February 10, 2006

Rapid growth in oil prices, Chinese imports pump up trade deficit to new record

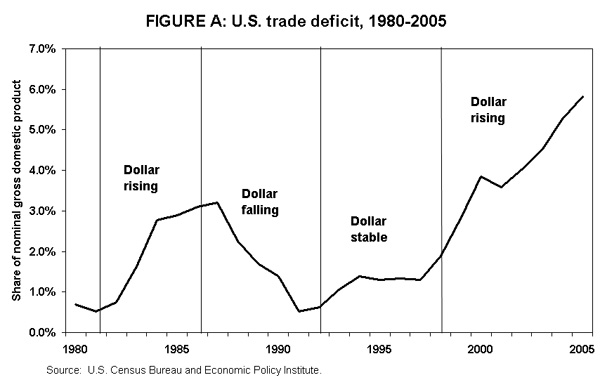

The U.S. Department of Commerce today reported that the international deficit in goods and services trade reached a record level of $726 billion in 2005, an 18% increase over 2004. The U.S. merchandise deficit alone, which excludes services, was $782 billion, also an 18% increase. The overall deficit increased $1 billion in December alone, to the third highest monthly level on record. The goods and services deficit as a share of U.S. gross domestic product (GDP) increased to an unprecedented 5.8% in 2005 (Figure A ). Rapid increases in the price of oil and related products were responsible for 63% of the increase in the deficit. The growth of the trade deficit with China, which reached $202 billion in 2005, was responsible for the entire increase in the United States’ non-oil trade deficit. The trade deficit in manufactured products (net of refined petroleum) increased $46 billion, to $655 billion (an 8% increase).

While the decline of the dollar against non-Asian currencies finally began to slow the growth rate of U.S. imports, export growth also slowed because the dollar has not fallen sufficiently. Much more depreciation will be needed to substantially reduce or eliminate the deficit. The determination of Asian governments to prop up the dollar to promote their export-led growth strategies is the largest barrier to needed dollar adjustments.

Dramatic increases in the cost of petroleum products and the volume of oil imports were responsible for nearly two-thirds of the increase in the trade deficit in 2005. The average price of crude oil imports increased 39% over 2004. In addition, the volume of petroleum product imports also increased 4% in 2005.

Total U.S. imports of goods and services reached $2 trillion in 2005 for the first time, 57% more than the $1.3 trillion in exports. To keep the trade deficit from widening further, the growth rate of exports must exceed the growth rate of imports by 57%. Last year, import growth (13%) exceeded export growth (10%), and imports expanded by $228 billion, almost twice as much as the increase in exports of $120 billion. Net imports as a share of GDP have increased for 10 consecutive years in a row (since 1995). If imports continue to grow at a 13% rate, the trade deficit will decline only if exports grow faster than 20%, which would be double their 2005 growth rate. In the absence of a dramatic and sustained slowdown in U.S. growth, exports can grow more than half again as fast as imports only with a substantial reduction in the value of the U.S. dollar.

The dollar must fall by at least an additional 30% to 40%, or more, to achieve the needed increase in export growth relative to imports. Imports grow rapidly and export growth slows when the dollar is increasing in value. Increases in the value of the dollar make imports cheap and U.S. exports more expensive on world markets. When the dollar appreciates, the rate of growth of imports typically surpasses the growth of exports (after a year or two). This pattern emerged in the early 1980s and has been the case since the mid-1990 when the trade deficit also grew rapidly (as shown in Figure A). Deficits can also be reduced by large, sustained falls in the dollar, as occurred between 1985 and 1991 when the dollar lost 26% of its value, which caused exports to grow faster than imports between 1987 and 1991, resulting in a large decline in the trade deficit.

The loss of U.S. export markets during the prolonged overvaluation of the dollar over the past decade has made it more difficult for U.S. firms to increase exports. The dollar simply has not fallen far or fast enough to stimulate adequate export growth. The dollar has only fallen 11.6% since 2002, much less than in the mid-1980s, yet the trade deficit is twice as large as it was in 1987. Hence, the trade deficit has continued to expand.

