The top charts of 2016: 13 charts that show the difference between the economy we have now and the economy we could have

The election of Donald Trump alerted many to what should have been obvious long ago: the U.S. economy has failed to deliver the goods to the vast majority of American families for decades. In the context of Trump’s election, this economic failure was often characterized as being unique to white working-class voters in the upper Midwest. But this is wrong. Income growth has been sluggish, and hourly wage growth near zero, for low- and middle-income families across the board. The fact is, our economy has generated enough income in recent decades to deliver very substantial wage gains for all workers—men and women, people of color and whites. Our economy has the capacity to provide not just decent wages but labor protections that support strong families and policies that provide security in retirement. These charts show the gap between what is and what could be. (For policies to close the gaps, see EPI’s Real agenda for working people.)

{kind=link}

{kind=link}

The minimum wage would be much higher if it had kept up with a growing economy: The inflation-adjusted minimum wage, and hypothetical minimum wage values if it had grown with average wages and productivity since 1968

| Actual minimum wage (2016$) | Minimum wage if it had grown with average wages | Minimum wage if it had grown with productivity | |

|---|---|---|---|

| 1938 | $ 3.67 | ||

| 1939 | $ 4.46 | ||

| 1940 | $ 4.43 | ||

| 1941 | $ 4.22 | ||

| 1942 | $ 3.81 | ||

| 1943 | $ 3.59 | ||

| 1944 | $ 3.53 | ||

| 1945 | $ 4.60 | ||

| 1946 | $ 4.24 | ||

| 1947 | $ 3.71 | ||

| 1948 | $ 3.46 | $5.43 | |

| 1949 | $ 3.51 | $5.52 | |

| 1950 | $ 6.49 | $5.94 | |

| 1951 | $ 6.02 | $6.11 | |

| 1952 | $ 5.91 | $6.28 | |

| 1953 | $ 5.86 | $6.50 | |

| 1954 | $ 5.82 | $6.61 | |

| 1955 | $ 5.84 | $6.87 | |

| 1956 | $ 7.67 | $6.88 | |

| 1957 | $ 7.43 | $7.07 | |

| 1958 | $ 7.22 | $7.22 | |

| 1959 | $ 7.17 | $7.48 | |

| 1960 | $ 7.05 | $7.61 | |

| 1961 | $ 8.03 | $7.84 | |

| 1962 | $ 7.95 | $8.14 | |

| 1963 | $ 8.52 | $8.42 | |

| 1964 | $ 8.41 | $8.69 | |

| 1965 | $ 8.28 | $8.96 | |

| 1966 | $ 8.05 | $9.24 | |

| 1967 | $ 8.75 | $9.35 | |

| 1968 | $ 9.63 | $ 9.63 | $9.63 |

| 1969 | $ 9.21 | $ 9.80 | $9.67 |

| 1970 | $ 8.79 | $ 9.90 | $9.80 |

| 1971 | $ 8.42 | $ 10.10 | $10.17 |

| 1972 | $ 8.17 | $ 10.55 | $10.44 |

| 1973 | $ 7.69 | $ 10.53 | $10.69 |

| 1974 | $ 8.74 | $ 10.27 | $10.52 |

| 1975 | $ 8.48 | $ 10.12 | $10.76 |

| 1976 | $ 8.78 | $ 10.25 | $11.06 |

| 1977 | $ 8.26 | $ 10.35 | $11.18 |

| 1978 | $ 8.91 | $ 10.47 | $11.29 |

| 1979 | $ 8.90 | $ 10.31 | $11.31 |

| 1980 | $ 8.56 | $ 10.01 | $11.23 |

| 1981 | $ 8.45 | $ 9.93 | $11.47 |

| 1982 | $ 7.96 | $ 9.91 | $11.30 |

| 1983 | $ 7.64 | $ 9.91 | $11.64 |

| 1984 | $ 7.34 | $ 9.85 | $11.94 |

| 1985 | $ 7.09 | $ 9.80 | $12.14 |

| 1986 | $ 6.97 | $ 9.83 | $12.39 |

| 1987 | $ 6.74 | $ 9.74 | $12.45 |

| 1988 | $ 6.50 | $ 9.70 | $12.60 |

| 1989 | $ 6.23 | $ 9.66 | $12.70 |

| 1990 | $ 6.73 | $ 9.58 | $12.88 |

| 1991 | $ 7.27 | $ 9.53 | $12.98 |

| 1992 | $ 7.09 | $ 9.52 | $13.45 |

| 1993 | $ 6.92 | $ 9.53 | $13.50 |

| 1994 | $ 6.78 | $ 9.58 | $13.63 |

| 1995 | $ 6.62 | $ 9.61 | $13.63 |

| 1996 | $ 7.20 | $ 9.67 | $13.96 |

| 1997 | $ 7.64 | $ 9.83 | $14.16 |

| 1998 | $ 7.54 | $ 10.09 | $14.44 |

| 1999 | $ 7.38 | $ 10.24 | $14.79 |

| 2000 | $ 7.14 | $ 10.29 | $15.13 |

| 2001 | $ 6.95 | $ 10.39 | $15.37 |

| 2002 | $ 6.84 | $ 10.52 | $15.80 |

| 2003 | $ 6.69 | $ 10.57 | $16.31 |

| 2004 | $ 6.51 | $ 10.51 | $16.75 |

| 2005 | $ 6.30 | $ 10.44 | $17.04 |

| 2006 | $ 6.10 | $ 10.51 | $17.14 |

| 2007 | $ 6.74 | $ 10.62 | $17.27 |

| 2008 | $ 7.26 | $ 10.62 | $17.29 |

| 2009 | $8.07 | $ 10.97 | $17.65 |

| 2010 | $ 7.94 | $ 11.05 | $18.17 |

| 2011 | $ 7.70 | $ 10.93 | $18.19 |

| 2012 | $ 7.54 | $ 10.87 | $18.29 |

| 2013 | $ 7.43 | $ 10.94 | $18.31 |

| 2014 | $ 7.31 | $ 11.01 | $18.42 |

| 2015 | $ 7.30 | $ 11.23 | $18.48 |

| 2016 | $7.25 | $11.35 | $18.85 |

Note: Growth in average wages measures average wages of production/nonsupervisory workers in the private sector.

Source: Adapted from David Cooper, The federal minimum wage has been eroded by decades of inaction, Economic Policy Institute Snapshot, July 25, 2016

The federal minimum wage is meant to ensure a fair wage for the nation’s lowest-paid workers. But it hasn’t done that since 1968. Since the inception of the federal minimum wage in 1938, Congress has periodically raised it, ostensibly so that its real (inflation-adjusted) value would reflect changing economic circumstances. Before 1968, the real value of the federal minimum wage grew at roughly the same pace as the growth in labor productivity—i.e., the rate at which the average worker can produce income from each hour of work. This makes sense: if the economy as a whole can produce more income per hour of work, it means there is capacity for wages across the distribution to grow at a similar rate. But after 1968, when the real value of the minimum wage in today’s dollars was $9.63, the minimum wage stopped rising at the same pace as productivity. As the top line in the graph shows, had the minimum wage kept pace with rising productivity, it would be nearly $19 per hour today. Not $7.25.

This is only one way in which policymakers have failed to ensure that the lowest-paid Americans get their fair share of economic growth and improving labor productivity. As the middle line in the figure shows, if, since 1968, the minimum wage had even just been raised at the same growth rate as average hourly wages of typical U.S. workers, the minimum wage would be $11.35 today. To sum up, minimum wage workers are falling behind not only productivity growth but typical worker pay growth and pay growth of their 1968 counterparts! And as the next chart shows, typical workers (measured here as the nonsupervisory production workers who constitute roughly 80 percent of all private-sector U.S. workers) themselves are lagging behind highly paid supervisors and executives when it comes to claiming a share of economic growth.

