Briefing Paper #202

Job loss, worker dislocation, and economic insecurity are continuing features of the U.S. labor market. This holds even as the overall unemployment rate during 2007 has hovered in the 4.5-4.7% range, nearly a full percentage point below its average of the past 20 years. Each year about 30 million new spells of unemployment occur, more in recessions. Each year, more then 1 million workers with three or more years of tenure at their companies are terminated with no prospect of returning to their former jobs.

Congress has offered major legislative proposals in 2007 to address the problems confronting unemployed and dislocated workers. A bill to “modernize” unemployment insurance (UI) with bipartisan sponsorship has been introduced by Senator Edward Kennedy in the U.S. Senate,1 and a UI modernization bill has been introduced by Representative Jim McDermott in the House of Representatives.2 Bipartisan proposals to reauthorize the Trade Adjustment Assistance (TAA) program have been introduced by Senator Max Baucus3 and Rep. Charles Rangel. These legislative initiatives would broaden the scope of the UI and TAA programs.

Both the Rangel and the Baucus TAA bill include provisions that would provide wage-loss insurance payments to certain workers dislocated by international trade and by technological change. Upon reemployment, workers would receive a payment that partially reimburses them for the loss of wages when their post-displacement job pays lower hourly wages than their previous job. While a limited degree of wage insurance is already available to some workers age 50 and older dislocated by international trade under current TAA provisions, the Baucus bill would expand wage insurance to a broader age group and more situations of worker dislocation.

This paper examines UI reform and wage insurance from a critical perspective. A prominent advocate of UI reform and wage insurance is Dr. Jeffrey Kling of the Brookings Institution. He testified recently in hearings before a subcommittee of the House Ways and Means Committee and advocates UI reform where individual UI accounts and wage insurance feature prominently.4 Kling’s UI reform proposal would institute a system with individual UI accounts for each worker and wage-loss insurance for experienced workers displaced from jobs by technological change and international trade. The individual accounts would be the source for most income support payments to the unemployed. Employer payroll taxes would finance the wage insurance payments.

This analysis of Kling’s reform proposal reaches the following conclusions:

1. The wage insurance program that he offers provides very modest income support because of its restrictions on eligibility and its low replacement rate among recipients (25% or less).

2. His proposal for individual UI accounts claims to generate savings by squeezing out “fat” among current UI recipients who have short-term unemployment. In fact, it is likely to generate little or no savings, and the consequence of shifting to individualized accounts is likely to weaken protections for the unemployed and weaken the counter-cyclical performance of the present UI system.

3. No necessary connection exists between providing wage insurance and instituting a system of individualized UI accounts other than to potentially save money on one to spend on the other. In fact, Kling is asking one set of ‘losers,’ the short-term unemployed, to compensate another set of ‘losers,’ the displaced, experienced workers who accept lower-paying jobs.

4. If the purpose of wage insurance is to cushion the fall in income among those displaced due to economic change, it is not readily apparent why such a program should be funded by cutting UI costs for other unemployed workers rather than, say, from general revenues generated by those on the winning side of change and associated income growth.

5. Additionally, if more resources are to be injected into the UI system, there are other groups in the system that can be considered to be of equally high or higher priority, e.g., part-time workers and low-wage workers.

Before examining details of the Kling proposal, this paper describes the current UI program, noting both its strengths and weaknesses in providing temporary, partial income support to unemployed workers and automatic macroeconomic stabilization for the economy. Several current limitations on benefit availability are identified. Changes that would improve access to benefits include instituting an alternative base period, increasing eligibility among part-time and low-wage workers, and reducing interstate differences in recipiency rates. Some of these changes are included in current proposals to modernize UI such as providing financial incentives to institute an alternative base period and improved access to benefits for part-time workers.

This paper then describes Kling’s reform proposal and offers observations and critical comments about the proposal. A concluding paragraph highlights a few main points.

A central tenet of the Kling proposal is that by moving to individual accounts, savings in benefit payments will be realized, which can then finance a program of wage-loss insurance with no increase in total costs compared to the present UI program. He asserts that wage-loss insurance will help cushion the drop in income among displaced workers who find new jobs at wage rates below the wage rates of their pre-displacement jobs. In effect, he suggests that the fat in the current UI system can be squeezed out and the savings can be redirected to new recipients without increasing total UI program costs.

This recent experience of UI reform in Chile is reviewed to provide a critical perspective (based on actual experience) on the likelihood of realizing substantial savings in moving to a system with individual UI accounts. The following section offers other critical comments about establishing a UI system that relies mainly on individual accounts to provide income support to the unemployed. Administrative problems in such a system may be more serious than suggested by Kling’s proposed reform.

Unemployment insurance in the United States as currently structured needs to be reviewed and reform proposals must be entertained. Some worthy reform proposals are included in legislation currently before the Congress. However, the framework provided by the present system of state-administered, employer-financed programs can be modified to address the current limitations of UI. Reforms that would increase recipiency should be entertained and several potential areas for reforming benefits are identified in this paper. Moving to a UI system with individual accounts is not necessary or desirable.

The current unemployment insurance system

State unemployment insurance programs have been providing cash benefits to eligible unemployed persons for seven decades. A long-established social insurance program created under the Social Security Act of 1935, UI has been studied and evaluated from a variety of perspectives. Its tax and benefit statutes and administrative procedures try to achieve a balance among three competing program goals: 1) providing adequate benefits to eligible claimants, 2) controlling total program costs and associated employer payroll taxes, and 3) limiting the labor market distortions caused by receipt of benefit payments.5

Since UI programs were first established in the mid-1930s, the e

conomy and the labor market have undergone several profound changes. A continuing challenge is to have UI evolve appropriately as the U.S. economy continues to grow and change.

Recently a proposal to “reform” UI has been made by Jeffrey Kling as part of a set of social protection reform proposals by the Hamilton Project. His proposal has three components: 1) wage-loss insurance for dislocated workers, 2) UI savings accounts (termed temporary earnings replacement accounts or TERAs), and 3) low-wage co-insurance to help defray the costs of UI benefit payments made to persons with very low hourly earnings. Details of the Kling proposal will be discussed below.

Before initiating that discussion, however, it seems appropriate to describe UI and discuss the strengths and limitations of UI as the programs currently operate in the states. This discussion is not offered as a comprehensive treatment, but as an overview that highlights the strengths and weaknesses of the present state UI programs.

State unemployment insurance programs

State UI programs are of limited scope. So-called regular UI, which is state-financed and state-administered, can provide up to 26 weeks of benefits to an unemployed person during a given 12-month period (termed a benefit year). Payment levels are modest with maximum weekly benefits that usually range between 35% and 65% of statewide average weekly wages and a statutory replacement rate that usually ranges from 50% to 59% of prior wages.6 More than 30% of all claimants have potential benefit entitlements of fewer than 26 weeks during a given benefit year. Thus payment levels and potential duration are accurately described as modest.

The limited scope of UI is reflected in program benefit statistics. Recipients of regular UI typically represent 33-37% of total unemployment during a non-recessionary year. In recent years, at least one-third of all claimants have exhausted their full entitlement, and the exhaustion rate exceeded 0.40 of all claimants during the recent high unemployment years 2002 and 2003. Recipiency varies widely across the states—above 40% in states like Massachusetts, Pennsylvania, Wisconsin, and Oregon but usually below 20% in Arizona, Florida, Georgia, Texas, and Virginia. Low-wage workers are much less likely to collect benefits than those with middling and high earnings. UI recipients are usually job losers who are experienced workers. Recipiency is not common among the unemployed who are job leavers and labor force reentrants. Workers under the age of 20 rarely collect UI. In short, the majority of unemployed workers do not collect UI benefits, and among recipients most are adult job losers.

