An evidence-based Fed would hold rates steady in September

The Federal Open Market Committee (FOMC) meets today and tomorrow to determine whether or not to raise interest rates. The FOMC has raised rates three times since December 2016. The evidence arguing that these increases were wise or necessary was thin at best. That rationale for raising interest rates is to rein economic growth that threatens to drive down unemployment so low that workers will be empowered to achieve unsustainably large wage increases. The worry is that such wage increases could push price inflation over the Fed’s target rate.

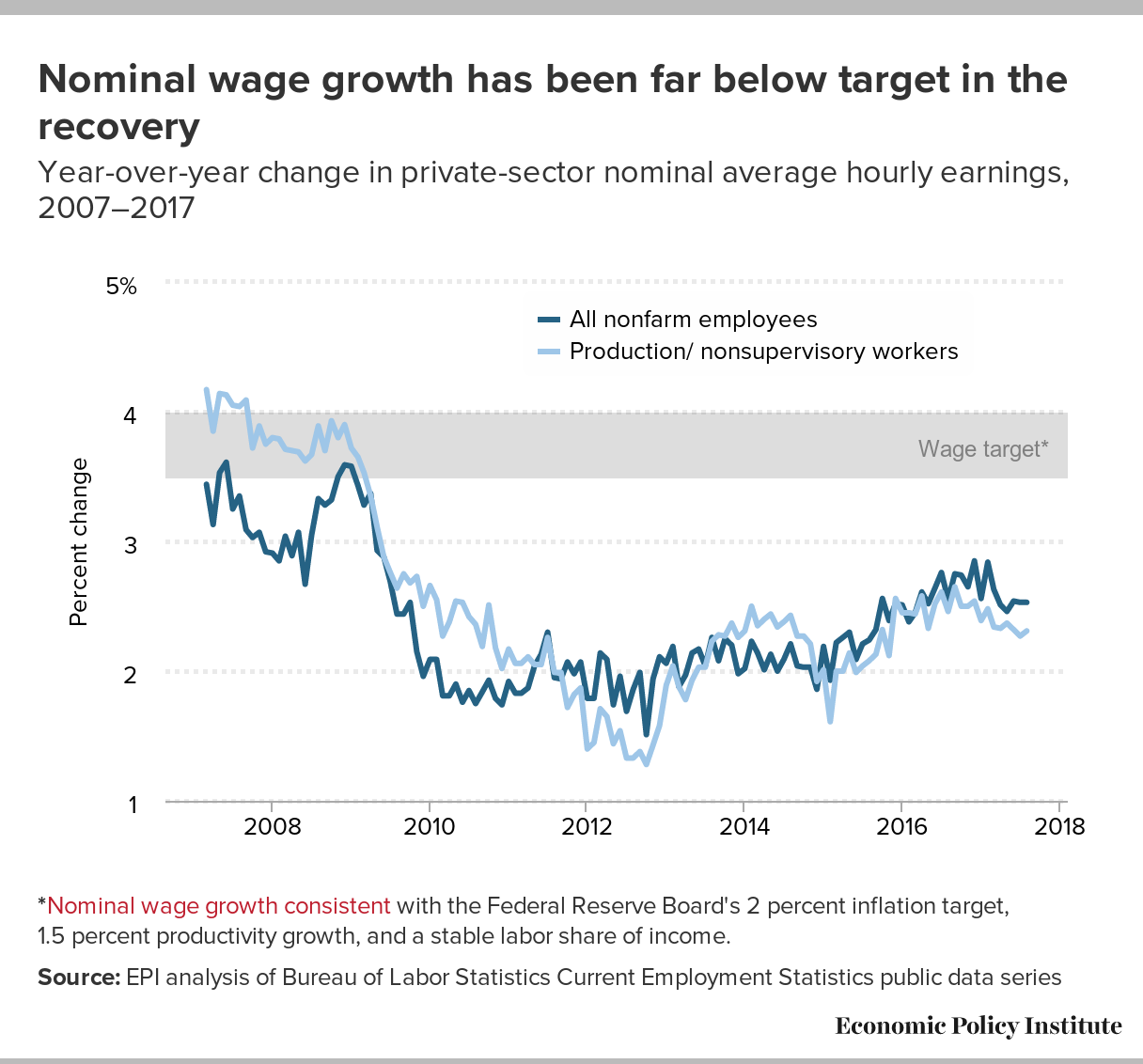

But the real-world data that exists on every link of this causal chain shows that such worries are baseless. Economic growth in recent quarters is depressingly slow, not fast. Unemployment rates are in the low-end of historical experience, but have been lower (without wage or price inflation) several times in recent years. Other measures of labor market slack show the economy is far from recovered. Wage growth shows little sign of accelerating to levels that would spark wage-price spirals.

{kind=link}

{kind=link}

The rate increase that happened in June was particularly dispiriting for those hoping the Fed would continue to follow the evidence-based approach largely adhered to under the reign of Janet Yellen as Fed Chair. The economic data going into that meeting gave plenty of reasons why a data-dependent Fed might worry that it was riskier to raise rates too high too soon than to stand pat for a couple of months. Yet the Fed raised rates.

Data since June has been much softer. The Fed’s preferred inflation measure has decelerated significantly, and any upward creep of wage growth has stopped. There just is no case for continuing to raise rates in the face of this data.

{kind=link}

While the outcome of any single FOMC meeting is not crucial for the American middle class, what this week’s meeting signals for the commitment of the Fed to genuine full employment is crucial. History has shown that low and middle-wage workers in the United States only get consistent annual wage increases when the economy is near genuine full employment. For example, for two solid years in 1999 and 2000 the unemployment rate averaged 4.1 percent and spent a number of months below 4 percent. And the late 1990s are the only time in recent economic history when wage growth was strong across the wage scale.

When the unemployment rate was held above estimates of how low it could go without generating inflation for a decade and a half between 1979 and 1995, a wage growth disaster for American workers resulted, with inflation-adjusted wages falling for the bottom 80 percent of workers.

Last week saw the release of Census Bureau data on incomes and earnings for 2016. The data confirmed that 2016 was a good year for most American households, with median income rising 3.2 percent, following an excellent year in 2015 as well. This data tells us that typical American families are finally getting a taste of real economic recovery. Yet the data on prices and wages tells us there is even more room to boost the economy, lower unemployment, and continue trying to push up their wages.

The Fed should be greedy in trying to provide American families this economic boost. And they should be evidence-based in keeping rates low until genuine, durable evidence of accelerating inflation shows up in the data. Both of these things argue strongly for the Fed keeping rates unchanged on Wednesday. An increase will be a deep disappointment and a sign that the Fed has diverged fully from its evidence-based approach. Holding steady will be a win for both rational policymaking and for American families’ economic prospects for the rest of the year.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.