A balanced budget amendment would be extraordinarily dangerous for the economy

The House is set to take up a balanced budget amendment this week, which would limit federal spending in each fiscal year to federal receipts in that year. Putting aside for a moment the chutzpah of House Republicans trying to pass a balanced budget amendment (BBA) just a few months removed from their passage of a $1.5 trillion tax cut that went largely to the richest households and big corporations, the simple fact is that the economic consequences of a balanced budget amendment range from extremely bad to catastrophic. The reason for this is that a BBA would amplify any negative economic shock to the economy and would thereby turn run-of-the-mill recessions into disasters.

When the economy enters a recession, government deficits increase as tax revenues decline and government spending on programs such as unemployment insurance increase. These “automatic stabilizers” are incredibly important as they cushion the blow to the economy from a recession. For example, researchers at Goldman Sachs found that the shock to private sector spending from the bursting of the housing bubble was larger than the shock that led to the Great Depression of the 1930s. Given this larger initial shock, why didn’t we have another Great Depression, with unemployment rates approaching 20 percent and beyond, in 2009–10? The simple reason is that the mechanical increase in the deficit from tax reductions and increased transfer payments absorbed a lot (not enough, but a lot) of this shock, and automatic stabilizers were either non-existent or a lot smaller in the 1930s. Having these programs in place to absorb recessionary shocks is one of the great economic advances of the past 80 years—and getting rid of them by imposing a BBA makes as much sense as outlawing computers or antibiotics. To comply with a BBA as a recession approached, Congress would have to offset any mechanical increase in the deficit by raising taxes or cutting spending. The increased taxes or spending cuts would further drag on the economy, raising the deficit again and requiring still further tax increases or spending cuts. This vicious cycle would amplify the damage to the economy. Essentially this vicious cycle would lead to a large increase in the fiscal multiplier, with each dollar in spending cuts leading to output losses of about $2.50.

The Federal Reserve could try to counteract this drag on the economy by cutting interest rates. But the extent to which they would be able to mitigate the damage may be extremely limited, for a couple of reasons. First, while the Fed can certainly restrain growth by raising interest rates, spurring growth by cutting rates is often ineffective; a dynamic often referred to as rate cuts akin to “pushing on a string.” Further, with current chronic downward pressure on aggregate demand, so-called “secular stagnation,” characterizing the U.S. economy in recent decades, it is likely that the Federal Reserve would be constrained by the zero-lower bound (ZLB) on interest rates—as it was during the Great Recession. Since interest rates cannot be moved (for too long or too far) below zero, when the Federal Reserve hits the ZLB they will be unable to offset any further drag on the economy through conventional monetary policy.

New UN data on international migrants highlights special responsibility for destination countries in the Global Compact for Migration

Large movements of refugees and migrants around the world since 2015, many in response to humanitarian crises, have led to a global negotiation at the United Nations (UN) to create a new Global Compact for Migration (GCM). The GCM will be a non-binding international agreement to establish a new regime for cooperation on international migration that can maximize the benefits of migration and better protect migrants in vulnerable situations. While governments—minus the United States—continue to negotiate the GCM, it’s important to step back and reflect on the lives at stake. The latest UN report and data on migration from the UN Population Division helps by providing a snapshot of migrants around the world. These data can assist policymakers who are currently negotiating the GCM’s substantive provisions, who should remember to take into account their special responsibilities to protect the human rights of all migrants who live and work within their borders.

The UN Population Division reported that there were 258 million international migrants worldwide in 2017, meaning that 3.4 percent of people had been living outside of their country-of-birth for at least one year. The number of international migrants rose by 10 million from 248 million in 2015, but was unchanged as a share of the global population. The number of migrants in 2017 is an increase of 50 percent from 173 million in 2000, rising 0.6 percent from 2.8 percent of the global share of the population in 2000. Almost 75 percent of international migrants are of prime working age, meaning between the ages of 20-64. Men were 52 percent of international migrants in 2017 and women 48 percent.

By continent, Asia hosted 80 million international migrants, Europe 78 million, North America 58 million, Africa 25 million, Latin America 9.5 million, and Oceania 8.4 million. Europe’s population would have declined between 2000 and 2015 had it not been for the arrival of international migrants.

What to Watch on Jobs Day: Multiple measures indicate the presence of labor market slack

I’ve written a lot about wages in recent months. In March, I detailed trends in wages through 2017 in a report, with specific emphasis on growing inequality both across the wage distribution and between black and white workers. My “What to Watch on Jobs Day” blog post last month, as well as my statement on jobs day, tried to put wage growth in perspective by comparing multiple measures of wage growth and showing how many of them fell short of levels that would be needed to confidently declare the economy at full employment. On Friday’s Jobs Day, I will look at wage growth once again, as well as other measures of labor market slack which indicate that the economy has yet to unambiguously reach full employment.

Wage growth is a really important measure of labor market strength, and while slow wage growth is not just an indication that the economy remains below full employment, by definition slow wage growth means there continues to be some slack in the labor market. Slow wage growth tells us that employers continue to hold the cards, and don’t have to offer higher wages to attract workers. In other words, workers have very little leverage to bid up their wages. Slow wage growth is evidence that employers and workers both know there are still workers waiting in the wings ready to take a job, even if they aren’t actively looking for one. But, you say, the unemployment rate is 4.1 percent. Where are these workers waiting in the wings? The focus of this blog post and what I’ll be looking at on Friday (along with wages) are the other measures that similarly indicate there remains a non-trivial amount of slack in the labor market. I’ll argue that we can actually see this “waiting in the wings” in the data in other measurable ways, aside from weak wage growth.

Last week, my colleague Josh Bivens highlighted one underappreciated measure of labor market flows: the share of the newly employed that come from out of the labor force. One might be tempted to believe that the labor force represents a rather static and cleanly-defined group of people: those who have a job or those who don’t but want one and are actively looking for one. If that were the case, then the total labor force wouldn’t fluctuate so much and only the unemployment rate would move up and down at different points in the business cycle. But, the labor force itself ebbs and flows, even relative to the working-age population.

Does high CEO pay matter to shareholders?

Last month, we did an analysis that examined the impact of a provision of the Affordable Care Act limiting the amount of CEO pay that could be deducted from profits to $500,000.

