working full time fell 1.1 percent, to $52,146, in 2017. Men’s earnings are down 2.5 percent since 2007, and are still 1.9 percent lower than they were in 2000.

Median annual earnings for women working full time fell 1.1 percent, to $41,977, in 2017. Women’s earnings are up 0.9 percent since 2007, and are 7.1 percent higher than they were in 2000.

Median annual earnings for men working full time in 2017: $52,146

Change over time:

- 2016–2017: -1.1%

- 2007–2017: -2.5%

- 2000–2017: -1.9%

Median annual earnings for women working full time in 2017: $41,977

Change over time:

- 2016–2017: -1.1%

- 2007–2017: 0.9%

- 2000–2017: 7.1%

What to watch for in the 2017 Census data on earnings, incomes, and poverty

Next Wednesday is the Census Bureau’s release of annual data on earnings, income, poverty, and health insurance coverage for 2017, which will give us a picture of the economic status of working families 10 years since the start of the Great Recession—and in the first year of the Trump presidency. Next week’s release will help us chart the progress made by the typical American household in clawing back nearly two decades of lost income growth—the result of a failure of incomes to return to the business cycle peaks of 2000 during the slow early-2000s recovery and expansion, and the Great Recession. We’ll be paying particular attention to differences in the recovery across racial and ethnic groups.

What happened with incomes in 2016?

After adjusting the series to account for changes to the survey in 2013, 2016 median incomes for American households fell just shy of their pre-Great Recession peaks, even after two years of impressive across-the-board improvements (as shown in the figure below). It is important to note, however, that some of the improvements in inflation-adjusted income we saw in 2015 and 2016 were driven by atypically low inflation—0.1 percent in 2015, and 1.3 percent in 2016. While we don’t expect a similar boost from low inflation in 2017 (inflation increased 2.2 percent in 2017), we anticipate that an additional year of even modest growth will likely bring the broad middle class back to pre-recession incomes. But, for non-elderly households, the latest data will be likely still below the peak reached 17 years prior.

Real median household income, all and non-elderly, 1995–2016

| All households | All households- imputed series | All households- new series | Non-elderly households | Non-elderly households- imputed series | Non-elderly households- new series | |

|---|---|---|---|---|---|---|

| 1995 | $53,330 | $55,020 | $61,268 | $63,173 | ||

| 1996 | $54,094 | $55,808 | $62,399 | $64,338 | ||

| 1997 | $55,207 | $56,956 | $63,203 | $65,168 | ||

| 1998 | $57,223 | $59,036 | $65,775 | $67,820 | ||

| 1999 | $58,647 | $60,506 | $67,451 | $69,548 | ||

| 2000 | $58,525 | $60,380 | $67,783 | $69,890 | ||

| 2001 | $57,248 | $59,062 | $66,737 | $68,811 | ||

| 2002 | $56,591 | $58,384 | $66,066 | $68,120 | ||

| 2003 | $56,522 | $58,313 | $65,464 | $67,499 | ||

| 2004 | $56,333 | $58,118 | $64,705 | $66,717 | ||

| 2005 | $56,947 | $58,752 | $64,275 | $66,273 | ||

| 2006 | $57,390 | $59,208 | $65,159 | $67,184 | ||

| 2007 | $58,150 | $59,993 | $65,457 | $67,492 | ||

| 2008 | $56,079 | $57,856 | $63,311 | $65,280 | ||

| 2009 | $55,689 | $57,454 | $62,451 | $64,392 | ||

| 2010 | $54,242 | $55,961 | $60,847 | $62,738 | ||

| 2011 | $53,413 | $55,106 | $59,374 | $61,220 | ||

| 2012 | $53,335 | $55,025 | $59,959 | $61,823 | ||

| 2013 | $53,513 | $55,209 | $55,209 | $60,220 | $62,092 | $62,092 |

| 2014 | $54,404 | $61,304 | ||||

| 2015 | $57,231 | $64,146 | ||||

| 2016 | $59,039 | $66,487 | ||||

Note: Because of a redesign in the CPS ASEC income questions in 2013, we imputed the historical series using the ratio of the old and new method in 2013. Solid lines are actual CPS ASEC data; dashed lines denote historical values imputed by applying the new methodology to past income trends. Non-elderly households are those in which the head of household is younger than age 65. Shaded areas denote recessions.

