Briefing Paper #213

Video, audio and written transcript from a May 29 forum featuring the authors

Most Americans are aware that income inequality has increased in the last 30 years. Less well known is that income instability—how much families’ incomes fluctuate up and down over time—has also grown substantially.

The Great Risk Shift (Hacker 2006; revised and expanded in 2008) documented a major post-1970s rise in family income instability and argued that it was one indicator of an increasing shift of economic risk from government and employers onto workers and their families. This Briefing Paper updates, improves, and extends these earlier estimates of rising family income instability and discusses potential causes and implications of this trend.

Part of the reason why family economic instability—sometimes called “income volatility”—has not been extensively examined is that aggregate economic statistics have been relatively stable and favorable. Neither the 1991 nor the 2001 recessions were particularly deep, and inflation and unemployment have remained historically low. Yet, as argued in The Great Risk Shift, these broadly stable and favorable aggregate indicators mask many signs of declining economic security among American families: dwindling health coverage and the rising financial threat posed by medical costs; the steady demise of pension plans offering a guaranteed benefit for the remainder of a retired workers’ life; the growing costs of job dislocations and high levels of involuntary job displacement; the rising levels of household debt, incidences of bankruptcy and mortgage foreclosures; and the dwindling of public benefits for American workers, especially in light of the increasing number of workers juggling household duties and paid employment due to the movement of women into the workforce. Along with rising levels of family income volatility, these long-term trends point to serious and growing threats to the economic security of American families that aggregate statistics on growth, inflation, and unemployment largely obscure.

In the time since The Great Risk Shift was published, new data have become available and a number of complementary analyses have appeared, all of which confirm the basic finding of rising family income volatility.1 These developments provide an opportunity to deepen and refine our understanding of this important trend. They also offer a chance to consider the strengths and weaknesses of the data used in studies of family income dynamics, as well as to suggest avenues for future research. Some of these revised analyses appear in the expanded paperback edition of The Great Risk Shift (2008). Others were done expressly for this briefing paper.

The main results reported in this brief are:

- The instability of family incomes has risen substantially over the last three decades. Although the precise magnitude of the increase depends on the approach to measuring income variance that is used, we estimate that short-term family income variance essentially doubled from 1969-2004. Much of the rise in income volatility occurred prior to 1985, and volatility dropped substantially in the late 1990s. It has, however, risen in recent years to exceed its 1980s peak.

- The proportion of working-age individuals experiencing a large drop in their family income (50% or greater) has climbed more steadily—from less than 4% in the early 1970s to nearly 10% in the early 2000s. The probability of large income drops varies predictably with the business cycle. Yet it has also trended strongly upward over time. For instance, the 2001 recession, which was mild in macroeconomic terms, was associated with a higher chance of large income drops than the recession of the early 1980s, which was the worst economic downturn since the Great Depression.

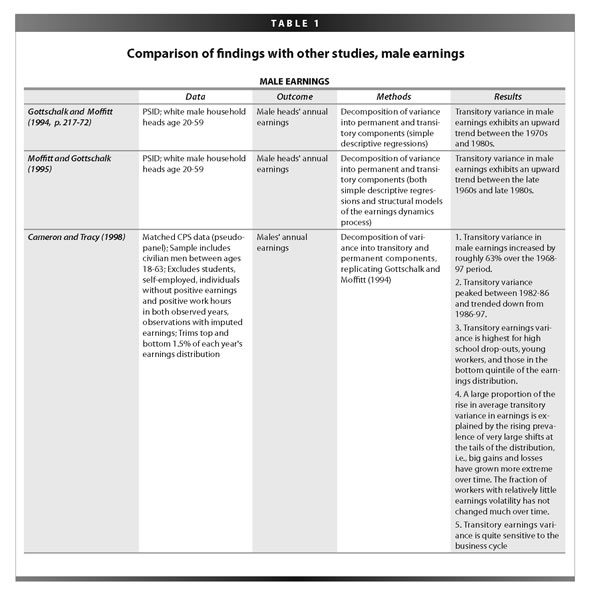

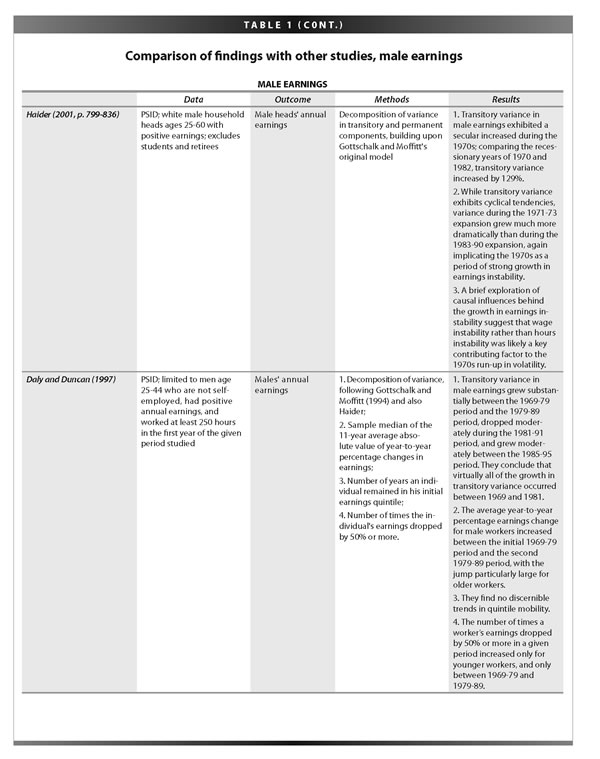

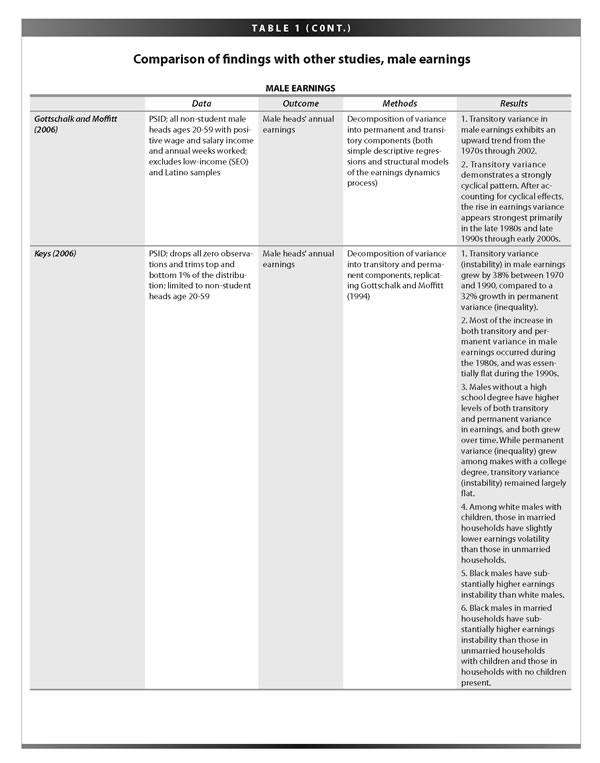

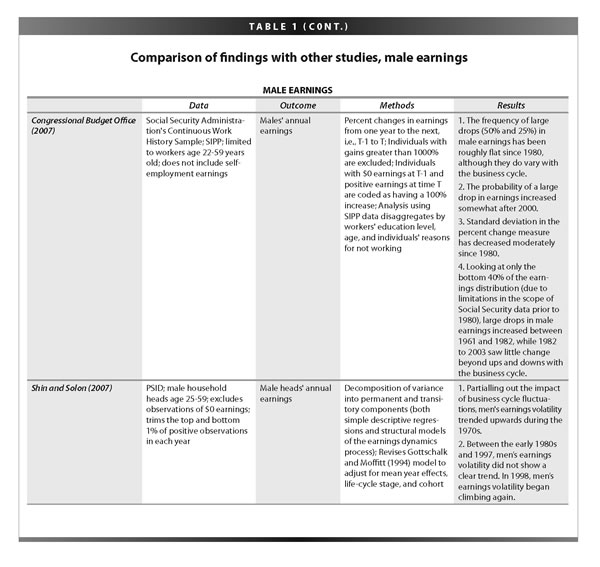

- There is an important distinction between family income (total earnings, asset income, and transfer income for all members of a family) and individual earnings. While the instability of individual male workers’ earnings rose sharply between the 1970s and 1980s, it has been more or less stable since then, trending up and down with the business cycle through the 1980s and 1990s, and rising again in the early 2000s. This basic trend—a rise in earnings variability in the 1970s, little clear trend from the early 1980s to the late 1990s, and an upswing in the early 2000s—has been confirmed by numerous analyses, including a recent study by the Congressional Budget Office (CBO). Moreover, this same basic pattern can be seen in data from both the survey-based Panel Study of Income Dynamics (PSID) (which is used in this brief) and the administratively collected Continuous Work History Sample (CWHS) of the Social Security Administration (used by the CBO).

- Contrary to assertions in the popular press, women’s increased workforce participation has not been a major factor contributing to the rise in family income volatility. Female earnings have, if anything, become more stable since the 1980s. Male workers have experienced a larger and more sustained rise in earnings instability. Because men’s earnings account for a larger percentage of total household income than do women’s earnings, on average, rising instability in male earnings helps account for the increase in family income volatility. In short, the stabilizing influence on family income of the decrease in female earnings instability is overwhelmed by the rise in men’s earnings instability.

- In addition to the increase in male earnings variability, other likely causes of rising family income volatility include the growing variability of cash transfers and the limited cushioning effect of having a second earner in the household. Although the evidence is limited, there is reason to believe that a second family earner is less of a benefit in terms of income protection today than it was prior to the 1990s. Indeed, in 2004, if a male worker’s earnings fell, on average his spouse’s earnings fell as well, exacerbating, rather than offsetting, the loss.

- While less educated and poorer Americans have less-stable family incomes than their better-educated and wealthier peers, the increase in family income volatility affects all major demographic and economic groups. Indeed, Americans with at least four years of college experienced a larger increase in family income instability than those with only a high-school education over the past generation, with most of the rise occurring in the last 15 years.

