American pay and productivity for typical workers: Still not growing together

James Sherk at the Heritage Foundation has written a piece claiming that there has been no gap between growth in productivity and growth in pay. It’s written largely as an attempted debunking of our work, but since there’s not actually any bunk in this work, the attempt fails.

Sherk raises many issues. Some have a bit of validity to them, some do not. I’ll discuss some of the nitpickier bits of his piece a bit later. In the end, however, the difference between his findings and ours boils down to the fact that he ignores the effect of rising inequality in driving a wedge between productivity and pay. And it’s true that if you ignore inequality, you get a much sunnier view of American wage performance in recent decades. But that’s the whole point, no?

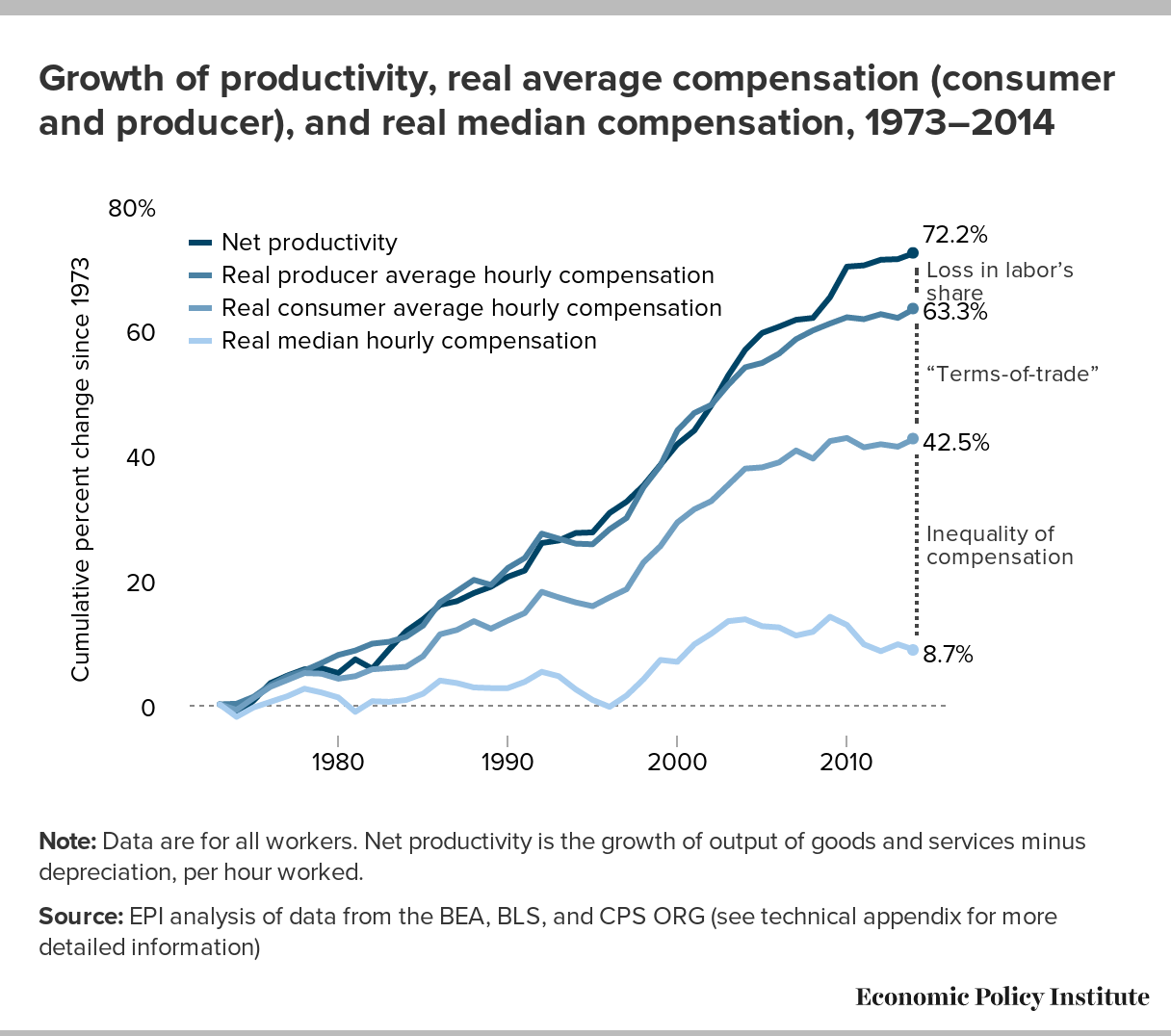

Past all the hand-waving, the difference between Sherk’s findings and ours is completely dominated by the same single point of contention that comes up in every debate about growth in productivity and pay: the difference between average versus typical pay growth. The title of our most recent piece on this topic is: Understanding the Historic Divergence Between Productivity and a Typical Worker’s Pay. That “typical” in the title is important. We look at two measures of hourly pay that we argue are relevant for typical American workers: average pay for private-sector production and non-supervisory workers from the Current Employment Statistics (CES) and the median worker from the Current Population Survey (CPS). Production and non-supervisory workers constitute 80 percent of the private workforce. We think that seems pretty typical. The median worker in the CPS is that worker who earns higher hourly pay that half of the workforce and lower hourly pay than half. This also seems broadly representative to us.

Sherk (and many others claiming to have debunked our work) look at average hourly compensation for the entire workforce. He insists that our choice to highlight the bottom 80 percent of the private-sector workforce, or the median worker, is a methodological mistake. It’s not—it’s a careful choice. Average hourly compensation for the entire workforce has been pulled up significantly in recent decades by extraordinarily fast growth at the very top of the wage distribution. This makes overall average compensation move closer in line with productivity, but this top-driven movement in overall average compensation is largely irrelevant to the economic fortunes of the vast majority of the American workforce. To put it too-bluntly, the fact that Mark Zuckerberg made $2.3 billion in 2012 tells us nothing about how the economy and the labor market are performing for typical workers.

