The Federal Reserve, Full Employment, and Financial Stability

The Federal Reserve, even after recent announced nominees take their jobs, will have two vacant slots on the seven-member Board of Governors. For a number of reasons, it even more vital than ever that these next two nominees be committed to using all the tools at their disposal (including the new ones provided by Dodd-Frank) to (1) generate genuine full employment in the American labor market and (2) rein in financial sector excesses that threaten economic growth and stability.

Targeting full-employment

Since roughly the end of 2008, a large majority of monetary policy observers have agreed that the Fed should focus entirely on boosting economic activity and employment, and not worry at all about inflationary pressures.

This is not the normal state of the world. Normally, it’s thought that the Fed must walk a narrow path between providing support to economic activity and employment, but not generating such an excess of aggregate demand that the economy overheats and unleashes inflation. But the extreme economic weakness of the Great Recession crushed inflationary pressures and led to a cratering of economic activity and employment. Hence, it was correctly recognized that this delicate balancing act wasn’t necessary and that attention should instead be laser-focused simply on jumpstarting economic growth.

Now, this large majority for aggressive action in boosting growth and employment looks to be fracturing, and worries about inflation and recommendations that the Fed stop its single-minded focus on generating a full recovery are surfacing.

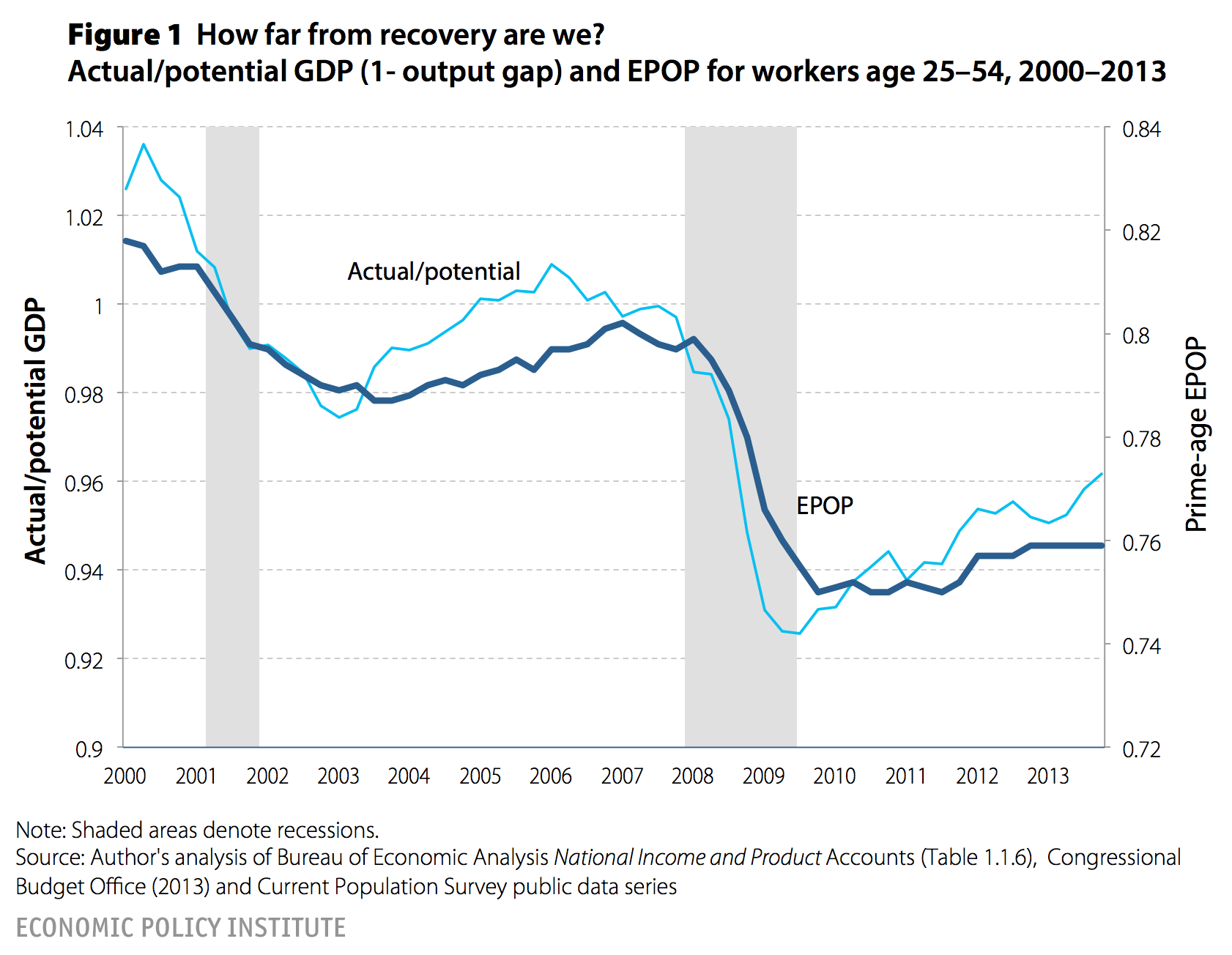

These are odd arguments to be making with the unemployment rate still matching the highest peak it ever reached in the 2001-03 recession and ensuing jobless recovery, especially considering that the headline unemployment rate has been driven down largely by the 6 million potential workers who are not actively searching for work but who would very likely join the labor force should job opportunities become less scarce. In essence, the arguments for a Fed “exit” from extraordinary efforts to boost recovery hinge on claims that very low rates of employment and very high rates of unused productive capacity relative to historic norms are not actually signs that the economy is operating below potential, because the resources idled by the Great Recession cannot be re-mobilized and should be just be considered gone forever from productive life. Importantly, however, this pessimistic argument has not been bolstered by any evidence showing that wages and prices are rising atypically fast. Indeed, the key measure of inflation tracked by the Fed has actually been pretty steadily decelerating in recent years—which is normally a sure sign that there is indeed lots of productive slack in the economy.

{kind=link}

So far, Fed Chair Janet Yellen has been steadfast in insisting that actual inflationary pressures in the data need to be observed before a case for Federal Reserve tightening will be entertained, and has managed to keep a large majority in line with her views on the Federal Open Market Committee (FOMC). But as I mentioned, there are two vacancies on the seven-member Board of Governors that vote in the FOMC (five regional Federal Reserve Bank presidents also vote in the FOMC, for a total of 12 voting members). Given that the economic recovery remains fragile, that fiscal policy has been a consistent drag on growth in recent years, and that the Fed will be the most influential policymaking body determining its pace going forward, it is vital that these vacancies be filled by governors determined to make a full recovery from the Great Recession their top priority, and who will not be spooked by claims of incipient inflation that just somehow have not shown up in the data.