- Finally, levels of family income volatility appear to be extremely high. Family income drops of 50% or greater affected nearly one in 10 non-elderly adults during the early 2000s. Meanwhile, earnings in the United States are also quite variable. The CBO’s recent analysis of earnings variance using the CWHS suggests that around 15% of workers experience a drop in their earnings of 50% or greater every year—a level comparable to what we find using the PSID.

The remainder of this Briefing Paper is divided into five sections. First, it lays out the method used and the approach to the major data issues that researchers working in this area

must confront. Second, the paper presents the main results and shows that the finding of rising family income instability is robust to alternative analytic choices. Third, it demonstrates that—but for a relatively short period in the early to mid-1990s, when the PSID was changing its procedures—the data appear highly representative and reliable. Fourth, it compares these results with other studies, including a forthcoming study of family income volatility from the CBO that purports to find lower levels of and no rise in family income volatility between 1985 and 2002. Fifth, it briefly discusses some of the potential causes of the rising family income instability that are found. It concludes, finally, by drawing out the broader implications of this analysis for contemporary efforts to address deepening public concern about economic security.

Methods

An examination of the instability of a family’s income requires what economists call “longitudinal” or “panel” income data, repeated observations of the income of the same individuals over time (rather than the typical “cross sectional” source of income data, i.e., repeated random surveys of different individuals). The core dataset used in this brief is the Panel Study of Income Dynamics, a highly respected panel income survey that has followed thousands of respondents and their families since the late 1960s—making it the longest continuous panel income survey in the world.2 Until 1996, the PSID data are available on an annual basis.3 Thereafter, they are available every other year. Thus, there are income volatility estimates only for even-numbered years after 1996. For the same reason, the estimates of the frequency of large drops in family income compare family income in a given year to family income two years prior. The last year in this analysis is 2004.

The PSID contains several survey groups, most notably, an original sample that was chosen to be nationally representative and a supplementary sample of low-income respondents. This study follows the lead of past PSID users and combines these two samples, weighting the analyses to ensure representative results using newly available longitudinal weights that consistently correct for attrition from the beginning of the survey.4 This procedure results in data that match up closely with other well-regarded income datasets.

Family income instability can be calculated using various definitions of income and various measures of instability. The original analyses in The Great Risk Shift looked at a comprehensive measure of family income that took into account key non-cash benefits as well as taxes. In the analyses reported in this brief, the focus is limited to pre-tax cash family income, defined as the sum of labor income, asset income, and public and private cash transfers for all members of a family. This makes the results more comparable with recent studies and addresses some data problems with broader income measures.5

The study of family income instability is still in its infancy. Indeed, the analyses that culminated in The Great Risk Shift represented the first examination of the changing instability of total family incomes from the 1970s to the early 2000s.6 In the last decade, however, a large and growing body of research on male earnings instability has emerged, giving rise to several approaches to measuring earnings variability. With appropriate modifications, these approaches can also be used for studying family income dynamics.7

Although family income instability remains less explored than individual earnings variability, it is more crucial for understanding Americans’ economic circumstances. Thanks to the dramatic movement of women into the workforce over the last quarter-century, the vast majority of Americans live in household units where the combined efforts of more than one individual earner add up to total economic well-being. Moreover, earnings are only one revenue stream of several that American families rely upon as income. Public and private transfers and assets also play a critical role. Thus, gaining a full picture of a family’s economic resources requires not only looking at earnings from workers in a family, but also accounting for these non-labor sources of income—neither of which is captured in studies of earnings instability, much less of male earnings instability.

In work on male earnings instability, most scholars have followed the seminal contribution of economists Peter Gottschalk and Robert Moffitt in parsing earnings into so-called permanent and transitory components.8 Permanent earnings is a worker’s long-term earnings level.Transitory earnings is a worker’s short-term earnings level, which reflects temporary shocks to earnings. This basic decomposition can be applied to family income as well. Permanent family income is a family’s long-term income level. Transitory family income is a family’s short-term income level, which reflects temporary shocks to family income, whether those are due to earnings losses, changes in asset or transfer income, or changes in the composition of a family itself.

In turning the analytic lens from individual workers’ earnings to total family income, several issues arise. The most obvious is that family composition can change, affecting both income and the character of a family.9 To deal with this, the analyses that follow all look at the family incomes of individuals, rather than at families taken as a unit.10 As is standard in research that examines family incomes at the individual level, this study adjusts family incomes to reflect the size of the family.11 To minimize the effect of schooling and retirement, the analyses examine only individuals older than 25 and younger than 62.12 All incomes are converted into 2006 dollars using the consumer price index for urban consumers (CPI-U).

In the analyses of family income instability that follow, this study applies the simplest technique outlined by Gottschalk and Moffitt to examine the fluctuation of individuals’ total family income relative to their average family income over four-year periods.13 (Thus, the first estimates are for 1973—four years after the first year of data, 1969.) The resulting values are technically known as the “transitory variance” of family income, but in what follows, they are also referred to as “family income volatility” and “family income instability.” The estimates are in a form familiar to economists, variance of log income.14 Since these numbers can be hard to interpret, we present the results simply as cumulative percentage change in transitory variance since the early 1970s.15

This brief also reports results from two alternative approaches to measuring family income instability. The first, used in several recent studies of earnings and family income instability, is the dispersion of changes in income over short periods of time. Following recent analyses, this study examines the standard deviation of changes in family income from one year to two years later. (Again, the two-year interval is required when using the PSID because of the move in 1996 to biennial surveys.)

This alternative approach, the measurement of the dispersion of short-term income changes, does not attempt to distinguish between persistent and temporary changes in income, as does the Gottschalk-Moffitt technique. Moreover, it requires devising standards for dealing with the asymmetry between gains and losses of the same size when percentage change is the measure. For instance, a drop in income from $1,000 to $100 is a 90% decline, while the return from $100 to $1,000 represents a 900% increase—a massive percentage increase that is likely to be especially influential when estimating the distribution of changes. A variety of potential algebraic solutions to the asymmetry of percent gains and losses are available. In these analyses, we simply use the difference between logged income at two years in time (for example, 19

96 and 1998), which eliminates the asymmetry between losses and gains.16

The second alternative measure is even more intuitive: the chance of large drops in family income from one year to two years later. This study looks at the share of individuals experiencing a 50% or greater loss in family income over a two-year period.

The probability of large short-term drops in family income is perhaps the most intuitive measure of family income instability. Its main disadvantage is its short-term nature—a problem that also plagues the distribution of changes metric. Because these measures rely on only two years of family income data for each individual, they offer little insight into the character of family income shocks. We do not know whether an income drop represents a serious deviation from that individual’s medium-term average income, or rather a return to “normal” following a windfall year. For answering this question, the Gottschalk-Moffitt method is a stronger approach. As reported later in this brief, however, there is little evidence to suggest that the large short-term drops found here represent a return to earth after big upward income swings.

More important, all of these measures—transitory variance, the standard deviation of income changes, and the probability of large income drops—show a substantial increase in family income instability. Moreover, once one takes into account differences in the underlying unit of measurement, they also show relatively similar trends. However you measure it, family income instability has grown substantially.

A final note before moving to the results themselves: While the PSID is a well-regarded data source used by many of the nation’s top social scientists, questions have been raised about the quality of the data in the 1990s, when the survey procedures changed. For most of the PSID’s history, the income reports in the PSID closely match those in other respected datasets, including the Census Bureau’s March Current Population Survey (CPS). Nonetheless, the PSID departs from the Current Population Survey at the bottom of the income distribution for roughly five years in the mid-1990s.17 During this time, the lowest income categories in the PSID have lower average incomes than seen in other income datasets and the overall variance of the PSID income data jumps.

Although the PSID is working to correct these apparent data problems, which are concentrated in a very small number of cases, several features of this analysis reduce their impact on the estimates reported. First, the analyses here begin by dropping all observations with family income of $1 or less. Second, they trim 1 percentile of the income distribution from the bottom and top of the remaining observations. This not only reduces the impact of very low incomes on the estimates, but also has the effect of eliminating concern about the inconsistent treatment of very high incomes in the PSID.18

These adjustments bring the PSID income distribution closely in line with that of other respected income datasets. Nonetheless, they do not completely harmonize the PSID and other datasets at the very bottom of the income distribution in the early to mid-1990s, so estimates for this period should be viewed as less reliable than those for the rest of the series. Thankfully, the PSID dataset with our adjustments matches up extremely well with other datasets at both the beginning and the end of the more than three decades we are examining, giving us considerable confidence in appraising the long-term trend.

Results

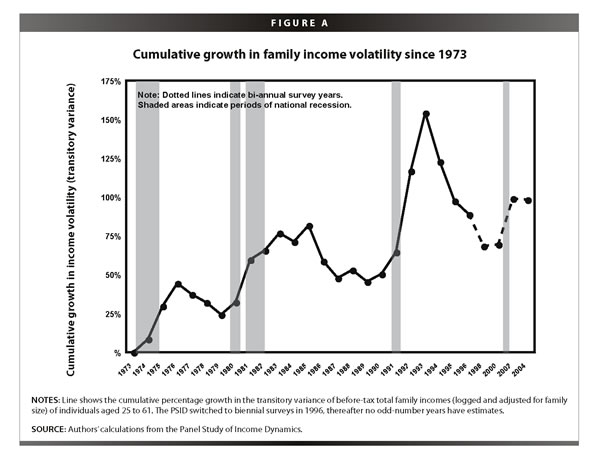

The basic finding of rising family income volatility is summarized in Figure A.19 From 1973 to 2004, the volatility of total family income increased by 99%—essentially doubling over the period.20

Several distinct periods of growth are apparent in Figure A: steady growth through the early 1980s, a flat period in the mid-to-late 1980s, sharp growth in the early 1990s, a dip in the late 1990s, and a slow tick upwards at the turn of the 21st century. The sharpness of the rise in transitory variance during the early to mid-1990s must be viewed with some suspicion due to its coincidence with the major administrative changes in the PSID, as discussed above. Even if it is ignored entirely, however, the overall trend is clear and positive: Income volatility has grown substantially from the early 1970s to the early 2000s.

