Full Report

Chief executive officers (CEOs) of the largest firms in the U.S. earn much more today than they did in the mid-1990s and many times what they earned in the 1960s or 1970s. They also earn far more than the typical worker,1 and their pay—which relies heavily on stock-related compensation—has grown much more rapidly than a typical worker’s pay. Rising CEO pay does not reflect a rising value of skills or contributions to firms’ productivity. What has changed over the years is CEOs’ use of their power to set their own pay. In economic terms, this means that CEO compensation reflects substantial “rents” (income in excess of actual productivity). This is concerning since the earning power of CEOs has been driving income growth at the very top—a key dynamic in the overall growth of inequality. The silver lining in this otherwise unfortunate trend is that CEO pay can be curtailed without damaging economywide growth.

Key findings

- Growth of CEO compensation (1978–2023). Since CEO pay is mostly stock based—and the value of stocks changes frequently—calculating it is not entirely straightforward. We use two measures to give a fuller picture: a backward-looking measure—realized compensation—and a forward-looking measure—granted compensation. Realized compensation of the top CEOs shot up 1,085% from 1978 to 2023 (adjusting for inflation), compared with the slow 24% growth in a typical worker’s annual compensation. CEO granted compensation rose 932% from 1978 to 2023.

- Changes in the CEO-to-worker compensation ratio (1965–2023). The realized CEO-to-worker compensation ratio was 290-to-1 in 2023, in stark contrast to the 21-to-1 ratio in 1965. Over the last two decades, the ratio has been far higher than at any point from the 1960s to the early 1990s. The granted CEO-to-worker compensation ratio was to 192-to-1 in 2023—significantly lower than its peak of 398-to-1 in 2000, but still many times higher than the 45-to-1 ratio of 1989 or the 15-to-1 ratio of 1965.

- Changes in the composition of CEO compensation. While stock-related components constitute a large and growing share of total compensation, the composition of CEO compensation is shifting away from the use of stock options and toward stock awards—a promising move to align CEO pay to longer-term incentives. In 2006, stock options accounted for just over 70% of stock-related pay in realized CEO compensation. But in 2023, stock options made up only 22%, with vested stock awards accounting for the rest. Stock-related pay (exercised stock options and vested stock awards) averaged $16.7 million in 2023 and accounted for 77.6% of average realized CEO compensation.

- Changes in the CEO-to-top-0.1% compensation ratio. CEO compensation has been breaking away from that of other very highly compensated workers. Over the last three decades, compensation grew far faster for CEOs than it did for the top 0.1% of wage earners (those earning more than 99.9% of wage earners). CEO compensation in 2022 (the latest year for which data on top 0.1% wage earners are available) was 9.4 times as high as wages of the top 0.1% of wage earners, a ratio 6.8 points greater than the 2.6-to-1 average CEO-to-top-0.1% ratio over the 1965–1978 period.

- Implications of the growth of the CEO-to-top-0.1% compensation ratio. The fact that CEO compensation has grown much faster than the pay of the top 0.1% of wage earners indicates that CEO compensation growth does not simply reflect a competitive race for skills (the “market for talent”) that would also increase the value of highly paid professionals more generally, but instead suggests the growth of substantial economic rents (income not related to a corresponding growth of productivity) in CEO compensation. CEO compensation does not appear to reflect the greater productivity of executives, but their ability to extract concessions from corporate boards—thanks to dysfunctional systems of corporate governance in the United States. But because so much of CEOs’ income constitutes economic rent, there would be no adverse impact on the economy’s output or on employment if CEOs earned less or were taxed more.

- Cost of rising inequality for most workers. If very high earners hadn’t pulled away so dramatically, there would be room for broader-based wage growth for the rest of the workforce. Most of the rise in inequality over the last four decades has redistributed wages away from most workers.

Measuring CEO compensation

We focus on the average compensation of CEOs at the 350 largest publicly owned U.S. firms (firms that sell stock on the open market) by revenue. Our source of data is the S&P Compustat ExecuComp database for the years 1992 to 2023, and survey data published by The Wall Street Journal for selected years back to 1965. We maintain the sample size of 350 firms each year when using the Compustat ExecuComp data.2

A note about the Compustat data

It is worth noting some complexity of the Compustat data at the outset. Compustat tracks data (including measures of CEO compensation) for all publicly traded firms in the United States across a range of years (we use it back to 1992 and find it reliable since that year). But public companies sometimes move out of the data universe of publicly traded firms. They might go private, go out of business entirely, or be bought by another firm. When a firm stops being public, it does not simply drop out of the sample from that point on; it is also removed from previous years’ samples in the Compustat database.

Optimally, we would like the Compustat data to provide information on the largest 350 firms that were public in a given year. Instead, the data provide information on the largest 350 firms that were public in a given year and that continue to be public, according to the most recent data. This explains why some of our data—even for years relatively far in the past—change with each iteration of this report.

Further, even the pre-1992 data that we use rely on a procedure that “backcasts” Compustat to pre-1992 data that originate from other sources. Therefore, even the pre-1992 data can change with each successive round of Compustat.

In practice, the degree of change to previous years’ data caused by this reshuffling of firms in the Compustat universe is quite small, but it is not zero.

