See Snapshots archive.

Snapshot for May 2, 2007.

The ARMs Alarm

by Randall Dodd and Jared Bernstein

The alarm raised by the jump in subprime mortgage defaults has deflected attention away from a serious problem that afflicts many homeowners with subprime and prime mortgages alike: a significant share of all outstanding mortgages have adjustable interest rates, and the majority of these will reset in 2007 and 2008 at much higher rates.

Adjustable rate mortgages, or ARMs, are loans that begin with relatively low payments, and then, after a short period, reset at a higher rate.1 There are many variations, but most offer a low “teaser” interest rate for the first two or three years before resetting.

ARMs account for about 30% of all mortgages—and 75% of subprime mortgages—and they can have a big impact on household budgets. A recent study shows that over the next two years 60% of all ARMs made since 2004 will have their payments increase by 25% or higher, and 25% will increase by 50% or more.2

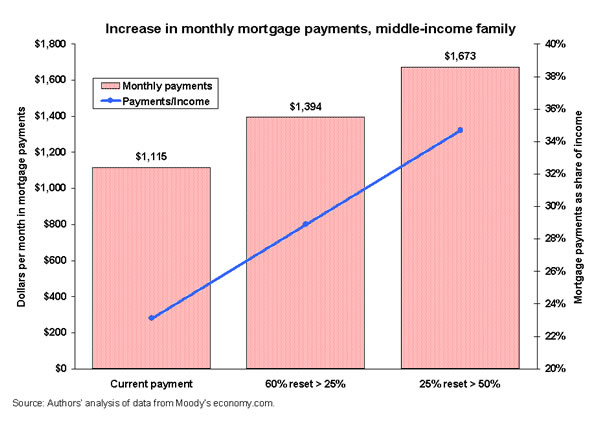

Just what could these resets mean to the typical family? As the Figure reveals, monthly payments for the median family could rise from about $1,100 per month to $1,400 to $1,700, increasing the mortgage payment from about 23% of income to about 35%.

These calculations are for middle-income families with annual incomes around $58,000 who borrowed to buy a home costing $223,000 (see data note for sources). But for lower income families, with an income of $35,000, for example, and a more modest home costing $200,000, a 25% jump in mortgage payments means going from a barely manageable 34% of income to 43%.

Many low- and middle-income families were already squeezed in this recovery, as indicated by the failure of the median income to keep pace with inflation. As family budgets are already being pinched by higher energy and food prices, that may turn out to be small change compared to the impact of higher home mortgage payments.

*Data note

Data refer to median family with income of $58,000, home value: $223,000, and initial mortgage rate of 6.4%, the median home price and average mortgage rate for the median family over the past six quarters, according to Moody’s economy.com.

Endnotes

1. The interest rate used to calculate the monthly payments on these loans is adjusted regularly according to changes in such short-term interest rates as U.S. Treasury bill yields.

2. Christopher L. Cagan. 2007. Mortgage Payment Reset: The Issue and the Impact. Report by First American CoreLogic, Santa Ana, Calif..