Source: EPI analysis of Current Population Survey Annual Social and Economic Supplement Historical Income Tables (Tables H-5 and HINC-02)

What do we expect in this year’s release?

Given the data we’ve seen for 2017 from other sources, it is likely that earnings, income, and poverty in the 2017 Census data will show some improvement over the past year. But it is also likely that this pace of improvement will be significantly slower than the previous two years’ growth. As the economy steadily strengthens, we’ve seen progress in key labor market indicators, including participation in the labor market and payroll employment, which should boost household labor earnings. However, hourly wage data suggest that wage growth in 2017 continues to be unequal and slower than expected at this point in the business cycle. In 2017, strong growth in hourly wages continued at the top (1.5 percent at the 95th percentile), while the 10th percentile saw the strongest growth at 3.7 percent due in part to a tightening labor market as well as state-level minimum wage increases. However, median wages grew only 0.2 percent.Read more

What to Watch on Jobs Day: Keeping a cautiously optimistic eye on wages

Nominal wage growth has been slower than would be expected over the last year, particularly in light of an unemployment rate hovering around 4.0 percent. In a tight labor market, employers should be finding it harder and harder to attract and retain the workers they want—and, therefore they should be raising wages in order to get them. But, that’s not happening enough to move the dial on wage growth. In this preview post for jobs day, I’m going to review some reasons that do NOT explain slower wage growth, then discuss some far more compelling explanations.

In the last several weeks, some colleagues and I tried to dispel a few myths about why wages aren’t rising as fast as would be expected in this labor market. One reason wage growth could be slow is if lower wage jobs are being added at a disproportionate rate, but the composition of new jobs is not what is keeping wage growth so sluggish right now. Instead, we are simply seeing sluggish wage growth within a wide variety of job-types. Some have posited that our far-less-than-stellar wage growth right now could be due to workers not having the skills employers need. But that idea has the logic backwards. When employers can’t find workers with the skills they need at the wages they are offering, they will raise wages in order to attract qualified workers—if employers can’t find the workers they need among the unemployed, they will offer higher wages in an attempt to poach needed workers from other firms, who will then raise wages in an attempt to keep their workers, and so on. In other words, if there are skills shortages, we should see signs of faster wage growth for workers with needed skills. This fast wage growth for skilled workers should push up average wages, not weigh them down. Furthermore, if there was a credential shortage, we’d expect faster wage growth among those with more credentials, which has also not been happening in the past couple of years.

So, then what is it? One reason why employers may not feel compelled as of yet to raise wages is that the unemployment rate is overstating the strength of the labor market. There are still sidelined workers—not counted in the unemployment rate—who are returning to the labor market month after month in search of, and, in many cases, finding jobs. The simple fact of these would-be workers out there lowers the leverage today’s workers have to see faster wage growth from their employers.

Separate is still unequal: How patterns of occupational segregation impact pay for black women

August 7th is Black Women’s Equal Pay Day, the day that marks how long into 2018 an African American woman would have to work in order to be paid the same wages her white male counterpart was paid last year. On average, in 2017, black women workers were paid only 66 cents on the dollar relative to non-Hispanic white men, even after controlling for education, years of experience, and geographic location. A previous blog post dispels many of the myths behind why this pay gap exists, including the idea that the gap would be closed by black women getting more education or choosing higher paying jobs. In fact, black women earn less than white men at every level of education and even when they work in the same occupation. But even if changing jobs were an effective way to close the pay gap black women face—and it isn’t—more than half would need to change jobs in order to achieve occupational equity.

Figure A plots the “Duncan Segregation Index” (DSI) for black women and white men, overall and by education, based on individual occupation data from the American Community Survey (ACS). This is a common measure of occupational segregation, which, in this case identifies what percentage of working black women (or white men) would need to change jobs in order for black women and white men to be fully integrated across occupations. Values of the DSI can range from 0 percent (complete integration) to 100 percent (complete segregation).