Two ways of measuring CEO compensation

We use two measures of CEO compensation: one based on compensation as “realized,” and the other based on compensation as “granted.” Both measures include the same measures of salary, bonuses, and long-term incentive payouts. The difference lies in how each measure treats stock awards and stock options—major components of CEO compensation that change value from when they are first provided, or granted, to when they are realized.

The realized measure of compensation includes the value of stock options when they are actually realized or exercised, capturing the change in value from when the options were granted to when the CEO invokes the options, usually after the stock price has risen and options value has increased. The realized compensation measure also values stock awards at their value when vested (usually three years after being granted), capturing any change in the stock price as well as additional stock awards provided as part of a performance award.

The granted measure of compensation values stock options and restricted stock awards by their “fair value” when granted. This fair value must be estimated based on several assumptions about the future path of stock prices, interest rates, and other variables. Compustat estimates of the fair value of options and stock awards as granted are derived from the Black-Scholes model. For details on the construction of these measures and benchmarking to other studies, see Sabadish and Mishel (2013).

In some sense, realized measures of pay are backward-looking, while granted measures are forward-looking. Realized measures of stock-related pay in 2023 are essentially measuring how much money CEOs were able to bring home based (largely) on the past year’s stock options and awards. Granted measures of stock-related pay in 2023 are essentially estimating how much new options and awards are likely to pay off in future years. Because neither measure perfectly maps onto a measure of how much a CEO “earned” in a single particular year, reporting both can be useful for understanding the full picture.

Trends in CEO compensation

Table 1 presents the trends in inflation-adjusted realized and granted CEO compensation for selected years from 1965 to 2023 (columns 1 and 2).3 Real changes in the stock market are as measured by the S&P 500 Index and the Dow Jones Industrial Average in columns 3 and 4. In general, CEO compensation follows the movement of the stock market

The last year of data saw a striking exception to that phenomenon: The drop in CEO compensation from 2022 to 2023 was large compared with very little change in the stock market over that period. Realized CEO compensation (reported in Table 1) declined by 19.4% to $22.2 million from 2022 to 2023.4 The granted measure of CEO compensation, which values stock options granted in 2023 (not those exercised), also fell by 14.1%. While it is somewhat puzzling for CEO pay to fall as the stock market largely held steady, it’s possible that the shift in stock-related pay away from options played a role, and this overall divergence will likely turn around with the stock market gains so far in 2024.

Longer-term trends in CEO compensation

Table 1 also presents the longer-term trends in CEO compensation for selected years from 1965 to 2023.5 Our discussion of longer-term trends focuses mostly on the realized compensation measure of CEO compensation—the measure preferred in most economic analyses. In general, CEO compensation follows the movement of the stock market but tends to exceed even the largest stock market gains.

CEO compensation, CEO-to-worker compensation ratio, and stock prices (2023$), selected years, 1965–2023

| CEO annual compensation (thousands) | Stock market (indexed to 2023$) | Private-sector production/nonsupervisory workers annual compensation (thousands) |

CEO-to-worker compensation ratio | |||||

|---|---|---|---|---|---|---|---|---|

| Year(s) | Realized | Granted | S&P 500 | Dow Jones | All private-sector workers | Workers in the firms’ industries* | Realized | Granted |

| 1965 | $1,041 | $793 | 694 | 7,172 | $47 | NA | 20.8 | 15.4 |

| 1973 | $1,367 | $1,041 | 617 | 5,310 | $56 | NA | 23.1 | 17.2 |

| 1978 | $1,874 | $1,426 | 386 | 3,302 | $57 | NA | 31.0 | 23.0 |

| 1989 | $3,496 | $2,662 | 720 | 5,596 | $54 | NA | 60.5 | 44.9 |

| 1995 | $6,777 | $7,529 | 1,010 | 8,392 | $54 | $61 | 117.7 | 130.9 |

| 2000 | $24,543 | $24,567 | 2,380 | 17,883 | $58 | $67 | 384.1 | 398.0 |

| 2007 | $22,208 | $16,853 | 2,094 | 18,680 | $61 | $72 | 330.2 | 243.6 |

| 2009 | $11,644 | $12,821 | 1,303 | 12,209 | $64 | $75 | 166.5 | 181.2 |

| 2022 | $27,549 | $17,132 | 4,261 | 34,204 | $70 | $79 | 360.2 | 225.5 |

| 2023 | $22,207 | $14,724 | 4,284 | 34,122 | $71 | $80 | 290.3 | 191.6 |

| Percent change | Change in ratio | |||||||

| 1965-1978 | 80% | 80% | -44% | -54% | 21% | NA | 10.2 | 7.6 |

| 1978–2023 | 1085% | 932% | 1008% | 933% | 24% | NA | 259.3 | 168.7 |

| 2022–2023 | -19% | -14% | 1% | 0% | 1% | 2% | -69.9 | -33.8 |

*Average annual compensation of the workers in the key industry of the firms in the sample.

** We round numbers to the nearest thousand in Table 1, but dollar and percent changes are calculated using unrounded data.