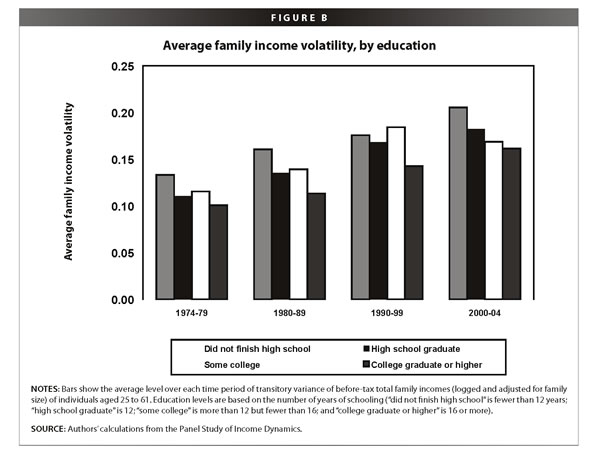

It might be assumed that less-educated Americans are the only ones to face rising family income instability. Yet, as Figure B shows, volatility has risen by roughly the same amount across all educational groups over the full period we examine.

Figure B illustrates that, during the 1980s, working-age adults with less formal education experienced a large rise in family income volatility, whereas those with more formal education saw a more modest rise. Since then, however, family income instability has reached higher and higher up the educational ladder—first touching those who went to college but failed to complete four years, and then spreading to those who had completed four years of college or were even more highly educated. The story of the last few decades is the generalization of the family income instability that once hit mostly the less educated. When it comes to family income instability, more educated Americans are riding the roller coaster once reserved for the working poor.

Other indicators of income volatility suggest the same upward trend over time. Following the lead of a team of scholars lead by Federal Reserve economist Karen Dynan, this report computes the standard deviation of two-year changes in individuals’ family income, using 1971 as a reference point. In 1971, the standard deviation was 37.32; by 2004 it was 56.03. In other words, the standard deviation of changes in income grew 51% in three decades, suggesting that the risk of a large income drop (or gain) is substantially greater today than it was 30 years ago. The lower percentage increase in income volatility using this method, compared with the Gottschalk-Moffitt approach, is mostly because of the differing units of measurement. The standard deviation is the square root of variance. Expressed in terms of standard deviations, the 99% rise in transitory variance found from 1973 to 2004 would be around 40%—very close to what is found using the standard deviation of change metric.

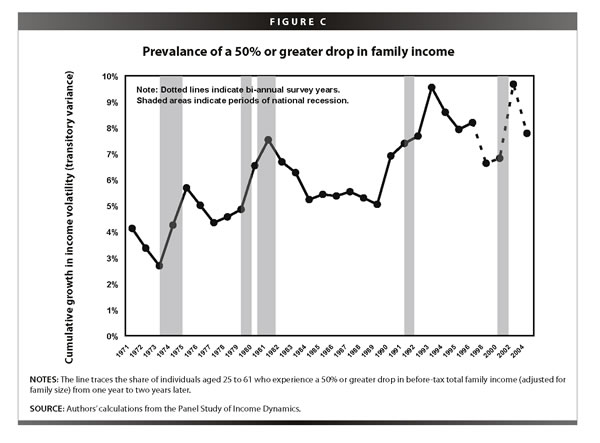

Finally, Figure C details the trend in income instability using a more intuitive measure of income volatility: the share of working-age individuals who experienced a drop in family income of 50% or greater over a two-year period.21 This measure is highly correlated with economic downturns (the shaded portions on the figure), with the risk of large drops increasing when the economy falters and decreasing when it recovers. Nonetheless, the frequency of large income drops trends upward over time, peaking above its previous level during each downturn. In the early 1970s, just over 4% of working-age individuals experienced a drop in their family income of 50% or greater. By the early 2000s, more than 8% did, with the share peaking at nearly 10% in 2002.22

In short, the trend in family income instability is strongly upward whatever measure is used. However, it is also worth emphasizing that family income instability, regardless of the exact degree to which it has increased over the last 30 years, is extremely high. Family income drops of 50% or greater affected almost one in 10 non-elderly adults at their peak during the early 2000s. The share of workers who see earnings drops of 50% or greater is even higher. These are levels of economic instability that are almost certain to cause substa

ntial financial hardship and personal anxiety, especially given how little most Americans have saved to deal with rainy days in their economic lives.

Comparison with other datasets

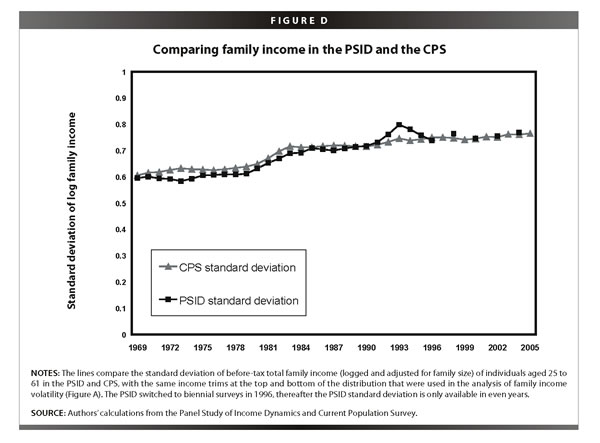

The PSID is the only dataset that allows for the analysis of long-term family income dynamics over the full span of the last generation.23 Does this comprehensiveness come at a major data-quality cost? The answer appears to be no. According to a careful review done in 2000, “PSID data are among the best available on income, wealth, active savings and average annual hourly earnings.” In particular, the PSID “seems to get more accurate reports of the poor income circumstances of lower-income families” (see Kim and Stafford 2000). The comparisons in this study suggest that the family income reports in the PSID closely track both the Census Bureau’s March Current Population Survey and the CBO’s income dataset, which is based in part on administrative tax data and hence considered quite reliable.

Figure D compares the PSID’s family income data for working-age adults with the CPS’s, with adjustments to each to ensure consistency across the two datasets. As can be seen, the two track each other extremely closely.

As noted earlier, the one notable point of incongruence between the PSID and other datasets comes during the 1990s, with the differences most pronounced at the bottom of the income ladder. As the PSID review cited earlier (Kim and Stafford 2000) notes, income observations from 1992 through 1996 “have a higher variance and … this seems to be concentrated in a small number of cases per year….The question is: are these cases real or just data artifacts?” Although the 1991 recession does result in a decrease in incomes at the bottom of the distribution, the sharpness and persistence of the drop strongly suggests that data artifacts do play a role, particularly because the PSID changed its survey administration procedures during the time. As discussed earlier, the treatment of the data here—namely, the dropping of very low income reports—reduces the impact of the small number of questionable observations. Equally important, the problem appears to be largely limited to the early to mid-1990s. By the end of the decade, the PSID once again looks highly representative.24

In short, with the exception of the spike in low-income observations in the mid-1990s that this report attempts to compensate for in the analyses (and which do not provide grounds for questioning the long-term trend), the PSID appears highly representative, lending credence to the finding of rising family income volatility.

