The American Jobs Plan’s tax provisions are valuable but not the limit on possible spending

The spending in the American Jobs Plan (AJP) is well targeted to meet several (but obviously not all) pressing social needs. Because so much of the spending is temporary and provides needed investments, there is no pressing economic need to “pay” for it with tax increases. Yet the tax provisions in the AJP are also smart and valuable. This post discusses some of the economics of the AJP, with a special focus on these tax provisions. Its main findings are:

- The bulk of these tax provisions undo some of the worst parts of the Tax Cuts and Jobs Act (TCJA) passed in the first year of the Trump administration. Given this, to make the case that rolling back these parts of the TCJA will harm the U.S. economy, one has to believe that the passage of the TCJA benefited the U.S. economy. There is no evidence this is the case.

- The entire case for corporate tax cuts benefiting the U.S. economy hinges on the effects on business investment. But business investment growth in the two years following the TCJA’s passage (even before the COVID-19 shock) was cratering, not rising.

- The vast majority of new revenue that will be raised from the AJP tax provisions will come from taxing “excess profits”—profits accrued by virtue of monopoly or other privileged market positions. As such, this extra revenue will have little to no effect on economic decision-making and hence will not reduce business investment or economic growth more generally.

- Two “model-based” analyses of the AJP find very different things: Moody’s Analytics forecasts strong positive effects on economic growth over the next 10 years, while the Penn Wharton Budget Model forecasts very slight negative growth effects by 2030. The finding that the AJP might reduce economic growth rests on a number of bad assumptions: that the corporate tax changes will significantly affect economic decision-making and reduce investment; that the productivity gains stemming from public investment are small; that budget deficits will crowd out large amounts of private capital formation over the next decade; and that AJP’s care investments will reduce labor supply. None of these assumptions are likely to be correct.

Ignoring the sad lessons of the Tax Cuts and Jobs Act

The signature economic policy achievement of the Trump administration (at least before the COVID-19 shock) was the TCJA, which was largely a corporate tax cut (among other things, it reduced the corporate income tax rate from 35% to 21%). In the run-up to passage of the TCJA, a long debate about the likely effects of corporate tax cuts was waged. The Trump administration made bold claims that the passage of the TCJA would lead to immediate and large wage increases for U.S. workers.

The textbook argument linking corporate tax cuts to wage increases rests on a long series of causal links. First, the lower corporate rate increases the post-tax return to investment and hence makes a larger number of potential investment projects profitable. Second, the higher post-tax return to capital also leads to increased savings (either domestic or foreign) and this increase provides the financing for the increase in desired investment. Third, these two previous influences in turn allow for a greater volume of investments in the capital stock of the business sector—leading to the purchase of more structures, equipment, and research and development services. Fourth, this larger capital stock gives U.S. workers more and better tools with which to do their jobs, increasing their productivity. Fifth, the productivity gains are seamlessly translated into wage gains.