Notes: Average annual compensation for CEOs at the top 350 U.S. firms ranked by sales is measured in two ways. Both include salary, bonus, and long-term incentive payouts, but the “granted” measure includes the value of stock options and stock awards when they were granted, whereas the “realized” measure captures the value of stock-related components that accrues after options or stock awards are granted by including “stock options exercised” and “vested stock awards.” CEO compensation for 2023 is projected from data reported through June 2024. CEO-to-worker compensation ratios are based on averaging specific firm ratios in samples and not the ratio of averages of CEO and worker compensation. Ratios prior to 1992 are constructed as described in the CEO pay series methodology (Sabadish and Mishel 2013).

Source: Authors’ analysis of data from Compustat’s ExecuComp database, the Federal Reserve Economic Data (FRED) database from the Federal Reserve Bank of St. Louis, the Bureau of Labor Statistics’ Current Employment Statistics data series, and the Bureau of Economic Analysis NIPA tables.

As mentioned above, realized CEO compensation has, in general, risen and fallen along with the S&P 500 Index over the last five and a half decades. But the period from 1965 to 1978 is an exception: Although the stock market fell by roughly half between 1965 and 1978, realized CEO compensation increased by 79.9%.

To assess the role of CEO compensation in the overall increase in income and wage inequality of the last four decades, it is best to gauge growth since 1978.6 For the period from 1978 to 2023, realized CEO compensation increased 1,085%—77% faster than stock market growth (based on the growth of the S&P 500) and substantially faster than the 24% growth in the typical worker’s compensation over the same period. CEO granted compensation grew 932% over this period.

Trends in the CEO-to-worker compensation ratio

Table 1 allows us to compare CEO compensation with that of a typical worker by showing the average annual compensation (wages and benefits of a full-time, full-year worker) of private-sector production/nonsupervisory workers (a group covering more than 80% of payroll employment; see Gould 2020) in column 5.

From 1992 onward, column 6 of the table also identifies the average annual compensation of production/nonsupervisory workers in the key industries of the firms included in the sample. We take this compensation as a proxy for typical workers’ pay in these firms and use it to calculate the CEO-to-worker compensation ratio for each firm.

Columns 7 and 8 present trends in the ratio of CEO-to-worker compensation, using both measures of CEO compensation. We compute this ratio, which illustrates the increased divergence between CEO and worker pay over time, in two steps:

- The first step is to construct, for each of the 350 largest U.S. firms, the ratio of the CEO’s compensation to the annual average compensation of production and nonsupervisory workers in the key industry of the firm (data on the pay of workers at individual firms are not available).7

- The second step is to average that ratio across all 350 firms. Note that trends before 1995 are based on the ratio of average top-company CEO pay to the compensation of economywide (not industry-specific) private-sector production/nonsupervisory workers.

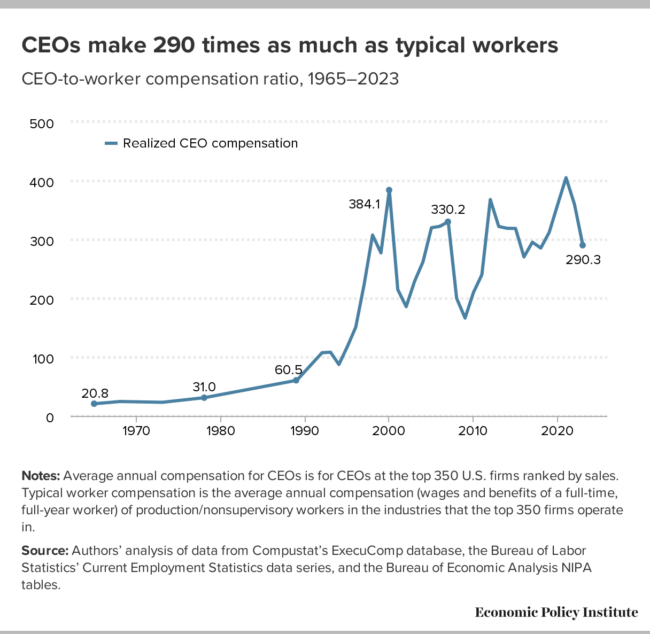

CEO-to-worker compensation trends are depicted in Figure A.

CEOs paid 281 times as much as typical workers: CEO-to-worker compensation ratio, 1965–2024