Comparison with other studies

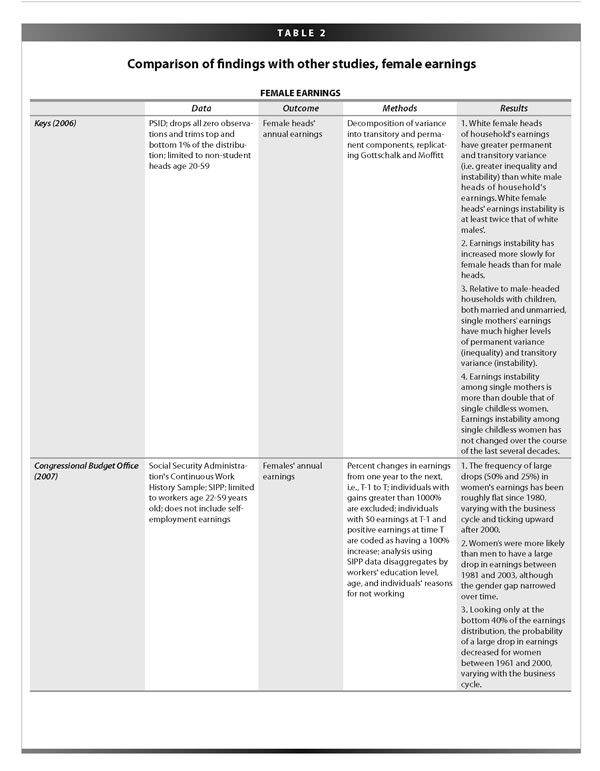

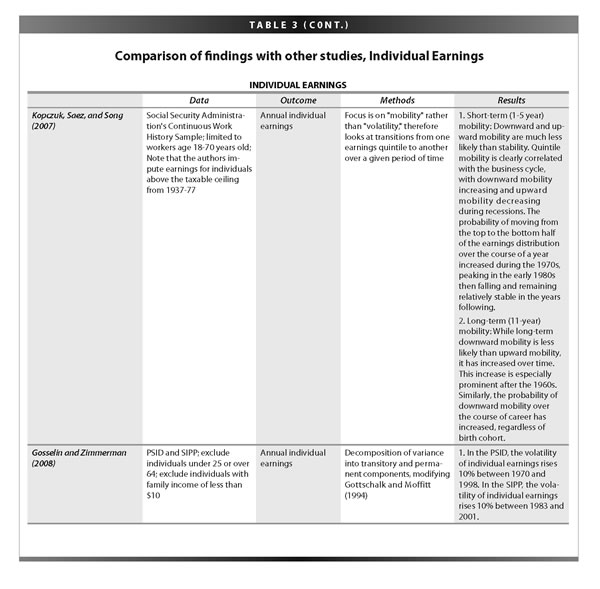

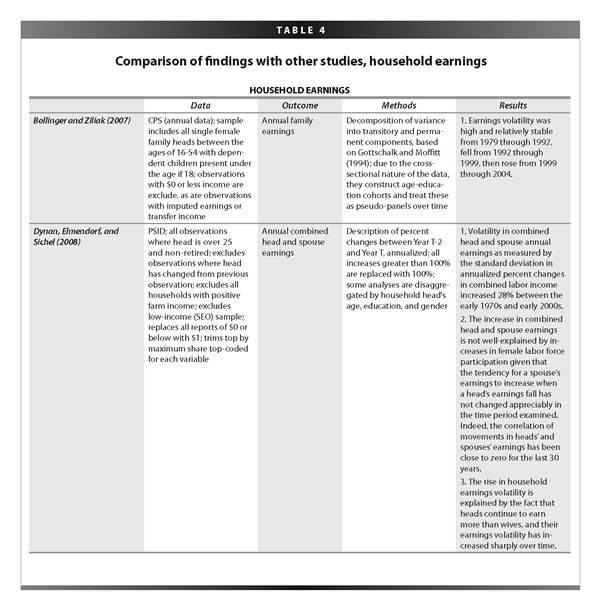

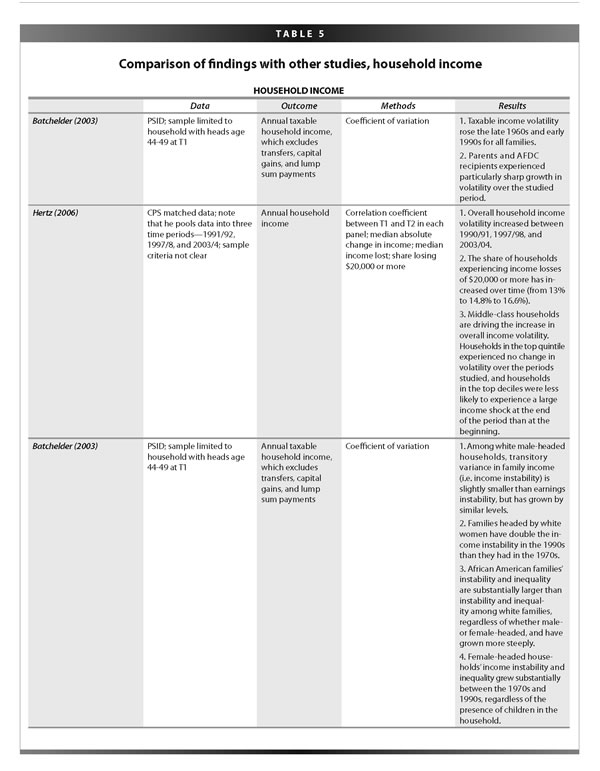

The trends in family income volatility that are found in this brief using the PSID compare closely to recent estimates made by other scholars. Although these other studies are detailed in the appendix to this brief, two deserve particular attention here. In a recent unpublished paper, Peter Gosselin and Seth Zimmerman use a variation of the Gottschalk-Moffitt method and find a 118% cumulative increase in the transitory variance of family income between 1970 and 1998 using the PSID. Given the differences in method and treatment of data, this result is remarkably close to the 99% cumulative increase that is found in this study. Moreover, Gosselin and Zimmerman find a parallel increase in family income volatility between 1983 and 2001 using the Survey of Income and Program Participation, strongly indicating that the rise in family income volatility is not an artifact of the PSID sample.

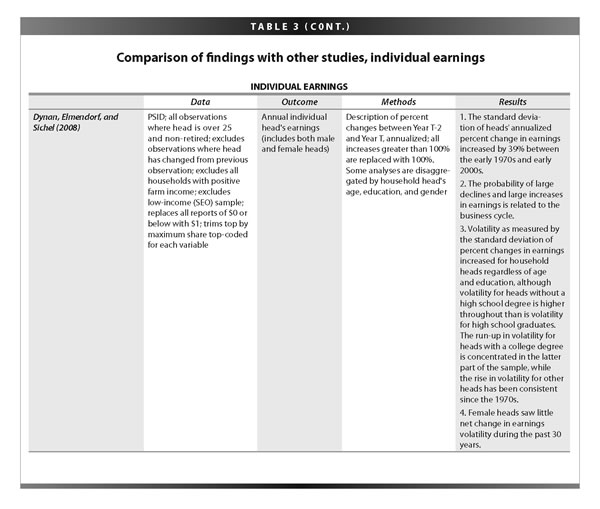

Likewise, a recent working paper by Karen Dynan, Douglas Elmendorf, and Daniel Sichel finds a 36% increase in the standard deviation of percentage changes in family income between the 1970s and the 2000s. Their method is similar to our analysis of the standard deviation of log differences, which found a 51% increase in short-term changes in family income over the same time period. Again, the lower rise in income volatility found in their analysis appears to be mostly because of the differing data choices they make.25

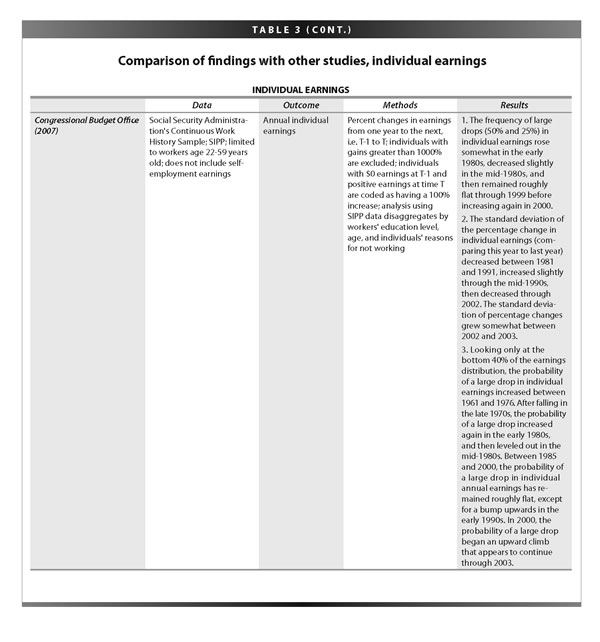

Turning from family income to individual labor income, the PSID also produces results that closely track a recent study by the CBO of earnings instability, based on Social Security Administration’s Continuous Work History Sample (CWHS). This assertion may come as a surprise, because the CBO study has been widely (and incorrectly) taken to indicate that family income volatility has not risen. Yet the CBO analysis is not of family income volatility. It is of individual earnings volatility. (In fact, it is not even of individual earnings volatility, but of wage volatility—because self-employment earnings are excluded.)26 The CWHS only allows for analyses of workers’ earnings—it has no information on family income, and, to the best of our knowledge, does not allow analysts to identify married pairs in order to compute family earnings. The CWHS has extremely limited demographic information (only the age and sex of workers), and it presents obstacles to examining earnings prior to 1978, because data were not collected on earnings that exceeded the upper threshold on Social Security taxation.

Even though the CBO’s analysis is not of family income volatility, we can compare what the CBO finds with comparable analyses of earnings data in the PSID. When we do, we find that the CBO findings are wholly consistent with the results of both older and recent studies that have used the PSID to assess changes in earnings instability—including this report’s analyses of trends in labor income instability using the PSID.

To recognize this consistency, it is important to understand that the CBO study includes the analysis of two samples. First, the CBO tracked individual earnings instability for all workers from 1980 through 2003, a period when Social Security wage data were available for workers regardless of earnings level. Looking at the standard deviation of year-to-year percentage changes in earnings, the CBO found remarkably high levels of earnings instability but little consistent trend in earnings instability for individual workers from 1980 through 2003, except for an upswing in instability in recent years.

Second, the CBO study tracks individual earnings instability for the bottom 40% of workers from 1961 through 2003, extending their analysis to include a period when accurate Social Security wage data were not available for top-earners. In this second analysis, the CBO found that male earnings variability rose between the 1970s and 1980s.

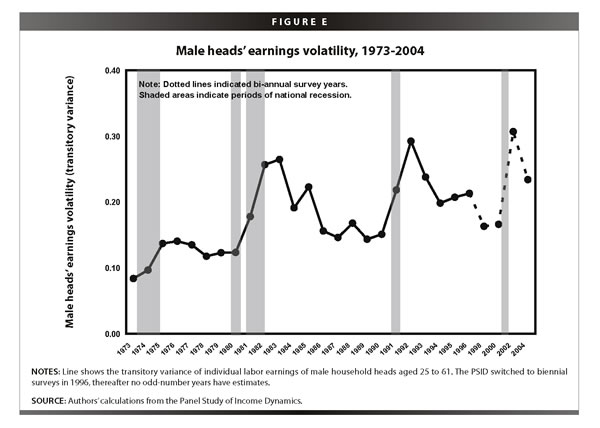

The CBO’s findings are essentially identical to what the PSID shows: generally flat overall earnings volatility since 1980, but a rise in male earnings instability between the 1970s and 1980s. Most analyses of the PSID, including this one, have found that earnings instability has not consistently risen since the deep recession of the early 1980s, when the CBO’s study begins. But all of them, including our own, show that earnings instability—and particularly male earnings instability—rose before the 1980s, as well as trending upward in recent years.27Figure E shows the transitory variance of individual labor earnings for male household heads aged 25 to 62, i.e., earnings volatility for working-age men. Earnings volatility rose quickly in the 1970s and early 1980s, fluctuated up and down with the business cycle between the early 1980s and late 1990s, and then rose again in the early 2000s—exactly the trend found by the CBO study.

Although we examine labor income in a slightly different way than does the CBO (the CBO looks at a slightly younger group of workers than we do, and does not include self-employment income, as we do), the basic results are close.28 For examp

le, the CBO estimates that between 10% and 15% of workers experienced year-to-year earnings declines of 50% or more over the last decade. Our estimates put the share in the same range. (Because of the PSID’s move to biennial surveys in 1996, we must look at earnings drops from one-year to two-years later. Our own investigations have found, however, that the magnitudes of year-to-year and year-to-two-years-later drops track each other closely and are similar in magnitude.)29

More recently, the CBO has indicated that it has examined family income instability from 1984/85 to 2001/02 and, in preliminary results, has found no consistent increase over that period. Because the CBO has provided us with only a basic outline of their findings, data, and methodology, we are unable to fully answer why the CBO analysis diverges from the emerging consensus.30 However, what we know of their analysis indicates that there are four straightforward reasons why the CBO’s findings on income instability differ from all prior analyses—including our own—and why our findings are more likely to be correct.

