As talk grows of a June interest rate increase, where’s the data to support it?

This piece originally appeared in the Wall Street Journal’s Think Tank blog.

Weak data had convinced many that the Federal Reserve was unlikely to raise interest rates in June, but in recent days multiple Fed policymakers have suggested that an increase should be on the table in the near future. What’s unclear is why.

Little new data have emerged to suggest that the economy is much better than it was six or nine months ago. Since interest rates were raised in December, in fact, the pace of economic improvement has slowed almost to a stall.

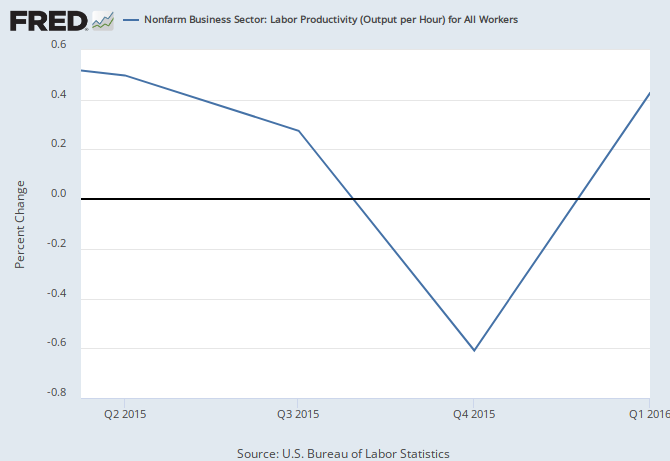

Gross domestic product grew at 1.4% in the fourth quarter of 2015 and at 0.5% in the first quarter of 2016. These annualized rates represent extraordinarily weak growth over a six-month period, driven by declines in labor productivity (GDP divided by total hours worked in the economy) in both quarters.

{kind=link}

This decline in productivity has largely been driven by historically anemic growth in business investment. Basically, in the face of weak demand, businesses have had little incentive to invest in new or better capital stock (physical plants and equipment). A larger capital stock gives workers more and better tools with which to do their jobs, making them more productive. But the extremely sluggish growth in business investment during the recovery has held back productivity growth.

{kind=link}

A related contributor to slow growth in labor productivity is still-weak growth of compensation. Firms respond to rapidly rising labor costs by investing in measures to economize on labor (or boost productivity). But compensation growth over the recovery remains weak, and suggestions that a decisive increase in compensation growth has arrived have proven premature.

