How to think about the job-creation potential of green investments: A boost to labor demand that will create some jobs, shift some others—and increase job-quality overall

A key dividing line between competing proposals to address climate change is the role of publicly financed and directed investments.

A recent open letter about policies that should be enacted to slow climate change from a group of prominent economists mentioned only carbon pricing, and, at least implicitly argued against publicly financed and directed investments by asserting that a carbon tax “should …be revenue neutral to avoid debates over the size of government.”

Alternatively, the central organizing principle around the “Green New Deal”—both the congressional resolution as well as the looser collection of ideas associated with the phrase–is that pricing carbon alone is not enough, and that a substantial degree of public planning and investment will be necessary to stop catastrophic climate change.

Here at EPI, we are firmly of the view that a robust package of publicly financed and directed investments should be part of a large portfolio of policies (which includes carbon pricing) for stopping climate change. Not every impediment to undertaking green investments is rooted simply in the too-low price of carbon. Public investments offer a way to cut through the Gordian knot of incentives and inertia that would slow green investments even in the presence of carbon pricing.

Often, calls for public investment to fight climate change are accompanied by promises of millions of new green jobs that will be created. These promises contain a lot of truth, but there are a couple of important things to note about jobs and climate policy.

First, the challenge of moving to an economy that emits far fewer greenhouse gases will be largely met by conservation (including efficiency) and fuel-shifting. This means that meeting the challenge of climate change is not likely to lead to more economic activity in the long-run–in fact it is likely to lead to a bit less activity. This means it is hard to make long-run claims that these efforts will lead, on net, to more jobs economy-wide than a scenario where no greater effort is made to mitigate greenhouse gas emissions.1 To be totally clear here–there is also no reason to think there will be fewer jobs due to efforts to transition to a greener economy, and there might be a small uptick in jobs. But because the effort to mitigate greenhouse emissions will largely be replacing dirty energy production and consumption with clean energy production and consumption, there will likely be only small net effects on employment.

Second, green investments that lead to a job shift instead of net job gains in the long-run may well create net new jobs in the short-run if they are undertaken in an economy that is not running at full employment. So if, for example, the first tranche of public investments in a future Green New Deal came online in an economy either in a recession or characterized by any gap between economy-wide spending and productive capacity, then it will lead to net new job creation. In a sense, this makes a Green New Deal a useful automatic stabilizer—providing a constant baseline of spending in the economy that will not spiral down as other flows of private spending slow or reverse during a recession. Further, this highlights that if there are aspects of Green New Deal investments that can be “moved forward” during times of economic slack, then the benefits from these investments would be even larger.

But, if the first tranche of public investments from a Green New Deal hit an economy characterized by today’s level of economic slack, a good portion of the jobs supported by green investments would likely result from pulling employment out of other sectors rather than creating net new employment. To be clear, I think there’s likely still some slack left in labor markets and some net new jobs could be created (maybe a lot). But, the best case for undertaking these public investments is the progress they’ll make towards a cleaner economy, not the net new jobs they’d be guaranteed to create.2

In a 2014 paper, I sketched out the number and types of jobs that would likely be created by large increases in public investments. One of the scenarios (scenario two in the figure below) I analyzed was a package of “green” public investments that included building retrofits for energy efficiency and large investments in the electricity generation and transmission sector. Another scenario (scenario three in the figure below) considered a package of “core” infrastructure investments, which included transportation infrastructure and water treatment, distribution and sewage systems, as well as investments in other utilities.3 A key figure from the paper is reproduced below, showing the number of jobs supported by a $1 million increase in spending on these public investment scenarios:

Direct and total jobs supported by $1 million in final demand, economy-wide average and under three infrastructure investment scenarios

| Direct jobs | Direct and supplier | |

|---|---|---|

| Economy average | 9.83 | 12.67 |

| Scenario 1 | 6.01 | 10.63 |

| Scenario 2 | 6.52 | 9.65 |

| Scenario 3 | 5.87 | 8.94 |

Note: This chart shows the relative labor intensity of infrastructure investment.

