Nevada state government has fiscal challenges–but granting state employees the right to bargain collectively does not add to them

A bill introduced in the Nevada State Senate (SB135) would allow state workers to collectively bargain over wages and benefits, a right they have been denied since 1965.

Opponents of public sector unions have begun making the usual arguments against granting Nevada state employees these rights. In two recent reports the Las Vegas Metro Chamber of Commerce (COC) and the Nevada Policy Research Institute (NPRI) make two essential arguments: granting state employees the right to bargain collectively will increase state spending and hence the tax burden on Nevadans, and these state employees are already overpaid, and collective bargaining rights would just make this worse. This logic ranges from myopic to misleading to outright false.

Take the first argument—that collective bargaining rights will reliably lead to higher state spending and a higher tax burden on Nevadans. The opposition to SB135 is trying to invoke a knee-jerk response from Nevadans to see higher spending as a bad thing always and everywhere; but what’s the evidence that Nevada’s spending has become bloated instead of inefficiently low? Take higher education. In the decade between 2008 and 2018 inflation-adjusted higher education spending per student in Nevada fell by 22.2 percent, a much worse performance than the national average. These cuts led directly to a staggering 56 percent increase in tuition for public universities over this same time period—one of the ten steepest tuition increases across the 50 states. Given this track record, the real problem facing Nevadans doesn’t seem to be ever-growing spending, but savage austerity that is sacrificing the future.

But maybe granting collective bargaining rights will radically overcorrect this problem and lead to Nevada becoming a profligate spender? It hasn’t happened in the K-12 education sector, where local government employees (including all teachers) currently have the right to bargain collectively. Even in this sector the downward pressure leading to inefficiently low spending has been ferocious. In a recent report card on education in Nevada, the Children’s Advocacy Alliance (CAA) gave the state an ‘F’ on funding, with low funding leading to some of the highest student-to-teacher ratios in the nation (48th out of 50). As recent teacher strikes over starved resources (not just pay) have shown in states like Oklahoma and West Virginia, lack of collective bargaining rights can lead to inefficiently low educational investments in states.

In short, the claim that collective bargaining rights always lead to bloated spending levels is a caricature. Instead, sometimes these rights provide a check (often insufficient) against relentless downward pressure on spending that leads to destructive cuts. The best empirical research linking public sector collective bargaining and state and local government spending finds mixed results, with the causal effect of collective bargaining rights in pushing up state spending either weak or non-existent. Given this evidence, the empirical claims made by opponents of SB135 about the magnitude of state spending increases that would occur should it pass are frankly absurd—they would require state employees’ compensation to rise by over 30 percent, with no beneficial effects on the state budget stemming from higher productivity or lower turnover or fewer state workers drawing public assistance benefits—all offsets that we know often accompany wage increases. The Chamber of Commerce study forecasts an even more outlandish increase—with total state spending forecast to rise more than the total amount spent on state employee compensation in the latest year of data.

Because the evidence is so inconvenient for those wanting to claim that granting collective bargaining rights to public employees leads always and everywhere to bloated spending, ideological opponents of unions often make another claim: public employees are overpaid and their pay can be cut without sacrificing the quality of services. Like all arguments promising a free lunch—in this case, that there will be no sacrifice in quality of public services even as taxpayers pay less—it should arouse some suspicion.

The evidence on public sector pay is clear: public employees are not paid more than their private sector peers. Before going into more detail on this, it is important to note that even if public sector pay in some state or local government did seem to offer a compensation premium over private sector workers, this would not justify stripping public employees of their fundamental human right to freely organize and bargain collectively. Instead, in this theoretical world of overpaid public employees, public-sector employers should bargain with the duly elected representatives of these employees to bring pay back into line with private sector benchmarks.