| year | Realized CEO compensation | Granted CEO compensation |

|---|---|---|

| 1965 | 20.62 | 15.30 |

| 1966 | 21.85 | 16.21 |

| 1967 | 23.08 | 17.12 |

| 1968 | 24.31 | 18.03 |

| 1969 | 24.04 | 17.83 |

| 1970 | 23.76 | 17.63 |

| 1971 | 23.49 | 17.43 |

| 1972 | 23.22 | 17.23 |

| 1973 | 22.95 | 17.02 |

| 1974 | 24.51 | 18.18 |

| 1975 | 26.07 | 19.34 |

| 1976 | 27.63 | 20.49 |

| 1977 | 29.18 | 21.65 |

| 1978 | 30.74 | 22.80 |

| 1979 | 33.41 | 24.78 |

| 1980 | 36.08 | 26.76 |

| 1981 | 38.75 | 28.75 |

| 1982 | 41.42 | 30.73 |

| 1983 | 44.09 | 32.71 |

| 1984 | 46.76 | 34.69 |

| 1985 | 49.43 | 36.67 |

| 1986 | 52.10 | 38.65 |

| 1987 | 54.77 | 40.63 |

| 1988 | 57.44 | 42.61 |

| 1989 | 60.11 | 44.59 |

| 1990 | 75.64 | 56.11 |

| 1991 | 91.16 | 67.62 |

| 1992 | 106.69 | 79.14 |

| 1993 | 108.24 | 99.20 |

| 1994 | 87.58 | 117.85 |

| 1995 | 117.07 | 130.09 |

| 1996 | 150.00 | 176.33 |

| 1997 | 223.10 | 234.83 |

| 1998 | 304.24 | 301.50 |

| 1999 | 275.26 | 288.46 |

| 2000 | 379.63 | 393.08 |

| 2001 | 214.27 | 325.71 |

| 2002 | 186.16 | 234.92 |

| 2003 | 228.47 | 226.40 |

| 2004 | 261.83 | 231.92 |

| 2005 | 319.52 | 244.33 |

| 2006 | 322.41 | 237.31 |

| 2007 | 328.49 | 242.43 |

| 2008 | 200.03 | 218.26 |

| 2009 | 166.39 | 181.24 |

| 2010 | 209.95 | 204.10 |

| 2011 | 238.91 | 212.40 |

| 2012 | 363.43 | 205.70 |

| 2013 | 318.54 | 211.34 |

| 2014 | 320.26 | 221.00 |

| 2015 | 320.30 | 215.88 |

| 2016 | 269.28 | 219.43 |

| 2017 | 294.38 | 233.51 |

| 2018 | 284.37 | 228.79 |

| 2019 | 311.48 | 229.36 |

| 2020 | 356.22 | 212.73 |

| 2021 | 408.47 | 272.98 |

| 2022 | 361.29 | 226.00 |

| 2023 | 276.47 | 196.98 |

| 2024 | 280.72 | 212.57 |

Notes: Average annual compensation for CEOs at the top 350 U.S. firms ranked by sales is measured in two ways. Both include salary, bonus, and long-term incentive payouts, but the “granted” measure includes the value of stock options and stock awards when they were granted, whereas the “realized” measure captures the value of stock-related components that accrues after options or stock awards are granted by including “stock options exercised” and “vested stock awards.” Projected value for 2024 is based on the percent change in CEO pay in the samples available in June 2023 and in August 2024 applied to the full-year 2023 value. “Typical worker” compensation is the average annual compensation (wages and benefits of a full-time, full-year worker) of production/nonsupervisory workers in the industries that the top 350 firms operate in.

Source: Authors’ analysis of data from Compustat’s ExecuComp database, the Bureau of Labor Statistics’ Current Employment Statistics data series, and the Bureau of Economic Analysis NIPA tables.

How our metric differs from firm-reported metrics

The Securities and Exchange Commission (SEC) now requires publicly owned firms to provide a metric for the ratio of CEO compensation to that of the median worker in a firm, as mandated by the Dodd-Frank financial reform bill of 2010 (SEC 2015). Those ratios differ from the ones in this report in several ways:

- First, because of limitations in data availability, the measure of worker compensation in our ratios reflects workers in a firm’s key industry, not workers actually working for the firm. The ratios reported to the SEC will reflect compensation of workers in the specific firm.

- Second, our measure reflects an exclusively domestic workforce; it excludes the compensation of workers in other countries who work for the firm. The ratios reported to the Securities and Exchange Commission may include workers in other countries.

- Third, our metric is based on hourly compensation annualized to reflect a full-time, full-year worker (i.e., multiplying the hourly compensation rate by 2,080 hours). In contrast, the measures firms provide to the SEC can be (and sometimes are) based on the actual annual (not annualized) wages of part-year (seasonal) or part-time workers. As a result, comparisons across firms may reflect not only hourly pay differences but also differences in annual or weekly hours worked.

- Fourth, our metric includes both wages and benefits, whereas the SEC metric focuses solely on wages.

- Finally, we use consistent data and methodology to construct our ratios; our ratios are thus comparable across firms and from year to year. The Securities and Exchange Commission allows firms flexibility in how they construct the CEO-to-typical worker pay comparison. This means there is no comparability across firms—and ratios for any given firm may not even be comparable from year to year if the firm changes the metrics it uses.

There is certainly value in the new metrics being provided to the SEC, but the measures we rely on allow us to make appropriate comparisons between firms and across time. More information on the SEC CEO-to-worker compensation ratio and our comparable measure can be found in Mishel and Kandra (2020).

As Table 1 and Figure A show, using the realized measure of CEO compensation, CEOs of major U.S. companies earned 21 times as much as the typical worker in 1965. This ratio grew to 31-to-1 in 1978 and 61-to-1 by 1989. It surged in the 1990s, hitting 384-to-1 in 2000, at the end of the 1990s recovery and at the height of the stock market bubble.8

The fall in the stock market after 2000 reduced CEO stock-related pay, such as realized stock options, and caused CEO compensation to tumble in 2002 before beginning to rise again in 2003. Realized CEO compensation recovered to a level of 330 times worker pay by 2007, still below its 2000 level. The financial crisis of 2008 and accompanying stock market decline reduced CEO compensation between 2007 and 2009, and the CEO-to-worker compensation ratio fell in tandem.