CEOs make 276 times more than typical workers: CEO-to-worker compensation ratio, 1965–2015

| Year | CEO-to-worker compensation ratio |

|---|---|

| 1965/01/01 | 20.0 |

| 1966/01/01 | 21.2 |

| 1967/01/01 | 22.4 |

| 1968/01/01 | 23.7 |

| 1969/01/01 | 23.4 |

| 1970/01/01 | 23.2 |

| 1971/01/01 | 22.9 |

| 1972/01/01 | 22.6 |

| 1973/01/01 | 22.3 |

| 1974/01/01 | 23.7 |

| 1975/01/01 | 25.1 |

| 1976/01/01 | 26.6 |

| 1977/01/01 | 28.2 |

| 1978/01/01 | 29.9 |

| 1979/01/01 | 31.8 |

| 1980/01/01 | 33.8 |

| 1981/01/01 | 35.9 |

| 1982/01/01 | 38.2 |

| 1983/01/01 | 40.6 |

| 1984/01/01 | 43.2 |

| 1985/01/01 | 45.9 |

| 1986/01/01 | 48.9 |

| 1987/01/01 | 51.9 |

| 1988/01/01 | 55.2 |

| 1989/01/01 | 58.7 |

| 1990/01/01 | 71.2 |

| 1991/01/01 | 86.2 |

| 1992/01/01 | 104.4 |

| 1993/01/01 | 111.8 |

| 1994/01/01 | 87.3 |

| 1995/01/01 | 122.6 |

| 1996/01/01 | 153.8 |

| 1997/01/01 | 233.0 |

| 1998/01/01 | 321.8 |

| 1999/01/01 | 286.7 |

| 2000/01/01 | 376.1 |

| 2001/01/01 | 214.2 |

| 2002/01/01 | 188.5 |

| 2003/01/01 | 227.5 |

| 2004/01/01 | 256.6 |

| 2005/01/01 | 308.0 |

| 2006/01/01 | 341.4 |

| 2007/01/01 | 345.3 |

| 2008/01/01 | 239.3 |

| 2009/01/01 | 195.8 |

| 2010/01/01 | 229.7 |

| 2011/01/01 | 235.5 |

| 2012/01/01 | 285.3 |

| 2013/01/01 | 303.1 |

| 2014/01/01 | 301.9 |

| 2015/01/01 | 275.6 |

Note: CEO annual compensation is computed using the “options realized” compensation series, which includes salary, bonus, restricted stock grants, options exercised, and long-term incentive payouts for CEOs at the top 350 U.S. firms ranked by sales. Typical worker compensation refers to annual compensation of the workers in the key industries of the firms in the sample.

Source: Adapted from Figure C in Lawrence Mishel and Jessica Schieder, Stock market headwinds meant less generous year for some CEOs, Economic Policy Institute Report, July 12, 2016

The compensation of the CEOs of the largest firms has grown much faster than stock prices, corporate profits, and the wages of the top 0.1 percent. But the most dramatic difference is between the compensation of CEOs and the compensation of typical workers. From 1978 to 2015, CEO compensation grew 941 percent compared with just 10 percent for the compensation of a typical worker (annual compensation of the workers in the key industries represented by the sample).

The figure illustrates the gap in pay between CEOs and employees by tracking the ratio of CEO compensation to that of the typical worker. CEOs of major U.S. companies earned 20 times more than a typical worker in 1965; this ratio grew to 59-to-1 by 1989, and then it surged in the 1990s, hitting 376-to-1 by the end of the 1990s recovery, in 2000. The two stock market crashes after 2000 reduced CEO stock-related pay and caused CEO compensation to tumble. But by 2014, the stock market had recouped all of the value it lost following the 2008 financial crisis and the CEO-to-worker compensation ratio was back to 302-to-1. A dip in the stock market and the value of associated stock options led to a decline in CEO compensation in 2015 and, correspondingly, the CEO-to-worker pay ratio fell to 276-to-1, similar to what happened in other stock market declines at the start of the new millennium and during the Great Recession. Though the CEO-to-worker compensation ratio remains below the peak values achieved earlier in the 2000s, it is far higher than it was in the previous four decades.

Boosting productivity is necessary but not sufficient for wage growth: Disconnect between productivity and a typical worker's compensation, 1948–2015

| Year | Hourly compensation | Net productivity |

|---|---|---|

| 1948 | 0.00% | 0.00% |

| 1949 | 6.25% | 1.55% |

| 1950 | 10.48% | 9.33% |

| 1951 | 11.75% | 12.35% |

| 1952 | 15.04% | 15.63% |

| 1953 | 20.84% | 19.55% |

| 1954 | 23.52% | 21.56% |

| 1955 | 28.74% | 26.46% |

| 1956 | 33.94% | 26.66% |

| 1957 | 37.14% | 30.09% |

| 1958 | 38.16% | 32.78% |

| 1959 | 42.55% | 37.64% |

| 1960 | 45.49% | 40.05% |

| 1961 | 47.99% | 44.36% |

| 1962 | 52.47% | 49.79% |

| 1963 | 55.02% | 55.01% |

| 1964 | 58.50% | 59.99% |

| 1965 | 62.46% | 64.94% |

| 1966 | 64.89% | 70.00% |

| 1967 | 66.89% | 72.05% |

| 1968 | 70.73% | 77.16% |

| 1969 | 74.66% | 77.88% |

| 1970 | 76.59% | 80.37% |

| 1971 | 82.01% | 87.10% |

| 1972 | 91.24% | 92.05% |

| 1973 | 91.29% | 96.75% |

| 1974 | 86.96% | 93.66% |

| 1975 | 86.84% | 97.92% |

| 1976 | 89.66% | 103.44% |

| 1977 | 93.13% | 105.79% |

| 1978 | 95.96% | 107.79% |

| 1979 | 93.43% | 108.14% |

| 1980 | 88.56% | 106.57% |

| 1981 | 87.59% | 111.02% |

| 1982 | 87.76% | 107.88% |

| 1983 | 88.35% | 114.13% |

| 1984 | 86.94% | 119.73% |

| 1985 | 86.31% | 123.43% |

| 1986 | 87.32% | 127.99% |

| 1987 | 84.59% | 129.12% |

| 1988 | 83.85% | 131.78% |

| 1989 | 83.70% | 133.65% |

| 1990 | 82.22% | 136.98% |

| 1991 | 81.87% | 138.89% |

| 1992 | 83.04% | 147.56% |

| 1993 | 83.38% | 148.37% |

| 1994 | 83.82% | 150.75% |

| 1995 | 82.70% | 150.86% |

| 1996 | 82.79% | 156.92% |

| 1997 | 84.80% | 160.50% |

| 1998 | 89.17% | 165.71% |

| 1999 | 91.92% | 172.08% |

| 2000 | 92.90% | 178.50% |

| 2001 | 95.56% | 182.84% |

| 2002 | 99.38% | 190.72% |

| 2003 | 101.63% | 200.17% |

| 2004 | 100.84% | 208.21% |

| 2005 | 100.05% | 213.58% |

| 2006 | 100.21% | 215.48% |

| 2007 | 101.70% | 217.70% |

| 2008 | 101.71% | 218.24% |

| 2009 | 109.69% | 224.75% |

| 2010 | 111.53% | 234.28% |

| 2011 | 109.06% | 234.67% |

| 2012 | 107.27% | 236.51% |

| 2013 | 108.32% | 237.57% |

| 2014 | 109.13% | 239.30% |

| 2015 | 112.53% | 241.08% |

Note: Data are for average hourly compensation of production/nonsupervisory workers in the private sector and net productivity of the total economy. “Net productivity” is the growth of output of goods and services minus depreciation per hour worked.

Source: Adapted from Figure K in Josh Bivens and Hunter Blair, Financing recovery and fairness by going where the money is, Economic Policy Institute Report, November 15, 2016

Source: Economic Policy Institute analysis of data from the Bureau of Economic Analysis’ National Income and Produce Accounts and the Bureau of Labor Statistics’ Consumer Price Indexes and Labor Productivity and Costs programs (see technical appendix of Understanding the Historic Divergence Between Productivity and a Typical Worker's Pay for more detailed information)