But, this theoretical consideration of public employees earning substantially more than their private sector peers is irrelevant in the case of Nevada. In its case, the evidence is clear: state government employees in that state make less than their private sector peers in total compensation—including benefits. In an apples-to-apples comparison that controls for the higher educational attainment of the public sector, along with some other relevant explanatory variables, state government employees see a substantial pay penalty in cash wages and salaries, on the order of 6-8 percent on average.1 Factoring in benefit costs, which are more difficult to estimate than wages and salaries, Nevada state employees’ total compensation is 1-13 percent lower than that of their private-sector counterparts, as will be explained in more detail below.

Though government employees are usually paid less on average than similarly qualified workers in the private sector, they are also less likely to be paid poverty-level wages than private-sector workers. Research has found that because unionization in both the public and private sector tends to raise the wage floor and improve benefits, this reduces taxpayer spending on means-tested government benefits such as Medicaid.

State government employees usually have better benefits than private-sector workers, though this is not necessarily true if you limit the comparison to large employers. In any case, it is no longer true in Nevada (regardless of establishment size), where state employees receive much less generous benefits than in most other states. State employees in Nevada are not covered by Social Security, and they shoulder half the total cost of the state employee pension, including—unusually—legacy costs attributable to past underfunding by the state. This means workers themselves actually paid for the bulk of the benefits they earned in 2017, with employers only contributing around 2.5 percent of pay to cover the remainder.2 State employees in Nevada also have less generous retiree health benefits than government employees in most other states.

Based on the 2017 cost of pension and retiree health benefits, state employee benefits were actually significantly lower for state employees in Nevada (33 percent of pay) than for workers in large establishments nationwide (45 percent of pay). 3 If the comparison is with all private-sector workers in the region, including those employed by smaller establishments, and if we average the cost over 2013-2017 to match the pay regression, then Nevada state employee benefits are more generous than in the private sector (43 percent versus 33 percent).4 Either way, total compensation remains lower in the state sector, ranging from 1 percent to 13 percent less than that of comparable workers in the private-sector, with the bigger compensation gap reflecting recent increases in state employee pension contributions, among other factors.

How, then, can critics claim public-sector workers are overpaid? First, they selectively include variables in the pay regression that tend to explain away the public-sector pay gap and exclude variables that tend to expand it. While the authors cited in the NPRI study, Andrew Biggs and Jason Richwine, have abandoned their controversial practice of omitting educational attainment from their pay regressions, they continue to include a detailed geographic variable that “explains” some of the lower pay of workers in the public sector by the fact that they tend to live in lower-cost neighborhoods than similarly qualified, but better paid, private-sector workers (discussed here). Biggs and Richwine also have a habit of excluding large groups of workers from pay regressions—in this case public safety officers, who tend to have compensation tilted in favor of benefits rather than pay. As a result, they find that state government employees in Nevada, excluding public-safety officers, were paid only one percent less than private-sector workers in the state in 2009-2012. As mentioned earlier, we find that, based on the same survey, state employees were paid 6-8 percent less than their private-sector counterparts in 2013-2017.

After explaining away the pay gap with faulty methods, Biggs and Richwine vastly inflate the cost of benefits, including supposed benefits that don’t cost taxpayers a dime but rather are a win-win for workers and taxpayers. One of these supposed benefits is job security, which Biggs and Richwine claim increases the compensation of state employees in Nevada by 8 percent relative to private-sector workers in the state. Leaving aside the question of whether public-sector workers in Nevada or elsewhere actually have more job security than similarly qualified private-sector workers after the government downsizing that occurred in the wake of the 2008 financial crisis, there is no reason to include lower turnover in this cost comparison since it is turnover, not employee retention, that is costly to employers.

