Not dead yet: Currency management and the need for a more competitive dollar

A number of commenters declare that currency management by our trading partners is an issue “whose time has passed.” At the risk of violating Brad DeLong’s wise rules (Paraphrased: “Mistakes are avoided if you follow two rules: (1) Remember that Paul Krugman is right, and (2) If your analysis leads you to conclude that Paul Krugman is wrong, refer to rule No. 1”), I’m not convinced by claims—even Krugman’s—that this is a dead issue.

Look at one key piece of evidence Krugman presents: the real (inflation-adjusted) appreciation of the yuan in the last year. But, as Krugman himself has said in previous writings on this:

“Notice that I didn’t mention the value of the renminbi at all in this account [ed: of China’s currency management]. … You want to keep your eye on the ball: it’s the artificial capital exports that are the driving force here.

We know that the renminbi is grossly undervalued … on a PPE (proof of the pudding is in the eating) basis: the current value of the renminbi is consistent with massive artificial capital export, and that’s that.” [Edited for clarity; I’m pretty sure I haven’t done any (much?) damage to his argument].

So, have the artificial capital exports from China continued? I haven’t delved into the data in a serious way for a long time (I think we’re all going to start missing Brad Setser and his data-work even more in coming years), but the latest Treasury report on foreign exchange rates indicates that China’s total reserve accumulation (i.e., their capital export) has proceeded strongly through the first quarter of 2012:

“Nevertheless, the underlying factors that distort China’s economy and constrain global demand growth remain. China accumulated $373.1 billion in additional foreign exchange reserves in the first three quarters of 2011. Reserve accumulation slowed in the fourth quarter to $11.7 billion, but increased again to $74.8 billion in the first quarter of 2012.”

Krugman also notes that this real appreciation of the yuan has been mostly spurred by higher Chinese inflation and points to the falling Chinese current account surplus as evidence that this real appreciation is doing its job.

The key question, however, is how durable this will all be. My guess is not very. The higher Chinese inflation has already greatly moderated, and was largely driven by commodity (and housing) price inflation as well as the big increase in domestic investment as China passed its own stimulus package in response to the Great Recession.

And the decline in China’s current account surplus can be attributed largely to the economic crises in the U.S. and the Eurozone in recent years. During the height of the Great Recession, American and Eurozone imports plummeted, from China and everywhere else. Since then, U.S. imports have been recovering (in fact, rising trade deficits have put a very mild drag on growth in the U.S. since the recovery began).

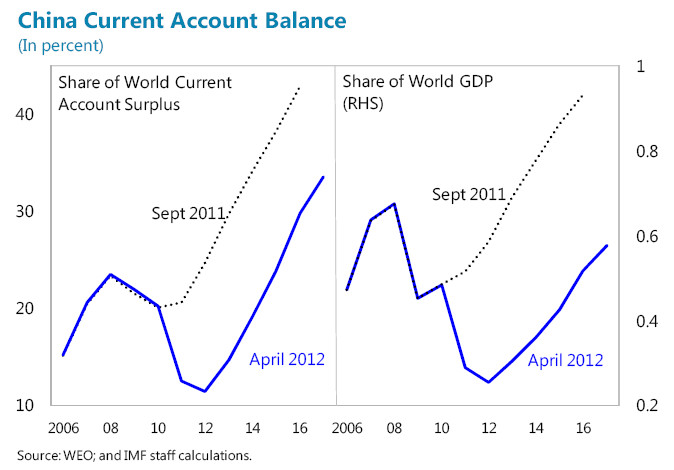

Further, a decline in the Chinese current account surplus measured as a share of its own economy can be slightly misleading in gauging its global impact. China’s economy is growing so rapidly that even a stable current account surplus measured as a share of its own GDP implies that the surplus is growing as a share of global GDP, or American GDP, or as a share of global trade balances. See the chart below from a recent IMF working paper on China’s imbalances—it shows the Chinese current account surplus as a share of both global trade surpluses and as a share of world GDP. Even under the mid-range estimate of the IMF that sees these surpluses at just 3.5 percent of Chinese GDP (down from a high of around 10.7 percent in 2006–2007) over the medium-term, they would grow rapidly measured against global trade flows and global GDP.

What does all this mean? That the fundamental forces that were driving large imbalances between China (in particular) and the U.S. economy (an undervalued yuan especially) are quite possibly still there. The pre-2007 trend of steadily rising Chinese current account surpluses was interrupted pretty spectacularly by the global economic crisis, but the prospect of a strong American recovery that is not plagued by some of the same international imbalances that characterized the pre-Great Recession period doesn’t look great to me without addressing the issue of currency management.

This diffidence about talking about China’s currency management makes some sense to me. Lots of people think that it amounts to blaming what is still a much-poorer country for what are America’s own economic problems. In a sense they’re right—it’s not China’s fault that U.S. policymakers have failed to, say, undertake the fiscal and monetary stimulus to get the nation back to full-employment. And it’s not even China’s fault that U.S. policymakers haven’t moved on the issue of currency management. Instead it’s the fault of corporate U.S. interests that gain from the undervalued yuan. But, this issue of “blame” just isn’t very useful: Currency management is not a moral failure, it’s just an economic policy that is clearly no longer good (if it ever was) for either the U.S. or China.

In the end, the issue is simple macroeconomics—we need a lower value of the dollar to reduce our trade deficit, and reducing our trade deficit is the only way we can have a rapid recovery over the medium-run without running larger budget deficits. Given that the politics of the day have (stupidly, but clearly) ruled out larger budget deficits, addressing the over-valued dollar is key. It’s worth stressing that there’s nothing magical or particularly malign in the fact that today’s overvalued dollar is driven by other governments’ policy decisions. In the past (the late 1990s), the dollar’s overvaluation has been driven by herds of private investors—and that should have been addressed as well (for different reasons, however, as unemployment in the late 1990s was genuinely low).

Today, however, the overvaluation is driven by currency management, and there is little evidence that this has stopped and that trade flows will be allowed to move closer to balance and contribute to U.S. recovery going forward. In this respect, the Joe Gagnon project of highlighting widespread currency manipulation is most welcome—this really should be an issue of debating the possible macroeconomic damage done by an overvalued currency, not an issue of how people want to feel about the rise of China.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.