Media clips

-

At this stage in the recovery —f ive years after the U.S. officially emerged from recession, labor economists would like to see the “quits rate” rise. It’s a measure of the percentage of people voluntarily leaving their employment — rather than being laid off or having a contract end. Workers might leave a job if they’ve been recruited for another one, or even to look for another job without having one already lined up. Or, they might quit to go back to school, or retire, or take a break from work altogether.

“When the economy is strong, people are more likely to be able to quit the job they’re in,” says labor economist Heidi Shierholz at the Economic Policy Institute, “to take another job that has better opportunities for wage growth and advancement, perhaps it better matches their skills and interests.”

Since plummeting at the start of the Great Recession, the quits rate has been gradually rising. But (at 1.8 percent in April 2014, the most recent month for Bureau of Labor Statistics reporting), the quits rate is still nearly 20 percent below its pre-recession level, says Shierholz, and nowhere near what would be expected in a robust economy with plenty of job opportunities.

Marketplace June 30, 2014 -

Ikea had this very notion in mind when it announced that it would raise the minimum wage of its employees. The hourly wage for each store will be based on the cost of living in that particular area, ranging from $8.69 to $13.22.

Because most workers’ wages are lower in states where prices are relatively low, a $10.10 minimum wage will tend to reach a lot more workers in Alabama than in Connecticut. According to an analysis by David Cooper at the Economic Policy Institute, the proposed federal increase would lift the pay of 24 percent of Alabama’s work force, but only 14 percent of Connecticut’s.

Some states and cities have already taken this matter into their own hands, setting their own minimum wages above the federal level to account for price and wage differences. (They have also done this because the federal minimum wage has become a political football that is often fumbled.)

New York Times June 30, 2014 -

Our current brand of capitalism is an ersatz capitalism. For proof of this go back to our response to the Great Recession, where we socialized losses, even as we privatized gains. Perfect competition should drive profits to zero, at least theoretically, but we have monopolies and oligopolies making persistently high profits. C.E.O.s enjoy incomes that are on average 295 times that of the typical worker, a much higher ratio than in the past, without any evidence of a proportionate increase in productivity.

If it is not the inexorable laws of economics that have led to America’s great divide, what is it? The straightforward answer: our policies and our politics. People get tired of hearing about Scandinavian success stories, but the fact of the matter is that Sweden, Finland and Norway have all succeeded in having about as much or faster growth in per capita incomes than the United States and with far greater equality.

New York Times June 30, 2014 -

As Danny Vinik points out, compensation hasn’t risen with productivity for over 40 years. You can see that in the chart below from the Economic Policy Institute. Since 1973, inflation-adjusted wages and benefits have barely increased for most workers, despite increasing productivity.

This is two-card monte, because we’re still waiting for the last one to trickle down. Now, you start by saying that we shouldn’t tax the rich too much, because they’re smarter than everybody else and deserve their wealth. Never mind, as Noah Smith points out, that nobody “deserves” the brains they inherit. Or that, when it comes to IQ, we shouldn’t put too much weight on nature over nurture, since we know, for example, that growing up in poverty can hurt children’s neural development. No, then you admit that it doesn’t matter whether they deserve their money or not. That we still shouldn’t tax the rich too much even if they are layabout heirs. That’s because we need their savings to fund the investments today that will make us all more productive — and hence, better paid — tomorrow.The Washington Post June 27, 2014 -

Indeed, Detroit is the fifth most affordable city in the U.S. for real estate, according to HSH.com, a mortgage-information firm. Residents only need to earn $32,250 a year for a median-priced home — making Detroit more expensive than only Cleveland ($29,788), Pittsburgh ($30,177), St. Louis ($31,275) and Cincinnati ($31,850). (San Francisco was the least affordable; median-price-home buyers need to earn $137,129 a year there.) More than 80% of homes for sale in Detroit are within reach of the middle class, compared with only 20% in New York and Los Angeles and 14% in San Francisco, according to real-estate website Trulia.

It’s also possible to live large in Detroit. “The duplex house I lived in 35 years ago on Detroit’s east side is still a beauty,” says Ross Eisenbrey, vice president of the Economic Policy Institute and a resident of Washington, D.C. He recently revisited it: The home has two units, each with leaded-glass windows, fireplace, Florida room, walk-in pantry, two bedrooms and kitchen. It sold for less than $50,000 two years ago. The lot next door can be bought for $1,000. “Once Detroit gets through the bankruptcy, restores city services, and makes progress on job creation, it will be an amazing value,” he adds.

Wall Street Journal June 27, 2014 -

Also, the evidence doesn’t entirely support the idea that policies that encourage businesses to invest more will actually help the average worker. This chart from the Economic Policy Institute shows how worker productivity–which increases when firms invest in equipment that makes workers efficient–has diverged from median pay.

As you can see, over the past 30 years, the growth in productivity and wages have decoupled, giving the middle class voter much less reason to care about whether the wealthy are encouraged to invest in their businesses through the tax code.

Fortune June 24, 2014 -

It’s not until the final three paragraphs that Mankiw explains his economic theory for why inherited wealth is good for the economy. Allowing parents to bequest wealth to their kids, he argues, incentivizes them to save. Those savings are then put to productive use. “Because capital is subject to diminishing returns, an increase in its supply causes each unit of capital to earn less,” he writes. “And because increased capital raises labor productivity, workers enjoy higher wages.” This could be a legitimate argument if workers had actually been reaping the reward from increased labor productivity. But as a report from the Economic Policy Institute shows, workers have seen their compensation barely rise over the past 40 years, despite significant gains in productivity:

The New Republic June 24, 2014 -

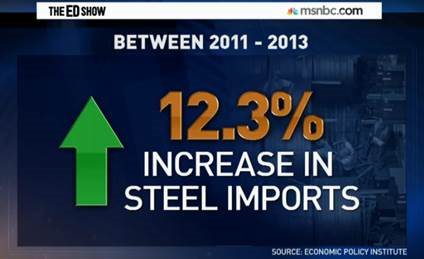

The Ed Show June 24, 2014

The Ed Show June 24, 2014 -

MSNBC June 24, 2014

MSNBC June 24, 2014 -

A separate paper, from left-leaning economist Dean Baker, argues that the trade deficit is a significant impediment to full employment. U.S. imports exceeded exports by $500 billion in 2013—that is, $500 billion of American demand for goods and services supported jobs overseas. In response, Baker proposes lowering the value of the dollar and cracking down on currency manipulators like China who artificially lower the value of their currency so that their goods and services are cheaper, boosting exports. Yet, trade policy is not an exciting or accessible issue to most voters. A candidate could include it as part of their economic platform, but it cannot form the backbone of it.

Bernstein and Larry Mishel, the president of the Economic Policy Institute, have both proposed a monetary policy regime that prioritizes low unemployment along with low inflation. Given the Federal Reserve’s independence from the federal government, though, it’s hard to imagine how better monetary policy could become a focal point of a campaign, as it hardly energizes voters. “You are basically getting at the fundamental problem for Democrats in terms of their economic agenda, in terms of the relationship between what they can run on and what they can actually do,” Teixeira said. “The public is not Keynesians or anything close to it. They don’t understand the relationship between spending, debt and growth. And, therefore, it’s the hardest sell.” Republicans, as the minority party, can simply promise a change from the Democratic agenda, regardless of voters’ understanding of their actual economic proposals.

New Republic June 24, 2014