Low recipiency also means the employer payroll taxes that support UI are not very high. Employers typically spend much larger amounts on health insurance, social security (old age and disability), private pensions, workers’ compensation, and even Medicare than they spend on UI.7

UI benefits continue to perform an important countercyclical role in the economy. During the 2001 recession, annual payments of regular UI benefits increased from about $20 billion per year in 1999 and 2000 to $30 billion in 2001, $40 billion in 2002 and 2003, and $30 billion in 2004. Temporary federal benefits paid during 2002 and 2003 totaled about $10 billion each year, so that total UI support payments were approximately $50 billion in both 2002 and 2003, more than double annual payments during the pre-recession years 1999 and 2000. An even stronger countercyclical response of benefit payments occurred during the recessions of 1975, 1980-82, and 1991.

The full structure of UI benefits has three levels or tiers of benefit payments. Regular UI can pay up to 26 weeks of benefits. It is financed by state-administered payroll taxes on employers with contributions and payouts flowing through individual state trust fund accounts maintained at the U.S. Treasury. Individual states administer payments, making decisions that affect eligibility, payment levels, and benefit duration.

The second tier is the Federal-State Extended Benefits (EB) program that can provide up to 13 additional weeks of benefits to persons who exhaust regular UI in periods when state unemployment is sufficiently high to trigger the EB program. The financing of EB is equally shared by the federal and state partners. Since the EB triggers were substantially modified in the early 1980s, however, the program has been of very limited scope.

The highest payout year for EB during the recent recession was 2003 with only $368 million in EB compared to $41.1 billion of regular UI and $11.0 billion of temporary federal benefits (Temporary Extended Unemployment Compensation or TEUC), the third tier of benefit payments.

Temporary federal benefits are fully financed by the federal partner. Some form of temporary federal benefit program has been enacted in every recessionary period extending back to the late 1950s. Emergency federal legislation has created these temporary federal programs that automatically sunset in the late stages of a recession. Because of the decreasing importance of EB, temporary federal benefits have provided the main form of extended benefits to exhaustees in each recessionary year since 1983.

All three tiers of benefit payments are administered by the states. Because EB and temporary federal benefits utilize the same administrative apparatus as regular UI, the system can implement payment of extended benefits quickly and efficiently.

Two evolutionary changes in the U.S. labor market have implications for the UI program: the aging of the labor force and the declining importance of temporary layoffs. As the baby boom generation has matured, the age composition of the labor force, employment, and unemployment have also changed. During the early 1970s, for example, half of the unemployed were persons aged 16 to 24. By 2006, their share had decreased to one-third. Because more of the unemployed are now older, experienced workers, they are more likely to have sufficient earnings to be eligible for UI. Older persons also experience longer spells of unemployment when compared to younger persons, and the differential contributes to the increase in average unemployment duration observed in data from the monthly labor force survey of households and in UI claimant data.

A second major change has been the decline in the importance of temporary layoffs.8 Typically during a recession, those on temporary layoff become a much larger share of total unemployment compared to non-recessionary periods. This pattern was present during the recessions of 1974-75 and 1979-80. However, a similar pattern was not observed during the recessions of 1991 and 2001. During the past two recessions employers have resorted to permanent layoffs to a much greater extent and to temporary layoffs much less often than in the past.9 Those on permanent layoff often experience difficulty in securing a new job.

Both changes are important for UI since both increase the average duration of unemployment spells and the associated need for UI benefits by persons experiencing long unemployment spells.10 The mean duration of unemployment in the monthly labor force survey has increased from 11.7 weeks during the 1950s to 15.7 weeks during the 1990s. Increasing duration of unemployment is also reflected in UI program data. Average duration was 12.0 weeks in the 1950s compared to 14.9 weeks in the 1990s. The average benefit exhaustion rate increased from 25.2% in the 1950s to 35.5% in the 1990s. Long duration unemployment spells have become much more common in recent decades in various labor market data series.

Key UI benefit provisions—like base period earnings requirements, maximum potential benefit duration, the waiting period, the statutory replacement rate, and the linkage between base period earnings and potential benefits—are all determined by the states. In many ways, however, benefit provisions are

quite similar. Across the state programs all but two have a maximum duration of 26 weeks with higher maxima present only in Montana (28 weeks) and Massachusetts (30 weeks). Washington reduced its maximum duration in 2004 from 30 weeks to 26 weeks. The federal partner plays only a small role in determining benefits for regular UI. Its role is restricted mainly to ensuring prompt and accurate administrative decisions regarding coverage and eligibility among persons who file claims for benefits.

While benefit provisions are controlled mainly by the states, there is considerable year-to-year continuity in the benefit provisions within individual states. Changes may occur automatically such as increases in the maximum weekly benefit, which take place in about two-thirds of states where the maximum is indexed to average earnings. Other provisions such as base period earnings requirements typically change legislatively.

In recent years, some benefit changes have been motivated by a desire to increase access to benefits. Most obvious has been the enactment of the alternative base period (ABP) by several states for determining monetary eligibility. Having an ABP allows the UI agency to use more recent earnings when a claimant is found to be monetarily ineligible based on earnings during the standard base period (usually the earliest four completed quarters of the past five completed quarters). The ABP is usually the past four completed quarters, meaning the most recent completed quarter is used to determine eligibility rather than the same quarter from one year earlier. In 2006, 19 states had an ABP, and the ABP has been shown to increase access to benefits among workers with low wages and irregular quarterly earnings. All 19 ABP adoptions have occurred since 1987. Typically the ABP causes the recipiency rate (the ratio of beneficiaries to total unemployment) to increase by 4 to 8 percentage points while benefit payouts increase some 3 to 5 percentage points. The ABP has definitely improved access to benefits among low-wage workers.

Overall, however, access to benefits is limited by a combination of factors that include short potential benefit duration, restrictive interpretations of “good” reasons for quitting (particularly what constitutes good or compelling personal reasons), and restricting UI eligibility to just persons seeking full-time jobs. Across the high-income developed economies of the world, the UI recipiency rate in the United States is similar to recipiency rates in Greece, Italy, Spain, Japan, and Canada, in other words, among the lowest.11

Strengths and weaknesses of the present UI system

During the past 40 years I have conducted several studies of UI programs in the United States both from a national perspective as well as the programs in several individual states. The projects have examined benefits, financing, and program administration. Based on this past research, three strengths and three weaknesses of these programs are especially noteworthy:

Strengths

1. Countercyclical performance. When the economy enters a recession and unemployment increases, UI benefit payments increase automatically. The automatic stabilizer aspect of the program response occurs without legislation, although enactment of temporary federal benefit programs does strengthen the countercyclical response. Payments increase strongly at a time when families and individuals need the payments. The increase in annual payout from roughly $20 billion in 1999 and 2000 to about $50 billion in 2002 and 2003 is the latest example of the strong cyclical responsiveness.

2. Low costs. The cost of the employer payroll taxes (as a percent of payroll) that support benefit payments is low. The average nationwide cost rate for employers during 2000-05 was 0.64% of payroll, considerably below the 1947-2005 average of 0.96%. Among the 21 high-income OECD countries with populations of at least 1 million persons, UI benefit costs as a percent of payroll are lower only in Greece and Japan. The American UI system is simply not very expensive.

3. Appropriate cost assignment. The United States is unique in using experience rating to assign the costs of UI benefit payments to individual employers. Firms where benefit payments to current and former employees are higher generally pay higher experience-rated UI taxes. Experience-rated UI taxes make employers more aware of the costs of layoffs and have a deterrent effect on layoffs. The current UI taxing system assigns roughly 60% of the costs of benefits back to employers who initiate layoffs. While many advocate making changes to increase the degree of experience rating, e.g., raising the maximum UI tax rate, the deterrent to layoffs is certainly higher than in other economies where UI is supported by payroll taxes levied at a single tax rate. Outside the United States, higher benefit payments have no effect on the UI tax rates of individual employers.