The Fed needs to become more aggressive in pursuing full employment even after the current crisis

This tension between maximum employment and price stability is, of course, not new. It’s the tension inherent in the Fed’s “dual mandate” to pursue both of these goals. But in recent decades, the weights on the two prongs of the mandate have been far too uneven, with the pursuit of very low rates of inflation leading to tolerance of too high rates of unemployment.

Throughout much of the 1980s and early 1990s the Fed (supported by the majority of macroeconomists and other policy commenters) kept unemployment too high. What do I mean by too high? Higher than it needed to be to keep inflation in check, and hence too high to generate wage growth for workers up and down the pay scale.

This is a huge issue, and one that progressives cannot take a pass on, or assume that technocrats will solve. Too many progressive priorities—checking the rise of inequality, reducing poverty, bolstering asset building and retirement security, and allowing for economic mobility—are much, much harder to attain when the unemployment rate is 6 to 7 percent versus when it is 4 to 5 percent.

The importance of appointing governors who appreciate the centrality of full employment to Americans’ economic outcomes becomes even clearer once one considers the institutional context of how monetary policy decisions are made. Besides the seven governors, the FOMC also contains the president of the New York Federal Reserve and four voting members that are drawn on a rotating basis from the 11 remaining presidents of regional Federal Reserve banks. These regional bank presidents are in turn chosen by the commercial banks within each regional Fed’s territory. If one believes (reasonably) that representatives of the financial sector have different interests than the rest of the economy—and in particular will be more inflation-averse—then this means that the FOMC will have a standing bloc of voting members that will push it towards overweighting the benefits of low inflation. To be clear, this isn’t an ironclad law. Some recent regional bank presidents (like current chair Yellen) have, to their great credit, been the loudest voices arguing for continued action to push the economy back towards full-employment in recent years. But other regional presidents have been the loudest voices calling for the Fed to scale back its aid to recovery and worry instead about phantom inflation.

This institutional structure of the Fed and the influence of commercial banks reflects a misguided fear that has been influential in monetary policy circles for decades now: that the key danger to be guarded against in monetary policy is irresponsible populism. A substantial minority of macroeconomists in the 80s and early 90s, for example, marshalled data arguing that the unemployment rate could indeed go below 6 percent—and significantly below 6 percent—without sparking inflation, and that the Fed should at least be probing lower rates. They were largely ignored; and yet they were proved correct. When, to his credit, Alan Greenspan pushed to hold off on tightening in the late 1990s as the economy breached ex ante estimates of the minimum rate of unemployment consistent with stable inflation (the horribly named NAIRU, or non-accelerating inflation rate of unemployment), the economy delivered the first across-the-board wage increases to American workers in a generation and delivered no rise in inflation.