First, and most important, the CBO utilizes different data than we and the majority of the other volatility scholars do. The CBO study brings together individual earnings data from the Continuous Work History Sample (CWHS), based on Social Security wage records, with longitudinal family income data from the Survey of Income and Program Participation (SIPP). According to those in attendance when the CBO’s preliminary results were presented at the American Economic Association’s annual meeting in early January, the CBO actually found an increase in family income volatility when it used the SIPP data alone. When they matched SIPP records with Social Security wage data from the CWHS, however, the increase disappeared. The CBO justifies its use of the CWHS earnings data with the claim that SIPP earnings reports may be “inaccurate.”31

The use of a different data set alone is not reason to be suspicious of the CBO’s findings. Indeed, it is encouraging to see that interest in the topic of income instability has inspired researchers to use creative strategies in service of advancing our understanding of family economic insecurity. The problem with the CBO’s work lies in the side-effects of their data strategy. By matching SIPP survey data with CWHS administrative data, the CBO throws out a good deal of the sample. According to those who saw the CBO January presentation, the “match rate” between the two datasets declined substantially over time, from 85% in 1985 to just 57% in 2002. It is difficult to believe that nearly half of the SIPP sample was not in employment covered by Social Security. There is thus clear reason to suspect that the CBO’s methods result in the exclusion of thousands of families with “valid” information. It is possible that the excluded cases may also be the most volatile, and thus may account for the fact that when they fold in the administrative data from the CWHS (and throw out the unmatched cases), the CBO finds that the rising family income volatility that they and other scholars find in the unadjusted SIPP data disappears.32

The three remaining explanations for CBO’s anomalous findings are less substantial, but worthy of mention. First, the CBO cuts a significant chunk of observations off of both the bottom and the top of the income distribution (2 percentiles of the distribution) when it analyzes the SIPP, ever after it excludes a sizeable percentage of individuals vis-à-vis the matching process. A key justification for trimming outliers in the PSID is that low or high values caused by measurement error may skew the results, and this convention is followed in this work by making reasonable trims. There is less justification for making such trims when using administrative data, which is arguably more reliable.33 Dropping individuals who have either very high or very low incomes in either of the two years used for the analysis of income dynamics obviously will reduce estimates of volatility substantially.

Second, the CBO study uses 1984 as its baseline for comparison, which is an odd choice since 1984 falls between not one but two national recessions—one of which was the worst economic downturn since the Great Depression. It is odd that the CBO does not provide results for every year between 1984 and 2002, as other scholars who use the SIPP have done, in order to allow a better sense of the dynamics of the results over time. In any case, there is every reason to believe that 1984 represents a local peak in volatility over the 1970-2004 period.

Third, it is difficult to reconcile the CBO’s 2007 findings on individual earnings volatility with their recent findings on family income volatility. In their 2007 findings, the CBO found between 10% and 15% of people experienced year-to-year labor income drops of 50% or greater. In its current analysis, the CBO finds year-to-year family income drops of 50% or greater in only about 4% of cases, which appears quite low and suggests an unrealistic amount of cushioning through government transfers and the work effort of other family members. Moreover, the CBO’s recent results do not include the effect of taxes, which means that the income-buffering impact of the Earned Income Tax Credit is not taken into account. The vast divergence between the CBO’s two sets of results is reason to view the latter with some skepticism.

In sum, with the exception of the CBO’s most recent volley, our results are highly consistent with other recent studies of family income volatility, and the trends in individual earnings volatility in the PSID match closely the trends found in the Social Security administrative data.34

Explaining the rise in volatility

What is driving the substantial rise in family income volatility? Additional studies will be needed to answer this question definitively, but these findings and other recent analyses offer several important clues.

First, the earnings of male workers have become markedly more unstable since the 1970s. This shift is obscured in the CBO study because of the use of 1980 as the baseline for its analysis of all workers—a move necessitated by the limits of Social Security wage records. The early 1980s stand out as the roughest period for workers since the 1970s, rivaled only by the early 2000s.35 It would be hard to find a more turbulent period for workers to establish as the benchmark for whether earnings instability has changed.

If, by contrast, the comparison is between the early 1970s and early 2000s, the rise in male earnings instability becomes undeniable. And because men still contribute considerably more to household income on average than do women, growing variability of male earnings has a major effect on overall family income stability.

Second, transfer income—cash benefits received by families from government programs—has also become more volatile since the 1970s.36 Dynan and her colleagues’ analysis suggests that transfer income volatility of heads and spouses rose by 31% between the 1970s and the early 2000s, using the standard deviation of percentage changes as the metric of volatility (Dynan et al. 2008). Several recent analyses, however, indicate the importance of considering varying causes of income volatility for different income groups, particularly with regard to persistently low-income Americans as compared to their wealthier peers. While the Dynan team finds an overall increase in transfer income volatility as compared to 1970, others have found that transfer income volatility actually decreased in recent years among the poor. For instance, two recent analyses suggest a decline in the volatility of transfers received by the poor after the 1996 welfare reform legislation, mainly because many fewer poor families received cash assistance from the government after 1996. Those remaining recipients of cash assistance may have been more likely to be disabled and therefore beneficiaries of stabl

e and reliable government aid. While transfer income volatility decreased, total family income volatility for low-income families increased substantially during the second half of the 1990s, perhaps because of the move from relatively stable government cash transfers to the highly volatile arena of low-wage work.37

Third, the rising prevalence of two-earner couples does not appear to have provided a big income cushion to families. Family income grew more unstable between 1973 and 2004, even as women entered the labor market en masse and two-earner couples became more common. Two-earner couples should have less income volatility than single-earner families, because they can share income risk across two earners. For instance, if the sole worker in a single-earner family loses his job, the household might incur a 100% income loss. But if the male earner in a dual-earner family loses his job, his wife’s earnings cushion the blow, so the loss might be just 50%. Yet while two-earner couples have become more common, family income volatility has risen—even among two-earner couples.

Beneath the aggregate trend, however, appear two broad eras. From the early 1970s till the mid-1980s, the cushioning effect of a second earner seems to have risen, reflecting the rapid movement of women into the labor force. But since the 1980s, the trend has reversed. In 2004, spouses stepped up their earnings only about a third of the time when household heads’ earnings fell—lower than in any year since 1981. Moreover, the amount by which spouses’ labor earnings offset drops in household heads’ labor earnings appears to have declined since its peak in the mid-1980s. In 2004, in fact, when household heads’ labor earnings dropped by more than 5%, on average their spouses earnings dropped as well.38 Apparently, the cushioning effect of a second earner is reduced when families are already running the two-worker engine at full throttle.

On the other hand, there is little support for the notion that the increased workforce participation of women increases family income volatility. A 2007 report by the think tank Third Way contends that:

…a principal reason for greater income volatility is both simple and benign—motherhood. In the 1970s, a minority of mothers were in the workforce and their pay was relatively low. By the 1990s, a majority of mothers were in the workforce and their pay was much higher. Because women today have a much more prominent role in the economy, their movements in and out of the workforce to take care of children are having bigger impacts on income volatility. When mothers re-enter the workforce, family incomes increase. This also counts as income volatility. (Kim et al. 2007)

This is a plausible claim, but there is no support for it in existing studies of family income volatility. To the contrary, married couples with two earners have lower income volatility than married couples with one earner, and the rise in family income volatility among dual-earner couples has been less steep than the rise among single earners. This suggests that, if anything, the rise in dual-earner families actually helped mitigate the overall rise in income volatility. At the same time, the gender gap in labor earnings volatility has been declining, suggesting that dual-earner couples are actually less likely to lose the wife’s labor income than in the past. Yet family income volatility has continued to rise for dual-earner families, albeit at a slower rate than for other family types. Moreover, preliminary analyses suggest that the birth of a child has the same impact on family income volatility today as it did in the mid-1970s, which makes it difficult to argue that mothers’ movement in and out of the labor force is the key to understanding the rise in family income volatility.

Moreover, the rise in family income volatility is not confined to any one demographic group, such as the poor or poorly educated. Average volatility is higher for women than for men, for African Americans and Hispanics than for whites, for those who never went to college than for those who have a college degree, for younger workers than for older workers, for the poor than for those who are not poor, and for single adults than for married-couple families. Yet the increase in volatility has occurred across all these groups. Indeed, workers with four years of college or more have seen a slightly larger increase in the instability of their incomes than did workers with only a high school education. The rise among more-educated workers, however, mostly occurred in the 1990s and after, whereas family income volatility rose sharply in the 1980s among less-educated workers.

The sharp rise in family income instability among highly educated workers might suggest that instability is driven by “windfall” years when families have a sudden large infusion of income—such as a sizable pay bonus, the capital gains from selling a home, or an inheritance. It is the case that the chance of both upward and downward short-term income shocks has increased; that, after all, is what an increase in income volatility means. But it is not the case that the increased chance of large income drops reflects a growing prevalence of “windfall” years. In fact, excluding from the analysis of income drops those with very large prior income gains has virtually no effect on either the level or the trend.39 The chance of large income drops has risen because people are more likely to tumble down the income ladder than they were in the 1970s, not because they are more likely to enjoy huge income gains in a single year and then ease back to their “normal” income.

Finally, short-term income volatility is distinct from longer-term upward or downward mobility. There is no evidence that long-term mobility—whether absolute mobility or mobility across income groupings or intergenerational mobility—has changed fundamentally during the era in which short-term income volatility has grown. Indeed, recent studies suggest that long-term upward mobility is basically flat, and that intergenerational upward mobility is lower in the United States than other affluent nations.40 The chance of long-term downward mobility may be higher today than in the past—at least when the focus is earnings. But the focus here is short-term income instability, which has clearly increased—a challenge to the ideal of economic security that is a critical part of the American Dream.41

Much work still needs to be done to explain the rising instability of family incomes. The basic trends, however, are increasingly clear: Male earnings have become less stable, and family incomes have followed suit. At the same time, government transfers appear to have become less stable. While many families have gained a second earner, doing so appears to provide less protection against income fluctuations than it did in the past. And the instabilities that were once confined to those with limited education have spread to workers higher up the educational ladder.

Conclusion

Workers and their families are increasingly on an economic roller coaster, shooting upwards in good years and plunging downward in bad. These up-and-down fluctuations are worthy of concern in their own right. Yet they also demand attention because of what they suggest about the American economy: Workers and their families are bearing more risk, even as the macro-economy (as measured by aggregate indicators like growth and inflation) has become more stable. Aggregate statistics provide a less and less reliable picture of what workers and their families are experiencing in their own economic lives.