Similarly, Biggs and Richwine more than triple the cost of public-sector pension benefits by claiming that these benefits are guaranteed, and therefore that the cost to taxpayers should be estimated based on the rate of return on Treasury bonds rather than the expected return on pension fund assets. The details are wonky (and explained in more depth here), but Biggs and Richwine are implicitly assuming that taxpayers are so afraid of investment risk, which can result in underfunded or overfunded pensions and therefore somewhat variable costs, that they would be willing to contribute more than three times as much to public pension funds to avoid this risk altogether—even though pension funds are better positioned than most investors to ride out market volatility. Or, to put it another way, Biggs and Richwine assume a dollar contribution to a pension fund has three times the value to workers as a dollar contribution to a 401(k)-style defined contribution plan because it comes with an implicit rate-of-return guarantee.

Biggs and Richwine cite like-minded economists to back up their assertion that “since public employee pension benefits are intended to be guaranteed and in most cases are protected under state laws or constitutions, a low discount rate should be used to reflect that low risk.” A more even-handed Government Accountability Office report pointed out that the rate of return used to estimate the value of future benefits depends on the context—including the measure of accrued benefits used. Biggs and Richwine falsely claim their measure of pension benefits reflects “guaranteed” (as opposed to “projected”) benefit obligations. In fact, the measure they use assumes salary increases that may never materialize and is decidedly not a measure of legally-protected benefits. Whatever credibility their school of thought had among financial economists was shattered in the wake of the 2008 market crash, as the Center for Retirement Research estimated that the entire cost to public pension funds was borne by workers in the form of higher cost sharing and reduced benefits—not by taxpayers.