As shown in Figure A, there has been little progress on reducing occupational segregation between black women and white men since 2000. From 2000 to 2016 (latest data year available), the DSI only changed from 59 percent to 56 percent. This means that on average, 56 percent of black women (or white men) would need to change occupations in order to achieve occupational equity, or full integration of these two groups in the workforce.

How do we know the tax cut isn’t working to boost wages? Investment, investment, investment

Earlier this week, my colleague Hunter Blair noted that economic data released over the past six months contained no real signs that any of the promised benefits of the Republican tax cut passed at the end of last year were showing up for workers. These benefits are certainly showing up for corporations and the wealthy households that own them—which makes sense, as the tax cut was overwhelmingly a tax cut for corporations. But the tax cut’s boosters promised that money corporations saved on taxes would quickly show up as higher wages for workers. In fact, they claimed this was happening so quickly that the tax cut was responsible for bonuses at the end of 2017 that were granted or announced before the tax cut actually became law.

As silly as those arguments were, a case that corporate tax cuts will lead to wage increases does exist in economics textbooks. The most crucial link in the chain leading from cutting corporations’ taxes to workers seeing higher paychecks runs through increased business investment in plants, equipment, and research. Essentially, lower corporate taxes are supposed to incentivize businesses to undertake more investment in productivity-enhancing plants, equipment, and research, and induce extra spending to finance these increased investments. This extra investment is supposed to lead to higher productivity, and hence to higher wages for workers. I should note that most of the links in this chain are broken, but for now, let’s just focus on the first—the effect of the tax cut in spurring business investment. If that fails, the whole case for tax cuts boosting wages fails.

The figure below shows the percent change in business investment relative to the same quarter in the previous year, with the vertical line showing when the tax cut was passed. The data is from the Bureau of Economic Analysis (BEA), National Income and Product Accounts (NIPA) Table 1.1.3. It is awfully hard to see a real regime change here in investment behavior.

What to Watch on Jobs Day: Wringing out every last bit of slack in the labor market

Two weeks ago, EPI released a paper by Estelle Sommeiller and Mark Price detailing, county-by-county, the rise in income inequality since the 1970s. Since the Great Recession, the top 1 percent of families have captured 41.8 percent of all income growth in the United States—and this disproportionate hoarding of economic growth is not unique to East Coast metropolises and Silicon Valley. All across the country, downward pressure on wages and incomes for most Americans has limited their ability to benefit from a growing economic pie. A decline in unionization and other deliberate policy choices that have reduced typical workers’ leverage and bargaining power in the labor market have contributed to these worrying trends.

Nonetheless, some experts still question why today’s relatively tighter economy isn’t bringing benefits to workers in the form of increased wages, given that we’ve seen relatively low unemployment rates over the course of the past two years—below 4.5 percent unemployment since March of last year. Josh Bivens reiterated this week EPI’s consistent stance that, “weak wage growth should make us think that by definition there is still slack in the labor market, and this might mean rethinking just how low unemployment can go.” Given this reality, policymakers (including the Fed) should stop attempting to slow the economy and allow the labor market to keep tightening, until there is consistent evidence that the benefits of a strong economy are being shared with a wide swath of the workforce. This includes many women of color who face pay gaps so large that they typically would need to work through the third or fourth quarter of another year just to earn as much as the average white man earned during the previous year. For black women, that date is next Tuesday, August 7.

In last month’s jobs report, we saw the unemployment rate tick up from 3.8 to 4.0, for positive reasons. The rise was accompanied by an increase in labor force entrants, suggesting workers are feeling optimistic about the jobs market and sidelined workers are indeed still being drawn back into the labor force. Looking at today’s prime-age employment-to-population ratio, which is still below the peaks of the last two business cycles, this is less surprising. As it has for most of the past several years, the low unemployment rate looks to be potentially overstating the strength of the labor market.