Over the 2009–2021 period, another surge in realized CEO compensation brought the ratio to 405-to-1, a historic high. The ratio experienced significant declines between 2021 and 2023, as CEO pay fell. In 2023, the CEO-to-worker compensation ratio was 290-to-1. Even with the recent losses, the 2023 ratio is still far higher than it was in the 1960s, 1970s, 1980s, and the early 1990s.

The pattern using the granted measure of CEO compensation is similar. The CEO-to-worker pay ratio peaked in 2000 at 398-to-1, even higher than the 384-to-1 ratio using the realized compensation measure. By 2023, the granted compensation ratio decreased to 192-to-1. This level is far lower than its peak in 2000, but still much greater than the ratios in 1995 (131-to-1), 1989 (45-to-1), or 1965 (15-to-1).

The extraordinarily high level of the CEO-to-worker compensation ratio reflects the strikingly different trajectory of CEO pay compared with typical worker pay over the past 40 years. On the one hand, there has been little growth in the compensation of a typical worker since the late 1970s: It has grown just 24.0% over the 45 years from 1978 to 2023, despite a corresponding growth of net economywide productivity of 74.8% (EPI 2024). Meanwhile, the 1,085% growth in realized CEO compensation from 1978 to 2023 (excluding 1979, since there are no data for that year) exceeded the growth in productivity in that period.

Changes in the composition of CEO compensation

Stock-related components of CEO compensation constitute a large and increasing share of total compensation. Realized stock awards and stock options made up 70.2% of total CEO compensation in 2006 ($15.1 million out of $21.5 million) and 76.6% of total compensation in 2023 ($17.0 million out of $22.2 million; not shown in chart). The growth of these stock-related components from 2006 to 2022 explains over 100% of the total growth in CEO realized compensation over this period.9 Of the stock-related components of compensation, stock awards make up a growing share, while the share of stock options in CEO compensation packages has decreased over time.

There is a simple logic behind companies’ decisions to shift from stock options to stock awards in CEO compensation packages, as Clifford (2017) explains. With stock options, CEOs can only make gains: They realize a gain if their company’s stock price rises beyond the price of the initial options granted, and they lose nothing if the stock price falls. Having nothing to lose—but potentially a lot to gain—might lead options-holding CEOs to take excessive risks to bump up their company’s stock price to an unsustainable short-term high.

Stock awards, on the other hand, likely promote better long-term alignment of a CEO’s goals with those of shareholders. A stock award has a value when granted or vested and can increase or decrease in value as the firm’s stock price changes. If stock awards have a lengthy vesting period of three to five years, then the CEO has an interest in lifting the firm’s stock price over that period while being mindful to avoid any implosion in the stock price—to maintain the value of what they have. In some sense, the shift from options to awards might represent a small glimmer of hope that CEO labor markets are getting a bit less dysfunctional (though there is obviously a long way to go).

CEO pay is excessive even relative to other extraordinarily privileged actors in the economy

This section highlights how distorted CEO pay is, even compared with the most privileged workers in the U.S. economy—the top 0.1%. CEO compensation has grown a great deal since 1965 and so has the pay of other high-wage earners.

To some analysts, this suggests that the dramatic rise in CEO compensation has been driven largely by the demand for the skills of CEOs and other highly paid professionals. In this interpretation, CEO compensation is being set by the market for “skills” or “talent,” not by managerial power or the ability of CEOs to extract economic rents (income in excess of their contribution to actually producing it). The “market for talent” argument is based on the premise that it is other professionals, too, not just CEOs, who are seeing a generous rise in pay. The most prominent example of this argument comes from Kaplan (2012a, 2012b), who claims that a stable ratio of CEO-to-top 0.1% pay indicates that market power is not operating uniquely in CEO pay markets.

This lies in contrast to the explanation offered by Bebchuk and Fried (2004) and Clifford (2017) who claim that the long-term increase in CEO pay is a result of managerial power. Similarly, Bivens and Mishel (2013) argue that CEO pay gains are not the result of a competitive market for talent, but rather reflect the power of CEOs to extract concessions from corporate boards. A growing CEO-to-top-0.1% pay ratio would indicate that the scope for this unique exercise of market power in CEO labor markets is large.

To test the alternative theories, we compare CEO-to-top 0.1% pay ratios beginning in 1965, shown in Figure B. In 2022 (the last year available for the top 0.1% data series), this ratio was 9.4, meaning that CEOs made over 9 times as much in salary as even the most privileged 0.1% of workers in the economy. This 9.4 ratio in 2022 was 6.8 points higher than the historical average of 2.6 over the 1965–1978 period. This is a large change, meaning that the relative pay of CEOs increased by an amount equal to the total annual wages of nearly seven of these very high wage earners.10

CEO pay rising far faster than that of the top 0.1% suggests that market power is uniquely operating in CEO pay markets and rising pay is not a result of a competitive market for talent.