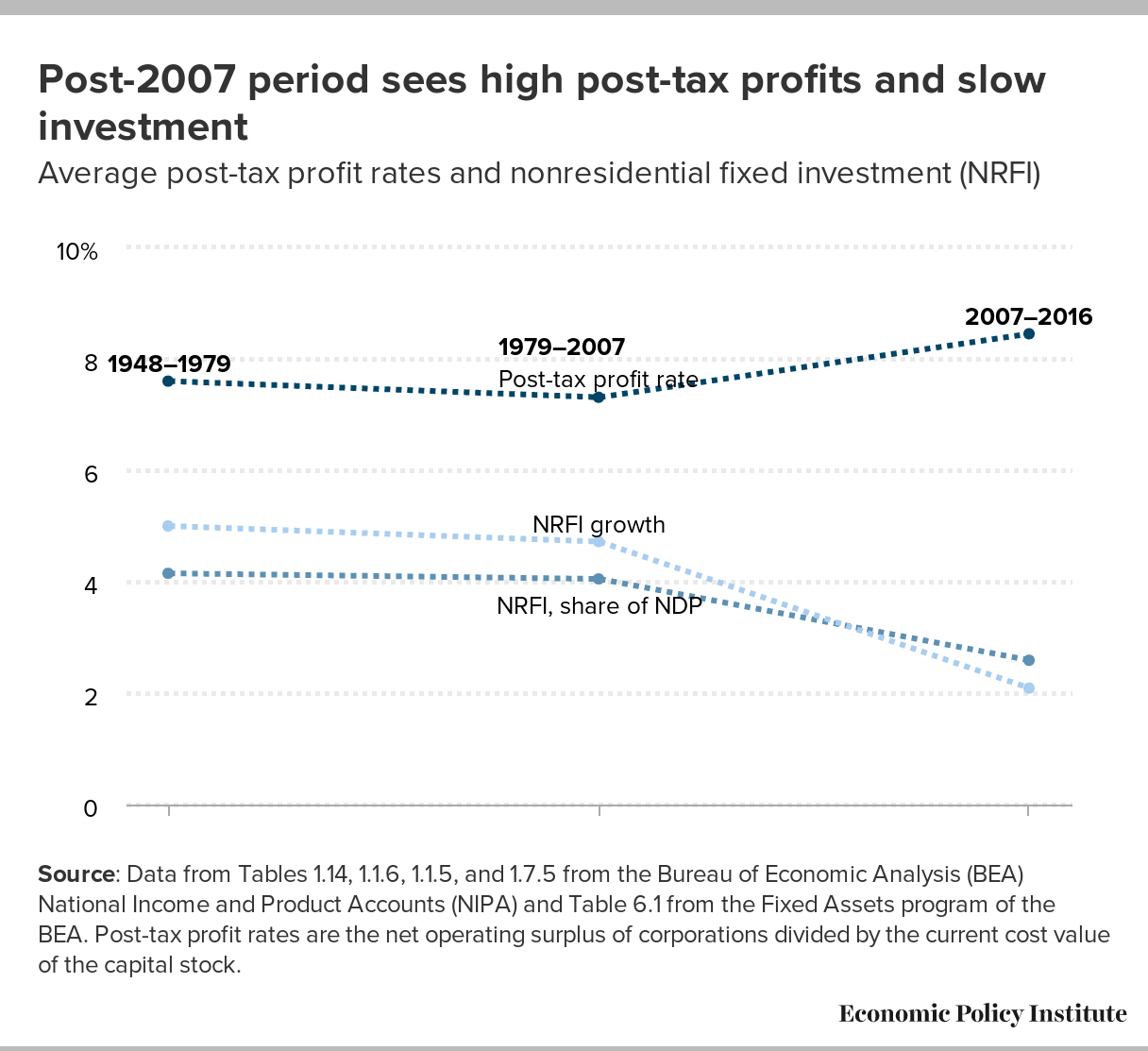

As we noted during this previous debate, most of the links of this causal chain are clearly broken. Over the past decade, profit rates and margins in the U.S. corporate sector reached record highs, yet investment was extraordinarily weak. Clearly it was not too-low rates of return muffling investment. This weak investment was almost surely driven overwhelmingly by weak growth of aggregate demand (spending by households, businesses, and governments), and anything that boosted savings would just depress demand even further. Predictably, the passage of the TCJA did not see an investment surge. Instead, business investment in the two years following the TCJA (but before the COVID-19 shock) was notably weak—and getting weaker even before the recession began in March 2020 (see Figure A).

{kind=link}

More evidence the Trump tax cuts aren’t working as advertised: Change in real, nonresidential fixed investment shows no investment boom