The rapid growth of imports and the loss of U.S. shares of world export markets, especially since 2000, have damaged the competitiveness of U.S. producers. The rising trade deficit in manufacturing has opened an ever-wider wedge between U.S. production and the nation’s purchases of manufactured goods. After accounting for exports and imports, U.S. manufacturing production fell from 86% of the value of our manufactured purchases in 2000 to 80% in 2004 (see Trade deficits and manufacturing employment ). U.S. producers have lost shares in many domestic and foreign product markets. If the trade deficit is to be reduced by recapturing domestic and foreign markets, substantial investments in new production capacity and marketing channels will be required. The tasks will be difficult but not impossible. U.S. manufacturing production would have to increase by about 25%, relative to domestic demand, in order to raise U.S. production to the same amount as our purchases and eliminate the trade deficit. This adjustment will take some time to complete, but it can be achieved in a few years if the dollar is allowed to depreciate by at least an additional 30% to 40%.

China’s trade surplus with the United States increased by 24.5% in 2005, to $202 billion, the United States’ largest bilateral deficit. This bilateral deficit with China increased $40 billion in 2005, more than accounting for the entire increase in the United States’ non-oil trade deficit. China has prevented any appreciable increase in the value of its currency, which has caused the bilateral trade deficit to balloon for a number of years. China’s intransigence has encouraged other Asian nations to prevent or slow increases in the value of their currencies. U.S. imports from China are six times the value of U.S. exports to China, making it the United States’ most imbalanced trading relationship. U.S. imports from China were $243 billion in 2005 (an increase of 24%), making China the second largest exporter of goods to the United States, behind Canada at $288 billion. At current rates of growth, China will surpass Canada and become the largest supplier of U.S. imports within the next two years.

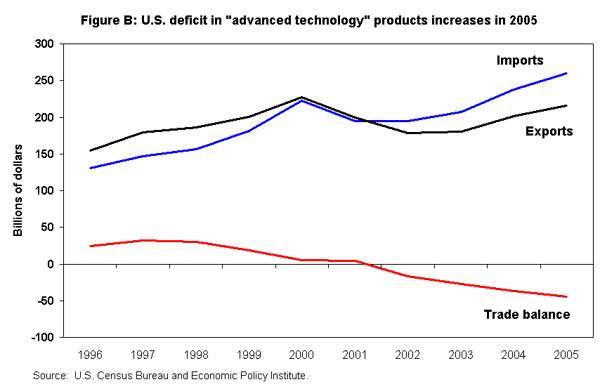

The U.S. also had a $44 billion trade deficit in “advanced technology products” (ATP) in 2005, an increase of 20% since 2004. The ATP exports declined between 2000 and 2002, and then recovered slowly, as shown in Figure B. While ATP imports also declined during the recession, they recovered sooner and have grown more rapidly. The United States has had a deficit in ATP products since 2002, and the balance in this sector has fallen steadily since 1997, when the United States had a surplus of $33 billion in these sectors. Imports of high-tech goods from China were responsible for the entire U.S. deficit in ATPs. The growth of the ATP deficit was responsible for 16% of the increase in the non-petroleum goods trade deficit. ATP goods generated 17% of the growth in exports in 2005, which demonstrates that this sector has significant potential for growth in the future.

The U.S. trade deficit poses great risks for the economy. The U.S. must borrow abroad to finance its trade deficits. The recent decline in the dollar indicates that private foreign lenders are less willing to supply new credit. Foreign governments stepped into the gap and financed a growing share of U.S. international debt in recent years. A rapid, uncontrolled decline in the dollar could destabilize U.S. financial markets and sharply increase interest rates and inflation. Foreign governments, primarily in Asia, have provided a substantial share of the net capital inflows in recent years.

The manufacturing sector has lost 3 million jobs over the last five years, including 81,000 jobs in 2005, as the manufacturing trade deficit has continued to expand. The U.S. deficit in manufactured goods rose from $609 billion in 2004 to $655 in 2005, an increase of 8%. Trade deficits and manufacturing job losses will continue to expand unless the dollar is brought down to a sustainable level. If these adjustments do not take place, the threat, according to the International Monetary Fund (see World Economic Outlook: Building Institutions, 2005, pp. 75-6), of an “abrupt and disorderly adjustment” could grow, leading to a “sharp contraction in economic activity,” otherwise known as a deep recession that would reduce the trade deficit by sharply reducing consumption (and employment) in the United States

—by EPI Senior International Economist Robert E. Scott with research assistance from David Ratner.

To view archived editions of TRADE PICTURE, click here.

The Economic Policy Institute TRADE PICTURE is published upon the release of quarterly and year-end trade figures from the Commerce Department.

EPI offers same-day analysis of income, price, employment, and other economic data released by U.S. government agencies. For more information, contact EPI at 202-775-8810.