Weaknesses

1. Low recipiency. Many unemployed workers with substantial recent work experiences do not collect UI benefits. Between 2000 and 2004 the UI benefit recipiency rate averaged 38.6% nationwide. This average includes substantial payouts of temporary federal benefits in 2002 and 2003. During the nonrecessionary period 1995-99, the recipiency rate averaged 30.7%. In the 60 years between 1947 and 2006 the recipiency rate across all three tiers of UI benefits exceeded 50% in only four years: 1958, 1961, 1975, and 1976. All four years were recession years with high unemployment, and all are now at least 30 years in the past. Recipiency in the United States has been consistently restricted to a minority of unemployed workers except in periods of high unemployment.

2. High benefit exhaustion rate. Among recipients of benefits, a large increase in the exhaustion rate has taken place. The exhaustion rate for regular UI that averaged 25.2% in the 1950s, averaged 37.6% during the first seven years of the present decade. This increase in the exhaustion rate has occurred while the generosity of UI weekly benefit payments has not changed noticeably. The replacement rate (weekly benefits divided by weekly wages) at the national level did not deviate from 34.5% by more than 4.0% in any year between 1947 and 2006. In the payment of weekly benefits, the UI system has not become more generous while the rate of disputes over eligibility has trended upward and the potential duration of benefits has not changed since the late 1950s. The increased duration of benefit payments per claimant is due to developments in the labor market, e.g., the aging of the labor force and the decline in the use of temporary layoffs discussed previously, not developments in UI that have made it more attractive to receive benefits.

3. Disincentive effects of UI benefits. Programs like UI that provide cash income transfers to eligible persons do experience disincentive effects. Three disincentive effects of UI have received considerable research attention: 1) effects on unemployment duration, 2) effects on applications for UI benefits (or take-up), and 3) effects on temporary layoffs. Note that the first two effects refer to aspects of worker behavior while the third refers to employer behavior in decisions to terminate workers.

In 2004, a review of the disincentive literature concluded that the disincentive effects of UI are relatively small and have not grown in recent years.12 That report can be summarized as follows: 1) Increasing the potential duration of benefits as occurs during recessions through activation of long-term benefit programs (Federal-State Extended Benefits and/or temporary federal benefits) does increase actual benefit duration. The parameter that shows the response of actual duration to increased potential duration, however, is generally estimat

ed to be in the 0.10-0.20 range. Increased potential duration of 13 weeks would raise actual duration by only some 1.3 to 2.6 weeks. 2) Take-up (applications for UI among the unemployed) does respond positively to higher benefit levels, but the size of the effect is again modest. Most of the increase in take-up that occurs during recessions arises from a change in the mix of unemployment by reason as the share of the unemployed who are job losers increases. Since job losers are most likely to be eligible to collect UI benefits, i.e., their job separations were initiated by employers and they have substantial past work experience, recipiency rises in recessions. The timing of the increase is a positive development since the associated benefit payments help to stabilize the macro economy. 3) Some employers do undertake more temporary layoffs because their benefit payments are not effectively experience rated, e.g., those employers already taxed at the maximum tax rate. However, the degree of experience rating has not changed in recent years13 while occurrences of temporary layoffs as a component of overall unemployment have decreased.

Thus, while the payment of UI benefits does have negative consequences in the labor market, the effects are small and nothing in the recent evolution of UI statues suggests the effects are becoming larger. The two aspects of the program that affect unemployment duration (the replacement rate and maximum potential benefit duration) have not become more generous in recent years. Hence, the secular increase in UI benefit duration and the associated increase in the benefit exhaustion rate of the past decades reflect other changes in the labor market such as the ageing of the labor force and decreased reliance on temporary layoffs when employers make workforce adjustments.

Readers should also be reminded of what is termed a general equilibrium effect of UI labor market disincentives. To the extent that recipients of benefits prolong their spells of unemployment, this has a positive effect on other unemployed job seekers who are not recipients. This substitution effect that favors non-recipients means that the full effect of UI benefits on the overall labor market is smaller than the effect on beneficiaries. Some of this group who secure new jobs would have remained unemployed longer had the UI recipients not prolonged their spells of unemployment. The general equilibrium aspect of UI benefit payments has not been extensively researched, largely because it is more difficult to characterize (or model, using the jargon of economists) behavioral relations in the full labor market than just the behavior of UI recipients. The direction of the general equilibrium effect, however, is clear: prolonged UI benefit recipiency improves the job prospects of unemployed non-beneficiaries.

In sum, three comments can be made. First, disincentive effects are present. Second, the disincentive effects have only small effects in raising unemployment. And finally, disincentive effects of UI benefits have not become larger in recent years.

Specific limitations in UI benefit availability

There are several areas where the current UI program does not provide benefits to large numbers of unemployed workers. Workers in many different situations do not collect benefits despite having extensive work histories and job separations that were initiated by their former employers. Unemployed workers in the following five situations experience restricted access to UI benefits: 1) low-wage workers, 2) part-time workers, 3) workers who complete temporary jobs, 4) those in low-recipiency states, and 5) the long-term unemployed. Large numbers of workers fall into each of these five situations.

Low-wage workers. Persons with limited work histories, low educational credentials, and irregular patterns of labor force attachment experience unemployment rates substantially above the national average. Using data from 1992-95, the U.S. Government Accountability Office noted that low-wage workers were twice as likely to experience unemployment as high-wage workers were but were only half as likely to collect UI benefits.14 While a number of factors contribute to the disparity, it is clear that UI is more effective in serving workers located above the bottom rungs of the labor market.

Part-time workers. Part-time employees are much less likely than full-time employees to receive UI benefits when they become unemployed. One analysis found part-time workers had a recipiency rate less than one-half the recipiency rate among full-time workers.15 Much of the disparity reflects a requirement in many states to seek full-time work as a condition of eligibility for UI benefits. While some states have changed their UI laws regarding availability, more than half still require search for full-time work regardless of hours worked per week on the pre-unemployment job. Much less change in this requirement has taken place in recent years when compared to the widespread adoption of alternative base period provisions since 1987.

Unemployed after completing a temporary job. Since 1994, the monthly labor force survey of households (the CPS) has identified persons who become unemployed after completing a temporary job. Like other job losers, the immediate cause of their unemployment is an employer decision to terminate their services. Data from a special UI supplement to the CPS in 2005 show that their rate of applying for UI benefits is about half the application rate of other job losers. Many do not appear to understand that their temporary employment is covered by the UI program. This group now accounts for about 10% of all unemployment (10.2% in 2005). Their understanding of and access to UI appears to be a problem.

Workers in states with low UI recipiency. As noted earlier, there are wide regional differences in recipiency rates, with workers in some states only half as likely to receive benefits as in others (e.g., recipiency rates of 40% versus 20%). There is considerable year-to-year consistency in these recipiency patterns, but they can be broken when a state has the will to change. Louisiana, for example, had a recipiency rate (typical for its region) that varied between 28% and 20% from 1986 to 2004. The extraordinary circumstances caused by hurricane Katrina and the response of Louisiana’s UI program more than doubled recipiency to 52% in 2005, and recipiency remained at 39% in 2006. The response of Louisiana’s UI program shows that a state has the ability to influence recipiency and that a sharp change in recipiency can occur if there is the will to make the change.

The long-term unemployed. The upward trend in exhaustions has already been noted. Most states have a variable potential duration of benefits with minimum potential durations often falling between 10 and 15 weeks. Exhaustion rates are consistently highest among persons with the shortest potential durations. For many individuals in a given 52-week benefit year, potential benefit duration is closer to 15 weeks than to 26 weeks.

The benefit provisions of state UI programs operate without federal standards for measures such as the recipiency rate (the share of the unemployed who collect benefits) or the replacement rate.16 Thus, instituting change to address the limitations in the five areas identified above presents major challenges. The larger point is that UI programs as currently structured have a number of shortcomings in providing adequate income support to unemployed workers. A proposal to reduce UI benefits among current recipients would move the UI program in the wrong direction.