| Years | Real, nonresidential fixed investment |

|---|---|

| 2003-Q1 | -2.3% |

| 2003-Q2 | 1.6% |

| 2003-Q3 | 4.0% |

| 2003-Q4 | 6.8% |

| 2004-Q1 | 5.2% |

| 2004-Q2 | 4.9% |

| 2004-Q3 | 5.7% |

| 2004-Q4 | 6.5% |

| 2005-Q1 | 9.2% |

| 2005-Q2 | 8.2% |

| 2005-Q3 | 7.4% |

| 2005-Q4 | 6.1% |

| 2006-Q1 | 8.0% |

| 2006-Q2 | 8.2% |

| 2006-Q3 | 7.8% |

| 2006-Q4 | 8.1% |

| 2007-Q1 | 6.5% |

| 2007-Q2 | 7.0% |

| 2007-Q3 | 6.8% |

| 2007-Q4 | 7.3% |

| 2008-Q1 | 5.8% |

| 2008-Q2 | 3.8% |

| 2008-Q3 | 0.2% |

| 2008-Q4 | -7.0% |

| 2009-Q1 | -14.4% |

| 2009-Q2 | -17.1% |

| 2009-Q3 | -16.1% |

| 2009-Q4 | -10.3% |

| 2010-Q1 | -2.3% |

| 2010-Q2 | 4.1% |

| 2010-Q3 | 7.5% |

| 2010-Q4 | 8.9% |

| 2011-Q1 | 8.0% |

| 2011-Q2 | 7.3% |

| 2011-Q3 | 9.3% |

| 2011-Q4 | 10.0% |

| 2012-Q1 | 12.9% |

| 2012-Q2 | 12.6% |

| 2012-Q3 | 7.2% |

| 2012-Q4 | 5.6% |

| 2013-Q1 | 4.3% |

| 2013-Q2 | 2.3% |

| 2013-Q3 | 4.4% |

| 2013-Q4 | 5.4% |

| 2014-Q1 | 5.5% |

| 2014-Q2 | 8.1% |

| 2014-Q3 | 8.4% |

| 2014-Q4 | 6.9% |

| 2015-Q1 | 5.3% |

| 2015-Q2 | 3.0% |

| 2015-Q3 | 1.3% |

| 2015-Q4 | -0.1% |

| 2016-Q1 | -0.3% |

| 2016-Q2 | -0.1% |

| 2016-Q3 | 0.7% |

| 2016-Q4 | 1.8% |

| 2017-Q1 | 3.6% |

| 2017-Q2 | 3.6% |

| 2017-Q3 | 2.9% |

| 2017-Q4 | 4.8% |

| 2018-Q1 | 6.4% |

| 2018-Q2 | 7.4% |

| 2018-Q3 | 7.5% |

| 2018-Q4 | 6.5% |

| 2019-Q1 | 4.5% |

| 2019-Q2 | 2.9% |

| 2019-Q3 | 2.7% |

| 2019-Q4 | 1.4% |

| 2020-Q1 | -1.3% |

| 2020-Q2 | -8.9% |

Note: Chart shows year-over-year change in real, nonresidential fixed investment from 2003Q1 to 2020Q2.

Source: Adapted from Figure A in Hunter Blair, "The Tax Cuts and Jobs Act Isn’t Working and There’s No Reason to Think That Will Change," Working Economics (Economic Policy Institute blog), October 31, 2019.

Source: Adapted from Figure A in Hunter Blair, The Tax Cuts and Jobs Act Isn’t Working and There’s No Reason to Think That Will Change, Economic Policy Institute, October 2019. Data are from EPI analysis of data in Table 1.1.6 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Finally, it is always worth noting that the primary impediment to decent wage growth in recent decades has not been a lack of productivity growth, but instead a failure to translate the productivity growth the economy did see to higher wages for the vast majority. Cutting corporate income tax rates likely would make this translation of productivity growth to wage growth even harder, as these cuts would incentivize efforts for capital owners and corporate managers to suppress wages even more than they had been (because these capital owners and corporate managers would get to retain more of every dollar in post-tax income they managed to keep from going to wages for rank-and-file workers).

Taxing excess profits doesn’t affect economic decision-making

The weak growth of demand over the past decade explains a good part of why high profitability didn’t translate into strong investment. But another key point as to why the TCJA failed so spectacularly is that a growing share of corporate income over time represents “excess profits.” A 2016 paper by the U.S. Treasury’s Office of Tax Analysis (OTA) estimated that three-quarters of corporate profits represented “excess profits.” One illustrative piece of evidence confirming this is that the high corporate profit rates that characterized the post–Great Recession recovery came during a time when “risk-free” interest rates (those paid on U.S. Treasury debt) were historically low. If corporate profits represented just the return to financing normal business investments in structures and equipment, then they should follow these risk-free rates more closely.

Additionally, the current corporate income tax includes generous depreciation allowances for new investments. This essentially guarantees that taxes fall only on profits in excess of the cost of these new investments—that is, they fall only on “excess” profits. These excess profits are essentially by definition those that are protected against being eroded away through normal economic competition. As such, if you tax a share of these excess profits away, there is still no reason why the owners of the capital generating the profits will have any incentive to do less investment—they’re still earning returns higher than they would if they invested anywhere else, and they’re still earning more than the cost of financing these investments at the going interest rate. This in turn means that raising taxes should not affect economic decision-making and should specifically not lead to reductions in business investment. This growing importance of excess profits likely explains why there is also no correlation between changing corporate tax rates and investment in cross-country evidence as well.

In short, if the TCJA did not lead to an investment boom—in significant part because it just cut taxes on excess profits—then there is no reason to think rolling back much of its worst provisions and collecting more revenue from corporate income taxes will lead to an investment bust.

Two competing estimates of the AJP forecast different economic outcomes, but critiques of the Biden plan are less convincing

Recently, two “model-based” estimates of the AJP were released, one by Moody’s Analytics and one by the Penn Wharton Budget Model (PWBM). The Moody’s analysis finds strongly positive net effects on macroeconomic performance in coming years, forecasting that GDP would be higher by just under 3% by 2030. The PWBM analysis concluded that the AJP would actually reduce overall growth very slightly, forecasting GDP that is lower by 0.25% by 2031.

It is clear that the Moody’s analysis is more convincing. The differences between the two studies center on a number of points of contention: the strength of the AJP tax provisions in affecting business investment; the strength of “crowding out” of business investment due to the near-term (next 10 years) effect of the AJP on federal budget deficits; the productivity-enhancing effects of public investments; and the effect of care investments on labor supply.

