Nominating Kevin Warsh as Fed Chair would be the latest way Trump reneged on promises to put workers’ interests over financial elites

A consistent drumbeat in Donald Trump’s campaign for the presidency was a promise that he would stand up for the American working class against financial elites who had rigged policy to enrich themselves, a message that clearly resonated with some voters. He has reneged on this commitment in virtually every area of public policy, including providing better health care coverage than Obamacare, crafting better trade agreements, making sure tax cuts go to the middle class, and standing up for workers’ rights at work.

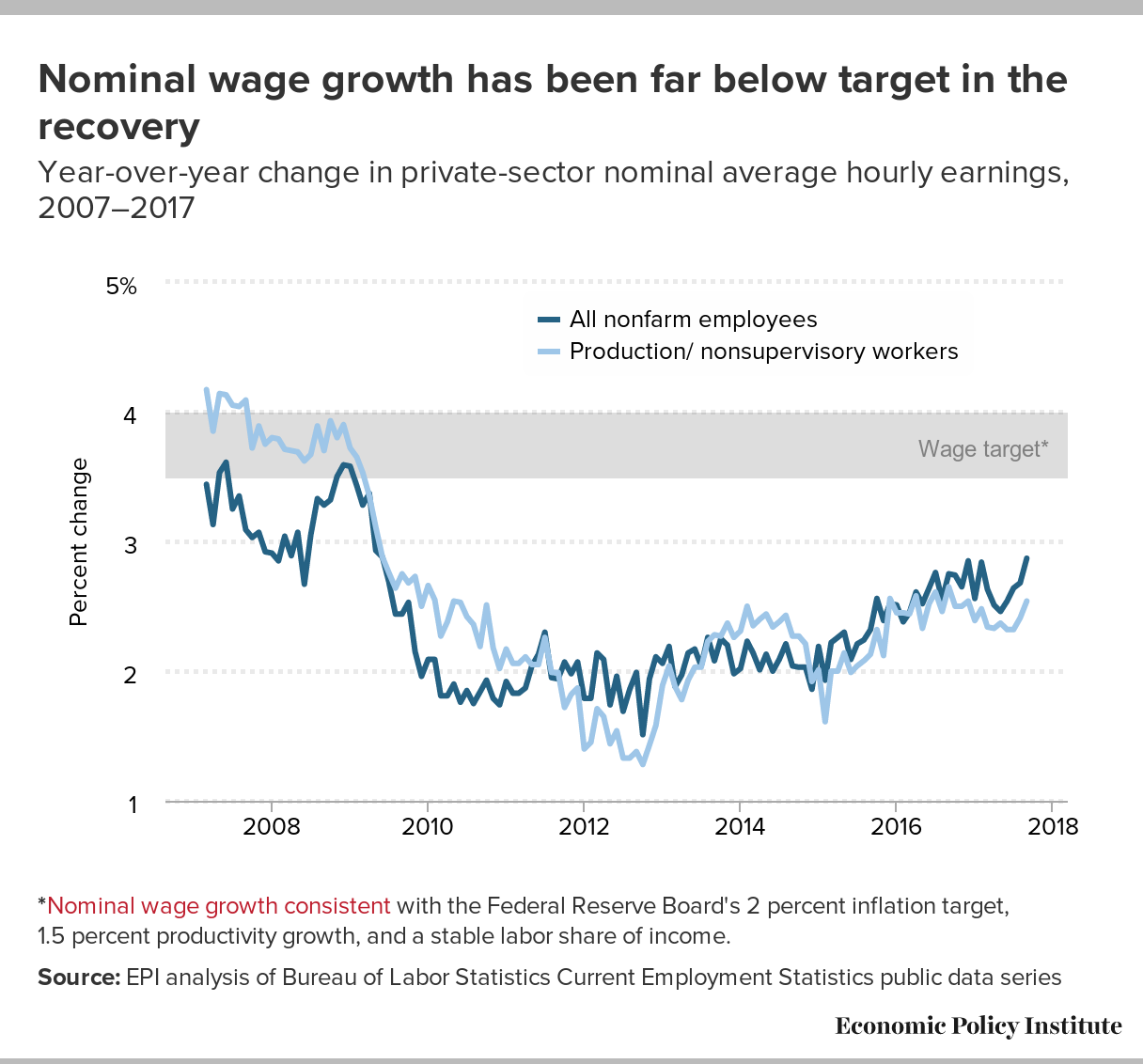

This month, workers who supported Trump may see another betrayal. It has been reported that Trump may pick Kevin Warsh, who married into a billionaire family, to replace Janet Yellen as the next Chair of the Federal Reserve Board of Governors (BOG). Decisions made by the Fed’s BOG are extraordinarily important for American workers. In recent years, pressure has built for the Fed to begin applying the brake to America’s economic recovery by raising interest rates. The rationale for this is that the Fed must slow growth to tamp down inflationary pressures. Warsh has consistently been on the side advocating for slowing growth to fight inflation. But these inflationary pressures appear nowhere in either wage or price data. And if the Fed hits the brake prematurely, millions of Americans could lose opportunities to work, and tens of millions could see smaller wage increases.

{kind=link}

{kind=link}

One underappreciated aspect of raising interest rates is that they will put upward pressure on the value of the U.S. dollar, and this stronger dollar will make U.S. exports less competitive on world markets while making foreign imports cheaper to American consumers. This will in turn lead to rising trade deficits which stunt growth in manufacturing employment. Warsh knows about this argument, but he just doesn’t really care.

“I would say that the academy’s view, the broad view of folks at the IMF and economics departments at elite universities, is that if only the dollar were weaker, then somehow we’d be getting this improvement in GDP arithmetic, we’d have an improvement in exports and we’d be getting much closer to trend. That’s not a view I share. My own views are that having a stable currency, now more than ever, provides huge advantages to the U.S. The U.S. with the world’s reserve currency is a privilege, but it is a privilege that we can’t just look to history to remind us of; it’s a privilege we have to earn and continually re-earn. And so it does strike me that those that think that dollar weakness, made possible by QE as one channel for QE, is the way to achieve these vaunted objectives are going to be sorely disappointed.”