The genesis of EPI’s analysis of productivity and typical workers’ pay stemmed exactly from debates wherein many argued that the only wage problems faced by American workers were those stemming from too-slow growth in economy-wide productivity. Slowing productivity growth is indeed, all else equal, a problem. But it turns out that most American workers had an even larger pay problem over the past generation—their rates of hourly pay growth severely lagged behind even the slowed-down growth in productivity.

If you think that that the clear empirical failure of economy-wide productivity growth to reliably raise the hourly pay of most American workers is not interesting, then you can feel free to ignore EPI’s work on this. But that’s what you’re doing—you’re not choosing a more methodologically complete or analytically sound approach, you’re just deciding to ignore the effect of inequality. The importance of ignoring inequality in driving the Sherk conclusions can be seen in his Table 1, which shows a huge gap between productivity growth and the pay of production and non-supervisory employees. But ignoring our work because you’re uninterested in the influence of rising inequality on the pay of American workers does not mean that our work has been “debunked.”

Our work highlights the two key prongs of this inequality wedge between productivity and hourly pay: rising inequality of compensation and the shift from overall labor income to capital incomes. Sherk’s analysis clearly shows the first, and the decline of labor’s share in recent years (since 2000, particularly) is well–documented.

In the report, Sherk raises many other points. Here is a lightning round of response to some of them:

- One of our wage measures (average pay for production and non-supervisory workers) doesn’t include performance pay. But the growth (see Table 2 in the link) of performance based pay has been concentrated in the upper portions of the pay distribution in recent decades, so is much less likely to have significantly boosted pay growth for our groups of typical workers

- Our wage measures do not include self-employed workers. Sherk strongly implies that this mechanically increases the gap between the growth of hourly pay and productivity. It does not. Including self-employed workers would only narrow the gap if their rate of hourly pay growth is substantially more rapid than our measures. He offers no evidence that this is so. Further, his remedy to this problem—taking sole proprietors’ income out of the numerator of the productivity measure while making no visible adjustment for hours in the denominator—seems not right.