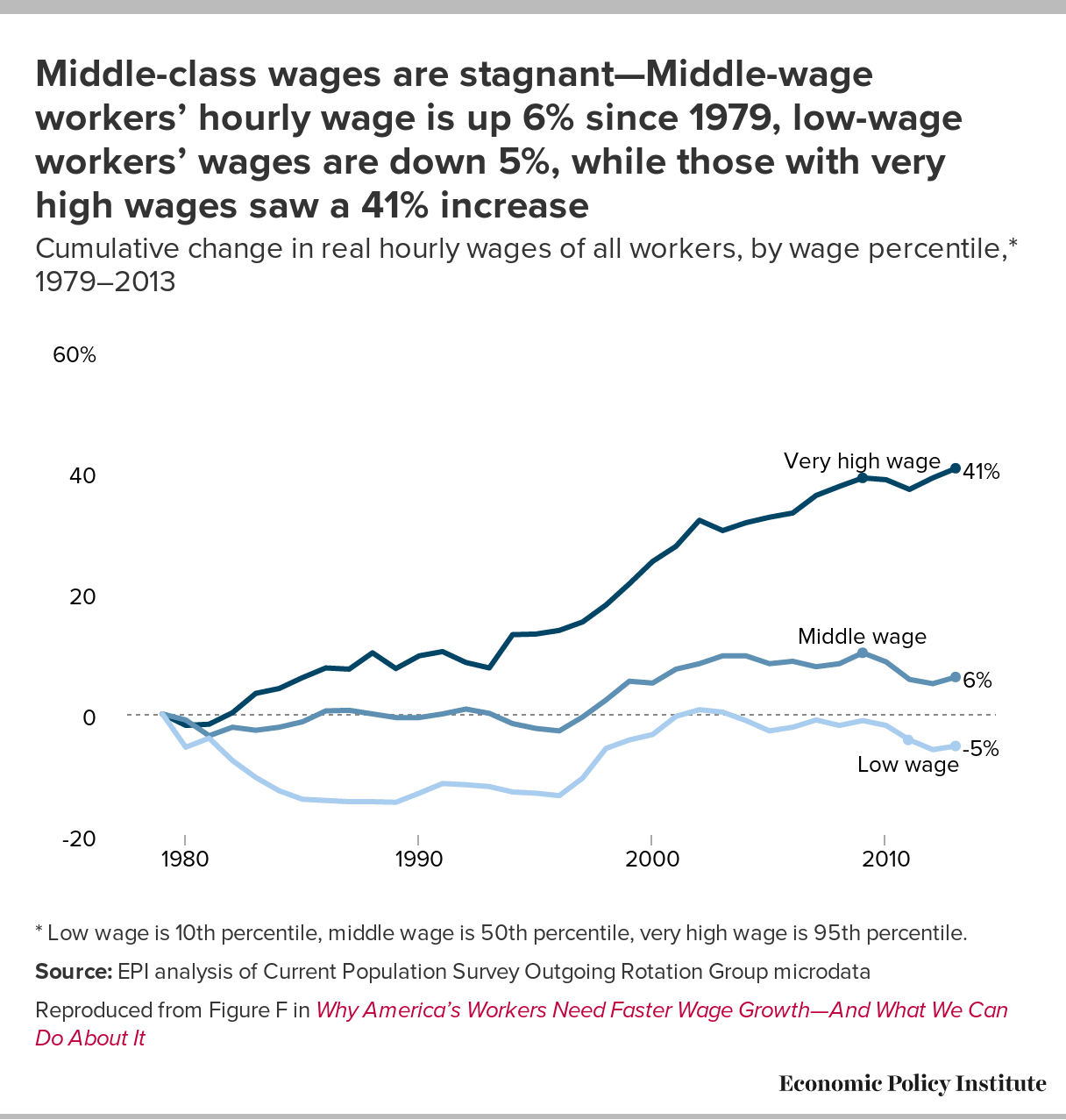

The root cause of the extraordinary rise in inequality and the near-stagnant growth of wages for typical workers over most of the past generation is the pay-productivity gap. Before the late 1970s, wages of the vast majority of workers grew in line with productivity. In the late 1970s, typical worker pay growth split from economy-wide productivity growth. Productivity is a measure of how much income is generated in an average hour of work in the economy. While productivity after 1979 grew more slowly relative to previous decades, it did grow steadily, offering the potential for broad-based wage gains. But income gains were not broad-based. In fact, average pay (wages plus benefits) for the 80 percent of the private-sector workers who are not supervisors barely budged in that time. The growing wedge between productivity and pay is the income generated by workers in the economy that has been claimed by corporate owners and managers and others at the very top of the pay scale.

Eliminating the gender and inequality wage gaps would raise women’s wages by 69%: Median hourly wages for men and women, compared with wages for all workers had they increased in tandem with productivity, 1979–2015

| Year | Wages for all workers | Men’s wages | Women’s wages | Wages for all workers had they grown in tandem with productivity |

|---|---|---|---|---|

| 1979 | $16.15 | $20.30 | $12.66 | $16.15 |

| 1980 | $16.07 | $19.98 | $12.60 | $16.03 |

| 1981 | $15.66 | $19.52 | $12.53 | $16.38 |

| 1982 | $15.75 | $19.30 | $12.61 | $16.13 |

| 1983 | $15.71 | $19.18 | $12.76 | $16.62 |

| 1984 | $15.71 | $19.15 | $12.93 | $17.05 |

| 1985 | $15.80 | $19.10 | $12.98 | $17.34 |

| 1986 | $16.27 | $19.70 | $13.26 | $17.70 |

| 1987 | $16.12 | $19.75 | $13.64 | $17.78 |

| 1988 | $16.10 | $19.23 | $13.64 | $17.99 |

| 1989 | $16.06 | $18.57 | $13.71 | $18.13 |

| 1990 | $15.85 | $18.12 | $13.62 | $18.39 |

| 1991 | $15.94 | $18.06 | $13.68 | $18.54 |

| 1992 | $15.98 | $18.10 | $13.82 | $19.21 |

| 1993 | $16.06 | $17.87 | $14.02 | $19.28 |

| 1994 | $15.80 | $17.67 | $13.98 | $19.46 |

| 1995 | $15.58 | $17.91 | $13.85 | $19.47 |

| 1996 | $15.65 | $17.93 | $13.87 | $19.94 |

| 1997 | $16.04 | $17.85 | $14.14 | $20.22 |

| 1998 | $16.49 | $18.65 | $14.54 | $20.62 |

| 1999 | $16.97 | $19.10 | $14.73 | $21.12 |

| 2000 | $16.83 | $19.20 | $15.03 | $21.61 |

| 2001 | $17.27 | $19.44 | $15.31 | $21.95 |

| 2002 | $17.27 | $19.64 | $15.72 | $22.56 |

| 2003 | $17.56 | $19.35 | $15.61 | $23.30 |

| 2004 | $17.55 | $19.17 | $15.69 | $23.92 |

| 2005 | $17.40 | $18.95 | $15.63 | $24.34 |

| 2006 | $17.51 | $18.91 | $15.58 | $24.49 |

| 2007 | $17.21 | $19.21 | $15.70 | $24.66 |

| 2008 | $17.30 | $19.06 | $15.85 | $24.70 |

| 2009 | $17.65 | $19.75 | $16.06 | $25.20 |

| 2010 | $17.40 | $19.09 | $15.92 | $25.94 |

| 2011 | $16.92 | $18.60 | $15.74 | $25.97 |

| 2012 | $16.83 | $18.59 | $15.44 | $26.12 |

| 2013 | $16.95 | $18.38 | $15.32 | $26.20 |

| 2014 | $16.90 | $18.41 | $15.14 | $26.33 |

| 2015 | 17.11 | 18.94 | 15.67 | 26.47 |

Source: Adapted from Figure B in Elise Gould, “A women’s economic agenda for the 45th U.S. president: Investing in the infrastructure to support a 21st century economy,” Working Economics (Economic Policy Institute blog), October 26, 2016. See also What is the gender pay gap and is it real?, Economic Policy Institute report, October 20, 2016

Closing the pay-productivity gap must be a part of an agenda to improve women’s economic security. Although the gap between what median men and median women are paid has narrowed (albeit too slowly) since 1979, the gap between typical workers’ compensation and economy-wide productivity growth has widened. Tackling both gaps would also raise the economic security of men. One example of why the pay-productivity gap needs to inform our thinking about progress in closing gender pay gaps is the fact that roughly a third of the progress made in closing the median gender wage gap since 1979 was due to the decline in men’s wages in an era of increasing inequality. Remedying unfairness of pay for women is necessary, but wage parity gained simply because male wages dropped is no cause for celebration.

The figure shows how high median wages for women could be if gender wage disparities had been closed between 1979 and today and if the economy had generated wage growth for all workers that matched economy-wide productivity growth. If the gender wage gap were closed and the economy’s gains broadly shared, women’s median hourly wages would be 69 percent higher today ($26.47 instead of $15.67). Notably, men’s median hourly wages would also be 40 percent higher. (To see how these differences compare for age and education cohorts, check out EPI’s new gender wage calculator.) These figures show that getting to gender pay equity is not a zero-sum game—if we also tackle inequality, typical men and women have much to gain.

Though all workers’ wages have failed to rise in tandem with productivity, black men have suffered most: Hourly median wage growth by gender, race, and ethnicity, compared with economy-wide productivity growth, 1979–2014

| Year | White men | White women | Black men | Black women | Productivity |

|---|---|---|---|---|---|

| 1979 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| 1980 | -2.1% | -0.2% | -2.0% | -1.9% | -0.8% |