The Kling reform proposal

In mid-2006 Jeffrey Kling of the Brookings Institution and the Hamilton Project proposed to radically revise UI. His proposal would replace the current UI program with a three-part program that offers wage-loss insurance to dislocated workers, a system of individualized accounts termed temp

orary earnings replacement accounts (TERAs) to other unemployed workers, and co-insurance payments to low-wage recipients of UI benefits.17 The new insurance arrangements will have eligibility and benefit provisions similar to provisions in the present UI program. He asserts that overall costs will be similar to costs of the present UI program, an assertion supported by a simulation analysis.

Kling’s proposal is motivated by at least four judgments: 1) the low UI tax base causes program financing to be regressive, 2) benefit payments are not effectively targeted on the unemployed with greatest need, 3) a program is needed to provide benefits to displaced workers who take jobs with wage rates below those of pre-displacement jobs, and 4) there should be no aggregate increase in the costs of the UI program, i.e., any expansion in one area needs to be offset by savings elsewhere.

Few students of UI would disagree with the first consideration. The UI tax base is low at the federal level and in nearly all states. His discussion of targeting implies (wrongly, in this author’s judgment) that many UI current recipients really do not need the benefits. While disincentive effects do exist such as prolonging duration in benefit status, the effects are not very large, as summarized above. Moreover, there are ample reasons why providing UI through a social insurance system is beneficial for the economy and unemployed workers.

Many would agree that the United States needs a program to address the problem of worker dislocation. Before adopting his or any other remedy for dislocation, however, there should be a debate on at least three questions. 1) Does wage loss insurance take priority over other labor market policy areas such as making improvements in the present UI program? 2) If dislocated workers are to be given priority, is wage loss insurance the appropriate form of support? Alternatives to wage loss insurance that could be targeted on dislocated workers include more extensive UI support, improved support for job search activities, and enhanced labor market training and education programs. 3) Even if wage-loss insurance is deemed the appropriate vehicle, what are the appropriate parameters for determining eligibility (extent of previous job tenure, size of the wage loss) and support (potential duration and the extent of wage-loss replacement)? The results from social experiments could inform this discussion.

Several aspects of the Kling proposal can be questioned, but the starting point here will be to describe the main points of the proposal. Wage-loss insurance and TERAs both represent a major departure from UI as presently structured. The discussion starts with wage-loss insurance, since it represents a labor market insurance contingency that has received only limited attention in the past.

Wage-loss insurance

Unemployment compensation programs in the U.S. and in other countries make all or nearly all of their payments to persons who meet the labor market survey definition of unemployment, i.e., without a job but able to work, available for work, and actively seeking work. Wage loss insurance, in contrast, makes payments to persons who are employed. The purpose of the payments is to encourage early reemployment using a financial incentive, a share of the gap between the hourly wage paid on the new job and the (higher) hourly wage of the previous job. Because displaced workers frequently experience major reductions in hourly earnings as well as lengthy spells of unemployment, wage loss insurance payments cushion the reduction in take-home pay for someone who accepts a job at a lower wage rate.

Displacement produces serious labor market consequences for substantial numbers of affected workers. Between January 2003 and December 2005 about 3.8 million workers aged 20 and older with three or more years of seniority were displaced from jobs (terminated with no prospect of returning at a later date). This estimate of displacement comes from the latest (January 2006) displaced worker supplement to the monthly household labor force survey (the Current Population Survey or CPS).18 These supplements have been conducted every two years since January 1984. Earlier CPS supplements also showed job displacements affecting millions of experienced workers with the rate of displacement exceeding 1.0 million per year and being higher during recessions.19

The consequences of worker displacement include a high likelihood of unemployment, lengthy unemployment spells, loss of health insurance coverage, and a large reduction in the hourly wage rate for many displaced workers able to find new jobs. Among workers aged 20 and older displaced between January 2003 and December 2005, 13.4% were still unemployed in January 2006 while 16.7% had left the labor force by that date. Of the 2.43 million wage and salary workers who were reemployed in January 2006, 0.49 million (or one in five) had jobs that paid at least 20% less than their pre-displacement jobs. The patterns from the January 2006 displaced worker supplement just described repeat patterns from earlier supplements. Job displacement results in serious economic hardship for many. Among those reemployed at substantially lower wage rates, the loss of earnings may extend over several years.

Wage-loss insurance payments fill part of the gap between the previous wage and the wage on the new job. Kling’s proposal would pay one quarter of the wage gap for up to six years. An example to illustrate his proposal is a worker who previously made $14 per hour moving to a post-displacement job that pays $10 per hour. Since one-quarter of the hourly wage-loss is replaced, the person receives $1 of wage loss insurance payment for each hour worked. Workers are to work a minimum number of hours per week (30 hours is implied) to be eligible for wage-loss insurance payments.20 To limit total costs, the pre-unemployment hourly wage rate used to calculate the insurance payment is the lesser of the previous wage rate or $15. A second hypothetical person who moves from a pre-displacement hourly wage of $24 to a $10 hourly wage would be eligible for an hourly wage-loss insurance payment of only $1.25 because the wage-loss used in the benefit calculation is only $5.00 per hour ($15.00 – $10.00), not the actual wage-loss of $14.00 per hour. The first person experiences a 25% replacement from wage-loss insurance ($1 per $4 of hourly wage loss), but the second person experiences only a 9% wage-loss replacement ($1.25 of $14 of hourly wage loss).

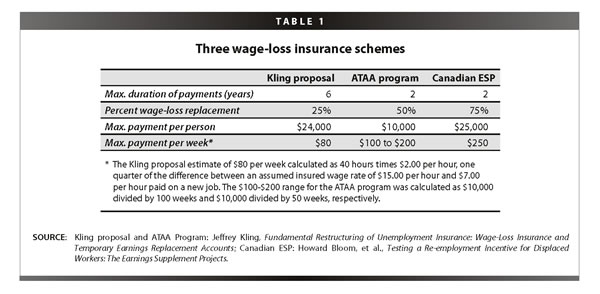

Wage-loss insurance must address several design issues. Table 1 summarizes key features of three programs: Kling’s proposal, adjustment assistance to workers aged 50 and older under the current Alternative Trade Adjustment Assistance (ATAA) program, and the Earnings Supplement Project (ESP), an experiment conducted in Canada during the mid-1990s. The table identifies four important design features: the maximum duration of payments, the percent of the wage-loss gap filled by wage-loss insurance payments, the maximum payment per person, and the maximum weekly payment per person.

The programs differ across all four dimensions of design included in Table 1. Potential benefit duration of six years in Kling’s proposal (even longer if more than 4,000 hours were worked in the two years before displacement) is three times as long as the two-year maximum of both ATAA and ESP. The gap-filling percentages range from a low of 25% in Kling’s proposal to 50% in ATAA to a high of 75% in ESP. The maximum payment per person ranges from $24,000 in Kling’s proposal and $25,000 in ESP down to $10,000 in ATAA. Thus while Kling’s proposal has the longest potential period of wage-loss support, it is the least generous proposal in terms of the gap-filling percentage and maximum

weekly support.

One purpose of wage-loss insurance is to speed reemployment among displaced workers who experience permanent job loss. The evaluation of the Canadian ESP did find modest effects in the expected direction.21 The treatment group was 4.4% more likely to become reemployed at a full-time job when compared to the comparison group. The treatment group was also 4.6% more likely to take a job with a lower wage than the comparison group. Interestingly, however, there were no savings on UI benefits. Thus, while there were effects on behavior, they were modest in this program that provided quite generous support payments to those who secured early reemployment.