Tomorrow morning, we will continue to look at the unemployment rate, given its recent volatility, but we will also be watching nominal wage growth and the prime-age employment-to-population ratio for evidence that the economy continues to move closer to full employment.

The “wage puzzle” is real—but low inflation and low productivity are also puzzles that need to be solved

Jason Furman’s recent piece in Vox is drawing lots of comments (including one by me on a relatively minor issue). The last couple of months have seen lots of attention focused on relatively weak wage growth even in the face of low unemployment—sometimes referred to as the “wage puzzle.” I and others have argued that this weak wage growth should make us think that by definition there is still slack in the labor market, and this might mean rethinking just how low unemployment can go. Furman argues instead that wage growth is not that low, and that labor markets are tight indeed. A main piece of evidence he highlights to support this view is that both inflation and productivity growth have been low in recent years, and, adjusted for these two influences we really can’t expect wage growth to be any higher than it has been.

Furman is quick to note that his outlook does not demand rapid policy tightening to rein in growth. I’m definitely happy he says this. However, I do think any argument that concludes that the U.S. economy is unambiguously at full employment, and that the labor market is even tighter than the late 1990s, is going to give succor to those calling for the Federal Reserve to continue raising interest rates briskly to rein in growth.

This would be a mistake, and Furman’s arguments should certainly not sway anybody to call for continued policy tightening. He makes some good points, but I think he misreads what low inflation and low productivity are telling us. They are not just background variables that we have to take as given and adjust our wage expectations accordingly. Instead, low inflation and low productivity should be seen as signs of slack in and of themselves.

Last week’s GDP data shows there’s still no reason to think the TCJA’s corporate rate cuts are trickling down to workers

Last Friday, new data was released by the Bureau of Economic Analysis (BEA) with the headline being a 4.1 percent annualized rate of GDP growth. Supporters of the Tax Cuts and Jobs Act (TCJA) have pointed to this data point as proof that the tax cuts are working, though there’s little indication that economic growth has moved off its previous trend. But the release of new economic data does give us another chance to see what that data is telling us so far about the effects of the TCJA. The punchline is simple: the TCJA has already fattened up the incomes of capital owners and corporations in a measurable way, but there’s no indication at all that any of it threatens to trickle-down to workers.

The corporate sector is unsurprisingly where the clearest near-term effects of the TCJA can be seen. Domestic after-tax corporate profits increased from 6.7 percent of GDP in 2017 to 7.4 percent in the first quarter of 2018. In particular, undistributed domestic corporate profits surged in response to the TCJA’s tax windfall for multinational corporations on the profits they had booked offshore. As the chart below shows, much like the spike following the 2004 repatriation tax “holiday,” undistributed domestic corporate profits rose from 2.5 percent of gross domestic corporate value added in 2017 to 12 percent in the first quarter of 2018. We should note that 2004’s tax holiday didn’t lead to a surge in wage growth in subsequent years.

First quarter data from 2018 shows an enormous spike in undistributed profits: Undistributed domestic corporate profits as a percent of domestic corporate gross value added, 1979Q1-2018Q1