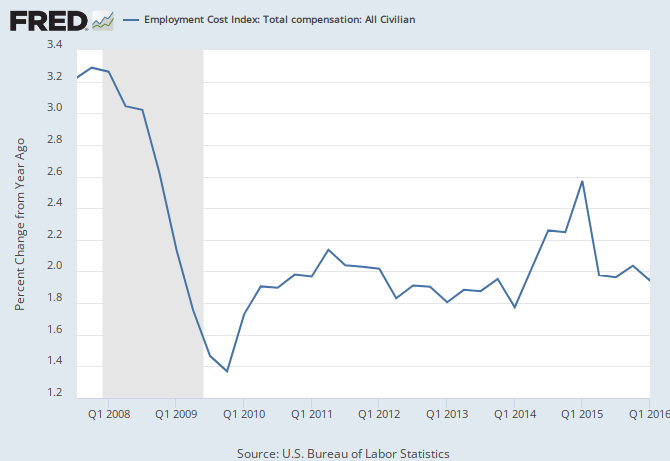

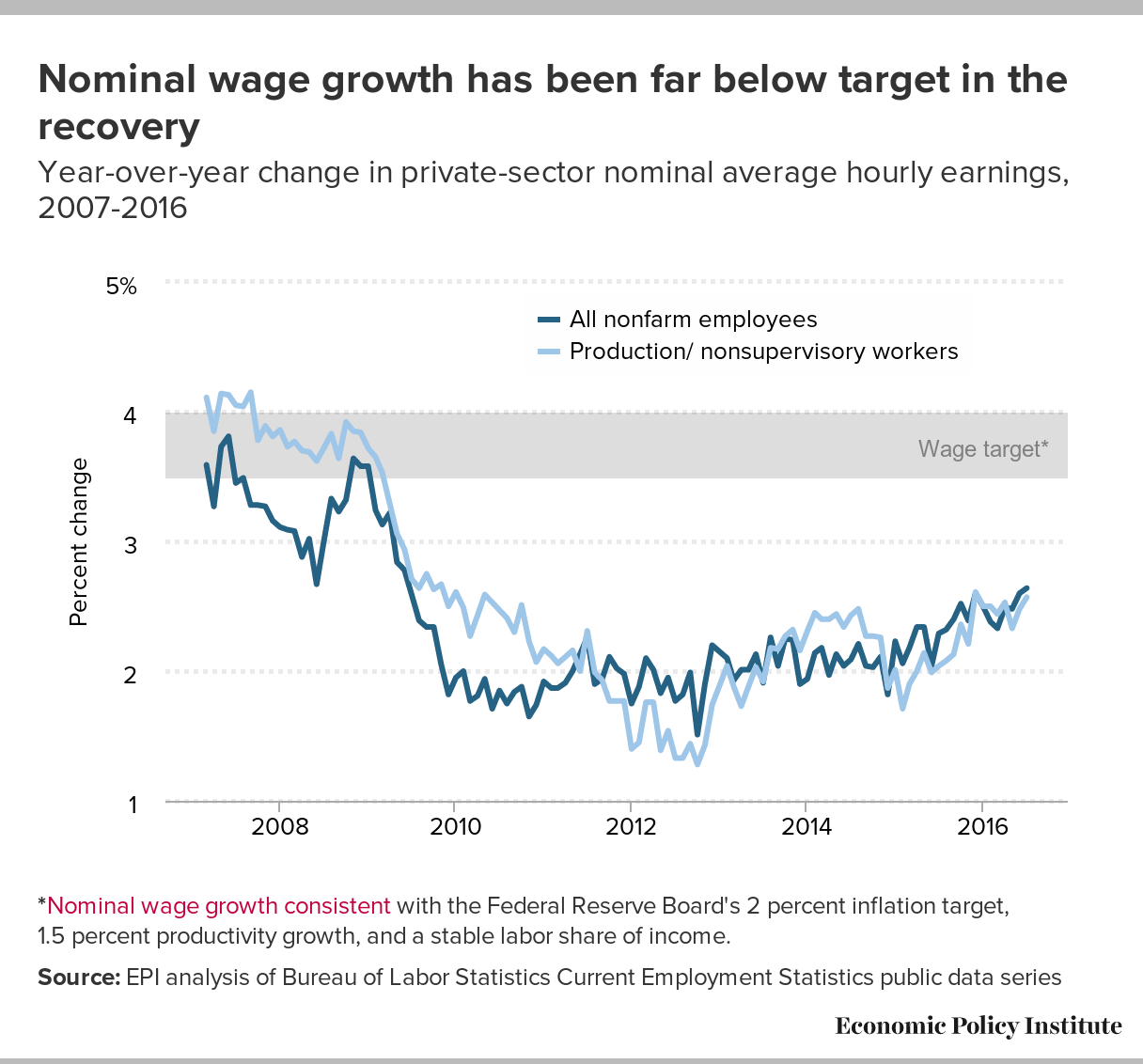

The Employment Cost Index for total compensation (including non-wage benefits) accelerated slightly in 2014 and 2015, reaching a peak growth rate of 2.6% in the first quarter of 2015. It has, however, slowed in every quarter since, matching its lowest growth rate in two years by the first quarter of 2016. Somewhat confusingly, growth in wages and salaries has uncharacteristically outpaced growth in benefits, leading to a slight uptick in some measures of wage growth. But the hyped measures of wage growth are still far too low for a healthy economy. Current growth rates of labor compensation are too low to put enough upward pressure on overall prices to meet the Fed’s 2% target for overall price inflation. These compensation growth rates are also far too low to allow workers to claw back the share of national income they lost during earlier phases of this recovery. In short, on the most fundamental metric that should eventually spur an interest-rate increase–cost pressure stemming from excess tightness in labor markets–there has been a slight regress in recent months.

{kind=link}

{kind=link}

{kind=link}

This failure to generate labor cost pressure explains why inflationary expectations and inflation remain extraordinarily low while productivity growth has decelerated rapidly. The Fed’s preferred inflation target—the “core” index of personal consumption expenditures, a measure that excludes food and energy prices, which tend to be volatile–has ticked up a bit in recent quarters; still, it remains below the 2% target. Each quarter that inflation is below the target suggests that an extended period of above-target inflation growth is needed to normalize the economy. Raising rates in June before the economy has firmed up would risk hardening the long-run price inflation target into a ceiling instead of an average.

Recently, Esther George of the Kansas City Fed and Eric Rosengren of the Boston Fed have argued for raising rates to help fight asset market bubbles. This justification for rate increases has become common enough that an Economic Policy Institute colleague and I recently wrote a brief arguing that interest rate increases are a terrible first tool to combat asset market bubbles. Rate hikes are inefficient bubble-fighters: The level to which rates would have to rise to snuff out bubbles implies ruinous outcomes for unemployment and inflation. Some have argued that the Fed should have raised interest rates to burst the housing bubble in the early 2000s. Empirical estimates of the effect of higher rates on home prices indicate, however, that rates would have had to skyrocket to restrain the bubble. And skyrocketing rates would have led the economy to never emerge from the recession and jobless recovery of 2001-03.

The Fed has a range of tools better suited for targeting asset market bubbles. The simplest is talking. Much attention has focused on the “forward guidance” the Fed has issued during the recovery. That guidance is simply communication. In the context of interest rate policy, it means providing strong guidance to markets about the likely future path of rates so that market participants are not caught flat-footed by Fed actions. Fed communication could also extend to economy-threatening bubbles when they arise. If the Fed mobilized data and communication to highlight where asset prices had diverged significantly from underlying fundamentals, that could make it much harder for market participants to continue propping up prices, confident that they could say “Who could have known?” when these investments lost value after bubbles burst.

Policymakers concerned with stopping bubbles should be talking more about these options for restraining them. Another benefit is that they would do much less collateral damage to the overall economy than sharp rate increases.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.