In the years after it took effect, this provision raised the cost of CEO pay to employers (i.e., shareholders) by more than 50 percent. Prior to 2013, shareholders of health insurance companies effectively paid just 65 cents on every dollar of CEO compensation, since their taxes would fall by 35 cents for every dollar they paid out. After 2013, they would be paying 100 cents of every dollar.

If CEO pay bears a close relationship to their value to the company, this change in the tax code should have led to some reduction in their pay. Using a wide variety of specifications, controlling for growth in profits, revenue, stock price, and other relevant factors, we found no evidence that the pay of health insurance CEOs fell at all in response to the limit on deductibility.

While this finding does support the view that CEO pay is not closely related to their value to shareholders, it is worth asking how much this provision mattered to insurers’ bottom line. In other words, how much more did they effectively end up paying to their CEOs, measured as a share of profits, as a result of the change in the tax code?

Evidence shows collective bargaining—especially with the ability to strike—raises teacher pay

Some recent media reports on a new academic study by political scientist Agustina S. Paglayan give the impression that the paper’s findings reflect badly on teachers unions. This is a misreading, however, of the study and of its implications. A key issue lost in the press accounts is that the study is, first and foremost, an historical analysis, examining the effects of the expansion of state collective bargaining rights for teachers between 1959 and 1990. Given the historical focus, the study excludes the experience of the last three decades, where the evidence clearly suggests that collective bargaining raises teachers pay.

But, even with respect to just the historical period studied, the paper’s conclusions are much more nuanced than the press reports suggest. A central conclusion, which has been overlooked in media accounts, is the author’s view that the reason that teachers unions might not have been effective in raising expenditures on education (including teachers’ pay) in the early days of expanding collective bargaining rights is because the laws that allowed collective bargaining often simultaneously restricted the ability of public-sector unions to strike. What the law gave with one hand, it often took back with the other. To illustrate the point, the paper shows that in states where public-sector workers had both the right to collective bargaining and the right to strike, collective bargaining did appear to increase expenditures on education.

More recent evidence on the effect of unions on teacher pay

Any analysis of unionized public-sector teachers’ pay needs to separate out two points of comparison: one is a comparison of teachers’ pay with what similar workers earn in the private sector; the other is a comparison between what unionized and non-unionized teachers earn in the public sector.

A perfect pairing: New tip provisions and a strong minimum wage

Last December, the U.S. Department of Labor (DOL) issued a proposal to allow employers to collect their workers’ tips, ostensibly to distribute them more evenly through tip pools. However, the rule was written in such a way that it would have made it legal for employers to simply pocket tips. This would have been a major windfall to restaurant owners and other employers of tipped workers, out of the pockets of people who work for tips. We estimated that if that rule were finalized, workers would lose $5.8 billion a year in tips, with $4.6 billion of that coming from the pockets of women working in tipped jobs.

Because of the overwhelming outcry from workers and allies in response to the proposal, along with excellent investigative journalism that uncovered the administration’s cover-up of its analysis showing the rule would be terrible for workers, DOL came to the table to hammer out a compromise. As a result, last week’s spending bill included a provision that makes it clear that employers may not keep any tips received by their employees, and ramps up the punishment for violations. Those things are huge wins for workers.

The clear next steps for protecting workers in tipped occupations are eliminating the tip credit for minimum wage employers, enforcing one minimum wage for all workers regardless of whether they receive tips, and substantially increasing the federal minimum wage. The rest of this post explains why these next steps are so crucial.

It is not uncommon for servers in restaurants to voluntarily share a portion of their tips with kitchen staff. A provision in the spending bill passed last week allows employers to operate tip pools between tipped workers and “back-of-the-house” or other non-tipped workers. Under the new rules, employers can operate these pools if they pay their tipped workers a base wage of at least the federal minimum wage, which is currently $7.25—i.e. employers cannot operate a tip pool between tipped and non-tipped workers if they use a tip credit to cover any wages up to $7.25 an hour. Non-tipped workers in tip pools must still be paid a base wage of the full minimum wage in their city or state. And, as always, the total pay of tipped workers (base wage plus tips) must be at least the full minimum wage in their city or state.

The Federal Reserve Bank of New York’s search for a new president was a flawed process that should go back to the drawing board

It is now widely recognized that the president of the Federal Reserve Bank of New York is a uniquely powerful economic policymaking position. More crucially, it’s likely the most important such position that is not chosen by President Trump. Given the poor choices Trump has already made in choosing the leadership of the Fed, it is more important than ever to make a great choice for the NY Fed presidency.

The process so far has not been encouraging. Several on a list of highly qualified and diverse candidates were not contacted by the NY Fed. Worse, the leading candidate in today’s news reports wasn’t even being mentioned a week ago. This is not how a transparent and publicly accountable process should work, and it’s why the Fed needs fundamental reform.

This leading candidate is John Williams, the current president of the San Francisco Fed. Hiring the current leader of another regional Fed bank hardly constitutes out-of-the-box thinking for the NY Fed. Further, while Williams has done valuable economic research, his tenure as a policymaker at the Fed is frankly disappointing. He has consistently underestimated how much lower the unemployment rate could sustainably go. In 2012, he even thought that 6.5 percent might be the lower limit on the unemployment rate. Since then, he has modified his estimates, but he has seemingly not been chastened about making firm before-the-fact predictions about how low unemployment could go before sparking accelerating inflation.

The Federal Open Market Committee (FOMC) has lost some of its leading proponents for testing the lower limits of unemployment, and has gained some members who have been deeply wrong in arguing that unemployment should not be allowed to fall as far and fast as it has in recent years. Shifting John Williams from the San Francisco Fed to the NY Fed does nothing to push back on this drift of the FOMC away from valuing genuine full employment.Read more

Congress is trying to use appropriations expand the H-2B temporary worker program—where migrants are exploitable and have few rights—by 73 percent

The GOP-led Congress is aiming to pass an omnibus appropriations bill to fund the federal government before the current temporary spending bill expires on March 23, 2018. Part of the negotiations include a major effort by legislators in both parties—who are being bombarded by corporate lobbyists in the hospitality, seafood, landscaping, and construction industries—to expand the H-2B temporary migrant worker program. We estimate the proposal would increase the number of H-2B workers that employers can hire in lesser-skilled occupations by at least 73 percent, from 66,000 per year to 114,000.