| Undistributed profits as a percent of corporate gross value added | |

|---|---|

| 1979Q1 | 4.71% |

| 1979Q2 | 4.39% |

| 1979Q3 | 4.05% |

| 1979Q4 | 3.70% |

| 1980Q1 | 2.84% |

| 1980Q2 | 1.73% |

| 1980Q3 | 2.42% |

| 1980Q4 | 3.02% |

| 1981Q1 | 3.30% |

| 1981Q2 | 3.57% |

| 1981Q3 | 4.13% |

| 1981Q4 | 3.74% |

| 1982Q1 | 3.15% |

| 1982Q2 | 4.05% |

| 1982Q3 | 3.70% |

| 1982Q4 | 3.05% |

| 1983Q1 | 3.35% |

| 1983Q2 | 3.88% |

| 1983Q3 | 4.08% |

| 1983Q4 | 4.39% |

| 1984Q1 | 5.08% |

| 1984Q2 | 5.02% |

| 1984Q3 | 5.17% |

| 1984Q4 | 5.39% |

| 1985Q1 | 5.15% |

| 1985Q2 | 4.77% |

| 1985Q3 | 5.37% |

| 1985Q4 | 4.36% |

| 1986Q1 | 3.72% |

| 1986Q2 | 3.08% |

| 1986Q3 | 2.83% |

| 1986Q4 | 2.34% |

| 1987Q1 | 2.62% |

| 1987Q2 | 2.98% |

| 1987Q3 | 3.45% |

| 1987Q4 | 3.18% |

| 1988Q1 | 3.80% |

| 1988Q2 | 3.43% |

| 1988Q3 | 2.91% |

| 1988Q4 | 3.62% |

| 1989Q1 | 2.09% |

| 1989Q2 | 2.15% |

| 1989Q3 | 2.13% |

| 1989Q4 | 1.75% |

| 1990Q1 | 1.48% |

| 1990Q2 | 1.81% |

| 1990Q3 | 1.01% |

| 1990Q4 | 0.92% |

| 1991Q1 | 1.49% |

| 1991Q2 | 1.57% |

| 1991Q3 | 1.59% |

| 1991Q4 | 1.31% |

| 1992Q1 | 1.54% |

| 1992Q2 | 1.50% |

| 1992Q3 | 1.36% |

| 1992Q4 | 1.66% |

| 1993Q1 | 1.53% |

| 1993Q2 | 1.99% |

| 1993Q3 | 2.30% |

| 1993Q4 | 2.54% |

| 1994Q1 | 3.09% |

| 1994Q2 | 3.24% |

| 1994Q3 | 3.40% |

| 1994Q4 | 3.55% |

| 1995Q1 | 3.30% |

| 1995Q2 | 3.46% |

| 1995Q3 | 3.71% |

| 1995Q4 | 3.75% |

| 1996Q1 | 4.14% |

| 1996Q2 | 4.04% |

| 1996Q3 | 3.91% |

| 1996Q4 | 3.97% |

| 1997Q1 | 4.25% |

| 1997Q2 | 4.20% |

| 1997Q3 | 4.38% |

| 1997Q4 | 3.92% |

| 1998Q1 | 2.83% |

| 1998Q2 | 2.85% |

| 1998Q3 | 3.16% |

| 1998Q4 | 2.69% |

| 1999Q1 | 3.04% |

| 1999Q2 | 2.94% |

| 1999Q3 | 2.57% |

| 1999Q4 | 1.82% |

| 2000Q1 | 1.37% |

| 2000Q2 | 1.08% |

| 2000Q3 | 0.87% |

| 2000Q4 | 0.46% |

| 2001Q1 | 0.57% |

| 2001Q2 | 1.00% |

| 2001Q3 | 0.33% |

| 2001Q4 | -0.29% |

| 2002Q1 | 1.38% |

| 2002Q2 | 1.56% |

| 2002Q3 | 2.06% |

| 2002Q4 | 2.36% |

| 2003Q1 | 2.66% |

| 2003Q2 | 1.88% |

| 2003Q3 | 2.66% |

| 2003Q4 | 2.41% |

| 2004Q1 | 2.92% |

| 2004Q2 | 3.34% |

| 2004Q3 | 3.51% |

| 2004Q4 | 1.22% |

| 2005Q1 | 3.24% |

| 2005Q2 | 4.83% |

| 2005Q3 | 6.26% |

| 2005Q4 | 8.40% |

| 2006Q1 | 3.79% |

| 2006Q2 | 3.40% |

| 2006Q3 | 3.22% |

| 2006Q4 | 1.40% |

| 2007Q1 | 2.11% |

| 2007Q2 | 2.38% |

| 2007Q3 | 0.99% |

| 2007Q4 | 1.16% |