| 1981 | -3.8% | -1.6% | -3.3% | 0.0% | 1.4% |

| 1982 | -3.9% | -0.6% | -7.1% | -0.8% | -0.1% |

| 1983 | -5.1% | 0.5% | -6.6% | -1.2% | 2.9% |

| 1984 | -5.5% | 1.0% | -5.9% | -1.2% | 5.6% |

| 1985 | -2.6% | 1.5% | -8.2% | 1.4% | 7.3% |

| 1986 | -2.4% | 5.4% | -4.5% | 3.0% | 9.5% |

| 1987 | -4.1% | 7.8% | -5.6% | 3.0% | 10.1% |

| 1988 | -4.5% | 8.8% | -5.0% | 4.0% | 11.4% |

| 1989 | -5.3% | 9.0% | -8.9% | 6.0% | 12.3% |

| 1990 | -7.0% | 8.9% | -9.9% | 4.8% | 13.9% |

| 1991 | -6.6% | 9.4% | -11.2% | 5.3% | 14.8% |

| 1992 | -7.2% | 10.7% | -11.8% | 5.8% | 18.9% |

| 1993 | -8.0% | 12.1% | -11.6% | 7.0% | 19.3% |

| 1994 | -9.0% | 12.0% | -11.6% | 5.2% | 20.5% |

| 1995 | -8.8% | 11.7% | -11.3% | 4.5% | 20.5% |

| 1996 | -8.5% | 13.9% | -12.4% | 4.5% | 23.4% |

| 1997 | -6.3% | 14.7% | -9.8% | 5.6% | 25.2% |

| 1998 | -3.2% | 17.7% | -6.9% | 11.2% | 27.7% |

| 1999 | -0.8% | 21.2% | -3.0% | 11.4% | 30.7% |

| 2000 | -1.1% | 21.9% | -3.4% | 16.1% | 33.8% |

| 2001 | 0.7% | 25.6% | -0.5% | 15.1% | 35.9% |

| 2002 | 0.9% | 28.4% | -0.3% | 18.0% | 39.7% |

| 2003 | 2.6% | 29.6% | -0.9% | 21.4% | 44.2% |

| 2004 | 1.8% | 29.3% | 1.0% | 22.9% | 48.1% |

| 2005 | 0.0% | 30.0% | -4.7% | 15.4% | 50.7% |

| 2006 | 0.0% | 30.0% | -1.9% | 19.6% | 51.6% |

| 2007 | 1.3% | 30.5% | -3.0% | 18.2% | 52.7% |

| 2008 | 0.0% | 29.6% | -3.1% | 16.0% | 53.0% |

| 2009 | 3.6% | 31.5% | 0.0% | 20.8% | 56.1% |

| 2010 | 1.8% | 31.6% | -1.9% | 20.2% | 60.7% |

| 2011 | -1.4% | 30.3% | -5.5% | 16.9% | 60.9% |

| 2012 | -2.2% | 29.2% | -5.9% | 14.0% | 61.7% |

| 2013 | -3.1% | 30.6% | -4.9% | 15.9% | 61.9% |

| 2014 | -3.1% | 30.2% | -7.2% | 12.8% | 62.7% |

Note: Race/ethnicity categories are mutually exclusive (i.e., white non-Hispanic, black non-Hispanic, and Hispanic any race).

Source: Adapted from Figure A in Valerie Wilson, Black workers’ wages have been harmed by both widening racial wage gaps and the widening productivity-pay gap, Economic Policy Institute Report, October 25, 2016

In the wake of Trump’s election, some commentators have focused on the economic failures afflicting white working-class men. White working-class men are suffering, but they are not the only group suffering from the chasm between what the economy can provide and what it is providing, and their loss has not translated into gains made by typical workers of other races. In fact, wage gaps between workers of different races have widened at the same time that economy-wide productivity and wages for typical workers overall have diverged. In short, what has caused sluggish wage growth for the vast majority of all workers is the rise of inequality that has redistributed income toward the very top of the income distribution.

The figure shows that between 1979 and 2015, median hourly real wage growth fell far short of productivity growth—a measure of the potential for pay increases—for men as well as for women and for both black and white workers. And white workers are not losing income to their black counterparts. Median hourly wages of black men fell 5.7 percent, compared with a 1.0 percent decline for white men. Median hourly wages of white women grew 31.6 percent, compared with 15.2 percent for black women.

What this figure does not show is that black workers already start out with a big pay disparity. In 2015, black workers overall were paid 26.2 percent less than their white peers. What has this double penalty of overall wage stagnation and regress on racial pay disparities cost black workers? Quite a lot, according to a 2016 report by Valerie Wilson. If the 1979 racial wage gap at the median had closed by 2015 and the overall median had grown with productivity (63.9 percent) between 1979 and 2015, the median black worker would be earning an hourly wage of $26.47 instead of $14.14—an increase of $12.33. That means the hourly wage of the median black worker would be an astounding 87.2 percent higher! And under this scenario, the median white worker would also receive an hourly pay increase of $7.30—the difference between $26.47 and $19.17—boosting their wages by 38.1 percent. The vast majority of workers of all races would be better off if we addressed both class and racial inequalities, with larger gains for African Americans because of the dual penalties imposed by class and race.

Drop in union membership has taken $14 to $52 out of nonunion workers’ weekly wages: Additional weekly wages that nonunion private-sector workers would earn, had the share of workers in a union (union density) remained the same as in 1979, 1979–2013 (2013 dollars)

| Year | Men | Women |

|---|---|---|

| 1979 | 0.00 | 0.00 |

| 1980 | 4.55 | 1.81 |

| 1981 | 7.34 | 2.50 |

| 1983 | 16.93 | 4.77 |

| 1984 | 22.11 | 6.18 |

| 1985 | 25.90 | 7.39 |

| 1986 | 28.29 | 8.14 |

| 1987 | 29.63 | 8.60 |

| 1988 | 31.24 | 9.19 |

| 1989 | 32.36 | 9.76 |

| 1990 | 33.57 | 10.07 |

| 1991 | 33.57 | 10.27 |

| 1992 | 33.58 | 10.57 |

| 1993 | 34.83 | 10.89 |

| 1995 | 38.96 | 11.74 |

| 1996 | 38.38 | 11.62 |

| 1997 | 40.31 | 12.33 |

| 1998 | 42.69 | 12.74 |

| 1999 | 43.50 | 12.84 |

| 2000 | 45.00 | 13.41 |

| 2001 | 46.29 | 13.48 |

| 2002 | 48.02 | 13.76 |

| 2003 | 49.62 | 13.91 |

| 2004 | 49.55 | 13.63 |

| 2005 | 50.49 | 13.89 |

| 2006 | 51.14 | 13.86 |

| 2007 | 51.98 | 14.09 |

| 2008 | 50.01 | 13.48 |

| 2009 | 50.07 | 12.87 |

| 2010 | 49.09 | 12.63 |

| 2011 | 50.08 | 13.48 |

| 2012 | 52.48 | 13.80 |

| 2013 | $52.39 | $13.80 |

Notes: Sample restricted to nonunion full-time workers in the private sector ages 16 to 64.

Source: Adapted from Figure C in Jake Rosenfeld, Patrick Denice, and Jennifer Laird, Union decline lowers wages of nonunion workers, Economic Policy Institute Report, August 30, 2016

All workers would be better off in terms of wage levels had the right of workers to associate and bargain collectively not been severely eroded in recent decades. Between 1979 and 2013, the share of private-sector workers in a union fell from about 34 percent to 10 percent among men, and from 16 percent to 6 percent among women. This decline in union density has eroded wages for nonunion workers at every level of education and experience, costing billions in lost wages. For the 32.9 million full-time nonunion women working in the private sector and the 40.2 million full-time men working in the private sector, there is a $133 billion loss in annual wages because of weakened unions. This translates to real weekly wage losses for workers. Women would be making $13.80 more a week and men would be making $52.39 more a week, had union density (the share of workers in similar industries and regions who are union members) remained the same as in 1979.

Unions keep wages high for nonunion workers for several reasons. Union agreements set wage standards that nonunion employers follow. And a strong union presence prompts managers to keep wages high to prevent workers from organizing or leaving. Unions also set industry-wide norms, influencing what is seen as a “moral economy.”

Though not shown in the graph, working-class men have felt the decline in unionization the hardest. Specifically, nonunion men lacking a college degree would have earned 8 percent, or $3,016, more in 2013 if unions had remained as strong as they were in 1979.