CEO compensation relative to top 0.1% earners is much higher than it was in the 1965–1978 period: Ratio of CEO compensation to top 0.1% wages, 1965–2022

| Year | Ratio of CEO pay to top 0.1% wages | 1965–1978 average ratio: 2.6 |

|---|---|---|

| 1965 | 2.3 | 2.6 |

| 1966 | NA | 2.6 |

| 1967 | NA | 2.6 |

| 1968 | 2.6 | 2.6 |

| 1969 | NA | 2.6 |

| 1970 | NA | 2.6 |

| 1971 | NA | 2.6 |

| 1972 | NA | 2.6 |

| 1973 | 2.4 | 2.6 |

| 1974 | NA | 2.6 |

| 1975 | NA | 2.6 |

| 1976 | NA | 2.6 |

| 1977 | NA | 2.6 |

| 1978 | 3.1 | 2.6 |

| 1979 | NA | 2.6 |

| 1980 | NA | 2.6 |

| 1981 | NA | 2.6 |

| 1982 | NA | 2.6 |

| 1983 | NA | 2.6 |

| 1984 | NA | 2.6 |

| 1985 | NA | 2.6 |

| 1986 | NA | 2.6 |

| 1987 | NA | 2.6 |

| 1988 | NA | 2.6 |

| 1989 | 2.4 | 2.6 |

| 1990 | NA | 2.6 |

| 1991 | NA | 2.6 |

| 1992 | 3.8 | 2.6 |

| 1993 | 4.4 | 2.6 |

| 1994 | 3.9 | 2.6 |

| 1995 | 4.4 | 2.6 |

| 1996 | 5.3 | 2.6 |

| 1997 | 7.0 | 2.6 |

| 1998 | 9.2 | 2.6 |

| 1999 | 7.2 | 2.6 |

| 2000 | 8.9 | 2.6 |

| 2001 | 5.9 | 2.6 |

| 2002 | 5.8 | 2.6 |

| 2003 | 7.4 | 2.6 |

| 2004 | 7.3 | 2.6 |

| 2005 | 8.3 | 2.6 |

| 2006 | 8.1 | 2.6 |

| 2007 | 7.6 | 2.6 |

| 2008 | 5.7 | 2.6 |

| 2009 | 5.5 | 2.6 |

| 2010 | 6.2 | 2.6 |

| 2011 | 6.8 | 2.6 |

| 2012 | 9.0 | 2.6 |

| 2013 | 8.6 | 2.6 |

| 2014 | 8.2 | 2.6 |

| 2015 | 8.0 | 2.6 |

| 2016 | 7.6 | 2.6 |

| 2017 | 7.7 | 2.6 |

| 2018 | 7.6 | 2.6 |

| 2019 | 8.4 | 2.6 |

| 2020 | 9.2 | 2.6 |

| 2021 | 8.2 | 2.6 |

| 2022 | 9.4 | 2.6 |

Note: Wages of top 0.1% of wage earners reflect W-2 annual earnings, which includes the value of exercised stock options and vested stock awards.

Source: Authors’ analysis of EPI State of Working America Data Library data on top 0.1% wages in Gould and Kandra 2023.

The extremely rapid growth of CEO compensation compared with the earnings of the top 0.1% of wage earners does not mean that the top 0.1% fared poorly. In fact, the very highest earners—those in the top 0.1% of all earners—saw their annual earnings (including realized stock options and vested stock awards) grow fantastically, though far less than the compensation of the CEOs of large firms (which are also a very small subset of the top 0.1%). Top 0.1% annual earnings grew a healthy 377.7% from 1978 to 2022, though that was just a small fraction of the 1,370.4% growth of realized CEO compensation achieved between 1978 and 2022 (strict comparability on the years 1979 to 2023 is not available because we do not have CEO data for 1979 nor top 0.1% data for 2023).

Since CEO pay growing far faster than the pay of other high earners is evidence of the presence of rents, one can conclude that today’s top executives are collecting substantial rents, claiming income that greatly exceeds their contribution to producing it. This means that if CEOs were paid less, there would be no loss of productivity or output in the economy.

The large discrepancy between the pay of CEOs and other very-high-wage earners also casts doubt on the claim that CEOs are being paid these extraordinary amounts because of their special skills and the market for those skills. It is unlikely that the skills of CEOs of very large firms are so outsized and disconnected from the skills of other high earners that they propel CEOs past most of their cohort in the top one-tenth of 1%. For everyone else, the distribution of skills, as reflected in the overall wage distribution, tends to be much more continuous, so this discontinuity is evidence that factors beyond skills drive the compensation levels of CEOs.

The stock market and CEO pay

There is normally a tight relationship between overall stock prices and CEO compensation. Some commentators draw on this regularity to claim that CEOs are being paid for their performance since, in the commentators’ view, the goal of CEOs is to raise their companies’ stock prices.

However, the stock–CEO compensation relationship does not necessarily imply that CEOs are enjoying high and rising pay because their individual productivity is increasing (for example, because they head larger firms, have adopted new technology, or for other reasons). CEO compensation often grows strongly when the overall stock market rises, and individual firms’ stock values are swept up in this wake. This is a marketwide phenomenon, not one based on the improved performance of individual firms.

Most CEO pay packages allow pay to rise whenever the firm’s stock value rises. In other words, CEOs can cash out stock options regardless of whether the rise in the firm’s stock value was exceptional relative to comparable firms in the same industry. Similarly, vested stock awards increase in value when the firm’s stock price rises in simple correspondence to a marketwide escalation of stock prices. If corporate taxes are reduced and profits rise accordingly, leading to higher stock prices, is it accurate to say that CEOs have made their firms perform better?