The rise in family income volatility would be less troubling if it was accompanied by dramatic income gains for the middle class. But, of course, this is not what has happened. According to the comprehensive post-tax income series of the CBO, average family income (adjusted for inflation and including public benefits) among the middle f

ifth of American families rose by 21% between 1979 and 2005. By contrast, the after-tax family income of the richest 1% of Americans increased by 230%. Meanwhile, workers in middle-class families are devoting much more time to paid work, mainly due to the increase work hours of women. Indeed, most of the income gains of the middle class are because of these increased work hours, rather than rising earnings. Even as family incomes are fluctuating more sharply, then, families are working harder for only modestly more income.

A wealth of research in psychology and economics suggest that major income fluctuations create not just financial hardship, but also anxiety and discontent. As economic actors, people are highly “loss averse,” meaning they fear losing what they have far more than they welcome gaining what they do not have.42 Commentators often assume that drops in income are irrelevant if people can maintain their spending. Yet research suggests that a wide range of important outcomes—happiness, child well-being, even, perhaps, obesity—may be worsened by sharp fluctuations in income.43

Moreover, the main way in which Americans maintain their spending—by borrowing—has led to a growing problem of indebtedness, bankruptcy, and home mortgage foreclosure. The personal saving rate has fallen from an average of 9.1% in the 1980s to an average of 1.7% so far this decade. Between the same periods, household debt as a percentage of aggregate personal income essentially doubled, rising from 60% to 100%—and in 2006, aggregate debt approached 120% of aggregate income.44 As a result, middle-class families have strikingly little in the way of liquid wealth with which to deal with short-term income fluctuations. According to a recent analysis of families with incomes between two and six times the federal poverty level and headed by working-age adults, more than half of middle-class families have no net financial assets (excluding home equity), and nearly four in five middle-class families do not have sufficient assets to cover three-quarters of essential living expenses for even three months should their income disappear (essential living expenses include food, housing, clothing, transportation, health care, personal care, education, personal insurance, and pensions).45

Until recently, the constraints on family finances posed by these trends were masked by the strong housing market, which allowed families to borrow against their home equity to finance present spending. But with the recent housing slump and credit crunch driven by the proliferation of risky sub-prime loans, this is no longer a ready option. The late Herbert Stein, chairman of Nixon’s Council of Economic Advisers, once reportedly pronounced that “Things that can’t go on forever, don’t.” Families cannot maintain consumption through borrowing forever, and the bill that eventually comes due can devastate family finances.

Still, income stability is not a direct measure of economic security. Economic security is best thought of as adequate protection against hardship-causing economic shocks that are at least partially beyond personal control. Fluctuations in income obviously cannot capture the risk that large expenses, such as catastrophic medical costs, pose to household budgets. Nor do they say anything about the massive increase in the risks posed by retirement (as responsibility for retirement planning has shifted from employers to workers) or the risks posed by higher education (as the cost of college tuition has skyrocketed and the returns to higher education have become more variable). And short-term income fluctuations provide little insight into the prevalence or severity of long-term downward mobility.46 Future research should delve into all these topics.

Ultimately, no single measure can capture a worker or family’s economic security. The best approach is to use multiple indicators, including, when possible, individuals’ own subjective perceptions of their economic vulnerability.47 Nonetheless, if the measure is income instability, the verdict is clear: Families are facing much greater up-and-down income swings than they did a generation ago. In an era of declining volatility in aggregate economic conditions, Americans are facing much greater economic volatility at work and home. All signs are that they are increasingly anxious about their economic security and looking to their nation’s leaders for fresh ideas and real action.48

—Jacob S. Hacker is professor of political science and resident fellow of the Institution for Social and Policy Studies, Yale University, and a fellow at the New America Foundation. His latest book is The Great Risk Shift: The New Economic Insecurity and the Decline of the American Dream, revised and expanded edition (Oxford University Press 2008). He is also the author of the Agenda for Shared Prosperity Briefing Paper, Health Care for America.

—Elisabeth Jacobs is a fellow in the Multidisciplinary Program on Inequality & Social Policy at Harvard University, where she is a doctoral candidate. Currently a guest at the Brookings Institution, she is also the founder and director of New Vision, an institute for policy and progress.

We would like to thank Frank Limbrock for his indefatigable assistance, and Nigar Nargis, Nancy Hite, and Mario Chacon for help with key data issues. We would also like to thank Jared Bernstein, Karen Dynan, Douglas Elmendorf, Peter Gottschalk, Peter Gosselin, Austin Nichols, Gary Solon, and participants in a workshop organized by the Brookings Institution and Pew Research Centers for helpful feedback and advice.

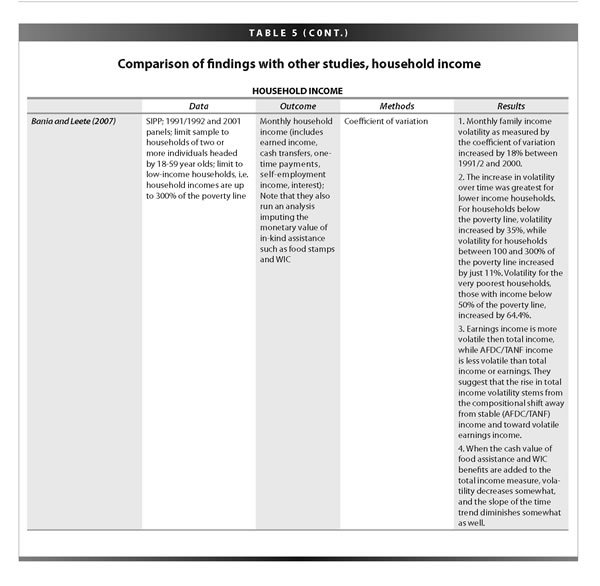

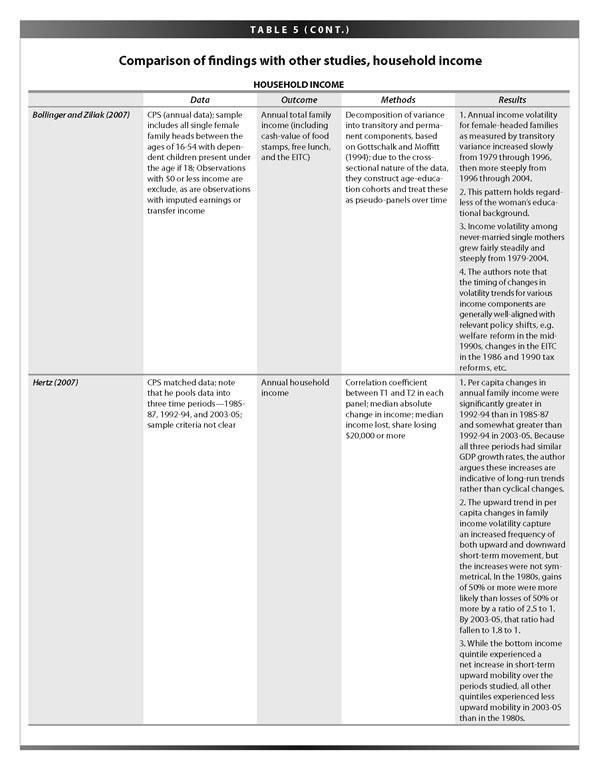

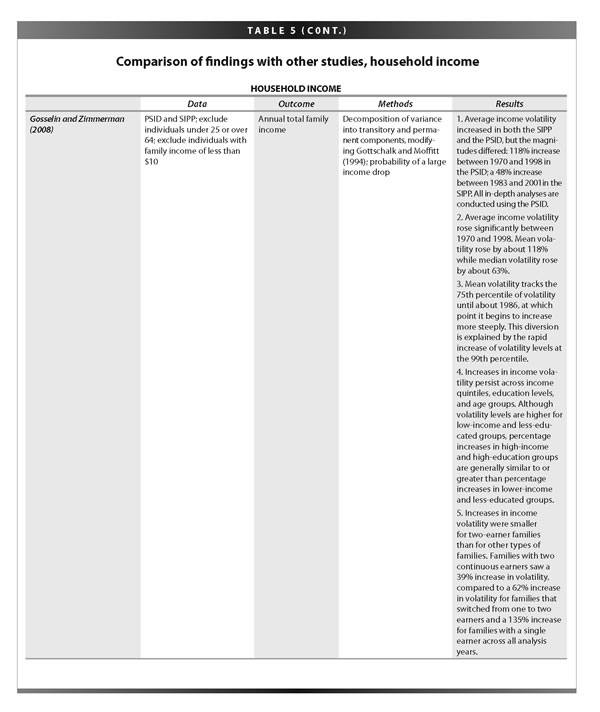

Appendix: Comparison of findings with other studies

Endnotes

1. A forthcoming study by the Congressional Budget Office using different data sources questions whether family income volatility has risen between 1984 and 2002. Based on the limited details of this study that the CBO has made available as of this writing (May 2008), we have serious doubts about its validity—especially given the growing convergence of existing research, even research that has used the same data as the CBO uses. We discuss the reasons for our skepticism in this briefing paper.

2. For further information about the PSID, please consult the study’s excellent Web site: psidonline.isr.umich.edu.

3. In each PSID release, income and earnings data are reported for the year prior. Therefore,

the 1997 release of the PSID includes data on income and earnings for 1996. Throughout this briefing paper, dates refer to the income year, not the survey year.

4. These weights were kindly provided by the PSID in advance of their public release, but we have been assured they will be released without modification soon. It is worth noting that these weights give zero weight to the PSID’s Latino sample, and thus our analyses largely exclude recent Hispanic immigrant groups—an exclusion that arguably dampens the overall rise in family income volatility. Our results are not notably impacted by using the publicly available weights in place of the limited-release test weights.

5. For example, actual tax data are not always available, requiring that taxes be imputed—a potential source of error. Moreover, some data inconsistencies have become apparent in the Cross-National Equivalent File (CNEF), a dataset prepared by researchers at Cornell University from the PSID that was used to obtain estimates of post-tax family income in the estimates reported in the first edition of The Great Risk Shift (Hacker 2006). Thus, we have shifted to using only the PSID’s own reported data, which do not consistently include information on taxes. (Information on the CNEF, a valuable effort to provide comparable data for researchers from national panel income datasets, is available at www.human.cornell.edu/che/PAM/Research/Centers-Programs/German-Panel/cnef.cfm. The CNEF includes imputed tax data based on the National Bureau of Economic Research’s tax simulation model.)

