Better pizza, bitter politics

This post originally appeared on Dissent Magazine’s website

By now it’s well known that Papa John’s Pizza CEO John Schnatter is claiming—or threatening—that compliance with the Affordable Care Act would force him to reduce employee hours or raise prices. This was one of a number of post-election “job-creator” tantrums based on the curious belief that President Obama’s re-election (and the continuation of his policies) had somehow changed the political and regulatory landscape.

Schnatter was quickly skewered for his inflated estimation of the ACA’s burden—he claimed it would increase prices 10 to 14 cents—which Forbes calculated to be about one-half of 1 percent of the chain’s operating expenses—or between 3.4 and 4.6 cents per pizza. With Papa John’s charging $1.50 for each extra topping, this is about the cost of a single slice of pepperoni on a large pizza (if we assume a generous portion of 30 pieces of pepperoni per pizza).

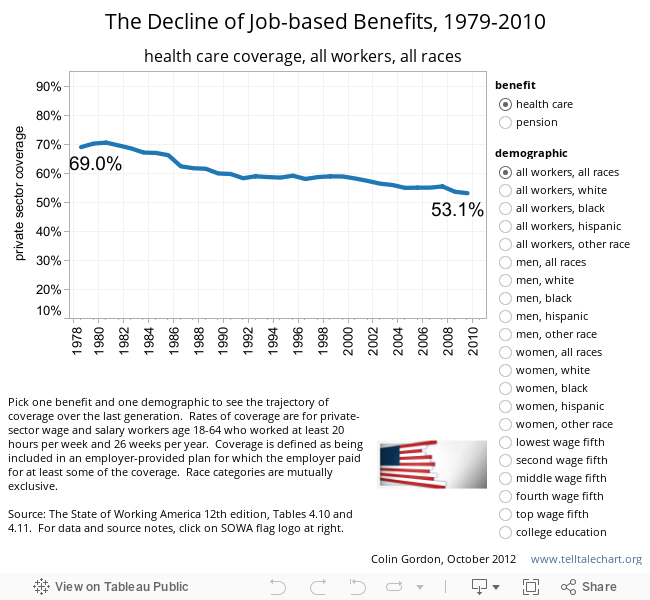

But, more important, in the big picture the best way to think of the ACA is that it is providing a mandate (with admittedly small and not particularly sharp teeth) that deters low-road employers like Papa John’s from continuing to shirk responsibilities to their employees. After World War II, employers routinely championed job-based provision as the best route to health security. But the reach of job-based health insurance coverage, provided by one’s own employer rather than a spouse’s, peaked in the late 1970s at about 70 percent of the workforce. It is now just above 50 percent. Despite its own “better pizza, better benefits” claims, Papa John’s only extends health coverage to about a third of its employees.

The requirement to insure employees is new for many low-wage service firms like Papa John’s. But, in this respect, the ACA simply closes off the ability of these companies to shuffle those costs onto the backs of responsible employers, public programs (Medicaid and the State Children’s Health Insurance Program), or the employees themselves. Papa John’s is losing some of the public subsidy (to which the light corporate tax burden contributes little) that has long sustained its miserable employment standards.

The graph below traces the decline of health care and pension coverage in private-sector employment by gender, race, wage level, and educational attainment, from 1979 to 2010. Health-care coverage has fallen across the board, and the losses are starkest for the most vulnerable workers. Black and Hispanic workers (men especially), low-wage workers, and those with only a high-school education began this era with lower rates of coverage, and they have lost coverage at a faster rate than others. As health-care coverage has slipped, the out-of-pocket costs (premiums, co-payments, deductibles) for enrolled workers have continued to climb.

While the reach of private pensions has declined less dramatically for other groups, and actually inched up for some women, coverage remains sparse—and is getting sparser—for low-wage workers. And again, these numbers understate the damage. As pension coverage has slipped, defined-contribution plans—which expose workers to both investment risks (the poor performance of invested contributions) and longevity risks (the possibility of running out of money in retirement)—have largely displaced traditional defined-benefit plans.

While Schnatter and his ilk would have us believe that big government is crowding out private initiative and imposing burdens on employers, in fact the reverse is true. As “low-road” employers shirk responsibilities to their workers, it is public programs—Social Security, Medicaid, the ACA—that pick up the slack. The security and productivity of their workforce is not threatened by these programs, it is sustained by them.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.