The lengthy period of support under the Kling proposal arises from an eligibility feature that allows three hours of wage-loss payment support for every hour worked in the two years prior to displacement. The money is paid by the UI agency and the agency is to be reimbursed by the employer who terminated the worker.22

Kling’s example of the dislocated worker who previously earned $14 per hour but then $10 per hour on the post-displacement job is worth reviewing. Prior to reemployment, the person is assumed to receive 10 weeks of UI benefits at $280 per week. The payments are financed by a drawdown of $2,000 from her TERA (the balance at termination from the previous job) and an $800 loan. Upon reemployment, 5% of weekly pay is withheld by the employer and used to repay the loan. Only after the loan is repaid and the account balance has been replenished to a level of $5,000 does the wage-loss insurance payment of $1 per hour worked go to the worker. Working 40-hour weeks continuously, it would take 40 weeks to repay the loan and an additional 125 weeks (2.4 years) to achieve a balance of $5,000 before starting to receive the $40 weekly payments.

It would seem that Kling’s wage-loss insurance provides very modest benefits to those deemed to need priority assistance. 1) The basic replacement rate is 25% or less. Many who take a job with at a reduced wage rate would experience a wage-loss replacement below 25% because of the limitation on the maximum allowable pre-displacement wage rate of $15 per hour. Many high-wage workers would be ineligible even if they experience a substantial wage rate reduction, say from $30 per hour to $20 per hour. 2) Outstanding loans from the person’s individual unemployment insurance account would need to be repaid and the account replenished before wage-loss insurance payments would be made to the worker. This repayment requirement could delay benefits for months after being reemployed. 3) Ultimately, the person must depend upon his or her own resources (earnings) except for the few who are exempt from part of the loan repayment requirement because their hourly earnings fall into the $5.15-$7.00 range.

Despite the limited scope of wage-loss insurance benefits, they would be a new form of support payment but targeted upon (a subset of) the employed population. As such, they would represent an increase in total financial support for workers with wage losses unless an equal volume of savings can be secured by reducing payments to the unemployed or through some other adjustment that either reduces expenditures or increases taxes.23 Kling asserts that Temporary Earnings Replacement Accounts (TERAs) will accomplish such a volume of savings. In fact, because there is so little “fat” in the UI system, it seems unlikely his proposal will realize substantial savings. A discussion of TERAs follows.

Temporary Earnings Replacement Accounts

Employers in Kling’s proposed system make payroll tax contributions that are experience rated as they are in the current UI program. Higher benefit charges against an employer’s account will lead to higher UI employer payroll taxes (except when the employer is already taxed at the maximum rate). Employers also withhold payroll tax amounts on behalf of workers for deposit into each worker’s TERA. The employee’s payroll tax is initially withheld at 1% of gross wages up to a limit defined by the tax base for Social Security OASDI ($97,500 in 2007), and withholding continues until the individual’s account balance reaches $5,000. Employees whose balances have reached $5,000 have no additional payroll taxes withheld for their TERA.

An individual with a compensable spell of unemployment may withdraw from his or her TERA an amount up to the full balance in the account. Additional benefit payments can be financed by loans to the unemployed worker. As noted, loan repayments are generated by a 5% withholding from wages undertaken by employers for any employee with an outstanding TERA loan.

During an individual’s working life, the pattern of withdrawals and subsequent deposits into TERA accounts reflects the time pattern of eligible UI claims. When the individual reaches retirement age, the remaining balance is made available to the individual. Kling’s proposal also includes arrangements for disbursements from TERAs in cases of disability and death prior to reaching retirement age.

The TERAs proposed by Kling are a specific kind of Unemployment Insurance Savings Account (UISA) and several UISA programs already exist in Latin American countries. The most prominent example is Chile’s UISA program, which was authorized in 2001. This new UI program is gradually replacing a flat benefit unemployment assistance program. The first contributions into the new UI program were made in late 2002, and benefit payments commenced in May 2003.

UISA programs are also present in Ecuador, Brazil, Colombia, Panama, and Peru. Summary details of UISA program provisions are available from a survey paper by Ferrer and Riddell.24 Their paper does not have information on the performance of UISAs in providing income support to the unemployed, but it has limited information on UISA financial operations.

Proponents argue that UISA programs address disincentive problems by making workers responsible for managing their own accounts. It is asserted that by creating a valuable asset, the individual will try to preserve the asset by limiting withdrawals during periods of unemployment. This reasoning can be questioned for at least two reasons. First, the disincentive effects of UI on unemployment in the United States are modest. Second, in a society like the United States. where the savings rate has been trending downward, creating a valuable asset can also lead to attempts to gain access to the asset before retirement, particularly an asset like a UISA that was created to be used before retirement.

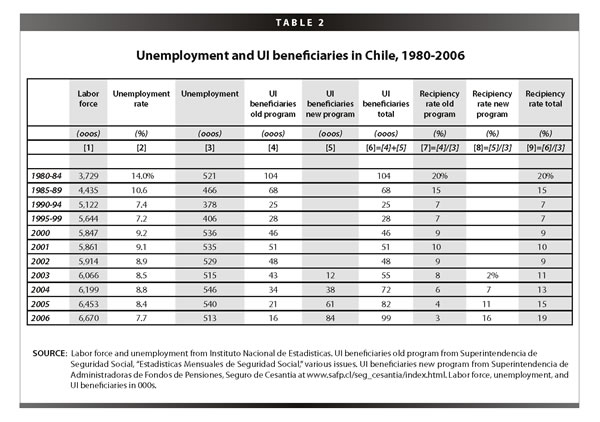

Because Chile’s new program frequently enters discussions of UISAs, it will be useful to describe it and discuss experiences to this point in time. An overview of the program is given in papers by Acevedo, Eskenazi, and Pages (2006) and by Vroman (2003).25 The new program pays UI benefits for up to five months under a declining benefit schedule. Benefits are 50% of past wages (subject to a maximum benefit) in the first month and then decrease by five percentage points in successive months, reaching 30% in the fifth month. Financing is joint with employers contributing 2.4% of wages and workers contributing 0.6%.26 The employee contribution and 1.6% (two-thirds) of the employer contribution go into individual accounts while the remaining 0.8% of the employer contribution goes into a common fund that finances benefit payments to individuals who have exhausted their individual accounts. The common fund in Chile plays a back-up role similar to the role that loans to persons with exhausted TERA accounts play in Kling’s proposal.

Table 2 displays selected Chilean performance data, emphasizing unemployment and the UI benefit recipiency rate. The old UI program pays much lower benefits than the new program.27 It can pay benefits up to 12 months with payments during the fi

rst three months roughly one-seventh of maximum initial benefits in the new system. In most years, duration per recipient in the old UI program has averaged between seven and eight months.

Table 2 shows that unemployment is a persistent problem in Chile with no unemployment rate in the table below 7.0%.28 Between 2000 and 2006, the unemployment rate ranged between 7.7% and 9.2% (column 2) and annual average unemployment has ranged between 513,000 and 546,000 (column 3). Traditionally, UI has been received by a small minority of the unemployed. The highest recipiency rate under the old UI program averaged only 20% during 1980-84, while the highest recipiency rate under the old and new programs combined was 19% in 2006. Between 1987 and 2002, the old UI program compensated less than one-tenth of the unemployed.

The new UI program has grown rapidly since 2003 when it started to pay benefits. During 2006 it accounted for more than 80% of all recipients, averaging 84,000 persons (column 5). The phasing out of the old UI program is vividly illustrated in column 4 of Table 2 where monthly recipients in 2006 were about one-third the number during 2000-02, the three years that preceded the introduction of the new UI program. The old UI program will be fully phased out by 2009. Already in 2006, however, the new program accounts for 84% of combined UI recipients and 98% of combined benefit payments. In terms of benefit payouts to workers, the transition to the new system of unemployment protection was largely complete by the end of 2006.

