Policy Memo #126

Senators John McCain and Barack Obama have presented very different plans to reform health care in the United States. Last week, the Urban Institute/Brookings Institution Tax Policy Center (TPC) provided what appears to be the first evaluation of each plan’s effect on costs and coverage outcomes.1 While the TPC findings are preliminary, there is a wealth of information contained in them; some of their implications, however, may not be immediately apparent even to those relatively well-versed in the U.S. health care debates. The punch lines of the TPC analysis can be stated relatively simply:

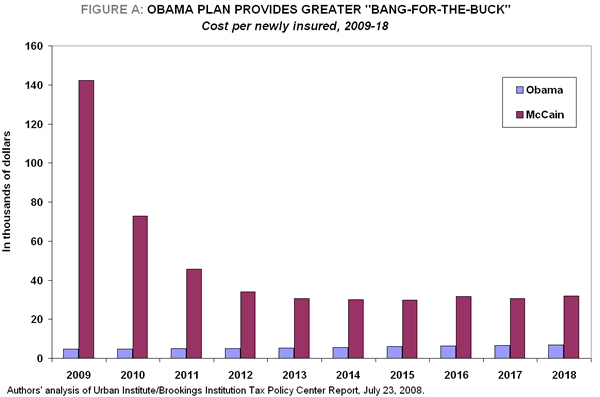

- Efficiency. Over the 10-year period analyzed by the TPC, Senator Obama’s plan provides far greater “bang-for-the-buck,” spending far less per capita for its coverage of the uninsured population (see Figure A below).

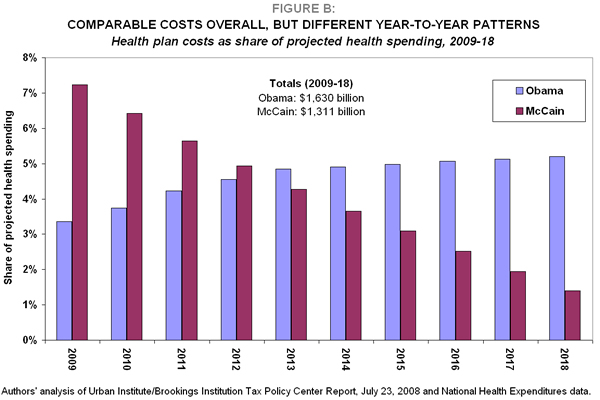

- Cost. The costs of the plans over the 10-year period are in the same ballpark: the Obama plan costs roughly $1.6 trillion, while the McCain plan costs $1.3 trillion (the Obama plan spends roughly 20% more than McCain’s) (see Figure B).

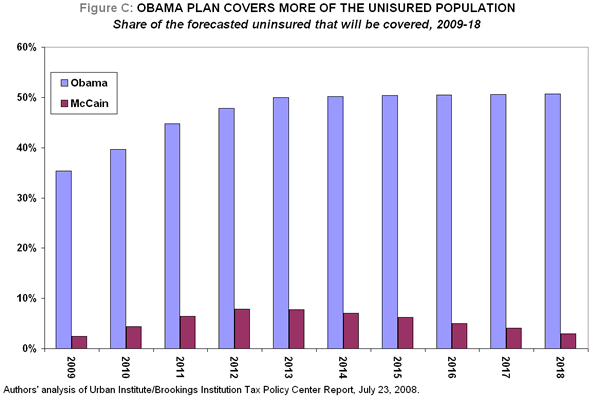

- Coverage. The Obama plan makes a much bigger dent in covering the uninsured population. On average over the 10-year period, the Obama plan covers over 47% of the forecasted uninsured population, while the McCain plan covers less than 5% (see Figure C).

Over the 10-year period, McCain’s plan spends roughly seven times more (per capita) than Obama’s to cover each of the forecasted uninsured, a huge difference in the “bang-for-the-buck” each plan provides in expanding health coverage (Figure A). The difference in outcomes is not particularly surprising, as the two plans are very different in conception.

- Obama’s plan proposes building upon the existing system of employer-sponsored insurance (ESI) and expanding the government’s role in providing insurance for those without access through their employer. This broader federal role includes both an expansion of existing public insurance programs (widening eligibility for Medicaid and the State Children’s Health Insurance Program) as well as the creation of a new federally run insurance pool that will offer coverage (at premiums unaffected by health status) to those who either do not receive ESI or are not eligible for existing public plans. Obama’s plan also provides subsidies to ensure affordability, and largely leaves the present tax treatment of health insurance premiums intact.

- McCain’s plan would eliminate the existing income tax exclusion for health insurance premiums paid through employers and would replace it with a direct, refundable tax credit. This change sets off a cascade of decision-making by firms and employees, the net effect of which would be to erode some of the incentives that employers and employees have to tie health care benefits to job-based compensation and encourage health care purchase through the individual market. It would also provide incentives for people to buy less comprehensive insurance coverage.