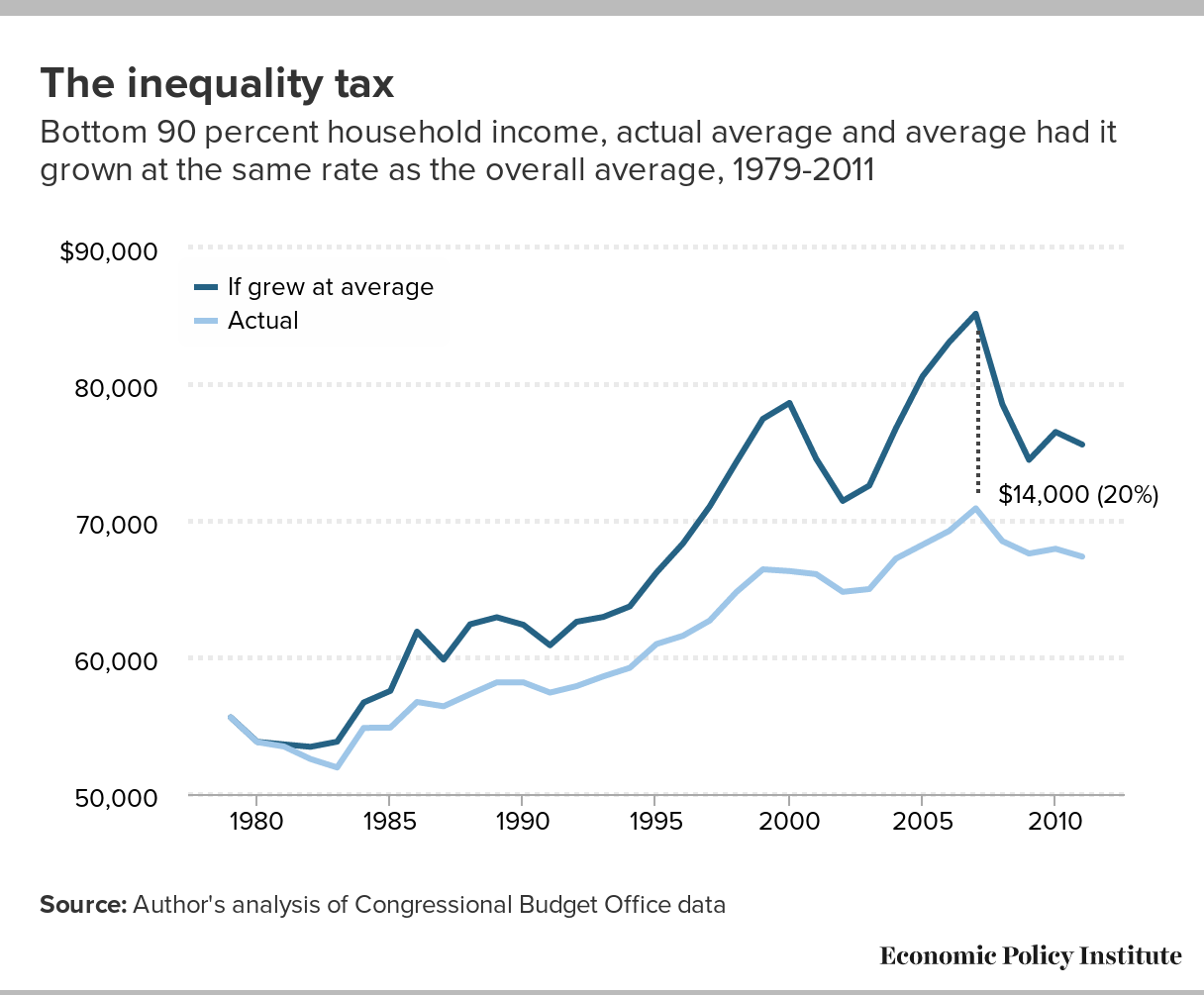

Source: Data are from a new data set compiled by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman. A new data set confirms what we know about the enormous increase in income inequality after 1979. This data set allows us to take another cut at this issue, with all of total national income and its distribution accounted for—market-based incomes like wages and dividends, transfer incomes like Social Security and Medicare, and even the income stemming from direct government purchases. The figure charts incomes (indexed to be 100 in 1979) for the bottom 50 percent of households, bottom 90 percent of households, households between the 50th and 90th percentiles, households in subgroups of the top 10 percent, and the top 0.1 percent of households. The results are clear: households nearer the top of the income distribution have seen far more rapid growth in recent decades. And counting income in the form of government benefits does not close the gap between income growth at the top and the income growth of everybody else.Yet another data source documents the enormous surge in American inequality: Post-tax-and-transfer household income growth from the distributional national accounts data, by income percentile