The connection between CEO pay and overall inequality

Some observers argue that exorbitant CEO compensation is merely a symbolic issue, with no real consequences for most workers. But on the contrary, the escalation of CEO compensation— and of executive compensation more generally—has likely helped fuel the wider growth of top 1% and top 0.1% incomes, contributing to widespread inequality.

Our data apply to the CEOs of the very largest firms. We presume that these CEOs set the pay standards followed by other executives—of the largest publicly owned firms, of smaller publicly owned firms, of privately owned firms, and of major nonprofit firms (hospitals, universities, charities, etc.). If so, then CEO compensation is indeed a nontrivial driver of top incomes.

Another implication of rising pay for CEOs and other executives is that it reflects income that would otherwise have accrued to others instead of being concentrated at the highest level. What these executives earned was not available for broader-based wage growth for other workers (Bivens and Mishel 2013). It is useful, in this context, to note that wages for the bottom 90% would be 16% higher today had wage inequality not increased between 1979 and 2022.11

Most of the rise in inequality took the form of redistributing wages away from the bottom 90%. This group’s share of total wage income fell from 69.8% in 1979 to 60.1% in 2022. Most of the loss experienced by the bottom 90% went to the top 1%, whose wage share grew substantially from 7.3% to 12.9% in these same years. And even among this gain going to the top 1%, most of it went to the top 0.1%, who saw their share of overall wage income nearly triple from 1.6% to 4.6% between 1979 and 2022. In other words, the bottom 90% lost 9.7% of total wage income between 1979 and 2022, and nearly 60% of this loss (5.6 of 9.7 percentage points) went to the top 1%, while 30% (or 3.0 of 9.7 percentage points) went to just the top 0.1%.

Policy recommendations: Reversing the trend

Several policy options could reverse the trend of excessive executive pay and broaden wage growth. Ideally, tax reforms would be paired with changes in corporate governance:

- Implementing higher marginal income tax rates at the very top would limit rent-seeking behavior and reduce the incentives for executives to push for such high pay.

- Setting corporate tax rates higher for firms that have higher ratios of CEO-to-worker compensation is another option. Clifford (2017) recommends setting a cap on executive compensation and taxing companies on any amount over the cap, similar to the way baseball team payrolls are taxed when salaries exceed a cap. One key consideration in making policies like this work concerns “fissuring”—the practice of spinning off the lower-paid workers in a given firm and using contracted third-party service providers to replace these functions (often rehiring the exact same workers but now no longer as permanent employees of the old firm). Such fissuring would boost firm-specific measures of typical workers’ pay and reduce the CEO-to-worker pay ratio, without changing any economic reality. The newly contracted workers would not necessarily see any higher pay, and the CEOs would not need to accept lower pay. This type of fissuring is endemic in the U.S. economy and is a policy obstacle to many efforts to constrain specific firms’ behavior through incentives like this.

Baker, Bivens, and Schieder (2019) review policies that would restrain CEO compensation and explain how tax policy and corporate governance reform can work in tandem:

Tax policy that penalizes corporations for excess CEO-to-worker pay ratios can boost incentives for shareholders to restrain excess pay, [but] to boost the power of shareholders [to restrain pay], fundamental changes to corporate governance have to be made. One key example of such a fundamental change would be to provide worker representation on corporate boards.

Given the vital importance of changing shareholders’ ability to restrain pay (not just their incentive to do so), another policy that could potentially limit executive pay growth is greater use of “say on pay,” which allows a firm’s shareholders to vote on top executives’ compensation.

The CEOs examined in this report head large firms. These firms, almost by definition, enjoy a degree of market power that some studies suggest has grown in recent decades. It seems that CEOs and other executives may have been prime beneficiaries of these firms’ greater market power. Using the tools of antitrust enforcement and regulation would help to restrain these firms’ market power. This would not only promote economic efficiency and competition but might help restrain executive pay as well.

Notes

1. For the pay of the typical worker, we use average compensation (wages and salaries plus benefits) of a full-time, full-year production or nonsupervisory worker (a group that makes up about 80% of the private-sector workforce).

2. In earlier reports, our sample for each year was sometimes fewer than 350 firms because some of these large firms did not have the same CEO for the entire (or most of the) year or the compensation data were not yet available. We now examine the top 350 firms with the largest revenues each year for which there are data to not let changes in sample size affect annual trends.

3. Authors’ analysis of the Compustat ExecuComp data.

4. Note that while we report executive compensation in millions in the text, and we round numbers to the nearest thousand in Table 1, dollar and percent changes are calculated using unrounded data.

5. We choose which years to present in the table based in part on data availability. Where possible, we choose cyclical peaks (years of low unemployment). It may be useful to note that our data here do not match earlier versions of this research (for example, see Table 1 in Bivens and Kandra 2023). While there are many reasons the data vary from year to year—primarily changes in the list of top 350 public firms by sales—another difference is that we are now using a chained Consumer Price Index to measure inflation because it better captures consumers’ ability to substitute away from goods and services with relatively faster price growth.