The H-2B program—like other temporary migrant worker programs—is not a work program that brings immigrants to the United States with equal rights and the option to stay permanently. Instead, it is used by employers carve out a lawless zone in the labor market where migrant workers have few workplace rights in practice, because they arrive indebted to labor recruiters and indentured to U.S. employers.

Nevertheless, rather than focusing on the most urgent immigration issues at hand, including a path to citizenship for immigrants who are in danger of becoming undocumented, like DACA recipients, and those who have Temporary Protected Status, Congress is instead focusing on making changes to temporary worker programs via the appropriations process. Congress has done this a number of times in recent years, something that Republican Senate Judiciary Chairman Sen. Chuck Grassley and Democratic Ranking Member Sen. Diane Feinstein came together last year to criticize for usurping the committee’s jurisdiction over immigration legislation. Other Senators have done the same, including Dick Durbin and Bernie Sanders. The New York Times editorial page and migrant worker advocates alike have also criticized this end-around the normal legislative process.

Using the H-2A guestworker program for year-round agricultural jobs would lower wages for farmworkers

The H-2A guestworker program provides an unlimited number of temporary work visas to agricultural employers to hire farmworkers from abroad to fill temporary or seasonal jobs lasting for less than one year. Last year, over 200,000 H-2A jobs were certified by the U.S. Department of Labor (DOL)—the most ever—despite the many abuses and exploitation that continues to occur at the hands of employers and labor recruiters. Members of Congress are currently negotiating and debating the fiscal 2018 omnibus appropriations bill to fund the federal government, and hope to pass it before the current temporary spending bill expires on March 23, 2018. On the table is a proposal to allow employers to use the H-2A program to fill year-round, permanent jobs in agriculture with H-2A workers who have few rights and no path to permanence and citizenship. It was first proposed in July 2017 by Rep. Dan Newhouse (R-WA) but never became law.

We have already explained why making H-2A year-round via appropriations is a bad idea, but one other major consequence that Congress should consider is that it will result in allowing agricultural employers to pay much lower wages to H-2A workers in year-round jobs than they pay to the Americans and immigrants who are currently employed in those jobs.

Making H-2A year-round would expand the scope of H-2A by allowing employers offering year-round employment on dairy, livestock, and poultry and egg farms, as well as in nurseries and greenhouses and other non-seasonal agricultural occupations, to hire H-2A workers—bringing H-2A workers into sectors that offer approximately 260,000 year-round full-time equivalent (FTE) jobs. Table 1 lists some of the main year-round agricultural industries in major agricultural states, accounting for 123,000 of the 260,000 full-time equivalent jobs, and shows how much farmworkers earned annually, on average in 2016 in those occupations (according to the Quarterly Census on Employment and Wages, from DOL).

Preemption laws prevent cities from acting on everything from labor and employment to gun safety

On Valentine’s Day, a 19 year-old with a legally purchased AR-15 assault rifle stormed into Marjory Stoneman Douglas High School in Parkland, Florida and murdered 14 students, and 3 educators. In Florida, an AR-15 military-style assault rifle is easier to buy than a handgun. Understandably, many of the students who survived the mass shooting and the families of the 17 victims have called for a change in the law, arguing that it shouldn’t be so easy to legally purchase weapons that powerful. I write here not to weigh in on the merits of any given gun law, but to comment on the process of advocating for legislative change, and the challenges at the local level with the preemption laws on the books.

In terms of advocating for a change in federal law, Congress’s ban on AR-15s and other semiautomatic assault weapons expired in 2004, and federal lawmakers have not been able to pass a similar ban since.

In terms of advocating for change in state law, dozens of Florida high school students recently loaded onto buses and drove to the Florida state capital to lobby for a bill banning assault rifles, which was voted down by the state’s House of Representatives.

In terms of advocating for a change in gun laws at the city and county level, the students, families of the victims, or anyone else won’t even have a chance because of Florida’s preemption law. “Preemption” in this context refers to a situation in which a state law is enacted to block a local ordinance from taking effect—or dismantle an existing ordinance.

What to Watch on Jobs Day: Putting wage growth in perspective

While payroll employment growth has continued to be more than fast enough to absorb working age population growth as well as workers idled by slack demand in previous years and the unemployment rate is holding at 4.1 percent, other economic indicators such as the labor force participation rate, the prime-age employment-to-population ratio, and wage growth resemble an economy with a fair amount of remaining slack. My attention this jobs day and in the discussion below is wage growth.

Last week, I released a paper on the State of American Wages in 2017, with comparisons to earlier periods as well as analysis by gender, race, and educational attainment. Key findings include a pickup in wages for the lowest wage workers over the last couple of years due in part to more workers finally feeling the effects of the growing economy in their wages plus state-level minimum wage increases occurring in states where about half of all workers reside. On the downsides, much of the 2000s and 2010s have been characterized by growing wage inequality and slow or stagnant wages for many. Black-white wage gaps have worsened over the 17-year period and the bottom 50 percent of college degreed workers have lower wages today than in 2000.

Tomorrow, the latest wage growth numbers from the Current Employment Statistics (CES) will come out. The paper I just referenced primarily examined the wage data found in the Current Population Survey Outgoing Rotation Group (CPS-ORG), which allows wage comparisons across the wage distribution and by demographic characteristics. For a read on the labor market and an assessment about whether wage growth reflects an economy at full employment, it’s important to look at nominal wage growth. What’s clear from both surveys, using different metrics (median versus average and total private versus production/non-supervisory) is that nominal wage growth is still below levels consistent with the Federal Reserve’s inflation target and with estimates of potential productivity growth—a sign that the economy still has considerable slack.

Congress should set the standard in being a good employer

The past year has provided countless examples of the ways in which our nation’s labor and employment laws fail workers. From the #MeToo social media campaign that helped expose that for many women sexual harassment is a daily fact of life in the workplace to a recent report revealing that the vast majority (74 percent) of Uber and Lyft drivers earn less than the minimum wage in their state, it is clear that American workers need policymakers to act to reform the current system of worker protections. That is why stories like the one in Vox today that some congressional lawmakers require unpaid interns to sign broad nondisclosure agreements that may discourage them from speaking out if they experience harassment or encounter other workplace issues are so troubling. How can we expect our elected representatives to legislate effective worker protection measures when they themselves adopt exploitative employment practices?