Bottom 90

Bottom 50

Next 40

91-95th

96-99th

99-99.9th

Top 0.1

1913

23.7327

33.65331

29.93943

43.27823

75.47623

1914

21.28975

30.44152

27.42943

38.72785

70.84473

1915

22.01303

31.29446

27.63197

33.98987

76.78276

1916

24.03428

35.05713

32.63794

45.75293

95.50515

1917

23.36389

37.55653

35.58478

48.98219

70.30063

1918

25.99977

37.45943

39.75538

51.13678

45.59054

1919

23.7557

29.73864

37.5025

55.97586

66.42215

1920

23.91308

30.49568

36.39877

52.00038

52.00913

1921

20.40423

33.57089

35.97857

46.24904

43.86804

1922

22.56271

35.35251

38.48873

48.60645

46.79869

1923

26.62762

36.18494

40.41201

51.57063

52.83884

1924

25.3325

37.78878

41.67534

53.30806

55.98231

1925

25.04011

35.89191

43.1564

60.36712

66.94126

1926

26.0494

35.2388

44.31057

65.07314

80.33322

1927

25.88253

35.26906

43.68758

62.20689

72.31164

1928

25.59061

36.8098

44.30285

63.26883

81.19631

1929

27.59766

36.22686

45.13929

63.97269

84.32806

1930

25.69753

36.78869

41.43329

53.91076

50.41799

1931

23.58497

37.6386

38.18021

42.38411

23.40733

1932

19.5378

33.37675

36.22934

33.874

12.42559

1933

18.8133

29.89834

35.59108

34.83715

16.7181

1934

20.12877

31.87053

41.05316

44.31979

30.83398

1935

22.40259

36.77853

41.38343

48.20434

35.22401

1936

24.67013

40.19861

42.85473

57.50882

45.48423

1937

26.43228

41.65951

44.5373

62.14962

50.66807

1938

24.79725

42.58223

43.10907

53.47296

34.3556

1939

25.55145

44.95177

46.81794

61.79799

46.51512

1940

27.62901

47.54603

48.92943

67.68232

61.10282

1941

33.88191

54.39828

53.65169

79.19836

73.09964

1942

43.29914

63.3563

55.50446

81.06559

73.31078

1943

52.80965

69.71679

58.40494

83.07906

70.12778

1944

54.60111

83.20119

61.25023

73.92529

58.40418

1945

54.2032

73.59434

58.5029

67.72197

42.88401

1946

47.1023

54.98784

55.75051

65.37271

42.55941

1947

45.61777

51.27523

52.65075

64.54918

52.81662

1948

46.27771

55.32878

56.69584

73.94818

67.30207

1949

44.85111

55.47728

53.61912

68.53701

64.51888

1950

48.95762

59.82028

58.26081

76.67206

69.6535

1951

53.13092

63.30267

61.1851

79.11648

66.05985

1952

55.543

63.20365

60.6588

75.66076

67.4788

1953

58.13027

66.00397

60.82156

74.12246

62.29707

1954

56.74598

64.72895

59.72348

73.76929

61.18403

1955

60.45715

66.59386

64.45841

81.47777

74.45941

1956

62.6146

66.07277

65.53554

78.24851

69.06196

1957

63.07287

64.54181

65.75526

77.86183

67.29979

1958

61.44245

65.657

65.02915

72.07397

56.18065

1959

65.02998

68.06952

68.14701

78.90449

69.33398

1960

66.89607

68.68847

68.1266

76.77248

69.91774

1961

67.78351

69.65426

70.63115

75.09075

67.87351

1962

70.4927

63.64325

74.46108

73.76656

75.63827

80.53871

77.82573

1963

72.34403

64.45871

76.91257

77.00796

79.27725

84.17178

83.4488

1964

74.78534

65.27417

80.29585

80.97379

83.68492

88.60585

90.01243

1965

78.97684

70.13567

84.09917

84.71663

87.38434

91.63466

93.81867

1966

83.00219

74.99717

87.64008

88.19319

90.8142

94.28764

97.31097

1967

85.64931

80.78541

88.46732

87.65472

88.85984

92.36706

88.88887

1968

89.01593

85.16668

91.24607

89.55186

89.20251

91.6852

88.51358

1969

91.25928

88.4355

92.8953

90.5163

88.4021

88.0171

83.84223

1970

89.31669

87.15028

90.57185

88.66994

86.42245

85.17894

75.69672

1971

89.55088

87.09922

90.9713

89.31088

87.57022

86.35819

76.34119

1972

92.38655

90.03742

93.74757

92.96691

92.13266

90.75359

79.82626

1973

96.11671

94.64942

96.96682

96.91853

96.75554

95.51017

81.34194

1974

94.02037

93.52424

94.30781

93.87008

92.52697

90.70497

76.23273

1975

91.01398

90.52585

91.29679

90.96083

89.50955

87.40869

74.26816

1976

94.35718

94.2051

94.44529

94.31208

92.73313

90.32411

76.67994

1977

96.81916

96.52656

96.98868

97.28635

96.48129

94.6759

82.49974

1978

99.88037

99.34863

100.1884

100.8638

100.2407

98.91114

90.22779

1979

100

100

100

100

100

100

100

1980

98.26488

97.61414

98.64191

97.76216

94.80523

93.1143

86.91483

1981

97.68509

96.23014

98.52805

98.91017

97.19851

98.64778

100.612

1982

94.07145

90.60212

96.08148

96.72842

94.56753

95.22981

101.7506

1983

94.64854

88.9539

97.94785

100.3394

97.77981

101.0831

103.9856

1984

98.68139

91.5108

102.8358

107.8385

107.5276

116.219

131.004

1985

100.8055

93.33651

105.1329

109.655

108.4626

118.0252

130.057

1986

102.7875

94.35348

107.6739

111.2332

109.3253

116.9127

110.9831

1987

104.7421

96.2283

109.6748

111.9271

112.8364

128.7529

134.6872

1988

106.8402

97.96563

111.982

115.4286

118.3864

143.0172

175.9767

1989

108.8137

100.2283

113.7879

116.895

119.2596

144.3395

165.6537

1990

108.8275

100.2639

113.789

116.7634

118.5356

144.6014

165.7722

1991

106.9756

98.14099

112.0942

115.7375

118.7417

137.8344

148.6849

1992

107.6168

97.72335

113.3488

117.3251

122.0337

147.7052

168.7361

1993

109.3271

99.80908

114.8416

119.6654

123.0398

142.693

159.3989

1994

112.7897

102.5032

118.7495

124.494

127.9362

146.7308

162.0879

1995

114.2954

103.2037

120.7217

127.2814

132.2493

154.3844

173.5347

1996

116.8251

105.3766

123.458

131.5369

138.125

162.6432

189.7594

1997

120.0619

107.7359

127.2032

136.0553

143.8332

171.3382

212.6514

1998

124.279

111.47

131.7001

140.7231

150.4667

182.4624

217.8013

1999

127.0094

113.8701

134.6219

144.6325

154.4141

192.1739

242.2452

2000

130.2871

116.1185

138.496

149.5242

160.0374

201.6449

262.2195

2001

130.563

116.4413

138.7448

149.1107

157.6435

196.2731

255.3759

2002

129.6873

115.0149

138.188

148.5807

158.6449

198.1229

258.2305

2003

130.7376

114.3935

140.2069

151.4572

159.7162

200.1824

268.4298

2004

133.1071

116.6533

142.6401

154.2173

164.2175

211.3237

298.3971

2005

135.1675

118.907

144.5884

157.2676

168.406

216.9945

327.02

2006

137.0963

120.5917

146.6586

160.8505

174.6956

230.622

345.1448

2007

136.5364

121.2232

145.4084

159.4222

171.626

221.0781

328.095

2008

134.4407

120.4954

142.5202

153.4786

163.4876

212.8995

330.0312

2009

128.613

111.9696

138.2557

148.2443

155.5828

195.6494

318.9889

2010

129.7716

114.2373

138.7717

150.9138

159.7115

205.1275

356.6267

2011

131.4316

114.5713

141.2

154.8323

165.0593

213.0578

348.0072

2012

132.2085

113.8685

142.8342

159.1319

171.7283

226.6272

380.3506

2013

134.7136

116.3695

145.3417

161.0668

174.0647

219.045

330.5724

2014

136.7039

118.4258

147.2938

164.6328

178.6594

227.4947

346.8308

The gap between the retirement ‘haves’ and ‘have-nots’ has grown since the recession: Retirement account savings of families age 32–61 by savings percentile, 1989–2013 (2013 dollars)

| 50th (median) | 60th | 70th | 80th | 90th | |

|---|---|---|---|---|---|

| 1989 | $0 | $5,423 | $14,461 | $32,536 | $90,379 |

| 1992 | $0 | $4,874 | $16,248 | $39,384 | $90,987 |

| 1995 | $2,277 | $9,866 | $24,286 | $47,054 | $113,841 |

| 1998 | $6,004 | $17,440 | $38,597 | $73,763 | $160,106 |

| 2001 | $7,879 | $23,638 | $48,326 | $92,818 | $223,247 |

| 2004 | $6,166 | $19,730 | $49,326 | $102,351 | $246,628 |

| 2007 | $11,228 | $30,315 | $61,754 | $123,508 | $258,243 |

| 2010 | $5,358 | $19,291 | $42,868 | $96,453 | $246,490 |

| 2013 | $5,000 | $20,100 | $50,000 | $116,000 | $274,000 |

Note: Retirement account savings include 401(k)s, IRAs, and Keogh plans. Scale changed to accommodate larger values.

Source: Adapted from Figure 9 in Monique Morrissey, The State of American Retirement:

How 401(k)s have failed most American workers, Economic Policy Institute Report, March 3, 2016

Over the past generation of economic life, the U.S. economy undertook a grand experiment in making defined-contribution (DC) pension plans such as 401(k)s, often financed directly by workers’ savings themselves, the primary vehicle of private retirement security. This experiment has decisively failed. Overall pension coverage has not increased, and fewer Americans are in defined-benefit (DB) plans (think company pensions). The DB plans crowded out by DC plans were more secure, providing a guaranteed income for life that was not subject to the vagaries of the stock market. They were also much more equal than DC plans because they were employer-funded and participation was automatic (rather than workers bearing most of the costs and all of the risks).

Nearly half of working-age families have nothing saved in retirement accounts, and the median working-age family had only $5,000 saved in 2013. Meanwhile, families in the 90th percentile of retirement savings had $274,000 in retirement, and the top 1 percent of families had $1,080,000 or more (not shown on chart). These huge disparities reflect a growing gap between the haves and the have-nots since the Great Recession, as accounts with smaller balances have stagnated while larger ones have rebounded.

Fiscal austerity explains why recovery has been so long in coming: Change in per capita government spending during recoveries of the last four recessions

| 1982Q4 | 1991Q1 | 2001Q4 | 2009Q2 | |

|---|---|---|---|---|

| -6 | 90.83817 | |||

| -5 | 96.46779 | 91.33168 | ||

| -4 | 96.72548 | 97.80345 | ||

| -3 | 96.51523 | 96.35624 | 94.05089 | |

| -2 | 97.21731 | 98.09825 | 98.14218 | 94.4813 |

| -1 | 98.26435 | 98.92533 | 97.98324 | 96.68474 |

| 0 | 100 | 100 | 100 | 100 |

| 1 | 100.3829 | 100.7468 | 101.5275 | 99.84022 |

| 2 | 100.9558 | 100.4456 | 102.3723 | 99.50632 |

| 3 | 101.005 | 100.9653 | 102.8023 | 100.7222 |

| 4 | 99.79553 | 102.3054 | 103.3013 | 101.0192 |

| 5 | 100.4771 | 102.4831 | 103.1351 | 101.1242 |

| 6 | 101.715 | 102.7714 | 104.3665 | 100.3432 |

| 7 | 102.037 | 102.2554 | 104.5556 | 98.88213 |

| 8 | 103.485 | 101.9195 | 104.6451 | 98.15822 |

| 9 | 104.602 | 101.724 | 105.4192 | 97.23836 |

| 10 | 106.0107 | 102.011 | 105.8382 | 96.86414 |

| 11 | 107.6073 | 101.868 | 105.804 | 95.9267 |

| 12 | 107.6288 | 101.2959 | 105.4445 | 95.78736 |

| 13 | 108.7749 | 101.4328 | 106.1767 | 95.40735 |

| 14 | 110.4932 | 102.1325 | 106.3521 | 94.83589 |

| 15 | 112.3029 | 101.9209 | 106.5289 | 94.21625 |

| 16 | 111.6476 | 102.6275 | 106.0185 | 93.90439 |

| 17 | 112.0741 | 102.8173 | 107.5423 | 93.62299 |

| 18 | 112.6221 | 102.3836 | 107.6773 | 93.04895 |

| 19 | 112.3952 | 101.1486 | 107.8776 | 93.22292 |

| 20 | 113.0807 | 101.9359 | 108.2144 | 93.60604 |

| 21 | 113.3476 | 103.2437 | 109.1187 | 94.245 |

| 22 | 113.3408 | 102.7047 | 109.0787 | 94.14226 |

| 23 | 113.108 | 102.7598 | 109.5846 | 95.09063 |

| 24 | 114.405 | 103.1194 | 109.8789 | 95.43504 |

| 25 | 114.9973 | 103.4402 | 95.722 | |

| 26 | 116.1049 | 103.3562 | 95.86387 | |

| 27 | 116.8758 | 103.2392 | 96.35498 |

Note: For total government spending, government consumption and investment expenditures are deflated with the NIPA price deflator. Government transfer payments are deflated with the price deflator for personal consumption expenditures. This figure includes state and local government spending.

Source: Adapted from Figure B in Josh Bivens, Why is recovery taking so long—and who’s to blame?, Economic Policy Institute Report, August 11, 2016

The agonizingly slow pace of recovery from the Great Recession is easy to explain: it is the result of austerity policies championed by Republican policymakers at the federal and state levels. Like every other postwar recession before it, the Great Recession was caused by a shortfall in aggregate demand, meaning that the spending of households, businesses, and governments was not sufficient to keep the economy’s resources fully employed.

Despite the Great Recession being the sharpest and longest on record since World War II, and despite monetary policy reaching its conventional limits to boost spending early in the recession, policymakers made damaging decisions to limit public spending following the recession’s trough in 2009. This growth has been historically slow relative to other business cycles even as the economy needed substantially faster-than-average growth to mount a full and timely recovery.

The figure shows the growth in per capita spending by federal, state, and local governments following the troughs of the four recessions. Astoundingly, per capita government spending in the first quarter of 2016—27 quarters into the recovery—was nearly 3.5 percent lower than it was at the trough of the Great Recession. By contrast, 27 quarters into the early 1990s recovery, per capita government spending was 3 percent higher than at the trough; 23 quarters following the early 2000s recession (a shorter recovery), it was 10 percent higher; and 27 quarters into the early 1980s recovery, it was 17 percent higher.