On the effect of corporate income tax increases, both model-based studies see some effect of higher corporate income taxes in depressing business investment. But in the Moody’s model, the effects are small enough that they get swamped quickly by the benefits of public investment. In the PWBM model, the negative effects are strong and persist. We think this gives far too much credence to theories that business investment responds robustly to corporate income tax changes. As we’ve discussed above, since the TCJA did not boost business investment, it is hard to see how a reversal of it and further efforts to raise revenue from the corporate income tax will harm investment. It’s worth noting that the PWBM did indeed predict an increase in investment resulting from the TCJA. Yet despite a highly favorable macroeconomic environment for business investment in 2018 and 2019, this investment was weak (and falling over that time).

Oddly, some of the tax provisions in the AJP that the PWBM indicate are the most damaging to U.S. growth are essentially those that clamp down on the flagrant tax avoidance engaged in by U.S. corporations in recent decades—specifically by reforming the taxation of corporate profits earned abroad. However, it makes little sense to think that stopping this kind of financial engineering for tax avoidance purposes will actually lead to less economic activity within the United States. If anything, the corporate income tax status quo actually incentivizes the shifting of both paper profits and actual productive activity abroad. Clamping down on international tax havens—and hopefully beginning a multilateral process that clamps down even more—is the most promising part of the provisions. There is even evidence that the shifting of paper profits out of the United States to tax havens in recent decades has reduced measured growth in U.S. gross domestic product (GDP). All else equal, ending this shift should boost measured GDP.

On the issue of federal budget deficits, both analyses allow for some effect of larger budget deficits over the next 10 years in “crowding out” business investment. The Moody’s analysis assumes such effects are modest, with the larger deficits over the next 10 years pushing up 10-year Treasury interest rates by just 0.05%. The larger PWBM estimates on “crowding out” are implausible, for a number of reasons. For one, the economy still has quite a bit of slack left from the COVID-19 shock. Until this slack is taken up and labor and other inputs into production become scarce, it is hard to see how upward pressure on interest rates will begin. Typically, this upward pressure begins largely because the Federal Reserve begins raising the short-term “policy” interest rates it controls, which in turn feeds through to higher longer-term interest rates that might slow business investment. But the Fed has made it clear it thinks it will be some time before it will be impelled to raise its policy interest rates.

Further, even in models of full-employment economies, it is supposed to be projections of future deficits, not contemporaneous deficits, that drive interest rates in financial markets. Over the long run, the AJP tax provisions are larger than the spending provisions, so projected future deficits are smaller. Very strong “crowding out” effects from a wholly temporary boost to public investment accompanied by permanent tax increases starting in the context of a still deeply depressed economy just aren’t credible.

On the productivity-enhancing effects of public investments, the PWBM analysis uses estimates from the Congressional Budget Office (CBO). These estimates are far too conservative. In a review of more than 30 studies examining the productivity of public investment, Bom and Ligthart (2017) found that the average rate of return was well over three times as high as the CBO estimates, and the median return well over double. If one restricts the Bom and Ligthart sample to just studies of the United States, the results remain essentially the same. The conservativeness of CBO estimates of the rate of return to public investment has been pointed out by Larry Summers a number of years ago as well. Moody’s explicitly notes (in footnote 1 of their study) that they are using a higher estimate than what is used by the CBO.

The last difference between the two model-based estimates concerns their treatment of the AJP care investments. The Moody’s analysis does not explicitly mention them, but it does highlight strong potential effects on labor force participation stemming from the overall package (it is slightly unclear whether there is a specific care investment effect being measured or if it is just assessing the physical infrastructure investments). PWBM asserts that the spending on care work in the AJP is simply a “transfer” payment that will unambiguously reduce labor supply, as “transfers to working-age households let individuals work less without consuming less, reducing overall labor supply.” This misses a large potential effect of the caregiving investments: They allow a huge number of working-age people (overwhelmingly women) who are currently providing unpaid work to care for loved ones to return to paid work if this care becomes more affordable and higher-quality. Compelling research shows that large caregiving investments made over the next decade could significantly boost, not reduce, labor supply and hence GDP growth. For example, Shen (2020) finds that for every 2.4–3 women whose parents receive formal home care as a result of expansions of public financing on home care, one of them will join the paid labor force full time.

Both the spending and tax provisions of the AJP are solid investments in the future

Again, the spending provisions of the AJP will successfully target many pressing social needs and are clearly investments—they will spur overall growth in coming years even over and above any useful effect they have in increasing spending and alleviating current shortages of aggregate demand. The tax provisions of the AJP will fix decades of corporate gaming of the U.S. tax code—most spectacularly with the TCJA of 2017. It will also provide a much more solid foundation to approach other countries around the world in an effort to build a united front against race-to-the-bottom tax competition and abusive tax havens. Being able to tax rich households and corporations for the social good is a key part of a decent society, and tax havens and global tax avoidance are key impediments to this ability. Fixing this would be a huge investment indeed in the future of the United States.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.