Source: Author’s analysis of data from Employment Requirements Matrix (ERM) data supplied by the Bureau of Labor Statistics

The jobs in the figure include only those directly supported by these investments, or jobs supported in supplier industries. It includes no jobs “induced” a result of greater economy-wide spending. Such “induced” jobs would only occur in economies characterized by lots of productive slack (ie, high unemployment and low rates of business utilization).

The way to interpret these figures is that a package of green investments that included, say, $50 billion in building retrofits and smart-grid investments would support 445,000 jobs ($50 billion times 8.9 jobs per million) and $50 billion in investments in transportation and water systems would support 485,000 jobs ($50 billion times 9.7 jobs per million), for a total of 930,000 jobs. Accommodating these 930,000 jobs would either require a reduction in the unemployment rate of 0.7 percentage point, an increase in the labor force participation rate of 0.4 percentage point, or some combination of both. It’s not inconceivable that the economy has enough slack left to allow this, but it’s a bit unlikely that no job-shift at all would occur from these investments, and instead all jobs would be net new jobs. If all of the new jobs came from reductions in the currently-unemployed, for example, this would leave unemployment at 2.9 percent, a level not seen since the early 1950s.

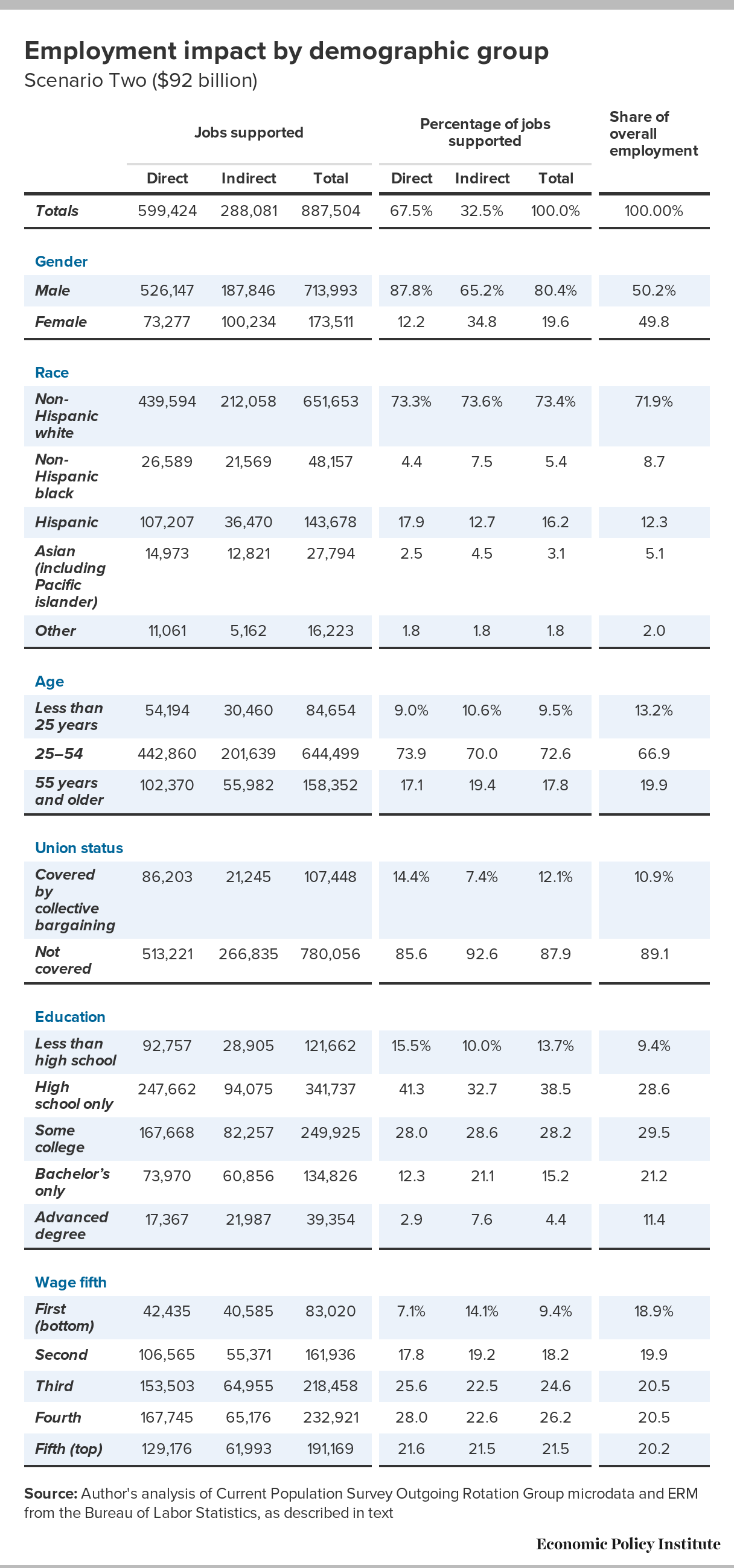

The same paper that generated this figure also showed that jobs supported through public investments were much more likely to be middle-wage and less likely to be low-wage. They were also a bit more likely to be unionized. Complementary policies could help amplify these beneficial outcomes. The jobs supported by public investments also traditionally skew very male, slightly whiter than average, and skew significantly away from black workers. Complementary policies would hence be needed to ensure that jobs created through climate investments were much more open to groups of workers that had traditionally be excluded from them.

{kind=link}

Public investments to help forestall catastrophic climate change are extraordinarily valuable, and policymakers should think hard about how to best incorporate them into an overall climate policy. A valuable knock-on effect of these green investments is the boost they would give to labor demand – particularly for workers without a 4-year college degree. But, as valuable as this boost to labor demand for non-college labor is, it’s not always the case that green investments will create net new jobs, and that does not detract from their value at all.

