Now It’s Explicit: Fighting Inflation Is a War to Ensure That Real Wages for the Vast Majority Never Grow

Remember that episode of The West Wing when Josh Lyman announced a secret plan to fight inflation? That was great. Turns out that Dallas Federal Reserve Bank President Richard Fisher has a secret paper telling us how to fight inflation: stop progress in reducing unemployment so that nominal wages never grow fast enough to actually boost living standards (or, never grow fast enough to boost real wages).

Last week, Fisher argued that a so-far unpublished (i.e. secret) paper by his staff showed that “declines in the unemployment rate below 6.1 percent exert significantly higher wage pressures than if the rate is above 6.1 percent.”

In the interview, Fisher mostly characterized this as a Phillips curve that is flat at unemployment rates higher than 6.1 percent, but which starts to have a negative slope below this rate, meaning that future declines in unemployment should be associated with higher rates of wage-growth. However, if you’re really thinking in terms of a stable Phillips Curve, this means that we can simply choose what unemployment/wage-inflation combination we’d like without worrying about accelerating inflation. Currently, nominal wage-growth is running around 2-2.5 percent. But as we’ve shown before, even the Fed’s too-conservative 2 percent inflation target is consistent with nominal wage growth of closer to 4 percent. So we have plenty of room to move “up” Fisher’s Phillips Curve before hitting even conservative inflation targets.

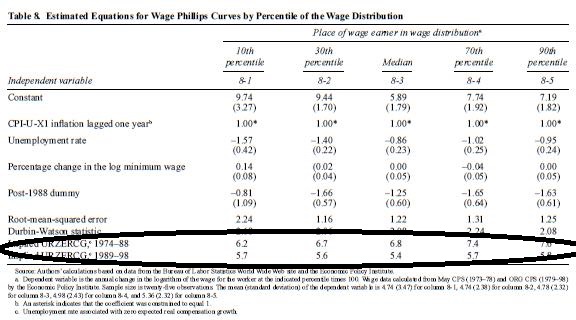

Also, the 6.1 percent threshold, beside being funnily precise, jogged my memory about something related—and relevant. In 2000, Larry Katz and Alan Krueger wrote a long paper on wages and unemployment. Among lots of other stuff, they estimated the lowest unemployment rate consistent with zero real (inflation-adjusted) wage growth for different parts of the wage distribution (which they label URZERCG in the table below). See the circled bits below, and focus in particular on the 10th percentile. This says that between 1974 and 1988, the 10th percentile had to see unemployment below 6.2 percent to not have their real wages fall. In the 1990s, wage headwinds were worse, and unemployment rates below 5.7 percent were needed. The deterioration of structural wage growth was even worse for the median. In the 1974-1988 period, they could see real wage gains with unemployment as high as 6.8 percent, but by the 1990s they needed unemployment to reach 5.4 percent to see any inflation-adjusted wage gains.

In replicating the Katz/Krueger work for the wages chapter in State of Working America, I actually calculated the URZERCG for the 10th percentile myself. I found basically identical results to Katz/Krueger results for the 80s and 90s, but by the 2001-2007 business cycle, the 10th percentile needed unemployment rates of 4.6 percent to not see their wages fall.

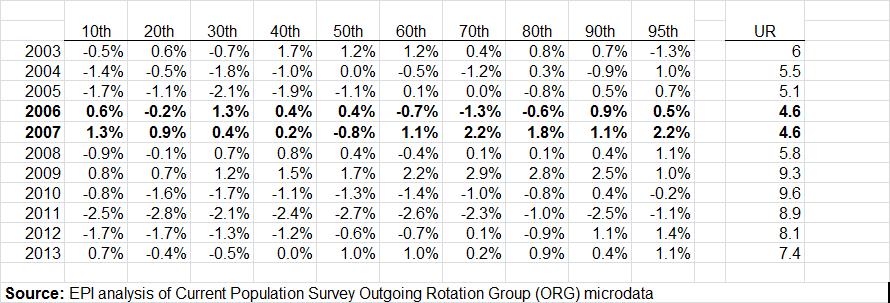

And, this fits with what actually happened over that business cycle. As the labor market recovered from the recession and jobless recovery of 2001-03, wages fell: by 2006 unemployment had reached 4.6 percent and it stayed that year on average for 2007. And this was the only two-year stretch that saw positive real wage growth at the bottom. The table below shows real hourly wage growth for years since 2003 and the associated year-round unemployment rate, using the supplemental data from our recent paper on wage-trends.

So, Fisher’s recommendations are pretty extraordinary—we have somebody who votes on monetary policy arguing that we should pull back on support for lowering unemployment even before we’ve reached levels that will keep real wages for the majority of the wage distribution from outright falling. He actually identifies improved wages as the problem we must confront.

And he wasn’t alone in his last dissent. It’s definitely time to fill the two open slots on the Fed’s Board of Governors with evidence-minded economists who don’t think real wage growth that is greater than zero is threat to the economy.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.