It is bankers, not workers, who really need the punchbowl taken away

An old maxim has it that the Fed’s job is to “take the punchbowl away just as the party gets started”—i.e., raise interest rates before any sign of economic overheating begins. The theory was that inflation is a terribly powerful force always trying to find a way into the economy, and the Fed could not afford to give it any opening by allowing unemployment to fall low enough for workers to have some real bargaining power or to demand wage increases, because this would set off wage-price spirals that would be costly to rein in. The experience of the late 1990s and dozens of studies belie this—inflation rises slowly, not irresistibly, as economies tighten from very weak conditions, and there is plenty of time to tamp down demand-pull inflation after it begins.

But this maxim about the punchbowl does have some truth to it, and in recent decades the Fed has clearly left the punchbowl out way too long, causing ugly hangovers all around. But this punchbowl profligacy wasn’t tolerating too-low unemployment or excessive wage-growth—it was tolerating obvious asset market bubbles and largely allowing the financial sector to self-regulate (or choose not to self-regulate). Until the Great Recession, the prevailing theory of the Fed and other financial market regulators was that bubbles were too hard for mere mortals to spot, and the their fallout could always be cleaned up after the fact by an extended period of low short-term interest rates.

New Fed governors should reject both parts of this argument. First, potential bubbles should be identified when asset market prices move far out of line of historical experience and fundamentals in markets large enough to have macroeconomic consequences, and then these bubbles should be addressed by the Fed. (A key thing to note is that examples of “false positives”—asset price booms that looked like bubbles but never popped and would have been disastrous to try to deflate—are very hard to identify.) Second, we now know for sure that while macroeconomic policymakers—both fiscal and monetary—may have the economic tools to neutralize damage from recovery, the U.S. political system cannot be relied upon to deploy them. To be concrete about this – the U.S. economy needed about three times as much fiscal stimulus to achieve full recovery as it got, simply because Republicans in Congress were able to greatly curtail efforts at fiscal stimulus after the American Recovery and Reinvestment Act.

Full employment plus financial stability requires a bigger tool kit

People sometimes claim that there’s a conflict here between our first criteria for a progressive Fed governor (being extremely hawkish in targeting low unemployment) and the second (not allowing bubbles to inflate to damaging sizes). That is, supporting economic activity and employment often means keeping short-term interest rates low, and some have argued that low short-term interest rates can help inflate bubbles. In fact, some have argued that low interest rates following the 2001-03 recession and jobless recovery, which were meant to support activity and employment, were a key cause of the housing bubble.

Aside from the fact that low interest rates were at best a contributing factor, not a fundamental cause, of the inflating housing bubble, this episode doesn’t tell us that there is an irreconcilable conflict between the goals of full employment and financial stability. What it tells us instead is that the Federal Reserve needs to use a much larger set of tools to manage the economy than just short-term interest rates. Think regulatory policy—say that the Fed worked with Fannie and Freddie to decrease LTV requirements during the housing bubble. Or say that in the future the Fed uses asset-based reserve requirements to raise effective interest rates precisely on asset classes that are displaying bubbly behavior.

Or, say that the Fed just engages in jawboning. The key argument against the effectiveness of this is Alan Greenspan’s half-hearted attempts in 1996 to rein in the stock market by labelling recent price increases as possibly driven by “irrational exuberance,” but this is a bad example. Price-to-earnings ratios in 1996 were actually not historically out of line—that speech really should have been given in 1998, 1999, or 2000. Moreover, asset bubbles get momentum, and it takes more than a single speech delivered at a time when the fundamentals were slightly mixed to push back on this momentum. But, a prolonged campaign of alerting the public to the fact that prices were hugely out of line with historical fundamentals, followed by concrete action (margin requirements, lowering LTV ratios, ABBRS…)? We’ve never tried this, and, it’s costless.

Help wanted: evidence-based central bankers

The Federal Reserve is the single most-powerful economic policymaking institution in the United States. The coming years will see heated debates over the proper path the Fed should take. We need to ensure that the Board of Governors are filled by people who see their constituency as American households and who are practical and evidence-based. In decades past, the Federal Reserve has been too hard on American workers and too soft on Wall Street. We need to reverse this.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.