1. A lower level of economic activity can be consistent with higher levels of employment if productivity (output generated in a given hour of work) declines. And in some sense climate change policies can be thought of as a negative shock to measured productivity, with measured productivity meaning productivity that does not account for the externality of climate emissions (ie, how productivity is measured by statistical agencies today). Essentially climate policy makes actions that are not profitable at prices that do not reflect the greenhouse gas externality (undertaking efficiency investments or switching to clean energy sources) either profitable or mandated. This leads to more labor-intensive activities and can lead to small upward pressure on employment for each given level of economic activity. These effects are highlighted in Bivens (2012), but they are likely to be relatively modest.

2. In the original version of this paragraph, I included these sentences:

“However, even when green investments do not create net new jobs, the jobs that are supported by green investments will almost by definition be better jobs than those they’d displace. After all, it is a voluntary decision when workers leave other sectors to take jobs created by green public investments and presumably they wouldn’t do it if the jobs were worse.”

In retrospect, this was inelegantly written and has caused confusion, hence I deleted these sentences. There are clearly some aspects of the larger agenda to fight climate change that could result in job loss or displacement for workers currently holding good jobs. Think carbon pricing or regulation that leads to layoffs at power plants. The current post and this paragraph specifically are about new publicly financed investments. These investments will, by themselves, generate jobs that are higher wage than economywide averages (I link to a table showing this later in the post) and, by themselves do not displace jobs. In fact, they boost economywide job quality and so would give even those workers displaced from good jobs by other aspects of climate policy a better set of jobs to transition into. Yet, these sentences were too easy to read as arguing that all aspects of climate policy would lead inevitably to better jobs—and that’s not inevitable, it will require conscious complementary policies.

3. While it is true that this 2014 paper did not examine “green” transportation investments, a sad secret of modeling of this type is that it’s nearly impossible to get data fine-grained enough to generate distinct job numbers for traditional versus green transportation investments. Further, the differences in job-intensity between these two types of transportation investments are likely to be quite small, so the current estimates are certainly good for rule-of-thumb assessments of their potential to support jobs.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.