Congress has a long history of exempting itself from workplace protection measures. When the Fair Labor Standards Act was passed, Congress exempted itself from coverage. When the Civil Rights Act, including Title VII which protected workers from employment discrimination on the basis of race, color, religion, sex, or national origin, was signed into law, Congress again exempted itself from these protections. It was not until 1995 that Congress passed the Congressional Accountability Act, finally extending workplace protections to congressional staff. However, recent reports of congressional settlements surrounding harassment claims have shown that Congress is not holding itself accountable for workplace protections.

Many of the policy recommendations from the Kerner Commission remain relevant 50 years later

In 1967, young black men rioted in over 150 cities, often spurred by overly aggressive policing, not unlike the provocations of recent disturbances. The worst in 1967 were in Newark, after police beat a taxi driver for having a revoked permit, and Detroit, after 82 party-goers were arrested at a peaceful celebration for returning Vietnam War veterans, held at an unlicensed social club.

President Lyndon Johnson appointed a commission to investigate. Chaired by Illinois Governor Otto Kerner (New York City’s mayor John Lindsay was vice-chair), it issued its report 50 years ago today. Publicly available, it was a best-seller, indicting racial discrimination in housing, employment, health care, policing, education, and social services, and attributing the riots to pent-up frustration in low-income black neighborhoods. Residents’ lack of Fambition or effort did not cause these conditions: rather, “[w]hite institutions created [the ghetto], white institutions maintain it, and white society condones it… [and is] essentially responsible for the explosive mixture which has been accumulating in our cities since the end of World War II.”

The report warned that continued racial segregation and discrimination would engender “two societies, one black, one white—separate and unequal.” So little has changed since 1968 that the report remains worth reading as a near-contemporary description of racial inequality.

Of course, not everything about race relations is unchanged. Perhaps most dramatic has been growth of the black middle class, integrated into mainstream corporate leadership, politics, universities, and professions. We’re still far from equality—affirmative action remains a necessity—but such progress was unimaginable in 1968. Today, 23 percent of young adult African Americans have bachelor’s degrees, still considerably below whites’ 42 percent but more than double the black rate 50 years ago.

In the mid-1960s, I assisted in a study of Chicago’s power elite. We identified some 4,000 policymaking positions in the non-financial corporate sector. Not one was held by an African American. The only black executives were at banks and insurance companies serving black neighborhoods. Today, any large corporation would face condemnation, perhaps litigation, if no African American had achieved executive responsibility.

How new Fed Chair Jerome Powell should get ready for the next recession

New Federal Reserve Chair Jerome Powell testified before Congress this week, roughly a month after replacing Janet Yellen. The key question many have is whether or not a change in personnel will mark a break with past policy. If it does, and if the Fed starts crediting arguments for raising interest rates that they correctly rejected before, then today’s low unemployment rate might be unfortunately short-lived.

Under Yellen’s leadership, the Fed was notably “dovish” in that it strove to keep monetary policy expansionary with the goal of pushing unemployment down, rather than contractionary in the service of guarding against an outbreak of inflation. Her replacement, Jerome Powell, served on the Fed’s Board of Governors with Yellen between 2012 and early 2018. Powell was by most accounts supportive of the policy path blazed by Yellen, so in that sense a radical change in the Fed’s stance would be surprising. But Yellen wasn’t just a dovish vote on the Fed, she was an intellectual leader in the defense of expansionary monetary policy over the past decade. As a highly respected academic macroeconomist and policymaker, Yellen had the ability and confidence to push back hard on weak arguments about why the Fed should reverse course and begin worrying about containing inflation rather than pushing down unemployment.

One of these weak arguments is that the Fed needs to raise rates faster and sooner so that when the next recession hits, there will be enough “room” to lower them. Proponents of this argument point out that in previous recessions the Fed lowered the short-term “policy” interest rates that it controls by 3–5 percentage points in an effort to restart growth. Today these rates are at 1.5 percent, and, they really can’t go much below zero for any extended period of time. This “zero lower bound” (ZLB) on interest rates is driven by the fact that once these rates hit zero, wealth-holders will just stop demanding bonds and will be happy to hold cash instead. This means that further Fed purchases of bonds to lower rates will have no effect. What hitting the ZLB means for policy is that we could enter the next recession without the ability of the Fed to lower policy rates as far as they have in the past.

While the constraints put on monetary policymaking by the ZLB are real, raising rates now to clear out room for cutting them later remains a silly idea. First, raising rates sooner and further doesn’t just give the Fed more interest rate “room” to fight the next recession, it also makes the next recession more likely. Post-war recessions have largely occurred because of asset market bubbles popping or the Fed raising rates too far and too fast.

An analogy might help point out the absurdity of this. Say that your house is a cool 50 degrees and you hike the thermostat to your desired temperature of 70 degrees. After the heat has been running for a while, the house has warmed to 60 degrees, and your roommate argues you should turn the thermostat off because if the room gets really cold again, you’ll want “room” to warm it by cranking the thermostat up again.

Does this make sense? Of course not. So long as one believes that the economy has not warmed up to its optimal setting, then one should not be using policy tools to cool it back down. Is there a convenient summary measure that can guide us as to whether or not the economy is running hot enough? There are lots, actually, but let’s use the Fed’s own announced measure: 2 percent price inflation. The economy has been running beneath this 2 percent inflation target for years now, and there is little evidence of any acceleration. Further, if one excludes rental prices, then inflation has been even lower. Fighting rent inflation (which occurs due to low supply of housing units relative to demand) by raising interest rates which will curtail home-building would be perverse.

{kind=link}

So, the economy is by the Fed’s own definition not running hot enough, yet they’ve already begun raising rates to cool it off, backed in part by arguments that this is necessary because one day they might want to try to heat it back up. This is a terrible way to prepare for the next recession.