Nominal wage growth shows economy is not overheating: Year-over-year change in private-sector nominal average hourly earnings, 2007–2016

| All nonfarm employees | Production/nonsupervisory workers | |

|---|---|---|

| Mar-2007 | 3.59% | 4.11% |

| Apr-2007 | 3.27% | 3.85% |

| May-2007 | 3.73% | 4.14% |

| Jun-2007 | 3.81% | 4.13% |

| Jul-2007 | 3.45% | 4.05% |

| Aug-2007 | 3.49% | 4.04% |

| Sep-2007 | 3.28% | 4.15% |

| Oct-2007 | 3.28% | 3.78% |

| Nov-2007 | 3.27% | 3.89% |

| Dec-2007 | 3.16% | 3.81% |

| Jan-2008 | 3.11% | 3.86% |

| Feb-2008 | 3.09% | 3.73% |

| Mar-2008 | 3.08% | 3.77% |

| Apr-2008 | 2.88% | 3.70% |

| May-2008 | 3.02% | 3.69% |

| Jun-2008 | 2.67% | 3.62% |

| Jul-2008 | 3.00% | 3.72% |

| Aug-2008 | 3.33% | 3.83% |

| Sep-2008 | 3.23% | 3.64% |

| Oct-2008 | 3.32% | 3.92% |

| Nov-2008 | 3.64% | 3.85% |

| Dec-2008 | 3.58% | 3.84% |

| Jan-2009 | 3.58% | 3.72% |

| Feb-2009 | 3.24% | 3.65% |

| Mar-2009 | 3.13% | 3.53% |

| Apr-2009 | 3.22% | 3.29% |

| May-2009 | 2.84% | 3.06% |

| Jun-2009 | 2.78% | 2.94% |

| Jul-2009 | 2.59% | 2.71% |

| Aug-2009 | 2.39% | 2.64% |

| Sep-2009 | 2.34% | 2.75% |

| Oct-2009 | 2.34% | 2.63% |

| Nov-2009 | 2.05% | 2.67% |

| Dec-2009 | 1.82% | 2.50% |

| Jan-2010 | 1.95% | 2.61% |

| Feb-2010 | 2.00% | 2.49% |

| Mar-2010 | 1.77% | 2.27% |

| Apr-2010 | 1.81% | 2.43% |

| May-2010 | 1.94% | 2.59% |

| Jun-2010 | 1.71% | 2.53% |

| Jul-2010 | 1.85% | 2.47% |

| Aug-2010 | 1.75% | 2.41% |

| Sep-2010 | 1.84% | 2.30% |

| Oct-2010 | 1.88% | 2.51% |

| Nov-2010 | 1.65% | 2.23% |

| Dec-2010 | 1.74% | 2.07% |

| Jan-2011 | 1.92% | 2.17% |

| Feb-2011 | 1.87% | 2.12% |

| Mar-2011 | 1.87% | 2.06% |

| Apr-2011 | 1.91% | 2.11% |

| May-2011 | 2.00% | 2.16% |

| Jun-2011 | 2.13% | 2.00% |

| Jul-2011 | 2.26% | 2.31% |

| Aug-2011 | 1.90% | 1.99% |

| Sep-2011 | 1.94% | 1.93% |

| Oct-2011 | 2.11% | 1.77% |

| Nov-2011 | 2.02% | 1.77% |

| Dec-2011 | 1.98% | 1.77% |

| Jan-2012 | 1.75% | 1.40% |

| Feb-2012 | 1.88% | 1.45% |

| Mar-2012 | 2.10% | 1.76% |

| Apr-2012 | 2.01% | 1.76% |

| May-2012 | 1.83% | 1.39% |

| Jun-2012 | 1.95% | 1.54% |

| Jul-2012 | 1.77% | 1.33% |

| Aug-2012 | 1.82% | 1.33% |

| Sep-2012 | 1.99% | 1.44% |

| Oct-2012 | 1.51% | 1.28% |

| Nov-2012 | 1.90% | 1.43% |

| Dec-2012 | 2.20% | 1.74% |

| Jan-2013 | 2.15% | 1.89% |

| Feb-2013 | 2.10% | 2.04% |

| Mar-2013 | 1.93% | 1.88% |

| Apr-2013 | 2.01% | 1.73% |

| May-2013 | 2.01% | 1.88% |

| Jun-2013 | 2.13% | 2.03% |

| Jul-2013 | 1.91% | 1.92% |

| Aug-2013 | 2.26% | 2.18% |

| Sep-2013 | 2.04% | 2.17% |

| Oct-2013 | 2.25% | 2.27% |

| Nov-2013 | 2.24% | 2.32% |

| Dec-2013 | 1.90% | 2.16% |

| Jan-2014 | 1.94% | 2.31% |

| Feb-2014 | 2.14% | 2.45% |

| Mar-2014 | 2.18% | 2.40% |

| Apr-2014 | 1.97% | 2.40% |

| May-2014 | 2.13% | 2.44% |

| Jun-2014 | 2.04% | 2.34% |

| Jul-2014 | 2.09% | 2.43% |

| Aug-2014 | 2.21% | 2.48% |

| Sep-2014 | 2.04% | 2.27% |

| Oct-2014 | 2.03% | 2.27% |

| Nov-2014 | 2.11% | 2.26% |

| Dec-2014 | 1.82% | 1.87% |

| Jan-2015 | 2.23% | 2.01% |

| Feb-2015 | 2.06% | 1.71% |

| Mar-2015 | 2.18% | 1.90% |

| Apr-2015 | 2.34% | 2.00% |

| May-2015 | 2.34% | 2.14% |

| Jun-2015 | 2.04% | 1.99% |

| Jul-2015 | 2.29% | 2.04% |

| Aug-2015 | 2.32% | 2.08% |

| Sep-2015 | 2.40% | 2.13% |

| Oct-2015 | 2.52% | 2.36% |

| Nov-2015 | 2.39% | 2.21% |

| Dec-2015 | 2.60% | 2.61% |

| Jan-2016 | 2.50% | 2.50% |

| Feb-2016 | 2.38% | 2.50% |

| Mar-2016 | 2.33% | 2.44% |

| Apr-2016 | 2.49% | 2.53% |

| May-2016 | 2.48% | 2.33% |

| Jun-2016 | 2.64% | 2.48% |

| Jul-2016 | 2.72% | 2.57% |

| Aug-2016 | 2.47% | 2.42% |

| Sep-2016 | 2.67% | 2.60% |

| Oct-2016 | 2.82% | 2.36% |

| Nov-2016 | 2.45% | 2.36% |

*Nominal wage growth consistent with the Federal Reserve Board’s 2 percent inflation target, 1.5 percent productivity growth, and a stable labor share of income.

Source: Adapted from EPI’s “Nominal Wage Tracker”

The year 2017 looks to be the year that the Fed begins raising short-term interest rates in earnest. The Fed should raise rates only when it fears the economy is growing too fast and pushing unemployment low enough that workers are empowered to demand (and get) raises above what their productivity justifies. Data on nominal wage growth show that the economy is not getting overheated and thus a rate increase is not justified.

The pace of economic growth should be considered unsustainable only when increases in labor costs force firms to raise prices enough to accelerate inflation above the Federal Reserve’s stated goal of 2 percent inflation. An absolutely crucial link in this chain is wage growth. If nominal (i.e., not inflation-adjusted) wages simply grow at the rate of economy-wide productivity, then wages are putting no upward pressure on prices. To see why, think of a 2 percent raise in hourly pay of a worker whose productivity (how much they produce in an hour) also rises 2 percent. The worker is getting 2 percent more, but is also producing 2 percent more. So the labor cost per unit of output is unchanged, and there is zero upward pressure on firms’ costs, or overall inflation. And the goal of Federal Reserve policy is not zero upward pressure on prices (or 0 percent inflation). Their stated target is 2 percent inflation. This means that nominal wages can grow at the rate of economy-wide productivity growth plus 2 percent before they are putting enough upward pressure on prices to make the Fed rein them in. EPI’s nominal wage tracker looks are how wages have grown over this recovery relative to a target of 1.5 percent (a common estimate of long-run, trend productivity growth) plus 2 percent. Nominal wage growth has been consistently below this target, meaning there is very little reason to worry about overheating in the economy.