| 2008Q1 | 0.88% |

| 2008Q2 | 0.66% |

| 2008Q3 | 2.14% |

| 2008Q4 | 1.91% |

| 2009Q1 | 1.01% |

| 2009Q2 | 1.53% |

| 2009Q3 | 3.22% |

| 2009Q4 | 3.84% |

| 2010Q1 | 4.38% |

| 2010Q2 | 4.73% |

| 2010Q3 | 5.10% |

| 2010Q4 | 4.57% |

| 2011Q1 | 3.40% |

| 2011Q2 | 4.51% |

| 2011Q3 | 4.52% |

| 2011Q4 | 4.69% |

| 2012Q1 | 4.49% |

| 2012Q2 | 4.78% |

| 2012Q3 | 4.17% |

| 2012Q4 | 2.56% |

| 2013Q1 | 4.60% |

| 2013Q2 | 4.71% |

| 2013Q3 | 3.49% |

| 2013Q4 | 4.75% |

| 2014Q1 | 2.65% |

| 2014Q2 | 3.81% |

| 2014Q3 | 4.97% |

| 2014Q4 | 4.75% |

| 2015Q1 | 3.63% |

| 2015Q2 | 3.37% |

| 2015Q3 | 3.65% |

| 2015Q4 | 2.47% |

| 2016Q1 | 3.33% |

| 2016Q2 | 2.18% |

| 2016Q3 | 2.48% |

| 2016Q4 | 2.00% |

| 2017Q1 | 2.17% |

| 2017Q2 | 2.24% |

| 2017Q3 | 3.06% |

| 2017Q4 | 2.58% |

| 2018Q1 | 12.04% |

Source: EPI analysis of data from table 1.14 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Corporate tax revenues as a share of the economy fell by more than a third, from 1.8 percent of GDP in 2017 to 1.1 percent in the first quarter of 2018. This data makes it clear that the TCJA made some people very rich in the first quarter of 2018. (Second quarter corporate data has not been released yet.) Does Friday’s data on the overall economy show any indication that the corporate tax cuts have started to trickle down to workers as the Trump administration promised?

Nope, not at all. For one, wages haven’t budged. To be fair, no serious economist should have argued that wages are expected to respond immediately to corporate tax cuts. Though that didn’t keep TCJA supporters (including some economists willing to act unserious) from touting bonuses paid late last year as proof that the tax cuts were working as intended. It’s worth reminding ourselves of the economic chain of causation that leads from corporate tax cuts to wage growth. First, the direct benefits of corporate tax cuts flow entirely to shareholders. That part has definitely happened. Then, (as we’ve previously explained), higher after-tax profitability is supposed to incentivize firms to invest more, with those investments financed by the higher savings that households provide in response to higher returns. These investments in turn are supposed to give workers more and better tools to do their jobs, which boosts productivity and eventually that increase in productivity translates into wage growth.