While the transition is still underway, some features of the new program are already apparent. The recipiency rate for the new program in 2005 and 2006 11% and 16%, respectively) already exceeds the recipiency rate for the old UI program for every year since 1990. The last year the old UI program had as many beneficiaries as the 84,000 of the new program in 2006 was 1986. Yet the unemployment rate in 1986 (12.1%, almost half again higher than the 7.7% unemployment rate of 2006. Many covered workers are already using the new system. The increase in recipiency (roughly doubling since 2000-02 in column 9) indicates that many unemployed workers are using the new UI program who did not utilize the old UI program. The recent increase in recipiency has occurred despite movement of most recipients from a program that potentially pays 12 months of benefits to a program that potentially pays only five months of benefits. To this author, it is obvious that take-up has increased substantially under the new UI program. For many, a valuable new personal asset is being accessed.

Data from Chile’s new UI program allow one to compare experiences of workers with two distinct types of labor contracts. Most employees in Chile work either under an indefinite-term contract or a fixed-term contract. The former group generally enjoys greater job security as well as higher pay. In 2006 a monthly average of about 1 million of both types of workers made contributions into the new UI program. However monthly recipiency averaged 33,300 for those with indefinite contracts but 51,600 for those with fixed-term contracts. The respective recipiency rates (the ratio of monthly beneficiaries to monthly contributors) were 0.028 and 0.049 in 2006 or 75% higher for those on fixed-term contracts. Because their pay is generally lower, the monthly benefit for those of fixed-term contracts in 2006 was 7% lower than for those on indefinite contracts. Chile’s program follows the expected pattern with higher utilization of benefits among wage and salary employees with a greater risk of unemployment.

This finding could have relevance for the United States if TERAs were to be implemented. At present, it appears many who are unemployed following the end of a temporary job have at best an imperfect understanding of their coverage by UI. If they had TERAs, it seems likely their application rate for UI benefits would increase and become more similar to the application rates exhibited by other job losers. Similar considerations might also apply to unemployed labor force reentrants who have rejoined the labor force and are searching for work. Creating a system of individual accounts will not necessarily lead to lower applications and benefit utilization by the unemployed.

Low-wage co-insurance

Kling’s proposal recognizes the special hardship that loan repayments would represent for workers paid a low hourly wage rate. He proposes creation of a co-insurance arrangement for those at the bottom of the wage distribution. Eligibility is reserved for persons paid between $5.15 (the federal minimum wage in 2006) and $7.00 per hour.29 A person paid $7.00 per hour would be fully responsible for repaying all loans while someone paid $5.15 would experience full forgiveness of loans.

One obvious comment to make about this phase-out structure is the rapid descent from full forgiveness to full responsibility for loan repayment as the hourly wage increases between $5.15 and $7.00. Arguments can be advanced for a more gradual phase-out schedule that could be achieved by raising the threshold above $7.00. Also, persons with frequent unemployment spells might be tempted to collude with employers to have their wage reported at the minimum wage to reduce or totally avoid loan repayments. Finally, since the federal minimum wage has been modified by legislation of 2007, this aspect of the proposal would have to be revisited.

Observations and critical comments

Implementation of Kling’s proposal would bring about a radical change in the UI program. Comments in this section will be organized around five broad themes followed by some smaller considerations.

Increased uncertainty 30

The proposal carries with it three kinds of increased uncertainty. First, there is greater uncertainty for the worker compared to the current UI program. In 70 years, the state programs have never missed a benefit payment because of a funding problem. When a state’s regular UI trust fund balance reaches zero due to a recession-related drawdown, loans can be obtained from the U.S. Treasury (or sometimes from the private bond market) without an interruption of payments to eligible beneficiaries. The worker continues to make claims with an absolute assurance regarding the receipt of payments. The individual does not participate directly in borrowing decisions that are made by experienced state officials based on rules set by federal legislation.

Under a system of TERAs, the individual worker may decide that borrowing is not an attractive option. For many, the decision whether to borrow or not will involve anxieties not present under current UI institutional arrangements, and the decision will be made in the midst of a high-stress situation, i.e., during a spell of unemployment. While the increased uncertainties may prompt many individuals to undertake more intensive job search and perhaps faster reemployment, the adverse effects on mental health for unemployed persons and on macroeconomic stabilization need to be carefully considered.

TERAs radically reduce the extent of pooling, effectively ending UI as a “social insurance.” Nearly all labor force participants will rely on their own resources to finance UI benefits with pooling limited to intertemporal pooling, i.e., the individual can build their account before the onset of unemployment while further account building and loan repayments by the individual will occur upon reemployment. The current UI system, in contrast, has many aspects of pooling that involve both firms and individuals. UI is accurately described as a social insurance program and both words, social and insurance, are important in understanding how the pr

ogram operates. Moving to a system of TERAs would eliminate much of the social aspect of the current UI program.

The second uncertainty involves the functioning of Kling’s proposed system. All three elements (wage-loss insurance, TERAs, and low-wage co-insurance) raise questions about take-up. How many eligible persons will actually use these components? At a minimum, a social experiment is needed to test the elements of the proposed new system. By conducting an experiment, any surprises and flaws in an initial program design can be addressed before a full rollout of the program.

A third uncertainty is the total cost of the proposed system. The earlier discussion of the Chilean experience could not be definitive because their new UI system is still being implemented. This review infers that costs will be much higher under Chile’s new system and a large part of the cost increase reflects increased take-up. It appears more unemployed workers are using the new UI program compared to the old system, and the long-run change could be a doubling of the recipiency rate compared to the old UI system. TERAs ala Kling may not generate any savings, much less the savings he anticipates. It could well be that the total cost of unemployment wage loss protection would increase as TERAs create an asset valued by the worker. Again, the usefulness of an experiment to address the cost question seems obvious.

Countercyclical performance of UI

As presently structured, UI performs an important countercyclical role helping to stabilize the macro economy, and it has done so in each of the 10 post-World War II recessions. Workers apply for benefits when they become unemployed, and the volume of applications increases sharply during recessions. The increase in benefit payouts helps to stabilize household income (replacing part of unemployment-induced wage losses) and stimulates demand in periods when output declines.

The increase in claims activity occurs without the individual claimant having to ask questions about the timing of their claim and the possible need for support (from their individual account) in later periods. Benefits are available with certainty from the present UI system, even if their state’s UI trust fund has a low balance. In Kling’s system, someone with a $5,000 balance entitled to $300 per week would exhaust the balance in roughly four months. Questions about borrowing would arise even sooner for persons with low balances. Young workers and others with a high risk of unemployment would more likely face this situation than older workers. To the extent that a reluctance to borrow enters individual decisions, the aggregate effect would be to reduce the countercyclical performance of UI compared to the present situation.

Unemployment duration increases strongly during recessions. Most recently, mean duration as measured in the CPS increased from 12.6 weeks in 2000 to 16.6 weeks in 2002 and 19.2 weeks in 2003. The need for UI benefits increases sharply during a recession and the present UI system responds strongly. This response helps many workers and families as well as the macro economy. Why replace the present system with one whose cyclical response is untested and less certain?

Administrative considerations

If a system of TERAs is established, a new type of administrative support apparatus will be required. Kling’s proposal has the government (presumably the state UI agencies) responsible for tracking flows into and out of TERAs. Individual workers make decisions about investing TERA assets. Employers also play a key role in administration of TERAs. They withhold employee payroll taxes that flow into each TERA. Employers also administer loan repayment by withholding 5% of earnings for their employees with outstanding loans. They also report hours worked for each covered worker in addition to the quarterly earnings and monthly employment that are now reported for each worker in all states in UI quarterly wage reports.

The number of micro earnings records involved in moving to the administration of TERAs for all covered workers is substantial. In 2005, total covered employment averaged 128.9 million per month, and the number who worked sometime during the year fell into the 150-160 million range. While the Social Security Administration and IRS track earnings records for similar numbers of workers, their need for real-time access to the earnings records of individual workers is less pressing because relatively few pre-retirement workers make claims for disability benefits within a given year. Turnover of beneficiaries is also much less frequent in the Social Security program than in UI.