The effect of a high dollar in worsening the trade deficit is not just something that people at the IMF and in elite universities say; it is well-establishedin the data. Warsh doesn’t offer any evidence to counter the widely accepted view that a high dollar leads to a larger trade deficit, he just says that he doesn’t like it.

This blithe waving-away of clear evidence that a rising dollar will lead to larger trade deficits and displace American manufacturing jobs is par for the course when it comes to Warsh’s views of globalization. He is an ardent proponent of trade agreements that expose American workers to fierce global competition but provide even greater protection for corporate profits, protections that come at the expense of policymaking autonomy and democratic accountability in the poorer trading partners of the United States. As a Fed governor, he proclaimed fhat the Fed had a role in weighing in to support trade deals like NAFTA and the Trans-Pacific Partnership, departing from the general view that the Fed should restrict its scope to issues directly related to the conduct of monetary policy.

A Warsh nomination for Fed chair would be a perfect example of how the financial sector capture of the Federal Reserve has hamstrung the economic leverage and bargaining power of low- and middle-wage workers. Finance hates inflation and doesn’t especially care if the unemployment rate is unnecessarily high. As a result, the Fed has for decades greatly overweighted its mandate to avoid above-target inflation while underweighting its mandate to pursue maximum employment. Part of the fallout of this frequently too-tight stance of monetary policy has been chronic trade deficits which have cost the country millions of manufacturing jobs. And while growing evidence shows that America’s stance towards globalization in recent decades has privileged the interests of corporations over typical workers, Warsh wants the Fed to be an advocate for doubling-down on this failed approach.

If Trump was serious about unrigging the rules of the American economy and globalization to help American workers, Warsh would not be in the running to be Fed chair. He both lacks the stature and the competence for the position. The clear choice is to re-appoint Janet Yellen, a chair with a solid track record as Trump himself has repeatedly acknowledged.

This blog post was originally published by the Center for Economic and Policy Research.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.