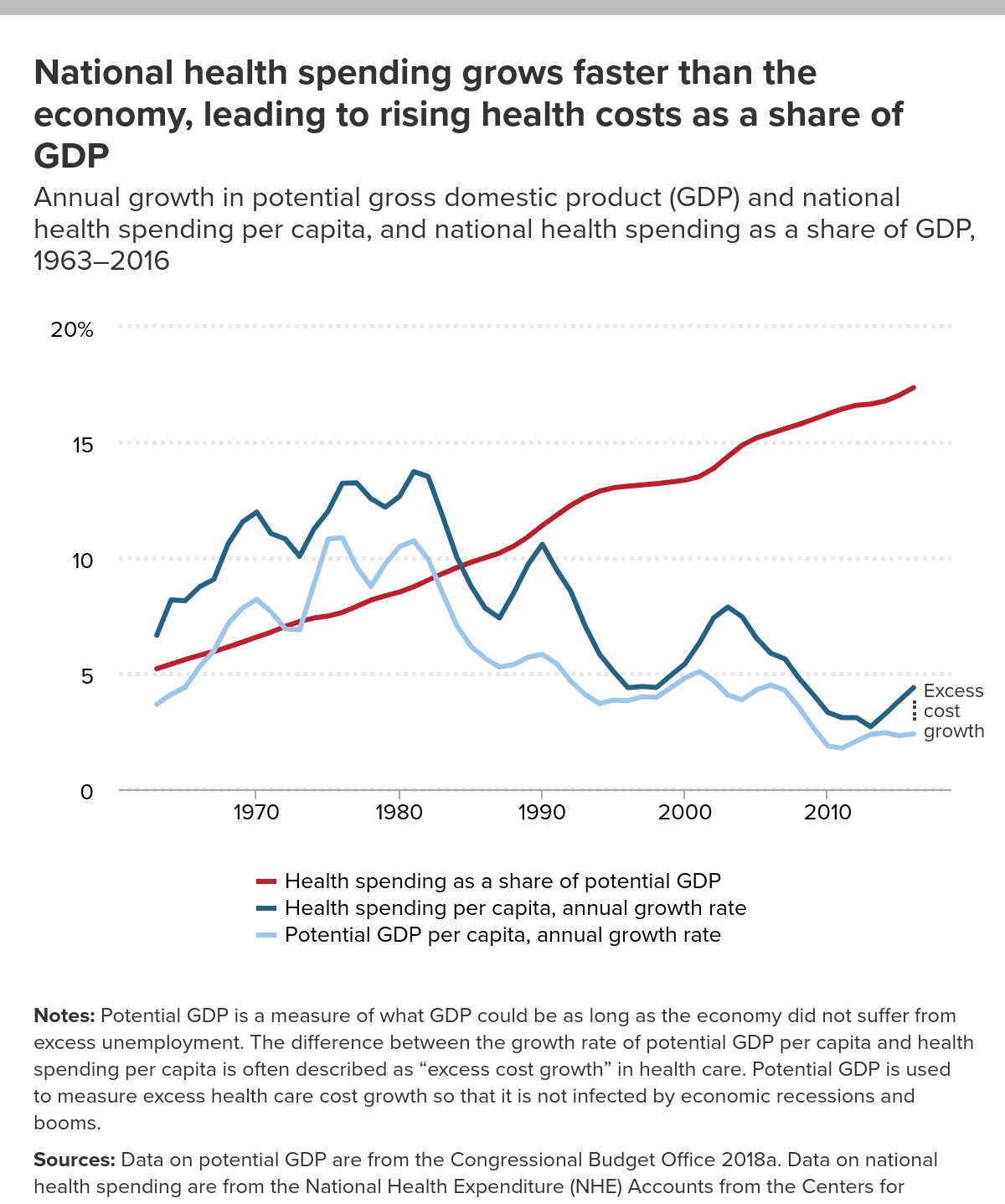

The value of public sector retiree health benefits also tends to be exaggerated, often by assuming high rates of “excess cost growth” in health care spending over very long time horizons. For example, actuarial valuations project continued health cost inflation, but not the increased cost sharing that inevitably results when costs escalate. These reports also assume, unrealistically, that healthcare costs will ratchet up indefinitely without policymakers intervening.

Not satisfied with these already-inflated cost projections, Biggs and Richwine magnify them further by again assuming a low rate of return to the funds set up to finance these costs. As a result, they estimate that employers would have to contribute an amount equal to 7 percent of pay each year to pre-fund Nevada state employees’ relatively meager retiree health benefits.

In our own estimates, we simply adopt the cost estimates in the 2013-2017 actuarial valuations, which range from 3 to 5 percent of pay, even though these are based on health cost inflation assumptions that are higher than recent experience (the most recent report assumes that health costs will increase by 6.5 percent annually in the short term and 5 percent annually in the long term—but in recent years per capita health costs have come in reliably below 5 percent). We ignore retiree health costs in the private sector entirely, since these benefits are not common in the private sector and their cost is hard to estimate (assuming they’re zero makes our estimate of the public-sector compensation gap more conservative). Biggs and Richwine assume retiree health costs in the private sector amount to 0.5 percent of pay.

{kind=link}

We should be clear that the relative pay of public sector workers compared to private sector peers is not uniform. Generally, workers with lower educational credentials see smaller compensation penalties—and sometimes even higher relative pay—compared to private sector peers, while workers with college degrees and above in the public sector see larger pay penalties. However, workers without a four-year college degree have seen absolutely abysmal labor market outcomes for most years in recent decades, as their pay has been assaulted by a number of policy-driven efforts to hamstring their bargaining power and leverage in the labor market.

{kind=link}

This is the case in Nevada as well, where workers without 4-year college degrees are paid slightly more in the state sector based on regression-adjusted estimates that take into account differences in education, work hours and age. Factoring in benefits, these workers were better compensated than private sector workers without four-year college degrees, many of whom receive few employer-provided benefits—at least before employee contributions to the pension fund dramatically increased in 2016. We could, as a society, demand state and local governments employ every lever at their disposal to beat down compensation costs for the most vulnerable workers in the labor market—and some of these governments seem sadly willing to do it. But we think that is bad policy, and it will lead to worse state outcomes in the long-run as the quality of the workforce deteriorates and as more workers are forced to rely on means-tested government benefits.