Consider the contrast between the current UI program and a TERA system in the area of loans and loan repayments. Following the 2001 recession, nine state UI programs borrowed from the U.S. Treasury between 2002 and 2006. These loans are now fully repaid. Tracking developments in financing across the entire set of 53 state programs is a comparatively simple matter. Tracking TERA developments for individual workers with outstanding loans, some of whom cross state boundaries through migration and routine commuting patterns would present much greater challenges. In a labor market where more than 150 million workers would have TERA balances, tracking deposits, withdrawals, loans, and repayment activities would represent a large administrative challenge with numerous chances for errors for individual workers.

The preceding discussion suggests that establishing and administering a new set of individual accounts would present serious challenges for UI program administration.

The need for wage-loss insurance relative to other needs

Worker displacement has been a persistent feature of the labor market for the past quarter century, probably for longer, but consistent measurement of displacement started only in the early 1980s. Strong arguments can be advanced for having a program to encourage and assist speedy reemployment among affected workers. Wage-loss insurance, reemployment bonuses, and career advancement accounts are proposed to address this need. A program that addresses the problem of labor market displacement due to technological change and international trade could help many workers.

Wage-loss insurance cash payments are just one form of support for displaced workers. Other support services such as labor market information, access to job listings, retraining, subsidies for higher education, and relocation allowances also can be useful. In short, wage-loss insurance is not the only policy tool or necessarily the most effective policy tool to address the worker displacement problem.

Nevertheless, the time may be ripe in the United States for serious consideration of a wage-loss insurance program, either a stand-alone program or in conjunction with other early reemployment interventions. Considerations of both equity and efficiency are relevant. Wage-loss insurance payments would ease the transition to new work by providing income support during the initial period of reemployment. To the extent that early reemployment is fostered, it would also reduce unemployment among displaced workers. However, even with no behavioral effects on job search and reemployment, the equity argument itself would be sufficient for many to advocate wage loss insurance. It is appropriate in a rich and caring society to provide compensatory payments to persons adversely affected by economic change.

As indicated in Table 1, Kling’s proposal for wage-loss insurance has one set of design parameters with low wage-loss replacement (25% or less), long potential duration, and modest weekly support. The Canadian ESP has been evaluated, and favorable (but modest) effects on reemployment

were found. Among the trio of proposals summarized in Table 1 (Kling’s proposal, ATAA, and Canadian ESP), ESP is the most generous. An evaluation of ATAA is underway, but results are not yet available.31

Before adopting wage-loss insurance, a series of other questions should also be addressed. Should wage-loss insurance recognize the loss of fringe benefits (health insurance and pension accruals) as well as reduced hourly wages in setting compensation levels? What are the labor market displacement effects of wage-loss insurance? What patterns of job stability do recipients of wage-loss insurance demonstrate in their new, lower-wage jobs? To what extent would TERA and wage-loss insurance cash benefits substitute for temporary federal benefits, e.g., Temporary Extended Unemployment Compensation (TEUC), during recessions, and would it be appropriate to debit individual accounts during recessions? In short, there may be other adverse effects in the labor market that lessen the attractiveness of wage-loss insurance even if it does speed the reemployment of displaced workers.

If the United States goes forward in adopting or at least considering wage-loss insurance, it should be assessed (at least initially) as a stand-alone program with its own financing and not financed by reductions in other UI benefits as in Kling’s proposal. Also, it should be considered against other possible reforms that would increase access to UI benefits by unemployed persons currently not eligible for benefits. The idea of wage insurance has merit because displaced workers can experience large financial losses, but its cost would depend both on program design parameters, such as those identified in Table 1, and upon the behavioral responses of eligible displaced workers.

It seems likely that reforms to increase access among part-time, low-wage, and temporary help workers would cost less per-recipient than wage insurance, because, on average, a lower-wage clientele would be served. If a larger number of clients would be served for a given total cost, many, including this author, would argue that reforms should improve UI eligibility in preference to establishing wage insurance.

Many dislocated workers have high pre-displacement hourly wages. To limit the permissible wage pre-displacement wage to $15 per hour as in Kling’s proposal, might be needlessly restrictive. Again, the public discussion would be furthered by having results from a well-designed wage-loss insurance experiment.

The rationale for suggesting a stand-alone program is twofold. First, wage-loss insurance payments indemnify workers for a contingency that is distinct from unemployment, because it occurs upon re-employment. Yet, insuring against this contingency could be costly. Second, while TERAs are part of Kling’s proposal, they are not a necessary feature of wage-loss insurance, as Canadian ERP and ATAA both illustrate. It would be easier to design and evaluate a wage-loss insurance experiment without, at the same time, establishing TERAs.

When wage-loss insurance is considered relative to other potential UI reforms, its appeal diminishes. As noted above, UI recipiency among the unemployed has been consistently low in the United States and several identifiable factors contribute to low recipiency. Strong arguments can be made to increase recipiency among specific groups of unemployed workers such as part-time workers, low-wage workers, and temporary help employees. Several observers of the labor market would feel it more important for UI reform to address the needs of these groups rather than the needs of workers who are reemployed following displacement. Many who would gain access to UI through reform would be drawn from the lower tail of the U.S. income distribution. Improving access could make UI more progressive than at present. In short, many with a serious interest in improved wage-loss protection in the United States would want to increase, not decrease, UI benefits among the unemployed rather than institute a new program with payments to persons who are employed.

UI reform priorities

The strategy of the Kling proposal is to establish wage-loss insurance for displaced workers and to finance its costs through savings generated by a new system of individual savings accounts (TERAs). He expects the new system will induce savings among unemployed claimants arising from changes in claimant behavior. The implicit judgment of the Kling proposal is that many current recipients could “get by” without UI. An accurate assessment of disincentive effects, however, indicates that the adverse effects of UI on duration and take-up are small. There is little “fat” to squeeze out of the present UI program.

An earlier discussion in this paper identified five specific situations where the present UI program does not protect large numbers of unemployed workers. Economic hardship for many unemployed workers, both recipients of UI and non-recipients, can also be demonstrated. Recent UI reforms such as establishing ABP programs, now present in 19 states, provide examples of changes that have clearly helped low-wage workers.

Who should be the target group for increased earnings-loss support payments? Even if the answer is “dislocated workers with substantial wage losses,” does the Kling proposal effectively target its support payments? Is there equity in providing 25% wage loss replacement when hourly wages decrease from $14 to $10 but only 9% wage-loss replacement when hourly wages decrease from $24 to $10 and zero support when hourly wages decrease from $30 to $20?

Low-wage unemployed workers who receive UI benefits can be supported at a much lower total program cost than high-wage workers. That is a direct consequence of having a UI system that links the benefit payment level to the past level of earnings. The United States operates a comparatively inexpensive UI program. A reform that causes a given increment in the cost of UI will help more individuals if the new recipients are drawn disproportionately from the low-wage segment of the unemployed population. A reform that provides wage-loss insurance payments to large numbers of displaced workers may be more costly than can be justified given the other limitations of the present UI program and other reform priorities that would favor low-wage workers or the other groups with low recipiency as identified earlier.

Some smaller considerations: reporting hours and phase-out schedules

Two other aspects of the Kling proposal that may represent problems should be noted. First, there are problems in reporting hours worked. Washington State uses base period hours worked as the main determinant of monetary eligibility. Eligibility requires 680 hours worked and earnings in two base period quarters of at least $5,819 (in 2006).

Many employers do not report hours for individual workers. In the past, researchers who worked with Washington’s quarterly wage record data have found that hours data were absent for about 20% of the wage records. Reporting hours worked has improved in recent years, partly due to increased agency oversight and penalties for failure to report hours, but hours worked data are still absent for about 10% of the earnings records. Following claims in such situations, the UI agency contacts the employer requesting hours data and indicate they will use the state minimum wage as the hourly wage if the employer does not supply the data. For non-responding employers, agency use of the minimum wage increases the estimate of hours worked (relative to actual hours worked) and the likelihood of achieving monetary eligibility. For other deficient wage records, contact with the employer may not occur and the records remain incomplete. Thus reporting hours worked is more of an administrative challenge than suggested by

Kling’s proposal.