- Sherk wants us to use the deflator for personal consumption expenditures (PCE) for deflating hourly pay growth. We instead use the consumer price index, research series (CPI-U-RS). Sherk’s use of the PCE is a reasonable choice—others also prefer the PCE. But it’s awfully hard to call using the CPI a clear mistake. The CPI is used by the IRS to adjust income tax brackets each year, by the Social Security Administration to set the Social Security cost-of-living adjustment, by the Census Bureau to calculate real median family income and the poverty rate each year, and by the Bureau of Labor Statistics (BLS) to calculate real hourly compensation in their productivity series. There are wonky details associated with a choice between the PCE and CPI-U-RS, but it’s just silly to call using one or the other a clear mistake. It seems to us that the CPI is better-targeted at the actual expenditures of typical families. We would prefer to use the chained CPI to get one of the methodological benefits of the PCE without having to import all of the other choices embedded in it, but the chained CPI does not go far enough back in time. We specifically identify the differences in deflators as one of the wedges between growth in a typical workers’ pay and productivity, and compute its contribution to the overall divergence in each time-period and overall. In the linked chart, it’s labeled the “terms of trade” wedge. Sherk claims that this gap is capturing factors besides simply changes in terms of trade, and that’s right. Who knows, maybe we’ll rename this wedge.But whatever we call it, accounting for it does not make the pay-productivity gap go away and we have fully and transparently assessed its empirical importance in our work. We should note as well that none of the growing wedge between productivity and typical workers’ pay that is the result of rising inequality (which is what we highlight and focus on) is affected by the change in deflators. So, adopting the PCE deflator would not shrink the gaps we show that are the result of growing within-compensation inequality or the decline in labor’s share. Instead, changing deflators just shrinks the share of the gap that is accounted for by different price changes in our productivity and pay series, leaving the inequality-driven wedge the exact same size. Which makes sense—changing deflators changes everybody’s hourly pay the same amount, so pay gaps between typical workers and very high-wage workers are going to be preserved.

- Sherk claims we have underestimated the influence of rising non-wage compensation in driving hourly pay growth in a particular way. We’ll take a look at this point for future reports. We should emphasize, however, that the effect of this change even by his own accounting would be exceedingly modest—moving up hourly pay growth for the 1979-2014 period, for example, by about 0.1 percent per year. It would not materially change any of our conclusions.

- Finally, and by far the least important, Sherk’s analysis of trends in industry output per hour worked and pay growth is not illuminating. As we noted before, we really don’t have an empirical dog in the fight over whether or not industry-level productivity and pay are correlated. All that we’re arguing is that: (1) competitive labor market theory says they shouldn’t be, and (2) even if they were, this still would not let you infer anything valid about the productivity of individuals within those industries. But, Sherk shows a scatter-plot of (implicitly) nominal wages and nominal output per hour worked and claims a correlation between productivity and pay at the industry level. His correlation is admittedly surprising to me, but it’s not a correlation between industry productivity and pay. It’s instead a correlation between industry revenue per hour worked and pay. That’s a very different thing and does not tell us anything about a link between productivity and pay at the industry level. If people want to keep flailing away trying to prove an industry-level level link between productivity and pay, that’s fine. But even if one shows up in data that has been properly analyzed, it does nothing at all to change the pay-productivity gap we’ve documented, nor does it prove anything about whether or not the typical American worker “deserved” to see their pay lag far behind productivity growth.

{kind=link}

All in all, though, every point raised in the new report, besides the substitution of average for typical hourly pay rates (ie, choosing to ignore the effect of inequality), is a lot of hand-waving that does not change the underlying empirical fact: hourly pay for a large majority of American workers has not tracked growth in economy-wide productivity for a long time now.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.