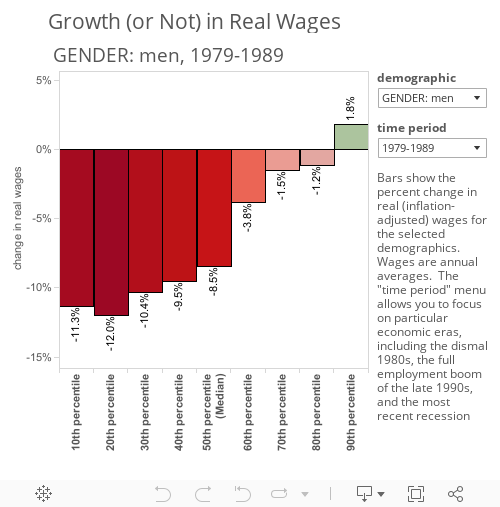

Growth (or not) in real wages

There is no starker metric for our unequal age than the stagnation of American wages over the last generation. Since 1973, productivity has grown about 75 percent, while the compensation of the typical worker has grown only about 12 percent. Since 1979, the hourly median wage has grown less than 10 percent in real dollars, or an average annual raise of barely 4 cents. While wages grew for many workers in 2017, wage growth is still far slower—and more unequal—than where it needs to be.

The interactive graphic below shows the change in real (inflation-adjusted) wages by wage decile, with drop-down filters for gender, race, educational attainment, and time period. This affords comparison of the wage gains (or losses) experienced by particular workers, and comparison across the full 1979–2017 span, or its constituent business cycles. The choice of “African-American” and “1979–1989,” for example, charts how black workers fared during the dismal 1980s; the choice of “BA or higher” and “2009–2017” charts how well-educated workers fared during the long recovery from the Great Recession.

There are a lot of moving pieces here—including shifting economic opportunities, changes in educational attainment, policy drifts and shifts, and five recessions that swallow up almost 6 of the 39 years since 1979. But here are four key takeaways:

Ron Blackwell (1946–2018)

Ron Blackwell, a friend to EPI since its early days, died on February 25.

Ron had a long career in the labor movement, starting with the Amalgamated Clothing and Textile Workers Union in New York, moving to the AFL-CIO in Washington, D.C. until he retired in 2012.

Raised in Alabama, he was a steadfast defender of the rights of working people and a life-long enemy of economic injustice in its many forms.

He pioneered in the design and management of campaigns to use the financial and pension assets of labor unions as a tool of organizing and collective bargaining.

Having studied economics and political economy at the New School, he understood how elite decisions hidden from the public can destroy efforts by ordinary people to better their lives. His was a relentless voice urging the labor movement to demand a seat at the table of economic policy. He also played an important role in efforts to create international labor solidarity in a world of globalizing capital.

Above all, Ron Blackwell was the rare man of principle who actually had the courage of his convictions. As a young man, he chose to go to prison rather than submit to those who were waging the unjust and terrible war in Vietnam. In his years as a labor advocate, he was quick to spot hypocrisy among political leaders, who—as the late mineworkers’ leader John L. Lewis once put it—“supped at labor’s table and sheltered in labor’s house” but then, “cursed with equal impartiality both labor and its adversaries.”

Ron told it like it was.

EPI, the labor movement, and the country have lost a valiant warrior in the struggle for justice.

50 years after the riots: Continued economic inequality for African Americans

Anniversaries of major events are nearly irresistible opportunities to reflect on the past, often with the hope that there has been some progress. So it is this year, 50 years after the Kerner Commission Report on Civil Disorders found systemic inequality and racial discrimination to be at the root of riots across America.

In a new report, Janelle Jones, John Schmitt and I present statistics showing what life was like for African Americans in this country 50 years ago compared to now. That document is a straightforward, unfiltered presentation of the facts, covering a wide range of economic, social, and health outcomes. In the spirit of reflection, I want to use this blog post to focus on racial economic inequality in the labor market, which directly affects approximately 20 million African Americans who get up every day and either go to work or go to find work.

The bottom line is simple. Despite decades of policies, programs, protests and outstanding achievements by African American men and women in many aspects of American life, race far too often remains a deciding factor in the economic status of African Americans relative to whites.

Great strides have been made toward raising educational attainment among African Americans and closing the education gap relative to whites, especially with regard to completing high school. In 1968, just over half (54.4 percent) of African American adults age 25-29 were high school graduates, compared to nearly three-quarters (75.0 percent) of whites. In 2016, 92.3 percent of African American adults age 25-29 were high school graduates with 22.8 percent having gone on to complete a bachelor’s degree or higher (up from 9.1 percent in 1968). Among whites, 95.6 percent are high school graduates and 42.1 percent have a bachelor’s degree or higher (up from 16.2 percent in 1968).

Sen. Hatch’s H-1B bill and other guestworker proposals should be kept out of Senate immigration debate

In the context of this week’s immigration debate in the Senate, Republican Senators will push for the reforms in the Secure and Succeed Act of 2018, which reflect the White House’s policy priorities for immigration. It’s likely, however, that one or more Senators will try to attach legislation to increase the number of temporary migrant workers who lack adequate wage and worker protections onto any bill that emerges. The thrust of any guestworker proposals that may arise will be to widen the essentially lawless zone in the labor market that has been carved out by the proliferation of temporary work visa programs, which put American and permanent immigrant workers into competition with temporary migrants who are denied all opportunity to bargain meaningfully for higher wages. This week’s debate in the Senate should prioritize providing a path to citizenship for DREAMers, not opportunistically expanding the share of workers in America who are not protected by labor standards.

As the Los Angeles Times recently suggested, there may be an attempt to include a bill from Sen. Orrin Hatch (R-Utah) that would triple the number of college-educated temporary migrant workers who are employed in the H-1B visa program—a flawed guestworker program used mainly to outsource jobs in information technology and send high-tech jobs offshore. Hatch’s bill is known as I-Squared, and although Hatch is trying to sell it as an increase in “merit-based” immigration, it is primarily an attempt to increase the number of temporary migrant workers the tech industry can hire at low wages.

There is no question in anyone’s mind that the United States will always need to attract the best and brightest workers from abroad, and many employers claim the H-1B visas is a tool to achieve that. But any migrant workers who enter the U.S. labor market must do so with equal rights, fair pay, and a quick path to permanent residence and citizenship that the worker controls—not the employer. Unfortunately, the H-1B guestworker program fails to meet any of those requirements. Hatch’s I-Squared bill would exacerbate the problems the H-1B program creates by vastly increasing the number of H-1B workers while failing to fix the three main problems with the H-1B program: first, employers are allowed to legally underpay H-1B workers compared to similarly situated U.S. workers; second, employers do not have to recruit U.S. workers before hiring H-1B workers, allowing them to ignore the U.S. workforce altogether; and third, the H-1B program allows employers to replace U.S. workers with much lower-paid H-1B workers—a deplorable practice that has occurred far too many times—and the laid-off workers are often forced to train their own H-1B replacements as a condition of their severance pay.