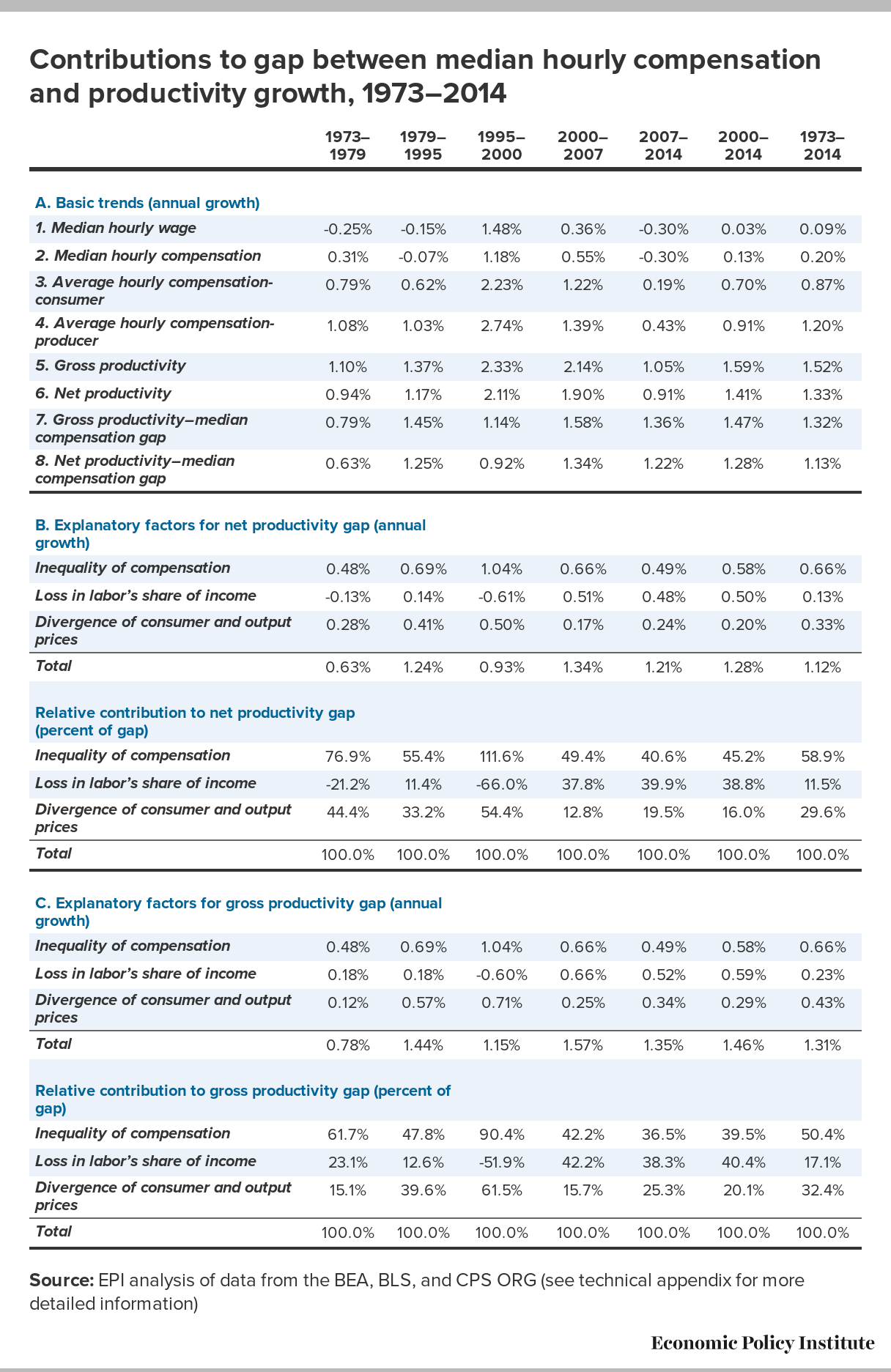

Nothing misleading about this: Typical workers’ pay and productivity have diverged

Jason Furman has an interesting piece on Vox today, claiming that the “puzzle” of weak wage growth in the face of low unemployment is not really a puzzle at all.

There’s a lot in this piece to agree with and a lot to quibble with. But, this post will just note one quick quibble. Furman describes a chart of ours—one we like a lot—as “misleading.” Here’s the full paragraph from him:

Productivity does a good job of explaining the evolution of average wage growth in the United States as well, especially prior to 2000. (But it does a decent job even since then, even with the wage slowdown.) From the end of World War II until around 2000 average wages grew almost lock-step with productivity — if you use the same measure of inflation for both concepts, so the comparison is apples to apples. Often, presentations of the comparison between wages and productivity, as in this much-reproduced graphic, use a higher inflation measure to adjust wages than productivity and thus produce a misleading impression.

This is a criticism we’ve seen, and addressed, before, so forgive me if I seem a tad sensitive on this, but I want to be really clear: there is nothing misleading about our presentation of this data. The wedge we show between our measure of pay and economy-wide productivity is indeed driven overwhelmingly by rising inequality and not the differing deflators. In this figure we measure the pay of typical workers, not average wages. We define “typical” as either the median worker (the one in the middle of the wage distribution) or the average pay of production and non-supervisory workers (a group consisting of about 80 percent of the private-sector workforce). We don’t use average pay precisely because, as Jason notes, average pay kept up pretty well with economy-wide productivity pre-2000. This means that the bulk of the rise in inequality over that time was driven by inequality within wages, or the divergence between average and typical pay (as we clearly show—see the previous link).

{kind=link}