6. A better comparison would be to the low-unemployment year of 1979, but those data are not available.

7. There are a limited number of firms, which existed only for certain years between 1992 and 1996, for which a North American Industry Classification System (NAICS) value is unassigned. This makes it impossible to identify the pay of the workers in the firm’s key industry. These firms are therefore not included in the calculation of the CEO-to-worker compensation ratio.

8. As noted earlier, it may seem counterintuitive that the two ratios for 2000 are different from each other when the average CEO compensation is the same. It is important to understand that (as described later in this report) we do not create the ratio from the averages; rather we construct a ratio for each firm, and then average the ratios across firms.

9. The managerial power view asserts that CEOs have excessive, noncompetitive influence over the compensation packages they receive. Rent-seeking behavior is the practice of manipulating systems to obtain more than one’s fair share of wealth—that is, finding ways to increase one’s own gains without actually increasing the productive value one contributes to an organization or the economy.

10. A one-point rise in the ratio is the equivalent of the average CEO earning an additional amount equal to that of the average earnings of someone in the top 0.1%.

11. This follows from the fact that from 1979 to 2022, annual earnings for the bottom 90% rose by 32.9%, while the average growth across all earners was 54.3% (Gould and Kandra 2023).

Acknowledgments

The authors thank the Stephen M. Silberstein Foundation for its generous support of this research. Steven Balsam has provided useful advice on data construction and interpretation over the years. He is an accounting professor at Temple University and author of Executive Compensation: An Introduction to Practice and Theory (2007) and Equity Compensation: Motivations and Implications (2013). Steven Clifford, author of The CEO Pay Machine: How It Trashes America and How to Stop It (2017), has also provided technical advice. Clifford served as CEO for King Broadcasting Company from 1987 to 1992 and National Mobile Television from 1992 to 2000 and has been a director of 13 public and private companies. The authors also wish to acknowledge Larry Mishel, former EPI president and economist, who was valuable in setting the foundation for EPI’s work on CEO pay.

References

Baker, Dean, Josh Bivens, and Jessica Schieder. 2019. Reining in CEO Compensation and Curbing the Rise of Inequality. Economic Policy Institute, June 2019.

Bebchuk, Lucian, and Jesse Fried. 2004. Pay Without Performance: The Unfulfilled Promise of Executive Remuneration. Cambridge, Mass.: Harvard Univ. Press.

Bivens, Josh, and Lawrence Mishel. 2013. “The Pay of Corporate Executives and Financial Professionals as Evidence of Rents in Top 1 Percent Incomes.” Economic Policy Institute Working Paper no. 296, June 2013.

Bivens, Josh, and Jori Kandra. 2023. CEO Pay Slightly Declined in 2022: But It Has Soared 1,209.2% Since 1978 Compared With a 15.3% Rise in Typical Workers’ Pay. Economic Policy Institute, September 2023.

Bureau of Economic Analysis (BEA). Various years. National Income and Product Accounts (NIPA) Tables [online data tables]. Tables 6.2C, 6.2D, 6.3C, and 6.3D.

Bureau of Labor Statistics (BLS). Various years. Employment, Hours, and Earnings—National [database]. In Current Employment Statistics [public data series].

Clifford, Steven. 2017. The CEO Pay Machine: How It Trashes America and How to Stop It. New York: Penguin Random House.

Compustat. Various years. ExecuComp [commercial database].

Economic Policy Institute (EPI). 2024. “The Productivity–Pay Gap.” Economic Policy Institute website, August 2024.

Federal Reserve Bank of St. Louis. Various years. Federal Reserve Economic Data (FRED) [database].

Gould, Elise. 2020. “The Labor Market Continues to Improve in 2019 as Women Surpass Men in Payroll Employment, but Wage Growth Slows.” Working Economics Blog (Economic Policy Institute), January 10, 2020.

Gould, Elise, and Jori Kandra. 2023. “Wage Inequality Fell in 2022 Because Stock Market Declines Brought Down Pay of the Highest Earners” Working Economics Blog (Economic Policy Institute), December 11, 2023.

Kaplan, Steven N. 2012a. “Executive Compensation and Corporate Governance in the US: Perceptions, Facts, and Challenges.” Martin Feldstein Lecture, National Bureau of Economic Research. Filmed July 10, 2012, in Washington, D.C.

Kaplan, Steven N. 2012b. “Executive Compensation and Corporate Governance in the US: Perceptions, Facts and Challenges.” National Bureau of Economic Research Working Paper no. 18395, September 2012.

Mishel, Lawrence and Jori Kandra. 2020. CEO Compensation Surged 14% in 2019 to $21.3 Million: CEOs Now Earn 320 Times as Much as a Typical Worker. Economic Policy Institute, August 2020.

Sabadish, Natalie, and Lawrence Mishel. 2013. “Methodology for Measuring CEO Compensation and the Ratio of CEO-to-Worker Compensation, 2012 Data Update.” Economic Policy Institute Working Paper no. 298, June 2013.

Securities and Exchange Commission (SEC). 2015. “SEC Adopts Rule for Pay Ratio Disclosure: Rule Implements Dodd-Frank Mandate While Providing Companies with Flexibility to Calculate Pay Ratio” (press release). August 5, 2015.