Senate must pass legislation this week to legalize DREAMers but avoid unnecessary immigration enforcement measures and green card reductions

Spurred on by President Trump’s ending of the Deferred Action for Childhood Arrivals (DACA) initiative in September 2017, on Monday the Senate began an “open-ended” debate on immigration, which is set to only last for this week. The debate is centered around possible legislation to legalize and provide a path to citizenship for the up to 1.8 million unauthorized immigrants who entered the United States as minors, known as DREAMers, including the 700,000 current recipients of DACA. Without the protection of DACA or new legislation, DACA recipients will be left without the ability to attend college or work legally, leaving them unable to access labor and employment law protections because they’ll fear deportation. Passing a bill that legalizes DACA recipients and DREAMers is an urgent priority that Congress should focus on, but the debate will unfortunately spend far too much time this week on adding new immigration enforcement measures and cutting the number of permanent immigrant visas (also known as “green cards”).

The White House and some Republican senators have made it clear that in return for DREAMer legalization, they’d like a large expansion in immigration enforcement and cuts to the number of immigrants that can become permanent residents and American citizens in the future. It is obvious to any rational observer that President Trump intentionally created a crisis for DREAMers by ending DACA as a way to achieve these immigration policy goals—which reflect the misguided and draconian priorities of his administration and Republicans on the hard-right—in exchange for ending the crisis Trump created. Both Republican Senators Tom Cotton (R-Ariz.) and Majority Leader Mitch McConnell (R-Ky.) have expressed their support for Iowa Senator Chuck Grassley’s Secure and Succeed Act of 2018—which is based on the White House’s proposed framework for an immigration deal that includes DREAMer legalization—and both believe it’s the only piece of legislation that can become law. Other Republican Senators who have co-sponsored the Secure and Succeed legislation include Joni Ernst (R-Iowa), John Cornyn (R-Texas), Thom Tillis (R-N.C.), David Perdue (R-Ga.), and James Lankford (R-Okla.).

The Trump administration’s infrastructure plan remains empty talk and will be paid for by cuts to programs that help working people

The Trump administration has released another variation of their long-dormant infrastructure plan. Just like the previous version, the plan amounts to empty talk. To understand why, one must examine the fiscal year 2019 budget proposal, released alongside their infrastructure proposal. While the administration trumpets an infrastructure plan, their budget radically cuts federal investments.

Even their trumpeting of the stand-alone infrastructure plan is hugely misleading. Instead of the $1 trillion being claimed by the administration (already pared back from the $1.5 trillion they claimed they’d be investing in infrastructure in earlier discussions), the plan only calls for $200 billion in federal funds. Finding the rest of the $1 trillion will be left overwhelmingly to states and localities, despite the fact that they already bear the brunt of paying for public infrastructure spending. In total, state and local governments account for 77 percent of public infrastructure spending in the United States. They account for 62 percent of capital investment and 88 percent of operations and maintenance. It is odd to argue that the United States needs a substantial infrastructure push to deal with past underinvestment, and then to propose that the same system that yielded this underinvestment—relying too much on state and local governments—should just be continued. If we want a real investment in infrastructure, continuing to kick the problem to state and local governments won’t solve anything.

The Trump administration will claim that their plans are different because they will leverage the private sector. This claim doesn’t change anything. Private entities will not build infrastructure for free, but will expect a return on investment. That means state and local governments will have to pay for the infrastructure with taxes, tolls, or other user fees. And if state and local governments predictably dodge the task of financing and funding projects directly, public-private partnerships come with their own set of problems, as natural monopoly characteristics can leave the private partner in a position to hike tolls and degrade service quality.

No, the stock market isn’t throwing a tantrum because the economy is “overstimulated”

Conventional wisdom is firming up quickly around the story that recent stock price declines are a result of the market realizing (in proper Wile E. Coyote fashion) that the economy has overheated. This conclusion is far too premature and ignores plenty of contrary evidence.

The story goes that the 2.9 percent year-over-year wage growth in last Friday’s jobs report is a signal that a tsunami of inflation is heading our way. This would force the Fed to step in and stop the inflationary wave by sharply hiking interest rates. Higher interest rates, in turn, can depress stock prices both by restraining overall growth and by attracting people towards buying bonds rather than stocks. The fiscal stimulus provided by the Tax Cuts and Jobs Act (TCJA) and new higher spending caps is thought to add fuel to an already raging economic fire (side note: the TCJA is expensive in budgetary terms, but is so inefficient as fiscal stimulus that its effect is very easy to overstate).

People have gotten way ahead of the facts on this. Yes, the unemployment rate is low, but it’s certainly been this low or lower for a longer span of time without the economy overheating. In 1999 and 2000, the unemployment rate averaged 4.1 percent for two years (and sat below 4 percent for five months), and core inflation nudged up for sure but never broke 2 percent (and the Fed had not even specified a 2 percent target in those years).

{kind=link}

Increased U.S. trade deficit in 2017 illustrates dangers of ignoring the overvalued dollar

The U.S. Census Bureau reported that the annual U.S. trade deficit in goods and services increased from $504.8 billion to $566.1 billion from 2016 to 2017, an increase of $61.2 billion (12.1 percent). The rapid growth of the overall U.S. trade deficit reflects the failure of Trump administration trade policies to materially affect trade flows in its first year, and its failure to address currency misalignment and prolonged overvaluation of the U.S. dollar.

The U.S. goods trade deficit increased from $752.5 billion in 2016 to $810.0 billion in 2017, an increase of $57.5 billion (7.6 percent). The U.S. goods trade deficit is dominated by the trade deficit in manufactured products (including re-exports), which increased from $648.7 billion in 2016 to $699.8 in 2017, an increase of $51.1 billion (7.9 percent). Rapidly growing trade deficits in manufactured goods are a threat to future employment in this sector, which remains a large employer despite decades of policy-inflicted decline.