6. For earlier presentations of these results, see Hacker (2004a), Hacker (2004b), Hacker (2004c), Hacker (2006), and Hacker (2008).

7. It is important to emphasize, as Shin and Solon (2008) do, that measures of income instability look at income deviations relative to individuals’ past income, rather than relative to the overall income distribution, which has clearly grown much more unequal during the period under analysis. Thus, it is entirely possible that income volatility has risen even as economic mobility across income quintiles has not fundamentally changed (as argued by, among others, Kopczuk, Saez, and Song (2007)).

8. Another approach, adopted recently by the Congressional Budget Office (CBO) in an important analysis of earnings instability, is to look at the distribution of percentage changes in income from year to year. In the CBO’s case, the metric is the standard deviation of average annual percentage changes. While this approach is sometimes seen as more intuitive and less model-dependent than the Gottschalk-Moffitt technique, we view this assertion as incorrect. The Gottschalk-Moffitt method treats volatility as transitory deviations from long-term income levels, a model that fits well with most people’s intuitive understanding of volatility as short-term income shocks. By contrast, the CBO approach conflates persistent and short-term changes in income. Moreover, the simplest of the approaches suggested by Gottschalk and Moffitt—and the one used in the following analysis—makes few modeling assumptions, except to calculate permanent income levels by comparing two time points that are sufficiently far apart to assume they are not jointly affected by the same transitory income shocks. Meanwhile, the CBO approach requires devising standards for dealing with the very large percentage changes that occur when people go from very low income levels to higher ones; the CBO adopts various rules, sometimes capping these increases at 100%, at others capping them at 1,000%. The other notable difference is that the Gottschalk-Moffitt technique uses log income, which is discussed further in endnote 13. Nonetheless, as discussed below, the basic finding of rising family income volatility does not depend on the technique chosen: While the magnitude of the increase varies somewhat, the finding of rising income volatility is highly robust.

9. For example, a divorce turns one family into two.

10. Thus, we are looking at the fluctuation of a working-age individual’s family income, adjusted for family size. These fluctuations can occur because income changes or because family composition changes. Another approach is to look only at families that do not change composition. This approach is not ideal, as it not only rules out family compositional changes as a source of income fluctuations, but also results in a focus on an unrepresentative sample of the entire surveyed population. Alternatively, one could follow only household heads, as do Dynan, Elmendorf, and Sichel (2008). In this approach, the income effects of separation or divorce are captured in the income of the household head. The effect on the spouse is not captured, because she or he (usually she, as noted shortly) leaves the family, and is then analyzed as a separate “new” family in subsequent years. Unfortunately, this approach also understates the effect of separation or divorce. From its inception, the PSID has automatically assigned men as household heads, except when households are headed by a single woman. Since men still contribute, on average, a substantially larger amount to household income, the income effect of divorce or separation is much smaller for men than for women. Thus, by following usually male household heads, the effect of divorce or separation looks smaller than it would if the analysis followed their spouses or averaged the income effects across the two.

11. The so-called equivalence scale used for this report is the square root of family size, but the results are robust to alternative family-size adjustments, such as the poverty line.

12. Again, the results are not appreciably different if, rather than excluding individuals from the analysis on the basis of age, exclusions are based on whether respondents say they are retired or in school.

13. The results are not appreciably different if six-year periods are used. Five-year periods, which Gottschalk and Moffitt employed in their original study, are not an option because the PSID became a biennial survey in 1996, allowing only even-year intervals for consistent estimates. It should be noted that the move to a biennial survey also limits the ability to implement CBO’s measure of year-to-year income variation. The only analysis to use this measure to look at family income instability, a recent paper by Dynan, Elmendorf, and Sichel (2008), thus looks at percentage changes in income over a two-year interval, rather than from one year to the next. The PSID does not allow for estimates of extremely short-term income volatility—for example, monthly deviations from annual income levels. A recent attempt to carry out such analyses using the Survey of Income and Program Participation (SIPP) (Bania and Leete 2007) finds an increase in such short-term volatility between the early 1990s and early 2000s, especially among low-income households.

14. Logged income is frequently used in economics research and has two favorable properties for analyses of income variance. First, it makes variance mean-independent (i.e., independent of the absolute level of income). Second, it ensures that equivalent increases and decreases in income are treated symmetrically (as they are not when the measure is percentage changes in income).

15. The raw variance numbers and the codes necessary to replicate the analysis presented here are available upon request.

16. The results are not appreciably different when computed using percent differences in raw income, but they are sensitive to the maximum percentage increase allowed. For this reason, the log-difference results are presented.

17. The number of PSID observations with $1 in income—the lowest recorded level for the most comprehensive income variable used in this report—also spikes during this period.

18. Versions of this analysis run with larger percentile trends, e.g. 2% and 3%, give similar results. The level of income volatility is dampened somewhat, but the basic upwa

rd trend is consistent regardless of the chosen trim.

19. This figure differs somewhat in presentation and content from the one in the hardcover edition of The Great Risk Shift (Hacker 2006), though the basic substance and conclusion from both figures are the same. First, Figure A presents an analysis updated through 2004. Second, to avoid some apparent data inconsistencies that have become apparent in the Cross-National Equivalent File (CNEF) prepared by researchers at Cornell University from the PSID—which were used to obtain estimates of post-tax family income in my previous estimates—we have shifted to using only the PSID’s own reported data, which does not consistently include information on taxes. Hence, all these analyses look only at pre-tax family income. (Information on the CNEF, a valuable effort to provide comparable data for researchers from national panel income datasets, is available at www.human.cornell.edu/che/PAM/Research/Centers-Programs/German-Panel/cnef.cfm. Because the PSID has not consistently collected information on actual taxes paid, the CNEF includes imputed tax data based on the National Bureau of Economic Research’s tax simulation model.) Third, we have made some changes to the data analysis to deal with some apparent underreporting of family income in the early 1990s. Finally, to make the results more intelligible, we show the growth in volatility since the baseline year of 1973, rather than the raw volatility levels expressed in terms of over-time variance of log income.

20. Because the apparent data problems in the 1990s appear to be linked to a rise in household heads coded as reporting zero earnings, we also ran the analyses dropping all households in which the head has no labor income yet is reported as employed. The results are essentially identical to those reported here.

21. Because the PSID switched to a biennial survey in 1996, these drops are measured by comparing real family-size-adjusted family income in a given year with its level two years prior. Thus, the first year for which a measure of income drops is available is 1971. Because we are interested in the fullest sample of those who experience large income drops, we do not trim the small number of observations with family incomes of $1 or less for these estimates. Instead, we bump these reported incomes up to $1, which creates a consistent floor on income, a practice known as bottom-coding. At the top of the distribution, the PSID has capped reported income in some years and not others, which could distort comparability of the data over time. Thus, we cap very high income values to create consistent top-coding over time. That is, we identify the year with the maximum share of the sample that is top-coded—around 0.4%—then set all incomes higher than this level at the income level of the 99.6th percentile for every year. The results are very similar if income values of $1 or less are dropped and the top and bottom 1% of observations are trimmed: the levels are slightly lower, but the trend is identical.

22. In this discussion, the “early 1970s” is defined as 1969-71, 1970-72, and 1971-73; the “early 2000s” is defined as 1998-2000, 2000-02, and 2002-04. There were two national recessions during the first period, and one during the second.

23. Future research should also seek to clarify the causes and magnitude of rising family income volatility by looking at alternative sources of income data. The PSID is unique in its combination of true longitudinal family income data (following the same individuals and families over time) and data availability back to the late 1960s. Other sources, however, could supplement and refine its findings. The Survey of Income and Program Participation (SIPP) begins in the mid-1980s and does not provide a continuous panel, but its shorter “mini-panels” (which range from two-and-a-half to four years in length) do allow for analyses of family income volatility and its larger sample size allows for more precise estimates. Recent studies using the SIPP all find a substantial increase in family income instability over the 1980s, 1990s, and early 2000s.

Two other useful but more limited datasets bear mention: the Social Security Administration’s Continuous Work History Sample (CWHS), mentioned earlier in the discussion of the CBO’s recent analysis of earnings variability, and the Census Bureau’s Current Population Survey, which features an extremely large sample, roughly half of which can be used for two-year analyses through statistical matching of households that do not move between surveys. Unfortunately, the CWHS only allows for analyses of workers’ earnings, has extremely limited demographic information (only the age and sex of workers), and does not allow for analyses of all workers prior to 1980. The CPS has a huge sample that allows for over-time matching of around half of households between two successive surveys, with data dating back to the 1960s. Matching is imperfect, however, and only households that do not move are included, making the sample unrepresentative. (Weights can be used to make the sample demographically representative, but not to control for the likely unobserved differences between households that move and those that do not.) Nonetheless, at least one analysis of matched CPS data has focused on short-term income fluctuations. It, too, finds a substantial rise in family income volatility between the early 1990s and early 2000s.

24. Indeed, if anything, its respondents look a bit too rich, rather than too poor.

25. One such choice is their decision to use only the original representative sample of the PSID without weights, which ends up reducing the rise in income volatility, presumably because people with more unstable incomes are more likely to drop out of the sample; without weights, there is no way to correct for this attrition. Another potential reason for the remaining discrepancy is the authors’ decision to follow the family income only of household heads. This ends up understating the effect of separation or divorce on family income. With this approach, the income effects of separation or divorce are captured in the income of the household head. But the effect on the spouse is not captured, because she or he (usually she, as noted shortly) leaves the family, which is then analyzed as a separate family in subsequent years. The reason this matters is that the PSID, from its inception, has arbitrarily assigned men as household heads, except when households are headed by a single woman. Since men still contribute, on average, a substantially larger amount to household income, the income effect of divorce or separation is much smaller for men than for women. Thus, by following usually male household heads, the effect of divorce or separation looks smaller than it would if the analysis followed their spouses or averaged the income effects across the two.

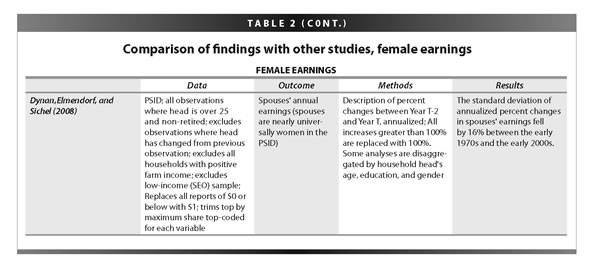

26. At least one paper reports that excluding self-employment income, reported by about 15% of household heads in the PSID, “significantly dampens the uptrend in estimated [earnings] volatility since 1980.” See Dynan, Elmendorf, and Sichel (2008).