The U.S. has a lower share of prime-age women with a job than do peer countries: Employment-to-population ratio of women workers age 25–54, select countries, 1995–2014

| Canada | Germany | Japan | United States | |

|---|---|---|---|---|

| 1995 | 69.434551% | 66.360158% | 63.233624% | 72.189196% |

| 1996 | 69.577146% | 67.220440% | 63.701741% | 72.770073% |

| 1997 | 70.971110% | 67.399584% | 64.566038% | 73.541046% |

| 1998 | 72.183646% | 68.944387% | 64.036077% | 73.642970% |

| 1999 | 73.245982% | 70.253128% | 63.551051% | 74.147991% |

| 2000 | 73.944309% | 71.210539% | 63.582090% | 74.213847% |

| 2001 | 74.297867% | 71.607431% | 64.124398% | 73.421299% |

| 2002 | 75.348504% | 71.845950% | 63.863976% | 72.259684% |

| 2003 | 76.000458% | 71.981067% | 64.407421% | 72.006189% |

| 2004 | 76.720415% | 72.129055% | 65.028791% | 71.848458% |

| 2005 | 76.488663% | 70.969949% | 65.733178% | 71.963537% |

| 2006 | 76.984912% | 72.647765% | 66.614235% | 72.504467% |

| 2007 | 78.190906% | 74.045933% | 67.370518% | 72.501768% |

| 2008 | 78.008148% | 74.744854% | 67.495987% | 72.301570% |

| 2009 | 77.114622% | 75.420875% | 67.595960% | 70.208609% |

| 2010 | 77.075022% | 76.320711% | 68.157788% | 69.343654% |

| 2011 | 77.207691% | 77.892216% | 68.459240% | 68.967922% |

| 2012 | 77.710148% | 78.235789% | 69.161920% | 69.196894% |

| 2013 | 78.090883% | 78.625264% | 70.773639% | 69.253713% |

| 2014 | 77.444969% | 78.839200% | 71.835052% | 69.997790% |

Source: Adapted from Figure F in Josh Bivens et al., It’s time for an ambitious national investment in America’s children, Economic Policy Institute Report, April 6, 2016

Reducing gender and inequality wage gaps and lowering unemployment enough to spur sustainable wage growth are absolutely essential steps if we are serious about restoring economic security to millions of working families. But a working labor market requires more than just jobs and wages. It requires a policy infrastructure that enables workers to enter the labor market and be productive in their roles as employees because they don’t have to make difficult choices between their careers and their caregiving responsibilities.

Paid family leave and subsidized child care provide family security, which benefits employers and the economy. But there are currently no national standards regarding paid family leave or subsidized child care. Each worker is left to the whims of individual company policies, which often means no allowance or support for family leave or child care. Therefore, workers have to make difficult choices between their careers and their caregiving responsibilities precisely when they need their paychecks the most, such as following the birth of a child or when they or a loved one falls ill. The lack of these policies particularly affects women, as they currently take on the lion’s share of unpaid care work. In contrast, many of our peer nations have such policies. Not surprisingly, the United States has fallen far behind some of our international peers in the share of women who are working. The graph shows the share of women age 25–54 with a job between 1995 and 2014. While the share of prime-age women with a job rose in Germany, Canada, and Japan, in the United States it actually fell. Policies that help workers, particularly women, balance work and family could meaningfully increase women’s employment, which would also mean more earnings for families and more economic activity for the country. (See EPI’s latest investigation into child care for how progressive child care policy, in particular, can benefit families, reduce inequality, and increase economic growth.)

The number of salaried workers guaranteed overtime pay has plummeted since 1979: Number of salaried workers* covered by overtime salary threshold, 1979–2014 (in millions)

| Year | Number of salaried workers* covered |

|---|---|

| 1979 | 12.6 |

| 1980 | 10.8 |

| 1981 | 8.9 |

| 1982 | 7.4 |

| 1983 | 6.5 |

| 1984 | 5.8 |

| 1985 | 5.1 |

| 1986 | 4.5 |

| 1987 | 3.8 |

| 1988 | 3.5 |

| 1989 | 3.4 |

| 1990 | 3.0 |

| 1991 | 2.4 |

| 1992 | 2.2 |

| 1993 | 2.1 |

| 1994 | 2.5 |

| 1995 | 2.3 |

| 1996 | 2.2 |

| 1997 | 2.0 |

| 1998 | 1.9 |

| 1999 | 1.6 |

| 2000 | 1.5 |

| 2001 | 1.3 |

| 2002 | 1.2 |

| 2003 | 1.1 |

| 2004 | 5.5 |

| 2005 | 5.5 |

| 2006 | 4.9 |

| 2007 | 4.8 |

| 2008 | 4.4 |

| 2009 | 3.9 |

| 2010 | 3.8 |

| 2011 | 3.8 |

| 2012 | 3.7 |

| 2013 | 3.6 |

| 2014 | 3.5 |

* The sample included salaried (nonhourly), full-time workers who are 18 years or older. It excluded teachers (pre-K through college) and religious workers, who are automatically exempt from overtime protections.

Note: The nominal threshold was set at $250 per week from 1975 until 2004 when it was increased to $455 per week. Under the Fair Labor Standards Act, all salaried workers under the threshold must receive overtime pay for hours worked beyond 40 per week.

Source: Adapted from Figure A in Ross Eisenbrey, Raising the overtime salary threshold is an important improvement in working families’ labor standards, Economic Policy Institute Testimony, October 5, 2015

Work-life balance is a fundamental goal of the Fair Labor Standards Act (FLSA). Its requirement that employers pay hourly and lower-earning salaried employees a premium for time worked beyond 40 hours a week makes the FLSA the most family-friendly law ever passed in the United States. Excessive work is detrimental to family life, health, well-being, and productivity, and the law aims to protect workers who are junior enough that they can be forced to work extra hours. If not for the law’s overtime rules, tens of millions more workers would be working 50, 60, or 70 hours a week for no additional pay, just as millions of Americans did before the FLSA was enacted in 1938.

But millions more are still dealing with this overwork and stress on families, in part because the salary threshold that determines whether workers are automatically eligible for overtime pay is set for a 1970s economy, not a 2010s economy. As shown in the graph, in 1979 more than 12 million salaried workers earned less than the salary threshold and were therefore automatically guaranteed the right to overtime pay, regardless of their duties. Today, with a 50 percent bigger workforce, only 3.5 million salaried employees are automatically protected.

A new rule that guaranteed overtime protection to salaried workers making between $23,660 and $47,476 was instituted by the Department of Labor and was supposed to go into effect on December 1, 2016. But an egregiously bad legal decision has delayed enforcement of this common-sense rule.

Note: Data on manufacturing employment are from Current Employment Statistics (CES) program of the Bureau of Labor Statistics (BLS). Data on Chinese trade balance are from the Census Bureau. As a share of GDP, the US/China trade balance was 0.00% in 1985 (first year of data availability). We assume this value holds for pre-1985 years as well. The presidential campaign often highlighted the decline of American manufacturing jobs. An incorrect conventional wisdom among economic commentators holds that the decline of manufacturing employment has been driven by automation. This explanation does not fit the facts. Manufacturing employment was actually quite stable (aside from business cycle fluctuations) for 35 years between 1965 and 2000. But certainly there was plenty of automation between 1965 and 2000. Indeed productivity growth (a proxy for automation) was just as rapid in those years as thereafter. But 3 million jobs were lost in the 2001–2003 recession and jobless recovery from that recession. Then rapidly growing trade deficits—particularly with China—kept the subsequent recovery from aiding manufacturing jobs. This meant that manufacturing entered the Great Recession without having regained the jobs lost in the previous recession, and in fact having lost a small number more as the rest of the economy recovered. As a result of two recessions and the “China shock,” the manufacturing sector today has nearly 5 million fewer jobs than it did in 2000.It’s not technology killing manufacturing—employment was steady for 35 years between 1965 and 2000: Manufacturing employment and trade deficit with China, 1965–2015

Trade balance

Manufacturing employment

1965

0.00%

17051

1966

0.00%

17998

1967

0.00%

18025

1968

0.00%

18410

1969

0.00%

18485

1970

0.00%

17309

1971

0.00%

17202

1972

0.00%

18158

1973

0.00%

18820

1974

0.00%

17693

1975

0.00%

17140

1976

0.00%

17719

1977

0.00%

18531

1978

0.00%

19334

1979

0.00%

19301

1980

0.00%

18640

1981

0.00%

18223

1982

0.00%

16690

1983

0.00%

17551

1984

0.00%

18023

1985

0.00%

17693

1986

0.04%

17478

1987

0.06%

17809

1988

0.07%

18025

1989

0.11%

17881

1990

0.17%

17395

1991

0.21%

16916

1992

0.28%

16769

1993

0.33%

16815

1994

0.40%

17217

1995

0.44%

17231

1996

0.49%

17284

1997

0.58%

17588

1998

0.63%

17449

1999

0.71%

17280

2000

0.82%

17181

2001

0.78%

15711

2002

0.94%

14912

2003

1.08%

14300

2004

1.32%

14287

2005

1.54%

14193

2006

1.69%

14015

2007

1.79%

13746

2008

1.82%

12850

2009

1.57%

11475

2010

1.82%

11595

2011

1.90%

11802

2012

1.95%

11960

2013

1.91%

12086

2014

1.98%

12294

2015

2.04%

12320