The U.S. trade deficit with China reached a new record of $375.2 billion in 2017, up from $347 billion in 2016, an increase of $28.2 billion (8.1 percent). China is a particular source of concern in trade in steel and aluminum, industries in which that country has accumulated massive amounts of subsidized, and often state-owned excess production capacity, over the past two decades. The president needs to promptly take trade action in pending national security investigations in these sectors.

The remainder of the goods trade deficit is composed of trade in petroleum and other energy products, and miscellaneous transactions. The United States also had a small trade surplus in agricultural commodities, which reached $22.1 billion (including re-exports) in 2017. The U.S. surplus in services trade declined from $247.7 billion in 2016 to $244.0 billion in 2017, a decline of $3.7 billion (1.5 percent).

EPI responds to Amazon’s claims that their fulfillment centers raise local employment

Last week, Janelle Jones and I released a new study showing that opening an Amazon fulfillment center does not actually boost overall employment in the county where it opens. Analyzing data for counties in 19 states containing Amazon fulfillment centers, we found that within two years, the opening of such a facility leads to a 30 percent increase in warehouse and storage employment in the surrounding county. However, this does not lead to an increase in overall employment in the county.

In response to our study, Amazon circulated a comment arguing that “Amazon’s investments led to the creation of 200,000 additional non-Amazon jobs” and “counties that have received Amazon investment have seen the unemployment rate drop by 4.8 percentage points on average.”

Both of these claims are misleading. First, although it’s true that unemployment fell during the economic recovery in places that Amazon opened fulfillment centers, unemployment also fell substantially in places without an Amazon presence at all. Nationally, over 2010–2016, unemployment fell by 4.7 percentage points—essentially the same as the 4.8 percentage point fall Amazon touts—even though most areas of the country did not have an Amazon warehouse. Amazon is simply riding the tide of the national economic recovery. Unlike the analysis that Amazon presented, our study actually accounts for employment changes that are happening regardless of Amazon during the recession and recovery, by controlling for national, regional, and state-specific employment shocks.

The bottom line on Trump and the economy: We’re not in good hands

If you follow the news, it’s hard to avoid the constant claims that President Trump has made, taking credit for a strong economy. This claim raises a bunch of questions, but a tl;dr assessment of the Trump economy in 2018 is pretty simple: It’s good, but not great. The Trump administration deserves zero credit for its pockets of strength. And everything they’ve done on economic policy indicates that they will be terrible macroeconomic managers, and will bungle any challenge that comes their way in the next few years.

The longer version of this is below.

The economy going into 2018: Good, but not great

By almost any measure, the economy today is stronger than it has been in a decade. But that’s a really low bar! This decade began with the worst economic crisis since the Great Depression, and the economy’s growth has been severely hamstrung ever since. After eight-and-a-half years of steady recovery, the unemployment rate today sits at 4.1 percent, lower even than its pre-Great Recession level. This is unambiguously good news. But other measures of health in the job market tell a bit less-rosy story.

For example, the share of “prime-age” adults (between the ages of 25 and 54) with a job remains below its pre-Great Recession peak even after years of improvement. We would need to add millions more jobs to push it back to levels it reached in the not-so-distant past of the early 2000s. Wage growth also remains distressingly weak, and this wage weakness has blunted the incentive for employers to make productivity-enhancing investments. After all, there’s not much point in spending money to economize on labor costs when workers are cheap and easy to find.

{kind=link}

{kind=link}

Why economics tells us that crediting the TCJA for wage increases is just PR

After the passage of the GOP Tax Cuts and Jobs Act (TCJA) in December, multiple companies announced decisions to give out bonuses or raise wages for workers and claimed that these decisions were driven by the corporate tax cuts embedded in the TCJA. Since proponents of the tax bill sold it to the public based on claims that corporate rate cuts would trickle down to typical workers, it’s no surprise those proponents would point to these companies’ announcements and claim vindication for their claims. And far too much reporting took the claims of corporations at face value, though some recent exceptions stand out as being much better at evaluating those claims.

While we’re not surprised by the cynicism of these corporate claims, that doesn’t change the fact that there is absolutely no economic evidence to think they’re true. What these companies are doing amounts to nothing more than PR. As we’ll detail, immediately handing out bonuses and raises is simply not how the economic theory that links corporate tax cuts to wage growth works. And we aren’t the only ones pointing this out. Companies are engaged in a clear campaign to gin up support for unpopular corporate tax cuts by crediting each new check they write to those tax cuts.

We’ve spent plenty of time detailing why we think corporate tax cuts won’t actually end up raising wages in the real-world, but even the theory that links corporate tax cuts to wages looks nothing like the campaign corporations are currently engaged in.

Here’s how that economic theory actually works: Corporate tax cuts increase the after-tax returns to owning capital like stocks and bonds. These higher after-tax returns induce households to save more. Higher after-tax profitability incentivizes firms to invest more and the new savings needed to finance these investments come from increased household savings in response to higher returns. The resulting investments in plant and equipment give workers better tools with which to do their jobs, and this boosts productivity (how much income or output is generated in an average hour of work). In turn, these increases in productivity are seamlessly translated into across-the-board wage growth.

The Trump administration’s attempt to dismantle the fiduciary rule: A year in review

February 3, 2018 marks one year since President Trump issued a Presidential Memorandum to “review” the fiduciary rule. This was just two weeks into his administration, a clear signal that undermining this common sense rule is a top priority for the administration.

If fully implemented, the fiduciary rule would require that financial professionals presenting themselves as investment advisers act in their clients’ best interests. The rule is needed because “conflicted” advice leads to lower investment returns, causing real losses for workers saving for retirement—an estimated $17 billion a year—for the clients who are victimized. The rule would prohibit common practices such as steering clients toward investments that pay the adviser a commission but provide the client a lower rate of return. It was exhaustively researched by the Department of Labor and debated over several years, survived several court challenges, and was completed in 2016. It was supposed to be implemented on April 10, 2017.

However, unscrupulous players in the financial industry are working to kill the rule so they can continue fleecing retirement savers—and the Trump administration is doing everything it can to help them out. Here’s the rundown of the fiduciary rule shenanigans from Trump’s first year:

February 3, 2017: President Trump issues a Presidential Memorandum ordering the Labor Department to needlessly reexamine the fiduciary rule.

