Opinion pieces and speeches by EPI staff and associates.

[ THIS PIECE WAS POSTED TO VIEWPOINTS ON JUNE 17, 2004 ]

The Wall Street Journal is wrong on job quality

A June 14 editorial in The Wall Street Journal argues that, contrary to claims by the Economic Policy Institute, wages are booming and the economy is adding mostly high-quality jobs. The Journal editorial, however, is brimming with inaccuracies and misleading numbers.

Error #1: Ignoring inflation

First, and most egregious, the wage numbers it cites are not adjusted for inflation, making them irrelevant as indicators of workers’ living standards. The Journal editorial says, for example, that:

Full-time workers got a 7.7% hike in their average weekly earnings over the last three years. Last month, hourly wages were up by 2.2% year-on-year.

But the most recent consumer price data show that over the past three years (May 2001-May 2004), inflation is up 6.4%, and over the last year (May 2003-May 2004), it’s up 3%. That means that the average worker’s real pay is up not 7.7% but only 1.3% over three years, or 0.4% per year. Over the past year, real wages fell, as 3% inflation outpaced 2.2% wage growth. Only on the editorial pages of the Wall Street Journal could falling real wages be presented as evidence that “the economy is booming.”

Compare those real gains with productivity growth, 14.1% over the past three years (4.5% per year). As Alan Greenspan has stated, “Most of the recent increases in productivity have been reflected in a sharp rise in the pretax profits.” Little has fed into wage growth – and none in the last year.

Error #2: Breaking the law of averages

Overall averages often mask how various groups of workers are faring. For male workers, real median weekly earnings are up a mere 0.4% over the past three years (2001q1-2004q1). Low-wage male workers, those at the 10th percentile, have actually lost ground over the past three years, down a total of 0.8%. Women workers have done much better, with median real earnings growth of 5.3%; 10th percentile women’s earnings are up 2.5%.

Error #3: The wrong yardstick

The Journal editorial also challenges EPI’s analysis that expanding industries pay less than contracting ones. That argument, however, uses the wrong measure to evaluate that question. Yes, the number of jobs is growing again, and some of the new jobs pay above-average wages. But that fact by itself reveals little about the quality of jobs. EPI’s online Jobs Picture analyzing the May jobs release from the BLS noted that:

With a solid job market recovery underway, it is useful to examine the industries that have been growing as a share of total employment and those that have been losing share. Most industries are now adding jobs, but some are doing so at a below-average pace and thus losing ground as a share of total employment. On average, the industries that are expanding as a share of total employment pay lower wages than those that account for a smaller share of the total.

Averaging over the past three months, and comparing this year to last year, industries expanding as a share of total employment pay on average 13% below industries contracting as a share. This is driven largely by the fact that even though industries such as manufacturing, information, and financial services are expanding again, they are growing more slowly than other low-paying sectors, such as hotels, restaurants, and temp jobs. [emphasis added]

Again, the key question is not just whether industries are adding jobs. Thankfully, most are. What’s important is which industries are growing faster or slower than average, i.e., which are growing or contracting as a share of total employment. If high-wage industries are growing faster than the overall average, and thus expanding their share of total employment, this speeds up the growth of average wages, and vice-versa.

Error #4: Misleading by example

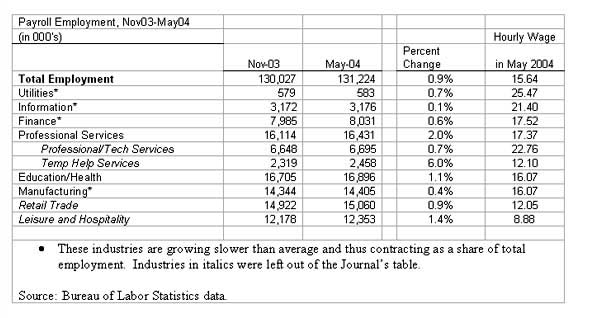

The Journal editorial cites six examples of high wage industries it claims are driving an improvement in job quality. As shown in the table below, however, four of the six industries cited in the editorial are growing slower than average, and thus contracting as a share of total employment. Of the two that are growing faster than average, employment in professional services is growing most quickly, and has a high average wage.

But the Journal’s analysis neglects to mention that it’s the low-end sub-sectors that are driving the growth in professional services. Temp work, with an average hourly wage of $12.10 (well below the overall average of $15.64), expanded as a share of total employment while the higher-paid technical sub-sector (including legal, accounting, architecture, computer systems, and management services), is growing slower than average, and thus contracting as a share of the total.

EPI’s table also includes two industries left out of the Journal’s table, retail trade and leisure (the latter including restaurants and hotels). These low-wage industries are growing either at the same rate or faster than overall payrolls, and are thus partly responsible for the slow growth of average wages.

By reporting only nominal wage gains and ignoring the fact that slower-growing industries can dampen wage growth, the Journal editorial has failed to get the facts straight on the ongoing problem of eroding job quality in the expanding labor market. The fact is that a recession followed by the longest jobless recovery on record has taken a lasting toll on wage growth. This unfortunate dynamic can neither be reversed by a few months of strong job growth, nor by aggressive misreporting of the data.

Jared Bernstein is senior economist at the Economic Policy Institute in Washington, D.C.

[ POSTED TO VIEWPOINTS ON JUNE 17, 2004. ]