In the end, there is little evidence that granting state government employees their human right to bargain collectively will lead to bloated spending. There is also little evidence that public workers are currently overpaid. So what’s behind the push in Nevada to ensure that state employees are not granted collective bargaining rights? Much of the push is simply an ideological agenda that tries to hamstring unions always and everywhere. We noted earlier the decades-long policy push to erode the bargaining power and labor market leverage of American workers by capital-owners and corporate managers—throttling the ability to bargain collectively is high on the list of this agenda. In Nevada specifically, however, it’s pretty easy to see why powerful actors might be extremely wary of any extra spending that asks for a contribution from taxpayers even as current spending is abnormally low. Nevada has one of the most regressive tax systems in the nation. The poorest fifth of Nevadans pay an effective state and local tax rate of more than 10 percent, while the richest one percent pay an effective rate of under 2 percent.

Further, Moody’s Analytics Economy.com has noted that the growing practice of granting tax abatements and incentives to businesses as an economic development strategy has held back revenue growth and further contributed to state budgets being tighter than they should be this far removed from the past recession.

All in all, for those genuinely worried about the tax bill typical Nevadans face, the first concern should not be eliminating basic human rights for the state’s workers, instead it should be figuring out how to get a fairer contribution from the state’s richest households and businesses.

Note: This blog post has been updated to correct a coding error in the regressions.

1. This is based on running separate regressions for workers with and without four-year college degrees, since the sectoral pay gap is different for these two groups of workers. Whereas less educated workers may benefit financially from being in the public sector, this is generally not true of more educated workers. The overall estimate of 6-8 percent is the weighted average of the college and non-college pay gap estimates. The smaller overall estimate (6 percent) is based on regression-adjusted comparisons that take into account differences in education, age, year, and usual hours worked. The larger overall estimate (8 percent) also adjusts for race and ethnicity, sex, marital status, and immigrant status, in addition to the above factors.

The rationale for controlling for demographic factors is that they may capture differences in work qualifications, or “human capital,” not reflected in survey data. For example, the pay gap between otherwise similar-seeming men and women may reflect unobserved differences in work experience at any given age since women are more likely to take time off from the labor force to raise children. However, to the extent that pay differences between demographic groups reflect labor market discrimination, including these controls will tend to minimize the public-sector pay gap if workers who experience discrimination are more likely to be employed—or less likely to be discriminated against—in the public sector (though this generalization does not hold true for Nevada, where the state workforce is less diverse). Biggs and Richwine include these demographic variables (as well as some less standard control variables), but estimate the sectoral pay gap with a single regression.

2. The current cost, or “service cost,” of accrued pension benefits was $1,107.5 million in 2017, of which $952.8 million was contributed by workers. Though the state contributed a roughly equal amount, most of this was to pay down legacy costs (Source: NVPERS Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018).

3. The cost of benefits as a share of compensation is based on summary statistics from the National Compensation Survey (NCS) accessed through the U.S. Bureau of Labor Statistics website, with certain adjustments. In all benefit cost estimates, supplemental pay, such as overtime, is included in pay rather than benefits. In this estimate, the benefit cost for private-sector workers is based on benefits in large (500+ employee) establishments nationwide, since larger employers tend to provide greater benefits as a share of compensation (NCS statistics for large employers are not available by region). For Nevada state employees, the cost of benefits is based on NCS statistics for state and local government employees nationwide, minus Social Security and retirement contributions, plus the “normal” or “service” cost of Nevada state employee pension and retiree health benefits for 2017 (NCS statistics are not available for government employees by region or for state government employees alone). The “normal” or “service” cost is an actuarial estimate of the cost of future benefits accrued in the current year, factoring in projected salary increases and health cost inflation.

4. In this estimate, the benefit cost for private-sector workers is for all private-sector workers in eight states, including Nevada, in the U.S. Census Bureau’s Western Region, Mountain Division (state-level statistics are not available). The estimate for state employees is the same as described earlier, but with pension and retiree health costs averaged over 2013-2017.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.