27. This includes analyses that use the same method as the CBO (e.g. Shin and Solon (2007); Dynan, Elmendorf, and Sichel (2008)), analyses that use our technique of parsing income variance into transitory and permanent components (e.g., Keys (2006); Gottschalk and Moffitt (2006); Moffitt and Gottschalk (2002); Haider (2001)), and even at least one analysis that applies this technique to the CWHS (Gottschalk and Moffitt (2006)).

28. The CBO analysis looks at workers aged 22 to 59, rather than 25 to 62, as we do. It also examines year-to-year variations, while limits of the PSID require that we look at variation from one year to the year after next.

29. It is worth noting that Dynan, Elmendorf, and Sichel (2008) find substantially smaller earnings drops in their analysis of the PSID, lending further credence to the earlier suggestion that their analytic decisions lead

to an overly restricted sample, and hence may underestimate volatility.

30. Our comments on the CBO’s most recent work on family income volatility are based on personal communication with staff members of the CBO. While we are grateful for the information they have shared thus far, we have requested more detail on their analysis, including a copy of their working paper. Because the devil is in the details when it comes to the study of income volatility, the information they have provided is not sufficient for us to fully interpret their findings. We continue to await a substantive response.

31. In particular, the CBO is suspicious of all SIPP respondents for whom earnings are imputed—the SIPP replaces missing data with estimated values in order to ensure that missing data do not skew the distribution of income and other critical variables in the dataset. However, the imputed data do not show higher volatility than the non-imputed data, according to those who saw the CBO presentation in January. This runs strongly contrary to the suggestion that imputation in either the SIPP or the PSID are leading to the finding of rising volatility.

32. One reason to suspect that the data matching procedure is behind the CBO’s divergent findings is that, according to the only existing study of family income volatility in the SIPP (Gosselin and Zimmerman 2008), the SIPP shows a very modest rise in the volatility of earnings between 1984 and 2002, around 10%, and a sharp rise in the volatility of family incomes over this period, around 50%. It is worth noting that these numbers are consistent with our and other researchers’ findings using the PSID. Moreover, the Gosselin-Zimmerman findings suggest that the rise in family income volatility in the SIPP is not driven by rising earnings instability. This makes it odd that simply substituting earnings records from Social Security would cause the rise in family income to disappear. The more likely reason why the CBO’s substitution of earnings data makes a difference is the exclusion of the most volatile households.

33. We note that administrative data is “arguably” more reliable because scholars have raised questions about the reliability of even Social Security wage records. For example, see Hotz and Karl (2001).

34. Donggyun Shin and Gary Solon (2007) reiterate this point regarding the broad consistency of results across data sources in a recent unpublished working paper, which applies yet another variation of the Gottschalk-Moffitt metric and finds similar results to ours for trends in male earnings volatility.

35. Using the Displaced Worker Survey, for example, Henry Farber (2007) finds that the earnings losses associated with involuntary displacement were actually higher in 2001-03 than in 1981-83.

36. These benefits do not include the Earned Income Tax Credit, because the PSID provides only pre-tax income.

37. For analyses of the volatility of transfer income, see Bania and Leete (2007); Bollinger and Ziliak (2007); and Dynan, Elmendorf, and Sichel (2008).

38. Calculations are based on preliminary analyses of the PSID. Details are available from the authors upon request.

39. Results available from the authors upon request.

40. For details on trends in long-term mobility, see Kopczuk and Saez (2007).

41. Part of the reason for this is rising economic inequality. Many studies of mobility look at the chance of moving from one quintile of earnings or income to another. As the gap between quintiles grows, however, these “transitions” (as they are called in mobility research) imply larger changes in income. Thus short-term mobility across income quintiles may not rise even as short-term income volatility does. The former looks at changes relative to other people’s current incomes. The latter looks at changes relative to one’s own past income—which for most people thinking about their short-term economic security, is arguably the more relevant standard.

42. Even opportunity-loving Americans share this fundamental predilection: In a 2005 poll by Lake Snell Perry Mermin, more than two-thirds said they would prefer the “stability of knowing your present sources of income are protected” than the “opportunity to make more money.”

43. For more detail on the relationship between socio-economic well-being and income security, see Kalil and Ziol-Guest (2008); Kalil and Ziol-Guest (2005); Smith, Trenton, Stoddard, Christina, Barnes, Michael (2007); and International Labour Office (2004).

44. For more detail, see Dynan and Kohn (2007).

45. See Wheary, Shapiro, and Draut (2007).

46. Research on the long-term costs of job displacement suggests that income volatility rooted in earning shocks can have persistent and pernicious impacts on individuals’ long-term economic prospects. For instance, a study by Huff Stevens (1997) finds that earnings remain 9% below their expected levels six or more years after an involuntary job loss.

47. With support from the Rockefeller Foundation, Hacker is currently heading a research project that aims to do just this. Building up from the best available data, the project will produce a new Rockefeller Economic Security Index (RESI) and will provide the first comprehensive measure of family economic security that can be used to compare individuals and families with different characteristics and chart changes in economic security over time.

48. According to recent surveys, Americans overwhelmingly believe that they are facing greater economic risk and that future generations will face even greater risk. See MetLife (2007); Rockefeller Foundation (2007).

References

Bania, Neil, and Laura Leete. 2007. Income Volatility and Food Insufficiency in U.S. Low-Income Households, 1992-2003. Institute for Research on Poverty Discussion Paper No. 1325-07.

http://www.irp.wisc.edu/publications/dps/pdfs/dp132507.pdf

Batchelder, Lily L. 2003. Taxing the poor: Income averaging reconsidered. Harvard Journal on Legislation. Vol. 40, No. 395.

Bollinger, Christopher, and James P. Ziliak. 2007. Welfare Reform and the Level, Composition, and Volatility of Income. Mimeo.

http://www.ukcpr.org/SeminarSeries/Ziliak-Bollinger_WelfareReformandVolatility_032007.pdf

Brooks, David. 2007. Who’s afraid of the New Economy? New York Times. February 11, 2007.

Cameron, Stephen, and Joseph Tracy. 1998. Earnings Variability in the United States: An Examination Using Matched-CPS Data. Mimeo.

http://www.newyorkfed.org/research/economists/tracy/earnings_variability.pdf

Comin, Diego, Erica L. Groshen, and Bess Rabin. 2006. Turbulent Firms, Turbulent Wages? Federal Reserve Bank of New York Staff Reports No. 238.

Congressional Budget Office. 2007. Trends in Earnings Variability Over the Past 20 Years.

http://www.cbo.gov/ftpdocs/80xx/doc8007/04-17-EarningsVariability.pdf

Daly, Mary C., and Greg J. Duncan. 1997. Earnings Mobility and Instability, 1969-1995. Mimeo. Working Paper in Applied Economic Theory. San Francisco: Federal Reserve Bank of San Francisco.

Dynan, Karen, Douglas W. Elmendorf, and Daniel E. Sichel. 2008. The Evolution of Household Income Volatility.

http://www.brookings.edu/~/media/Files/rc/papers/2008

/02_useconomics_elmendorf/02_useconomics_elmendorf.pdf

Dynan, Karen E., and Donald L. Kohn. 2007. The Rise i

n U.S. Household Indebtedness: Causes and Consequences. FEDS Working Paper 2007-37.

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1019052

Farber, Henry. 2007. Job Loss and the Decline in Job Security in the United States. Working Paper #520. Princeton, N.J.: Princeton University, Industrial Relations Section.

http://irs.princeton.edu/pubs/pdfs/520.pdf

Gosselin, Peter, and Seth Zimmerman. 2008. Trends in Income Volatility and Risk. Prepared for the APPAM Fall Research Conference.

http://www.urban.org/UploadedPDF/411672_income_trends.pdf

Gottschalk, Peter, and Robert Moffitt. 1994. The Growth of Earnings Instability in the U.S. Labor Market. Brookings Papers on Economic Activity. Washington, D.C.: Brookings Institution. p. 217-72.

Gottschalk, Peter, and Robert Moffitt. 2006. Trends in Earnings Volatility in the U.S.: 1970-2002. Prepared for presentation at the Annual Meeting of the American Economic Association.

Hacker, Jacob S. 2004a. Call it the family risk factor. New York Times. January 11, 2004.

Hacker, Jacob S. 2004b. Privatizing risk without privatizing the welfare state: The hidden politics of social policy retrenchment in the United States. American Political Science Review. Vol. 98, No. 2, pp. 243-60.

Hacker, Jacob S. 2004c. False positive: The so-called Good Economy. The New Republic. Vol. 16, No. 23 August.

Hacker, Jacob S. 2008. The Great Risk Shift: The New Economic Insecurity and the Decline of the American Dream. Rev. and Exp. Ed. Oxford University Press.

Hacker, Jacob S. 2006. The Great Risk Shift: The Assault on American Jobs, Families, Health Care, and Retirement—And How You Can Fight Back. Oxford University Press.

Haider, Steven J. 2001. Earnings instability and earnings inequality of males in the United States: 1967-1991. Journal of Labor Economics. Vol.19, No. 4, pp. 799-836.

Hertz, Tom. 2006. Understanding Mobility in America. Center for American Progress Research Paper. Washington, D.C.: CAP.

Hertz, Tom. 2007. Changes in the Volatility of Household Income in the United States: A Regional Analysis. Mimeo prepared for the Brookings Institution Metropolitan Policy Program. Washington, D.C.: Brookings Institution.

Hotz, V. Joseph, and Scholz, John Karl. 2001. “Measuring Employment and Income for Low-Income Populations with Administrative and Survey Data.” In Michele Ver Ploeg, Robert A. Moffitt and Constance F. Citro, eds., Studies of Welfare Populations: Data Collection and Research Issues. Committee on National Statistics/National Research Council.

Huff Stevens, Ann. 1997. Persistent effects of job loss: The importance of multiple job losses. Journal of Labor Economics. Vol. 15, No.1, pp. 165-88.