Over the 10-year window analyzed by the TPC (2009-18), the Obama plan costs $1.6 trillion, while the McCain plan costs $1.3 trillion. It is unclear from the TPC analysis just how much credit (if any) each candidate’s plan is given for investments in cost-saving technology and other cost-containment strategies.

These overall 10-year costs mask very different expenditure patterns over time. Furthermore, expressing costs in dollar-terms (as the TPC does in its analysis) can seem to inflate the costs of both plans, as all health-related costs in the U.S. economy rise rapidly over time due to faster growth of prices in this sector relative to the rest of the economy.

Given the differences in year-to-year spending patterns and the rapidly rising prices for medical care, Figure B shows each plan’s cost as a share of forecasted national health spending in each year.

- The Obama plan’s costs rise in dollar terms over the full period, but essentially keep pace with national health care spending for most of the 10-year window.

- The McCain plan’s costs start quite a bit higher than Obama’s (spending twice as much in the first year of implementation) and then dwindle. This pattern largely reflects the fact that the value of the tax credit to buy health insurance will erode over time, as the pace of health insurance premium growth exceeds the rate at which the credit will rise. Thus, the value of the tax benefit will eventually be overwhelmed by higher costs for insurance premiums.

Without a policy change, the uninsured population is forecasted by the TPC to increase by 15 million, from roughly 52 million in 2009 to 67 million in 2018 (which also implies a rise in the rate of uninsurance from 17% to 20% over this time period). Given this forecast:

- On average, the McCain plan covers just over 5% of the uninsured population forecast for this time period. After a peak coverage rate of 7.8% in 2012, his plan begins covering a smaller share, falling eventually to less than 3% of the forecast uninsured in 2018.

- On average, the Obama plan covers just over 47% of the forecast uninsured population. The coverage under the Obama plan improves over time, and by 2018, more than half of the uninsured population would be covered.

Changes in sources of coverage

In both plans, net changes in the overall uninsured population are accompanied by substantial shifts in the sources of coverage, both for the forecast uninsured and for those who already have coverage.

Coverage sources and the McCain plan

Under McCain’s plan, the relatively small net effect on the uninsurance rate results from large gross losses in employer-sponsored insurance and large gross gains in the individual market. In fact, roughly 20 million fewer people are projected to have employer-sponsored insurance by 2018 under McCain’s proposal, while the number of people purchasing in the individual market will have grown by a corresponding amount. The reason for this shift is that McCain’s plan changes the incentives for purchasing in the employer market as compared to the individual market. This change will lead to destabilized employer pools and fewer employers offering insurance.

First, some workers–likely those who are young and healthy–will decide to decline their employer’s insurance to seek out plans in the individual market. The remaining workers in the ESI pool will thus have higher average health costs, causing their premiums to rise. When premiums rise, other workers may leave the pool, worsening the problem.

Second, employers may decide to stop offering insurance as it becomes more expensive and less valuable to their entire workforces. Additionally, small employers who were offering insurance to their workers to gain the tax advantage themselves will no longer see a benefit to offering and might stop sponsoring coverage.

Some of the people who lose coverage through their employer will simply lose coverage altogether. The individual market subjects individuals

to the whims of the insurance industry: poor information about policies, discriminatory pricing, coverage waivers, refusal to pay for pre-existing conditions, and denial of policy renewal. To make matters worse, other parts of the McCain plan remove many of the (already insufficient) consumer protections that currently exist in state regulations–such as mental-health parity and “guaranteed issue” (the requirement that insurance companies offer insurance to all comers).2

Coverage sources and the Obama plan

The Obama plan’s large net increase in coverage is the result of small increases in employer-sponsored and public insurance, and large enrollment (almost 30 million) in the new national insurance pool. This pool would offer insurance at “community-rated” prices, that is, prices that do not discriminate based on health status. This large pool would have substantial administrative and marketing cost-savings relative to the existing non-group market, creating potential savings not just for those judged to be bad risks by insurance companies, but for all purchasers who do not currently have access to employer or public programs.

Notes

[1] See Burman, Leonard E., Surachai Khitatrakun, Greg Leiserson, Jeff Rohaly, Eric Toder, Roberton Williams. An Updated Analysis of the 2008 Presidential Candidates’ Tax Plans Urban Institute/Brookings Institution Tax Policy Center, July 23, 2008 (website: http://www.taxpolicycenter.org/UploadedPDF/411741_updated_candidates.pdf uploaded July 23, 2008). It should be noted that while this issue brief draws largely on the Tax Policy Center’s research findings, its interpretations and judgments are solely those of the authors.

[2] See Lewis, Stephanie (2008), “Conservative health reform proposals: Severe consequences for people with pre-existing health conditions”, Center for American Progress Action Fund. http://www.americanprogressaction.org/issues/2008/conservative_health_reform.html