The second issue is the phase-out schedule for low-wage co-insurance. The schedule suggested by Kling is very steeply sloped and may be subject to manipulation by workers and their employers when hourly pay falls into the $5.15-$7.00 range (based on the federal minimum wage of $5.15 in 2006). A more gradual phase-out when wages rise above the minimum wage seems appropriate.

Conclusion

The proposal to institute wage-loss insurance is timely in the U.S. economy where more than 1 million experienced workers suffer permanent job loss each year. These workers can be helped without establishing a system of individual UI accounts—TERAs in Kling’s terminology. However, it may be a higher priority to provide increased access to UI benefits among the unemployed and especially the low-wage unemployed. Many observers might feel that wage-loss insurance and increased access among the unemployed should both be supported. With the current low level of UI recipiency, wage-loss insurance should not be financed by reducing access to UI benefits among its current recipients.

— Wayne Vroman is an economist, employed at the Urban Institute since 1976. He has directed many projects on the unemployment insurance (UI) program and has authored numerous articles, reports, and five books on UI. His research has covered topics on UI benefits, taxes, and program financing. Opinions expressed in

this report are those of the author and do not necessarily represent the views of the Urban Institute.

Endnotes

1. The Unemployment Insurance Modernization Act, Senate bill S. 1871.

2. The Unemployment Insurance Modernization Act House bill H.R. 2233.

3. Trade Globalization and Adjustment Assistance Act of 2007, Senate bill S. 1848.

4. Statement by Dr. Jeffrey Kling before the Subcommittee on Income Security and Family Support of the House Committee on Ways and Means, (September 19, 2007) and Jeffrey Kling, Fundamental Restructuring of Unemployment Insurance: Wage-Loss Insurance and Temporary Earnings Replacement Accounts, Hamilton Project Discussion Paper 2006-05, September 2006. www.brookings.edu/views/papers/200609kling.pdf.

5. Three other goals of UI are also frequently noted. 1) Benefit payments automatically vary over the business cycle and help to stabilize the macro economy. 2) The program also tries to limit the volume of layoffs by having taxes tied to claims made by current and former employees. This linkage (termed experience rating) is intended to affect employer behavior by making it expensive to terminate workers, hence discourage layoffs. 3) It also tries to involve employers in program administration through their participation in UI agency process for determining benefit eligibility. When workers file for benefits, the UI agency contacts the employer to elicit employer input regarding the circumstances of the job separation. Most quits are disqualifying separations while most nonprejudicial layoffs are not disqualifying.

6. Across 51 programs (the 50 states plus the District of Columbia) in 2005 the ratio of the maximum weekly benefit to weekly wages fell between 35% and 65% in 45 programs and the statutory replacement rate between 50% and 59.9% in 47 programs.

7. The respective percentages of hourly compensation represented by these employer payroll contributions in June 2006 were 7.7%, 4.5%, 4.3%, 1.8%, and 1.1%. Employer contributions to UI were 0.5% of hourly compensation in the same BLS survey of Employer Costs for Employee Compensation. See Table 1 in the September 22, 2006 press release USDL: 06-1640 at www.bls.gov/ncs/ect/home.htm.

8. In a temporary layoff situation the employer has committed to rehire the worker, usually within 30 days.

9.The temporary layoff share of unemployment increased from 14% in 1974 to 21% in 1975, from 14% in 1979 to 19% in 1980 but was unchanged at 15% between 1990 and 1991 and only increased from 15% in 2000 to 16% in 2001.

10. For example, in 2005 25.6% persons on permanent layoff had unemployment spells of 27 weeks or longer compared to only 4.5% of persons on temporary layoff.

11. There are 21 high-income OECD-member countries with populations of more than 1 million persons. From 2000 to 2004, the average UI recipiency rate exceeded 50% in all but the six countries identified in the text. The ratio for the United States was 38.6%, and only Greece and Japan had lower ratios.

12. See Wayne Vroman, Systemic Disincentive Effects of Unemployment Insurance, paper prepared for the Department of Labor Research Exchange Conference of May 5-7, 2004.

13. The Office of Workforce Security of the U.S. Department of Labor has published an Experience Rating Index (ERI) for the period 1988 to 2005. During these 18 years the national ERI has averaged 0.60 with no tendency to increase or decrease.

14. See Tables 1-5 and pages 13-17 of U.S. General Accounting Office (now Government Accountability Office), Unemployment Insurance: Role as Safety Net for Low-Wage Workers is Limited, Report GAO-01-181 (Washington, D.C.:USGAO, December 2000). The U.S. Government Accountability Office has recently updated this earlier analysis, reaching qualitatively similar conclusions. See U.S. GAO, Unemployment Insurance: Low-Wage and Part-Time Workers Continue to Experience Low Rates of Receipt, Report GAO-07-1147 (Washington, D.C.: USGAO, September 2007).

15. See Table 3 and associated text in Wayne Vroman, Labor Market Changes and Unemployment Insurance Benefit Availability, Unemployment Insurance Occasional Paper 98-3, (Washington, D.C.: Employment and Training Administration, 1998).

16. There is federal oversight of the speed and accuracy of state administrative decisions about eligibility.

17. Jeffrey Kling, Fundamental Restructuring of Unemployment Insurance: Wage-Loss Insurance and Temporary Earnings Replacement Accounts, Hamilton Project Discussion Paper 2006-05, September 2006. http://www.brookings.edu/views/papers/200609kling.pdf.

18. See the Bureau of Labor Statistics (BLS) news release USDL 06-1454 “Worker Displacement 2003-2005” (August 17, 2006) also at www.bls.gov/cps/.

19. The previous CPS supplement (January 2004) indicated that 5.3 million workers with three or more years of job tenure were displaced during the high unemployment period from January 2001 to December 2003.

20. Three other eligibility requirements are: 1) one year of work experience with the pre-displacement employer, 2) work with a different employer on the post-displacement job, and 3) a non-disqualifying separation from the pre-displacement job.

21. See Howard Bloom, et al. Testing a Re-employment Incentive for Displaced Workers: The Earnings Supplement Project, Social Research Demonstration Corporation, May 1999.

22. To ensure employer obligations are met, firms are required to purchase policies against bankruptcy.

23. This statement assumes that the Congress operates under pay-go discipline, i.e., any change in expenditures has to be financed by some combination of increased taxes and reduced spending elsewhere in the federal budget.

24. See Ana Ferrer and Craig Riddell, Unemployment Insurance Savings Accounts in Latin America: Overview and Assessment, Department of Economics, University of British Columbia, September 2004.

25. See German Acevedo, Patricio Eskenazi, and Carmen Pages, Unemployment Insurance in Chile: A New Model of Income Support for Unemployed Workers, World Bank Social Protection Discussion Paper, June 2006, and Wayne Vroman, Unemployment Protection in Chile, report to the World Bank, The Urban Institute, August 2003.

26. The combined employer-employee contribution rate of 3.0% is some four to six times the average contribution rate (as a percent of to

tal payroll) for regular UI in the United States.

27. The December 2006 maximum benefit during the first month was 134,149 pesos in the new program compared to 17,338 pesos in the old program.

28. In the 22 years between 1975 and 2006 for which estimates of the unemployment rate can be obtained, Chile’s unemployment rate has never fallen below 6.1% and just five of those 22 years had unemployment rates between 6.1% and 6.9%.

29. Presumably these limits evolve as the federal minimum wage changes.

30. This discussion uses the term uncertainty in the general sense that the individual faces a range of possible outcomes. Because the distribution of outcomes may or may not be known, elements of both risk and uncertainty (as these terms are used by economists) are present.