UN Secretary General’s report on migration highlights the need for government action and cooperation, but lacks key guidance on labor migration

The United Nations Secretary General (UNSG) released a report in January 2018 titled Making migration work for all, that laid out four “considerations” to guide governments negotiating a Global Compact for Migration, an agreement to promote more “safe, orderly, and regular” international migration. The four considerations focus on how to maximize migration’s benefits, increase labor migration, address the legitimate security concerns of unauthorized migration, and address issues arising as a result of mixed flows of migrants and refugees.

The report is aimed primarily at governments that are major destination countries for migrants, urging them to open doors wider to legal migrant workers, protect migrant workers during recruitment and employment abroad, and during their return to their home countries or re-integration there, and to offer protection to vulnerable migrants who are not refugees but nevertheless require some form of protection.

While the report offers many thoughtful and useful recommendations, there are no priorities among the long list of “shoulds” and no analysis of the trade-offs between competing recommendations. For example, is there competition or are there trade-offs that must be balanced between opening doors wider to migrant workers and protecting the rights and labor standards of local, destination country workers? Can both be done while ensuring that migrant workers are fully protected?

What to Watch on Jobs Day: How the Trump administration stacks up against an economy on autopilot

Friday marks the first full year of Bureau of Labor Statistics Employment Situation reports since the beginning of the Trump administration. Put simply, overall economic growth and the labor market are healthier today than they’ve been in years, and President Trump and his supporters have been quick to claim credit for this relative health. These are ridiculous claims. An analogy might help. A person’s health is a function of many variables: genetics, diet, exercise, and environmental factors, for example. Eventually, of course, almost everyone will at some point in their life need access to quality medical care to remain healthy. But, noting that somebody is healthy at a given point in time says nothing about whether their doctor is competent or not. The Trump administration was handed an economy and a labor market whose health had improved radically (if too slowly) over the preceding eight years, and which was trending steadily in an even better direction. Macroeconomic trends tend to have lots of momentum, so we shouldn’t be shocked that this recovery has continued. But nothing the Trump administration has done has boosted its trajectory.

Friday’s jobs report will give us an opportunity to look at the last year in the context of what we would have expected from an economy that was completely on autopilot, just moving along its preexisting trajectory.

EPI’s Autopilot Economy Tracker focuses on four key measures: the unemployment rate, the prime-age employment-to-population ratio, wage growth, and payroll employment growth. Here I’ll take each in turn—I’ll look again on Friday to see what story the newest data tell.

Providing unpaid leave was only the first step; 25 years after the Family and Medical Leave Act, more workers need paid leave

February 5, 2018 marks the 25th anniversary of the Family and Medical Leave Act (FMLA), which allows eligible employees to take up to 12 weeks of unpaid, job-protected leave within a calendar year for a serious health condition, the birth of a child or to care for a newly born, adopted, or foster child, or to care for an immediate family member with a serious health condition. While it’s important to celebrate this important milestone, stopping there on the national level has been a huge mistake. Because eligibility is limited based on size of firm, work hours, and tenure at job, the FMLA only provides access to an estimated 56 percent of the workforce. But the largest loophole in the FMLA is that it is unpaid, so many workers who would want to take advantage of it to care for themselves or a family member, simply cannot afford to.

Only 13 percent of private-sector workers have access to any paid family leave, which means that 87 percent do not. Due to this widespread lack of paid family leave, workers have to make difficult choices between their careers and their caregiving responsibilities precisely when they need their paychecks the most, such as following the birth of a child or when they or a loved one falls ill. This lack of choice can often lead workers to not take any leave or cut their leave short; about 45 percent of FMLA-eligible workers did not take leave because they could not afford unpaid leave and among workers who took time off for caregiving responsibilities, about one-third of leave-takers cut their time off short due to cover lost wages.

The distribution of workers with paid family leave is skewed toward higher-wage workers. As shown in the figure below, workers in the top 10 percent of the wage distribution are six times more likely to have paid family and medical leave to care for themselves or a family member when coping with a serious health condition or to care for a new child in their family than workers in the bottom 10 percent. This bears repeating: only 4 percent of the lowest-wage workers have access to paid family leave. The disparities are stark, but even among the highest paid workers, only about one-fourth have paid family leave.

Year one of the Trump administration: Normalizing itself by working for the top 1 percent

Tomorrow, President Trump is set to deliver his first State of the Union speech, in which he will likely provide a triumphalist account of the economic policy changes made during the first year of his presidency. But despite big talk on the campaign trail about how he would stand up for the forgotten working man (for Trump, it was always men who were left behind), the first year of the Trump presidency has been no triumph for typical American workers. Instead the big winners over the past year have been the already rich.

This really shouldn’t come as a surprise. Trump’s was crystal clear in his inaugural address about who he considers the cause of American workers’ disempowerment: foreigners. This diagnosis is stunning not just in how wrong and bigoted it is, but how cynically it attempts to distract from the privileged group that really was reaping gains that should have been broadly shared—the top 1 percent and their enablers. His agenda of continuing the upward redistribution of income to this top 1 percent while scapegoating immigrants and allegedly nefarious foreign governments is essentially the orthodoxy among the Republican Congressional majority, and it will do nothing to help America’s workers.

The cynicism is clearest when considering the signature piece of legislation signed by Trump, the Tax Cuts and Jobs Act (TCJA). The TCJA provides a number of temporary tax cuts to households, most of which will accrue to those at the top of the income distribution. But it saves its permanent tax cuts for the nation’s corporations, whose profits eventually flow overwhelmingly to the richest households in America. By 2027, when the household tax cuts have expired but the corporate tax cuts remain, the top 1 percent will see 83 percent of the gains from the TCJA. Corporations have been so giddy about the windfall they’ve reaped from the TCJA that they’ve mounted an absurdly transparent public relations campaign on its behalf, claiming that every bonus and wage increase they have bestowed since its passage was somehow the result of it—even those that occurred before the TCJA actually took effect. This is, needless to say, not how economics argues that tax cuts can potentially boost wages. It’s also important to note that in any given year about half of all workers see raises, and nearly 40 percent receive bonuses. In short, it is extremely likely that not a single worker who wasn’t a high-placed CEO or corporate manager has seen a raise because of the TCJA. And if they got a bonus this year because of the TCJA, it was a likely a one-time attempt by their employer to sneak in a deductible expense before the tax cuts made these deductions less profitable, and no future TCJA-linked bonuses will be seen again.